- Beauty & Personal Care

- Lip Powder Market

Lip Powder Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Lip Powder Market by Form (Palettes and Pens), By End-user (Up to 30 Age Group, Under 18 Age Group, and Up to 45 Age Group), Sales Channel (Beauty Stores, Specialty Outlets, Convenience Stores, E-Retailers, and Other Sales Channels), and Regional Analysis for 2026 - 2033

Lip Powder Market Size and Trends Analysis

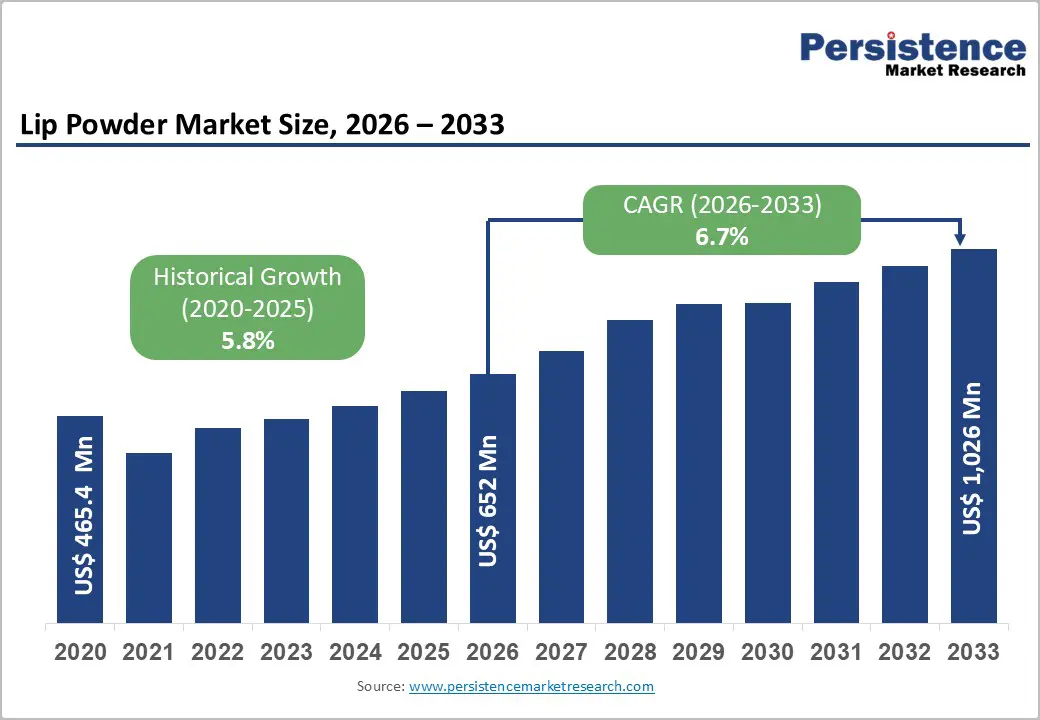

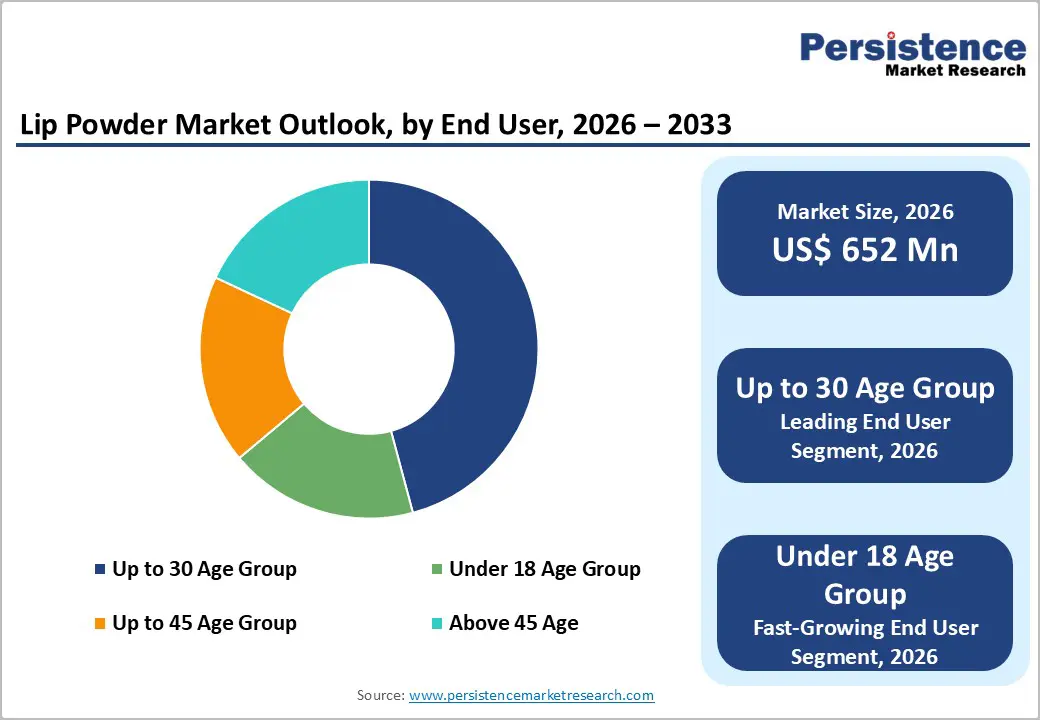

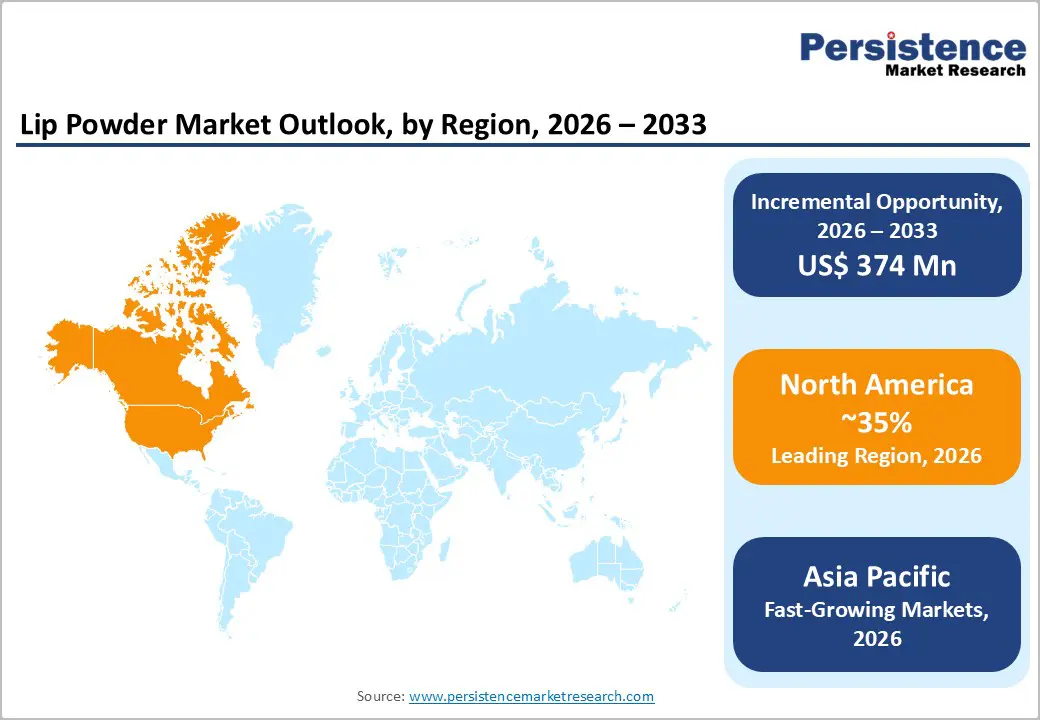

The global lip powder market size is likely to be valued at US$ 651.9 million in 2026 and is projected to reach US$ 1,025.9 million by 2033, growing at a CAGR of 6.7% during the forecast period (2026-2033). Lip powder is a finely milled, pigmented formula prepared by ingredients such as silicones, binding agents, and moisture-activated polymers. The lip powder market demonstrates sustained expansion driven by evolving consumer preferences for long-lasting, lightweight lip cosmetics and the proliferation of e-commerce distribution channels. Rising consumer awareness regarding natural and organic beauty formulations, combined with increased disposable income among younger demographics, particularly in Asia Pacific regions, underpins market momentum.

The segment benefits from technological advancements in cosmetic formulation, delivering enhanced pigmentation, improved wear-time, and diverse application methods. Market accessibility through digital platforms has fundamentally transformed consumer purchasing behaviors, enabling brands to reach previously untapped markets while offering personalized beauty solutions through customizable product formats.

Key Industry Highlights:

- Dominance of Form: Lip powder palettes maintain market dominance with 55%+ revenue share, while pen formats represent fastest-growing segment with 7.1%+ CAGR, reflecting emerging consumer preference for simplified application and portability

- End-user Analysis: Consumers aged 18-30 years command 40%+ market share with the fastest growth occurring within the under-18 age cohort (8-9% CAGR), indicating substantial long-term demographic tailwinds

- Regional Analysis: Asia Pacific region contributes 40%+ of global market value with 6.8-7.2% projected growth, driven by emerging market opportunity in India, Indonesia, and Vietnam; North America maintains 30%+ revenue share with mature market characteristics

- By Sales channel Analysis: E-commerce channels demonstrate 6.6-7.1% growth trajectories, substantially exceeding traditional retail expansion, with digital channels capturing 35-40% of developed market sales volume; specialty outlets represent the fastest-growing distribution channel

- Strategic market developments include accelerated DTC expansion by multinational corporations, emerging brand consolidation through acquisition activity, and product innovation focusing on clean beauty and sustainability integration, establishing competitive differentiation themes through 2033

| Key Insights | Details |

|---|---|

|

Lip Powder Market Size (2026E) |

US$ 652 Mn |

|

Market Value Forecast (2033F) |

US$ 1,026 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Dynamics

Drivers - Rising Demand for Matte, Long-Lasting Lip Colors

The shift toward matte lip finishes and long-wearing formulations represents a significant market catalyst, with matte lip powder products accounting for substantial revenue growth across beauty retailers globally. Contemporary consumer preferences increasingly favor shine-free, smudge-proof lip cosmetics that deliver intense pigmentation without frequent reapplication, directly addressing professional and lifestyle needs across demographic segments. Market research indicates that 70%+ of lip powder consumers prioritize wear-time and finish quality over traditional lipstick formats. This preference trend correlates with social media influence and beauty content creators who systematically promote matte lip aesthetics across platforms like Instagram and TikTok, driving aspirational purchasing behavior among Gen-Z and millennial consumers.

The technical advancement in long-wear polymers and silicone-based formulations has enabled manufacturers to deliver superior adhesion, moisture retention, and color stability, reducing application frequency and enhancing perceived product value. Regional markets, including North America and Europe, demonstrate the highest penetration of matte lip powder formats, with estimated market share contribution exceeding 45% of form-based segmentation, validating the sustained demand for performance-driven lip cosmetics across developed markets.

Restraint - Toxicity Concerns and Regulatory Compliance Complexity

Growing scientific evidence identifying heavy metals, including lead, cadmium, and arsenic in cosmetic formulations, has generated heightened consumer health consciousness and regulatory scrutiny across global markets. Published research documenting elevated lead concentrations in commercial lip products has prompted increased consumer preference for lead-free and organically formulated alternatives, directly constraining market expansion for conventional lip powder products lacking third-party testing certification. Regulatory bodies, including the FDA, European Commission, and emerging market authorities, have implemented stringent compliance requirements, extending product development timelines and increasing formulation costs. Approximately 15-20% of consumer survey respondents cite health and safety concerns as primary decision factors, creating material market segmentation between premium, certified products and conventional offerings. Non-compliance penalties and potential product recalls impose significant financial liabilities for manufacturers, disproportionately impacting smaller regional competitors lacking centralized quality assurance infrastructure. This restraint particularly constrains growth in price-sensitive market segments where cost pressures limit investment in advanced testing and certification protocols.

Opportunity - Natural, Organic, and Sustainable Product Innovation

The accelerating consumer migration toward clean beauty and sustainability-focused formulations represents a substantial whitespace opportunity with an estimated 3-4 year advantage window for first-mover brands establishing category leadership. Market research indicates 60%+ of consumers actively consider environmental and ingredient transparency when evaluating cosmetic purchases, with premium pricing capacity for certified organic and cruelty-free products.

Opportunity sizing suggests the organic lip powder subsegment could achieve 8-10% CAGR through 2033, materially exceeding conventional product growth rates. Brands investing in clean formulation innovation, sustainable packaging materials, and transparent supply chain documentation have demonstrated pricing power and customer loyalty premium exceeding 25-30% versus conventional competitors. Secondary benefits include reduced regulatory risk and enhanced brand positioning within aspirational consumer demographics, supporting long-term competitive differentiation and margin expansion.

Category-wise Analysis

Product Type Insights

Palettes dominate the global lip powder market with over 55% revenue share, driven by their versatility, portability, and ability to offer multiple shades within a single compact format. Consumers value the creative flexibility palettes provide, enabling customized blends, diverse finishes, and experimentation without purchasing multiple standalone products. Premium palette collections also command significantly higher price points, typically US$ 35–65 per unit, compared to US$ 12–25 for single-shade formats, reinforcing their role as value-enhancing, long-term beauty investments rather than simple consumables. Leading brands such as MAC, Huda Beauty, and Revlon continue to strengthen category leadership through innovation cycles, seasonal editions, and curated color stories. Regionally, palettes show the strongest acceptance in North America and Western Europe, where higher spending power and mature beauty routines sustain demand for premium multi-shade offerings.

Lip powder pens represent the fastest-growing segment, expanding at 7.1%+ CAGR, significantly outpacing palette growth. Their rising popularity stems from an intuitive, precise application that reduces skill barriers and appeals to beginners. Social media demonstrations highlighting ease of use and travel-friendly design amplify adoption among younger consumers. Advantages such as built-in applicators, reduced packaging waste, and premium aesthetic support higher pricing and wider retail penetration. Brands such as Essence Cosmetics and By Terry Paris have gained strong traction, with the Asia Pacific and Latin American markets offering substantial future expansion potential.

End-user Insights

The up to 30 age group remains the dominant segment, contributing over 40% of total revenue, driven by heightened beauty consciousness, strong social media influence, and growing independent purchasing power among millennials and Gen Z. This cohort shows the highest adoption of product innovations, strong willingness to try new formats, and deep engagement with digital marketing, enabling brands to achieve superior marketing efficiency with youth-focused positioning. Rising income levels among employed young consumers have increased spending on premium and specialized cosmetics compared to previous generations. Their strong preference for sustainable, clean, and ethically aligned beauty products reinforces brand loyalty and supports premium pricing. With projections indicating this group will maintain over 45% of market value throughout the forecast period, it remains a core strategic focus for digital-first and experience-driven brand strategies.

The under-18 segment represents the fastest-growing category, expanding at an estimated 8–9% CAGR. Earlier age-of-first-use trends and high exposure to beauty content on TikTok and YouTube accelerate awareness and trial. Increasing self-expression needs, participation in social occasions, and rising discretionary spending further support adoption. Although currently accounting for 10–12% of market value, this cohort offers significant long-term growth potential as early brand engagement builds strong lifetime customer value.

Sales Channel Insights

Beauty stores remain the dominant sales channel in the lip powder market, accounting for more than 35% of total revenue. Retailers such as Sephora, Ulta, and regional beauty chains continue to lead due to their curated assortments, access to professional consultations, and premium in-store experiences. These outlets play a crucial role in product discovery by allowing consumers to test shades, compare textures, and receive expert application guidance, significantly improving purchase confidence and conversion. Their premium positioning also enables higher price realization and larger basket sizes, supporting stronger profitability even if volumes remain lower than mass-market channels. Ongoing international expansion of beauty store networks, particularly across the Asia Pacific, is expected to sustain growth at approximately 5.5–6.0% annually through 2033. Strategic partnerships, exclusive launches, and loyalty programs further strengthen channel performance.

Specialty outlets represent the fastest-growing channel, with an estimated CAGR of 6.8–7.2%. This includes brand-owned boutiques, dedicated cosmetic stores, and lifestyle retailers. Their growth is driven by rising direct-to-consumer preferences and the ability of brands to control merchandising, margins, and experiential retail formats. Leading DTC players such as Huda Beauty and MAC Pro continue to gain share through immersive retail concepts, while expansion into underpenetrated Asia Pacific and Latin American markets is accelerating channel momentum.

Regional Insights and Trends

North America Leads Lip Powder Market with Premiumization and Strong Digital Growth

North America accounts for over 35% of the global lip powder market revenue, with the United States serving as the largest and most mature market characterized by strong premiumization trends and deep category penetration. The region benefits from advanced beauty retail networks, high disposable incomes, and a well-developed e-commerce ecosystem that enables diversified product offerings and faster innovation cycles. In 2026, the U.S. market is expected to have a steady 6.2% CAGR through 2033, driven by rising consumer sophistication, preference for premium textures, and strong digital marketing adoption.

Demand continues to strengthen as beauty consciousness increases and consumers seek performance-driven, clean, and texture-enhancing lip formats. A stable regulatory environment supported by FDA oversight and ISO-aligned manufacturing frameworks reinforces product quality, enabling brands to command premium prices and maintain strong consumer trust. The competitive landscape features global leaders such as L’Oréal and Estée Lauder alongside niche indie brands, fostering continuous innovation.

North America also leads in digital engagement, with online platforms accounting for over 40% of sales. Influencer-led content across YouTube and Instagram strengthens product visibility, while high loyalty-program participation supports repeat purchases and long-term margin opportunities. Strategic M&A and vibrant DTC brand growth further elevate innovation intensity in the region through 2033.

Asia Pacific Emerges as Fastest-Growing Beauty Market Driven by Youth and Digital Expansion

Asia Pacific has emerged as the fastest-growing regional market, with a projected 8.3% CAGR in the forecast period. Growth momentum is driven by rising disposable income, expanding e-commerce infrastructure, and a strong demographic youth advantage, with emerging economies such as India, Indonesia, and Vietnam recording double-digit expansion. China remains the region’s largest market, generating an estimated US$150–170 million in 2026, supported by the rapid adoption of social commerce, live-streaming retail formats, and strengthening domestic brands. India exhibits the highest growth trajectory at 8–9% CAGR, fueled by middle-class expansion and increasing cosmetics adoption among younger female consumers. Japan shows moderate but steady expansion at 6-7%, while ASEAN markets, including Indonesia, the Philippines, and Thailand, demonstrate 7-8% growth profiles.

Fundamental demand is reinforced by a youthful demographic base (median age below 30 across many markets), rising female purchasing power, and strong digital retail penetration through platforms such as Alibaba, JD.com, and regional marketplaces enabling national distribution. Regulatory harmonization under the ASEAN Cosmetics Directive, China’s easing of import requirements, and India’s evolving framework collectively improve market access. Competitive intensity continues to rise as global brands (L'Oréal, Estée Lauder, Shiseido) expand investments, while domestic brands like Lakme, Maybelline India, and emerging Chinese labels gain share through culturally aligned innovation.

Competitive Landscape

The global Lip Powder market demonstrates a moderately consolidated structure with significant competitive diversity, enabling multiple success strategies. The market exhibits characteristics of medium-concentration markets, with the top 5-8 brands controlling approximately 40-50% of total revenue, while the remaining market share is distributed among 50+ specialized and regional competitors. This structure contrasts with highly consolidated consumer product markets, providing substantial opportunity for specialized competitors with differentiated value propositions.

Leading market participants include established heritage brands (Sitka Gear, KUIU, Carhartt, Browning, Cabela's, Columbia Sportswear), specialty-focused manufacturers (Kryptek, Mossy Oak, ScentLok), and emerging direct-to-consumer brands capturing incremental market share through digital innovation and targeted positioning. The competitive positioning spectrum ranges from low-cost mass-market providers competing on affordability to premium-positioned heritage brands emphasizing craftsmanship, performance, and innovation. Market fragmentation reflects diverse consumer segments with varying priorities, including price sensitivity, performance requirements, aesthetic preferences, and values-based positioning around sustainability and conservation.

Key Industry Developments

- In 2022, L’Oréal unveiled Beauty Genius, a virtual personal beauty assistant available 24/7 via smartphone. It’s an AI and Gen-AI powered solution designed to provide a simple, safe and easy way to ask and learn anything about beauty.

Companies Covered in Lip Powder Market

- L'Oréal S.A

- Maybelline LLC

- MAC Cosmetics

- NARS Cosmetics

- Stellar Beauty

- Urban Decay Cosmetics

- NYX PROFESSIONAL MAKEUP

- BUXOM Cosmetics

- Clinique Laboratories, LLC

- Revlon, Inc

- Other Market Players

Frequently Asked Questions

The lip powder market is estimated to be valued at US$ 652 Mn in 2026.

The key demand driver for the Lip Powder market is rising beauty consciousness and growing preference for lightweight, long-lasting, innovative lip textures among young consumers.

In 2026, the North America is likely to dominate with an exceeding 35% revenue share in the global Lip Powder market.

Among end-users, Up to 30 Age Group have the highest preference, capturing beyond 40% of the market revenue share in 2026, surpassing other end-users.

L'Oréal S.A, Maybelline LLC, MAC Cosmetics, NARS Cosmetics, Stellar Beauty, and Urban Decay Cosmetics are a few leading players in the Lip Powder market.