- Food Ingredients & Additives

- Lecithin and Phospholipids Market

Lecithin and Phospholipids Market Size, Share, and Growth Forecast, 2025 - 2032

Lecithin and Phospholipids Market by Source Type (Soy, Sunflower, Rapeseed & Canola, Egg, Others), Form Type (Fluid, De-oiled, Modified), Application Type (Food & Beverages, Bakery Products, Convenience Foods, Confectioneries, Feed, Others), and Regional Analysis for 2025 - 2032

Lecithin and Phospholipids Market Size and Trends Analysis

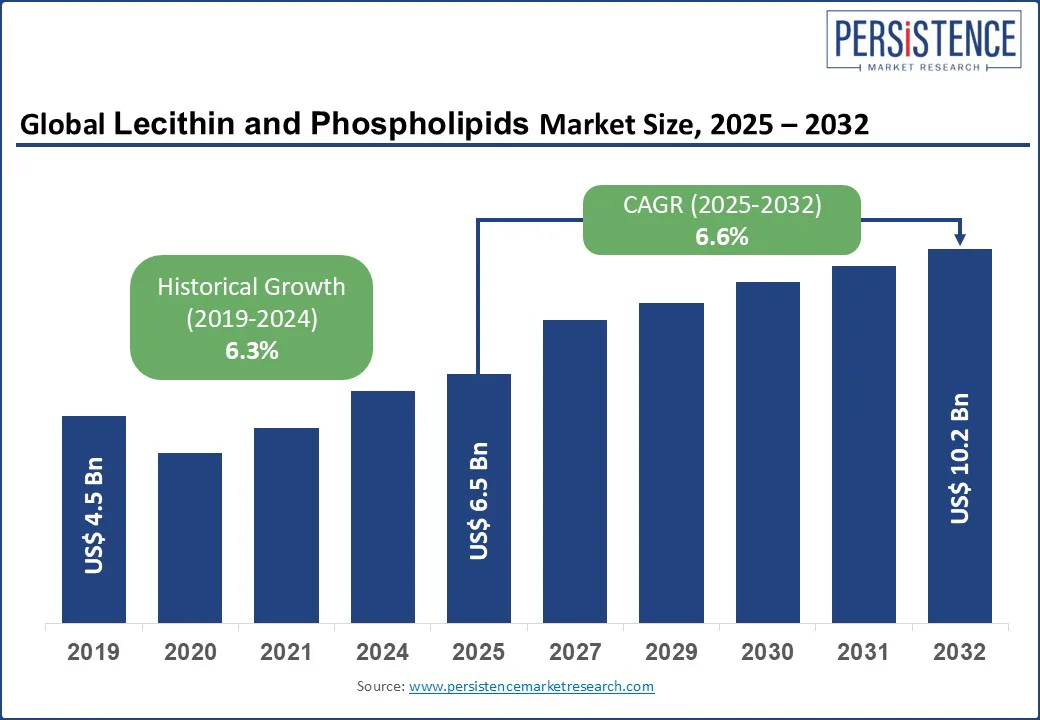

The global Lecithin and Phospholipids Market size is likely to be valued at US$ 6.5 Bn in 2025 and is expected to reach US$ 10.2 Bn by 2032, registering a CAGR of 6.6% during the forecast period 2025 - 2032.

The market has experienced steady growth, driven by increasing demand for natural emulsifiers, rising health consciousness, and expanding applications in food, feed, and pharmaceutical industries. Lecithin and phospholipids, derived from sources such as soy, sunflower, and egg, are valued for their emulsifying, stabilizing, and nutritional properties.

The Lecithin and Phospholipids market is propelled by the growing popularity of clean-label products, urbanization, and advancements in processing technologies, catering to diverse consumer needs across multiple sectors.

Key Industry Highlights:

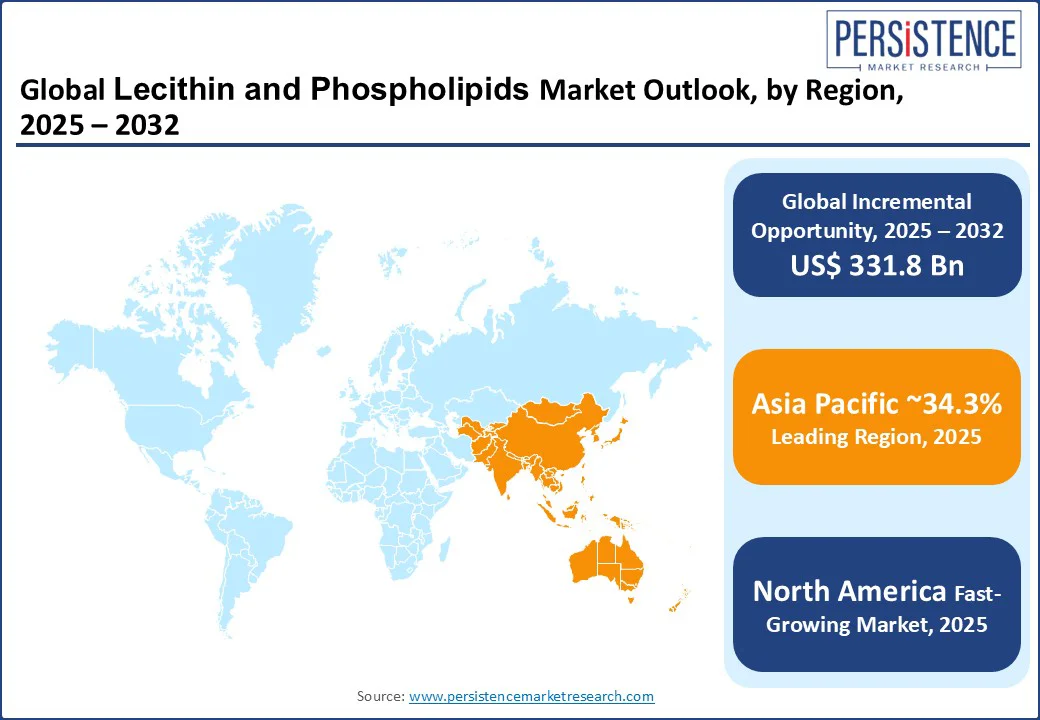

- Leading Region: Asia Pacific holds a 34.3% market share in 2025, driven by large-scale food production, high population density, and increasing demand for functional foods in countries such as China and India.

- Fastest-growing Region: North America, fuelled by rising consumer demand for clean-label and organic products, advanced food processing infrastructure, and strong adoption of health-focused ingredients.

- Regulatory support: Europe is focusing on sustainable sourcing and organic lecithin, backed by regulatory frameworks such as the EU’s Farm to Fork Strategy and consumer demand for eco-friendly products.

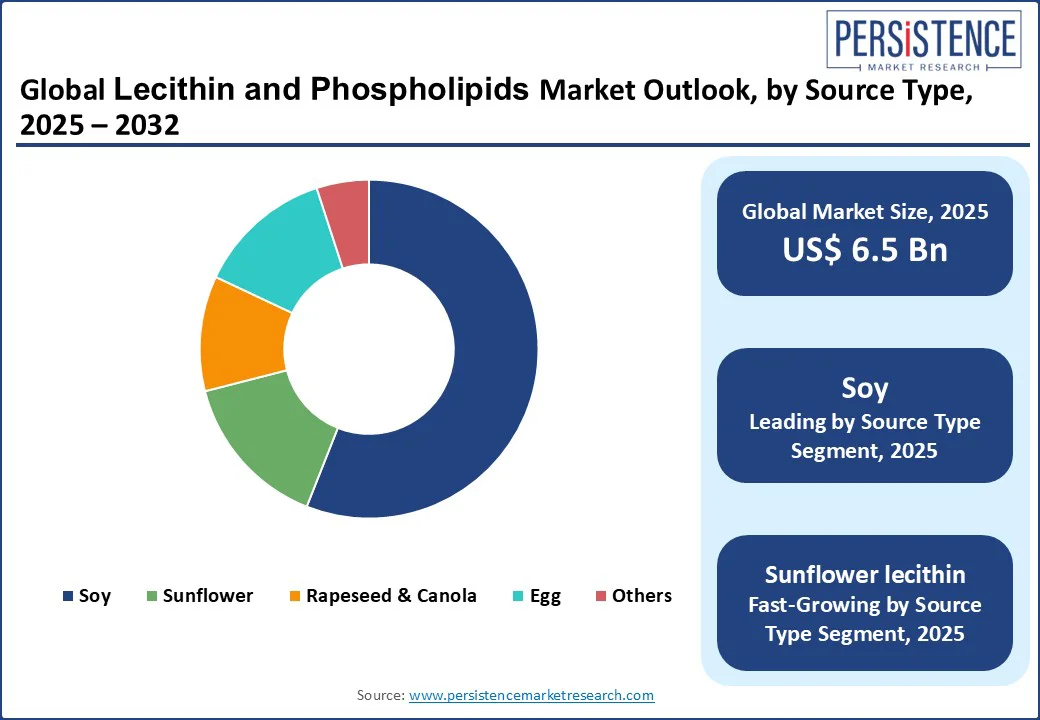

- Dominant Source Type: Soy lecithin accounts for nearly 56% of the Lecithin and Phospholipids market share, driven by its cost-effectiveness and widespread use in food applications.

- Leading Application Type: Food & beverages lead with a 45% share, reflecting the extensive use of lecithin in processed foods and beverages.

|

Key Insights |

Details |

|

Lecithin and Phospholipids Market Size (2025E) |

US$ 6.5 Bn |

|

Market Value Forecast (2032F) |

US$ 10.2 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.3% |

Market Dynamics

Driver - Rising Demand for Clean-label Products and Health Consciousness Pushes Demand

The global rise in health consciousness and demand for clean-label products is a key growth driver. Consumers are increasingly seeking natural, non-GMO, and organic ingredients, with a significant portion of the population preferring clean-label foods, according to industry surveys. Lecithin, known for its emulsifying properties and health benefits such as cholesterol reduction, aligns well with these consumer preferences. Research has shown that soy lecithin supplementation can contribute to improved lipid profiles in individuals with high cholesterol, further boosting its use in functional food applications.

The growing popularity of plant-based diets and functional foods also fuels demand. As veganism continues to gain traction in North America and Europe, lecithin derived from soy and sunflower is being widely incorporated into plant-based dairy and bakery products. The rising popularity of plant-based alternatives has increased the need for natural emulsifiers such as lecithin in formulations such as vegan chocolates, spreads, and other non-dairy items.

Government-backed nutrition initiatives also support market growth. In India, the Food Safety and Standards Authority (FSSAI) promotes fortified foods, incorporating lecithin in products such as infant formula, reaching over 50 million beneficiaries by 2023. These programs emphasize lecithin’s role in enhancing nutritional value, driving institutional demand.

Restraint - Supply Chain Volatility and Allergen Concerns Restrict Adoption

Supply chain volatility, particularly for soy and sunflower lecithin, poses a significant barrier to market growth. Fluctuations in raw material availability driven by factors such as climate change, extreme weather events, and geopolitical instability can disrupt supply and elevate production costs. Droughts in major producing countries, trade restrictions, and logistical challenges have made it difficult to maintain a steady sourcing of key inputs. These disruptions often lead to price increases, limiting the accessibility of lecithin in cost-sensitive regions such as Latin America and parts of the Asia Pacific. As a result, market expansion in these areas remains constrained despite growing demand.

Allergen concerns also hinder market growth, particularly for soy and egg-based lecithin. A 2022 International Food Information Council survey found that consumers avoid soy-based products due to allergen risks, restricting adoption among sensitive populations. This perception drives demand for alternative sources such as sunflower lecithin, but higher costs limit their scalability in cost-sensitive regions.

Opportunity - Innovation in Organic Lecithin and Sustainable Sourcing Boosts Consumption

The rise of organic and non-GMO lecithin offers significant opportunities by catering to increasing consumer demand for clean-label and transparently sourced products. As awareness of food ingredients grows, more consumers are prioritizing health-focused and ethically produced options, especially in vegan and plant-based categories. This trend is particularly strong in regions such as Europe and North America, where the preference for natural and minimally processed ingredients continues to rise. Companies can capitalize on this shift by expanding their portfolios with certified organic lecithin and emphasizing quality standards such as USDA Organic and Non-GMO Project Verified to enhance brand credibility and consumer trust.

Sustainable sourcing and eco-friendly processing present another growth avenue. With global concerns about environmental impact, brands are adopting sustainable practices. For example, in 2024, Cargill invested US$130 million to help our partners and local communities address urgent needs across 70 countries, including efforts to strengthen food security, farmer livelihoods, sustainable food systems, and more. In the Asia Pacific, companies such as Wilmar International are exploring energy-efficient extraction methods, reducing carbon footprints by 20%.

The growing popularity of e-commerce also presents strong opportunities for market expansion in the lecithin and phospholipids sector. Online B2B and B2C platforms are increasingly being used to distribute both raw ingredients and finished products, driven by the convenience of direct-to-consumer models and the rise of subscription-based services. This digital shift enables brands to reach a broader audience, including health-conscious consumers and specialty food manufacturers, through targeted digital marketing, product customization, and personalized recommendations. E-commerce also facilitates quicker market entry for emerging players and enhances visibility for organic, non-GMO, and clean-label lecithin offerings.

Category-wise Analysis

By Source Type

The market is segmented into Soy, Sunflower, Rapeseed & Canola, Egg, and Others. Soy lecithin dominates, accounting for approximately 56% of the lecithin and phospholipids market share in 2025, due to its cost-effectiveness, availability, and widespread use in food and feed applications. Products such as Cargill’s Topcithin are favored for their emulsifying properties in chocolates and baked goods.

Sunflower lecithin is the fastest-growing segment, driven by rising demand for allergen-free and non-GMO alternatives. Sunflower-based products, such as those from Stern-Wywiol Gruppe, appeal to health-conscious consumers in North America and Europe, where allergen concerns are driving market shifts.

By Form Type

By form type, the market is divided into Fluid, De-oiled, and Modified. Fluid lecithin leads, accounting for 50% of the market share in 2025, due to its versatility in food applications such as sauces and confectionery. Its ease of use and cost-effectiveness make it a preferred choice for large-scale manufacturers.

De-oiled lecithin is the fastest-growing segment, fueled by its high purity and suitability for premium applications such as nutraceuticals and infant formula. Products such as Lipoid GmbH’s de-oiled lecithin are gaining traction for their enhanced stability and nutritional benefits.

By Application Type

By application, the segmentation comprises Food & Beverages, Bakery Products, Convenience Foods, Confectioneries, Feed, and Others. Food & beverages lead with a 45% share in 2025, driven by the extensive use of lecithin as an emulsifier in processed foods such as margarine and beverages. Brands such as ADM dominate with solutions for large-scale food production.

Bakery products are the fastest-growing segment, fueled by the rising demand for clean-label and plant-based baked goods. Lecithin’s role in improving dough stability and shelf life, as seen in products such as Kewpie Corporation’s bakery emulsifiers, drives adoption in urban markets.

Regional Insights

North America Lecithin and Phospholipids Market Trends

In North America, the U.S. is the fastest-growing region for global lecithin and phospholipids market, driven by rising consumer demand for clean-label and organic products and advanced food processing infrastructure. U.S. lecithin sales in food applications continue to rise steadily, with soy and sunflower lecithin leading due to their prevalent use in plant-based dairy and bakery products. The increasing popularity of veganism further fuels demand for lecithin as a natural emulsifier in various clean-label and health-focused food formulations.

Consumer trends in the U.S. strongly favor organic and non-GMO lecithin, with brands such as American Lecithin Company experiencing significant market growth. The Lecithin and Phospholipids market also emphasizes sustainable sourcing practices, with companies such as Cargill introducing traceable lecithin lines certified by USDA Organic. Regulatory support for clean-label standards and broader health initiatives further contributes to market expansion.

Europe Lecithin and Phospholipids Market Trends

Europe is led by Germany, the U.K., and France, driven by regulatory support and consumer demand for organic products. Germany holds the largest share in the lecithin market, with sales growth driven by prominent brands such as Lipoid GmbH and Stern-Wywiol Gruppe. The EU’s Farm to Fork Strategy promotes sustainable sourcing practices, further boosting the production and adoption of organic lecithin across food, pharmaceutical, and nutraceutical applications.

The U.K. market is driven by health-conscious millennials and Gen Z, who prefer non-GMO and allergen-free lecithin in bakery and confectionery products. France sees growth in lecithin for infant formula, with companies such as Lasenor Emul offering specialized solutions. Regulatory incentives for eco-friendly processing further support market expansion.

Asia Pacific Lecithin and Phospholipids Market Trends

Asia Pacific dominates with a 34.3% market share in 2025, led by China, India, and Japan. In India, rising health awareness and urbanization drive demand for affordable soy lecithin, with companies such as Sodrugestvo and VAV Life Sciences leading the Lecithin and Phospholipids market. India’s functional food market is expanding, supported by government programs such as FSSAI’s fortification initiatives, which promote the use of lecithin in fortified foods.

China’s market is driven by large-scale food production and rising demand for convenience foods, with brands such as Wilmar International leading in soy lecithin for snacks and beverages. Japan emphasizes premium lecithin for nutraceuticals, with Kewpie Corporation’s egg-based products gaining traction. The region’s rapid digital transformation and growth in B2B e-commerce further accelerate market expansion.

Competitive Landscape

The global lecithin and phospholipids market is highly competitive, with global and regional players competing on product quality, pricing, and sustainability. The rise of organic and non-GMO products intensifies competition, as consumers demand transparency and eco-friendly options. Strategic partnerships, certifications, and technological advancements are key differentiators.

Key Developments

- In March 2024, Louis Dreyfus Company (LDS) displayed its line of packaged cooking oils and plant-based ingredients. It sells plant-based goods such as phospholipids (lecithin) made from rapeseeds, sunflower seeds, and soybeans.

- In Dec. 2021, Hain Celestial Group announced that it had reached an agreement to acquire that’s how they roll, the manufacturer & marketer of ParmCrisps & Thinsters, two quickly expanding, healthier brands with popular products that are convenient and tasty, from Clearlake Capital. The acquisition strengthens the company’s position in the snacking industry.

Companies Covered in Lecithin and Phospholipids Market

- Cargill Incorporated

- ADM

- Stern-Wywiol Gruppe GmbH & Co. KG

- Dowdupont

- Lipoid GmbH

- Wilmar International Ltd.

- Sodrugestvo

- Kewpie Corporation

- American Lecithin Company

- Sime Darby Plantation Berhad

- Lasenor Emul

- VAV Life Sciences

- Lecital

- Sonic Biochem

- Others

Frequently Asked Questions

The global Lecithin and Phospholipids market is projected to reach US$6.5 Bn in 2025.

Rising demand for clean-label products, health consciousness, and government nutrition initiatives are the key market drivers.

The Lecithin and Phospholipids market is poised to witness a CAGR of 6.6% from 2025 to 2032.

Innovation in organic lecithin and sustainable sourcing are the key market opportunities.

Cargill Incorporated, ADM, and Lipoid GmbH are among the key market players.