- Industrial Goods & Service

- Industrial Hose Assemblies Market

Industrial Hose Assemblies Market Size, Share, and Growth Forecast for 2025 - 2032

Industrial Hose Assemblies Market by Material Type (Rubber, Plastics, and Metal), Product Type (Low Pressure, Medium Pressure, and High Pressure), Component Type (Industrial Hose Assemblies and Industrial Hose Fittings), End User, and Regional Analysis from 2025 - 2032

Industrial Hose Assemblies Market Size and Share Analysis

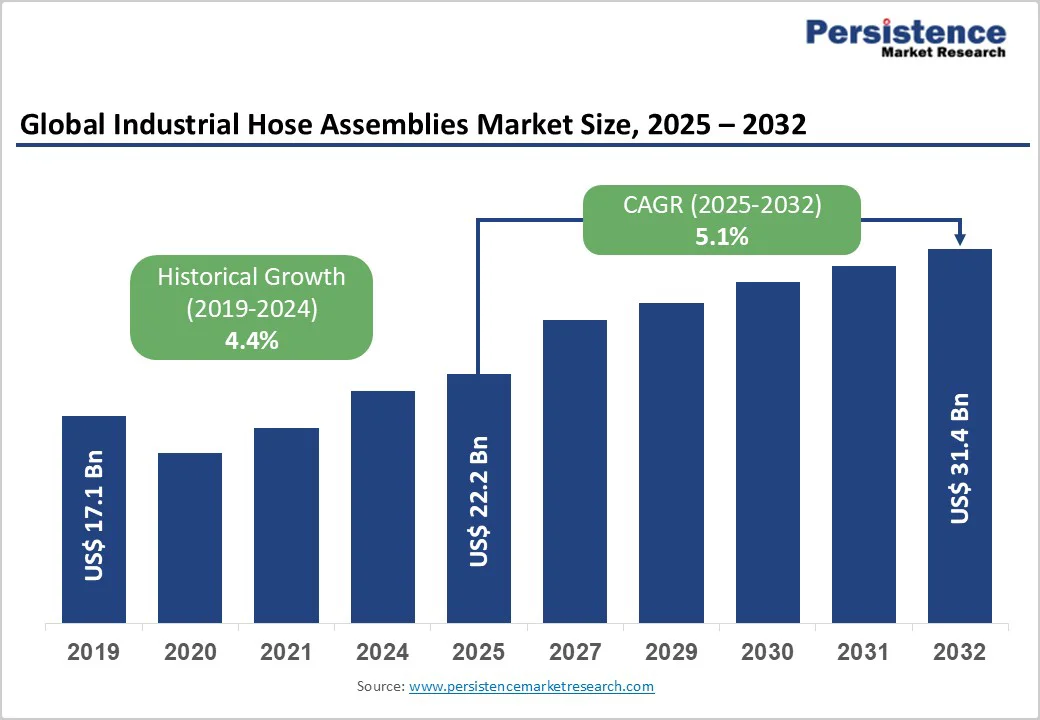

The global industrial hose assemblies market size is likely to value at US$ 22.2 Bbillion in 2025 and is projected to reach US$ 31.4 billion, growing at a CAGR of 5.1% between 2025 and 2032. Factors such as rising demand from industries such as oil & gas, chemicals, construction, and food processing, and increasing investments in industrial automation and process efficiency are driving the demand for industrial hose assemblies across the globe. The shift toward high-performance, abrasion-resistant, and temperature-tolerant hose materials also supports sustained market growth through 2032.

Key Industry Highlights:

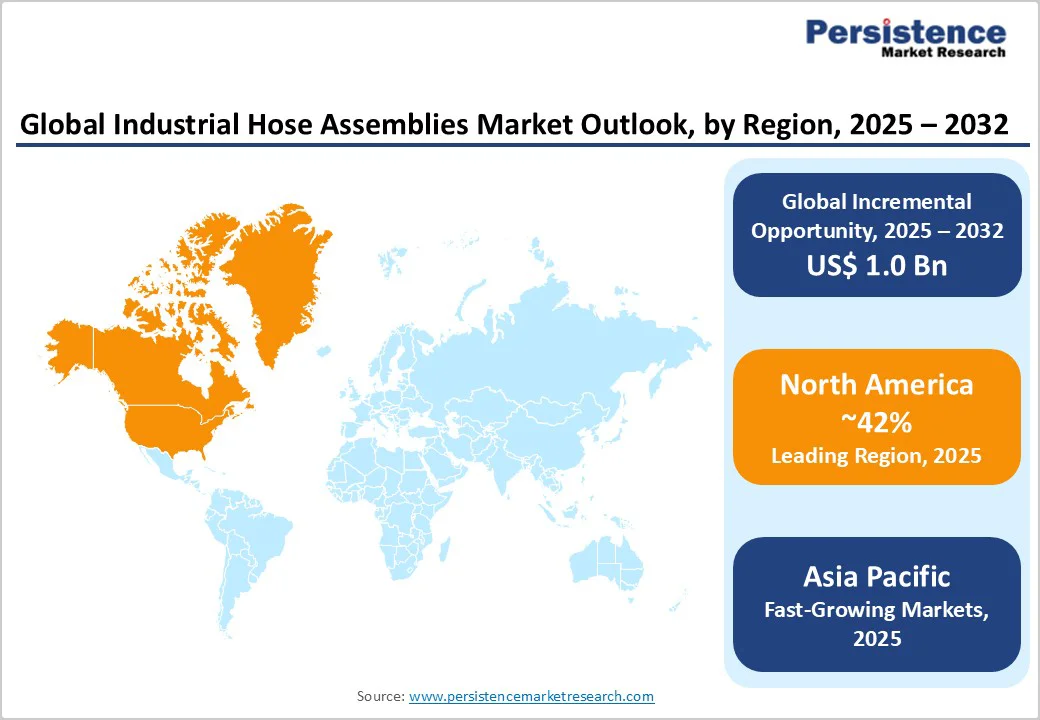

- Regional Leaders: North America maintains regional market leadership with mature industrial base and robust manufacturing infrastructure.

- Fastest-Growing Region: Asia-Pacific represents fastest-growing region at 6.5% CAGR through 2032, driven by China construction dominance, India mechanized agriculture expansion, and Southeast Asian industrialization supporting sustained demand growth.

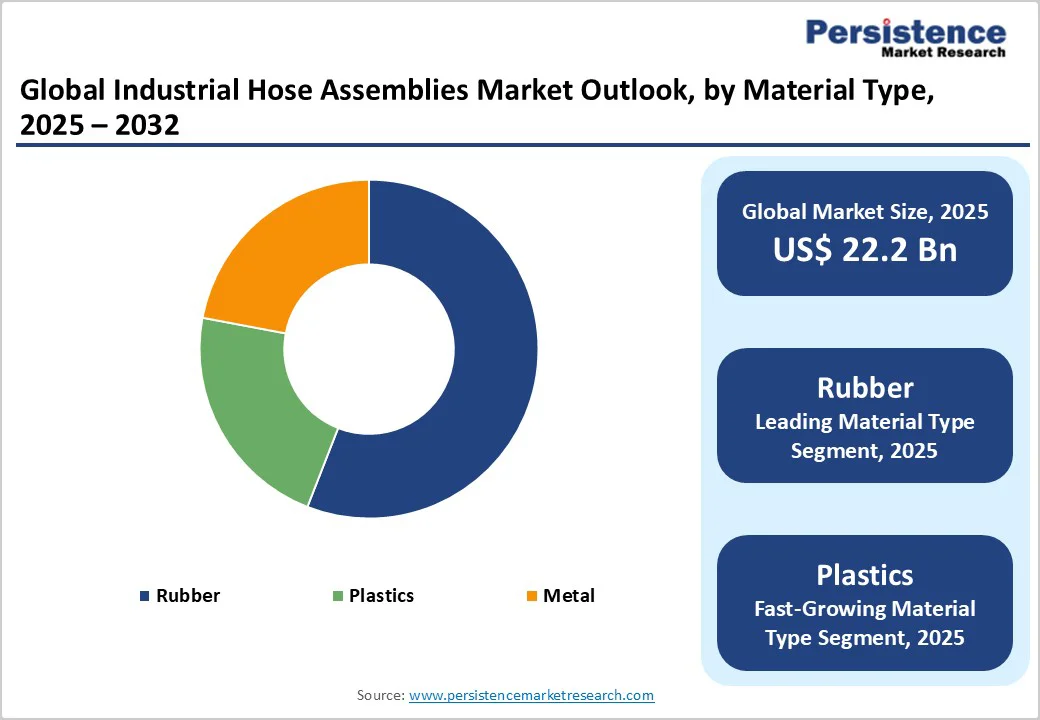

- Leading Material Type: Rubber hose assemblies dominate material type at 54% market share, supported by proven reliability, temperature tolerance, and exceptional chemical compatibility across diverse industrial applications.

- Product Type: Low-Pressure hose assemblies lead pressure categories at 40% market share, representing optimal performance-cost balance for cooling systems, lubrication applications, and general industrial requirements serving cost-conscious industrial segments.

- Market Opportunity: Agricultural sector modernization across Asia-Pacific and Latin America creates substantial industrial hose assemblies demand driven by mechanized farming adoption and precision irrigation system expansion.

| Key Insights | Details |

|---|---|

|

Industrial Hose Assemblies Market Size (2025E) |

US$ 22.2 Bn |

|

Projected Market Value (2032F) |

US$ 31.4 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.1% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

4.4% |

Market Dynamics

Market Growth Drivers

Accelerating Global Infrastructure and Construction Development Programs

Industrial automation expansion across manufacturing, construction, and process industries drives sustained demand for high-performance hydraulic hose assemblies supporting precision equipment operation and fluid transfer optimization. Global manufacturing output reached approximately US$ 13.9 trillion in 2024, with automation investment accelerating at 8.2% annually according to international manufacturing association data. The convergence of automation technologies with advanced hose assembly components including integrated sensors and smart connectors creates premium market positioning opportunities. Industries including automotive, chemicals, pharmaceuticals, and food processing increasingly adopt precision hydraulic systems requiring specialized hose assemblies meeting enhanced performance, reliability, and safety standards supporting sustained capital equipment investments driving consistent market expansion.

Expanding Oil & Gas Exploration and Production Requirements

The rapid expansion of oil and gas exploration and production activities significantly drives the growth of the global industrial hose assemblies market. Global crude oil production maintaining approximately 100 million barrels daily in 2024, with deepwater production expanding 3-4% annually through 2032, necessitates sophisticated hydraulic systems utilizing high-pressure and ultra-high-pressure hose assemblies withstanding extreme conditions. Upstream and midstream operations rely heavily on hose assemblies for fluid transfer, drilling mud circulation, fuel handling, and chemical injection processes under high-pressure and extreme-temperature conditions.

As global energy demand rises, oil companies are increasing investments in offshore platforms, shale extraction, and pipeline infrastructure, all of which require robust, flexible, and corrosion-resistant hose solutions. Additionally, the development of enhanced oil recovery (EOR) technologies and deepwater projects creates demand for specialized hose assemblies capable of handling aggressive fluids and abrasive materials. Manufacturers are responding with advanced materials and reinforced designs to ensure safety, reliability, and operational efficiency. The continuous growth in oil and gas activities worldwide thus remains a primary driver propelling the industrial hose assemblies market forward.

Market Restraining Factors

High Maintenance Costs and Frequent Replacement Needs Restrain Market Growth

High maintenance costs and frequent replacement requirements act as key restraints in the global industrial hose assemblies market. Hose assemblies operate under harsh conditions, exposed to extreme temperatures, high pressures, corrosive chemicals, and mechanical stress, which accelerates wear, leakage, and degradation. Frequent inspections, replacements, and downtime add substantial operational costs, particularly in sectors such as oil & gas, chemicals, and construction, where equipment uptime is critical.

Improper installation, kinking, and incompatible fluid usage can further shorten hose lifespan, leading to safety hazards and performance losses. In remote or offshore locations, maintenance and replacement activities require skilled labor and logistical support, increasing overall project costs. These challenges discourage small and medium-scale operators from adopting advanced hose systems, limiting market penetration in cost-sensitive industries.

Opportunity

Agricultural Mechanization and Precision Irrigation Infrastructure Development

Agricultural sector modernization across Asia-Pacific and Latin America creates substantial industrial hose assemblies demand driven by mechanized farming adoption, precision irrigation system expansion, and equipment utilization increasing at a 5.8% CAGR through 2032. India's agricultural equipment manufacturing sector demonstrated 12.3% year-on-year growth in FY 2023-2024, directly supporting hydraulic hose assemblies demand across tractors, harvesters, and specialized farming machinery.

FAO data indicates that over 60% of farmland in South and Southeast Asia relies on rain-fed irrigation, necessitating deployment of efficient water distribution networks utilizing rubber hose-based irrigation systems. Companies developing specialized agricultural hoses featuring UV corrosion resistance, operational flexibility optimization, and cost-effective formulations achieve competitive advantages, capturing rapidly-expanding agricultural market segments.

Renewable Energy Infrastructure and Advanced Material Technology Development

Renewable energy sector expansion, particularly solar thermal and wind power installations, creates substantial demand for durable, heat-resistant hose assemblies supporting energy infrastructure modernization. The International Renewable Energy Agency (IRENA) reports that Asia-Pacific accounted for over 55% of global renewable energy investments in 2023, with China, India, and Australia leading large-scale solar and wind projects generating sustained hose assembly procurement.

Thermoplastic and composite hose technology advancement represents critical growth opportunity, with thermoplastic hoses projecting 6.8% CAGR through 2032 driven by 20-30% weight reduction benefits, enhanced corrosion resistance, and improved compatibility with emerging industrial requirements. Lightweight composite reinforcement combining carbon fiber and aramid materials enables significant weight savings while maintaining high pressure ratings, further strengthening opportunities for premium, high-performance hose solutions across the renewable energy and industrial infrastructure sectors.

Category-wise Insights

Material Type Analysis

Rubber hose assemblies dominate the material segment with approximately 54% market share in 2025, driven by exceptional flexibility characteristics, temperature tolerance spanning -40°C to +100°C, and proven reliability across diverse industrial applications. Natural and synthetic rubber formulations deliver superior resilience and chemical compatibility, supporting extensive utilization across oil & gas, mining, construction, and manufacturing sectors. Rubber hose assemblies demonstrate operational longevity exceeding 10-15 years in standard applications, establishing compelling total-cost-of-ownership metrics supporting widespread commercial adoption across cost-conscious industrial segments.

Thermoplastic hoses project 6.8% CAGR through 2032, representing the fastest-growing material segment driven by 20-30% weight reduction benefits, enabling simplified installation and reduced equipment stress. Plastics and composites serve specialized applications where lightweight characteristics and chemical resistance represent primary selection criteria.

Technology Analysis

Low-Pressure hose assemblies command approximately 40% market share, representing the most widely utilized pressure range serving cooling systems, lubrication applications, and low-intensity industrial processes where pressure containment requirements remain moderate. This segment demonstrates exceptional versatility, accommodating diverse equipment types and industrial processes, supporting widespread commercial adoption across cost-sensitive applications.

Medium-pressure segments demonstrate exceptional market resilience through proven reliability and established application standardization supporting broad commercial acceptance. These hoses serve construction equipment, agricultural machinery, and general industrial applications requiring balanced performance and cost-effectiveness.

Component Type Analysis

Industrial Hose Assemblies command approximately 62% market share, encompassing complete integrated systems combining hose tubes, reinforcement structures, and factory-crimped fittings delivered as ready-to-install solutions. Integrated assembly solutions reduce customer installation complexity, enhance system reliability through factory quality assurance, and support rapid equipment deployment across diverse industrial operations. Assembly components, including adapters, protective sleeves, and integrated sensors, enhance functionality and operational reliability, supporting premium pricing.

Regional Insights

North America Industrial Hose Assemblies Market Trends

North America maintains mature market leadership with the United States dominance commanding approximately 42% regional market share, driven by established industrial base, sophisticated manufacturing infrastructure, and substantial oil & gas operations spanning 240 active drilling rigs and extensive production infrastructure. The U.S. industrial hose assemblies market demonstrates 4.8% CAGR growth through 2032, supported by infrastructure modernization initiatives, equipment replacement cycles, and manufacturing facility upgrades across automotive, aerospace, and industrial manufacturing sectors.

Canada contributes a significant regional share, driven by oil sands development, representing 2.9 trillion barrels of proven reserves, mining operations, and construction activities supporting sustained hose demand expansion. The region benefits from established distribution networks, local manufacturing capabilities, and technical support infrastructure operated by Parker Hannifin, Gates Corporation, and Continental, maintaining technological leadership through continuous innovation in advanced pressure-resistant materials and smart assembly systems.

Europe Industrial Hose Assemblies Market Trends

Europe represents approximately 24% global market share, with Germany leads the regional demand through advanced manufacturing infrastructure and sophisticated industrial operations. German industrial hose assemblies demand demonstrates a 4.6% CAGR growth through 2032, supported by automotive manufacturing excellence, chemical processing industries, and renewable energy infrastructure modernization initiatives. The United Kingdom, France, and Spain collectively contribute approximately 42-48% regional share, driven by construction projects, oil & gas operations, and industrial facility modernization.

European regulatory emphasis on environmental compliance (EU REACH directives, wastewater discharge limitations) drives adoption of sustainable hose formulations across manufacturing operations. Germany's Made in Germany quality standards, combined with stringent engineering requirements, support technology differentiation strategies pursued by Continental, Trelleborg, and regional manufacturers maintaining a strong European presence through integrated manufacturing facilities and comprehensive technical support networks.

Asia Pacific Industrial Hose Assemblies Market Trends

Asia-Pacific represents the fastest-growing regional market, projecting 6.5% CAGR through 2032. China dominates regional production and consumption with approximately 38% regional share, driven by massive construction activities reaching US$ 5.8 trillion annually, expanding automotive manufacturing, and industrial facility development supporting sustained hose demand. China's hydraulic hose assemblies industry projects 7.2% CAGR growth through 2032, supported by the Made in China 2025 program emphasizing automation and advanced manufacturing. India demonstrates exceptional growth at approximately 7.0% CAGR through 2032, benefiting from infrastructure development initiatives allocating US$ 1.5+ trillion, agricultural mechanization expansion, and manufacturing sector modernization supporting diverse industrial hose applications.

Competitive Landscape for the Industrial Hose Assemblies Market

The global industrial hose assemblies market demonstrates moderately consolidated characteristics with top five companies (Parker Hannifin, Gates Corporation, Eaton, Continental, Trelleborg) commanding approximately 35-45% global market share through integrated manufacturing capabilities and extensive distribution networks. Market leaders compete through comprehensive product portfolios spanning multiple hose types, pressures, and materials; continuous R&D programs developing next-generation thermoplastic and composite technologies; and established customer relationships across industrial sectors.

Recent Industry Developments

- In April 2025, Continental AG (ContiTech Division) established a manufacturing partnership with Polyhose India Pvt. Ltd. for production capacity expansion in India, targeting agricultural, construction, and automotive markets with a focus on specialized hose formulations meeting regional requirements.

- In September 2024, Gates Corporation launched an IoT-enabled smart hose monitoring system integrating pressure sensors, temperature monitors, and cloud connectivity, reducing downtime by 35% through predictive maintenance alerts supporting preventive service scheduling and operational efficiency improvements.

- In August, 2024, Parker Hannifin Corp. announced expanded thermoplastic hose production capacity in Ohio and Indiana facilities, targeting 6.8% CAGR growth in lightweight composite hose applications serving automotive and precision machinery markets with enhanced performance characteristics.

Companies Covered in Industrial Hose Assemblies Market

- Gates Corporation

- Parker Hannifin Corp.

- Continental AG

- Eaton Corporation Plc.

- Trelleborg AB

- Semperit AG Holding

- Campbell Fittings Inc.

- United Flexible

- Polyhose India Pvt. Ltd.

- RYCO Hydraulics

- RADCOFLEX Australia Pty Ltd.

- Manuli Hydraulics Group

- Alfagomma Group

- Transfer Oil Group

Frequently Asked Questions

The global industrial hose assemblies market was valued at US$ 22.2 billion in 2025 and is projected to reach US$ 31.4 billion by 2032, growing at 5.1% CAGR during the forecast period.

Key demand drivers include industrial automation expansion, construction sector expansion, and robust growth of oil & gas industry, supported by mechanized agricultural adoption and smart manufacturing initiatives incorporating IoT-enabled systems reducing downtime.

Rubber dominates the material segment with 54% market share in 2025, driven by exceptional flexibility characteristics, temperature tolerance spanning -40°C to +100°C, proven reliability across diverse applications.

North America maintains regional market leadership with 42-48% regional share driven by United States industrial dominance, mature manufacturing infrastructure, and substantial oil & gas operations.

Major opportunities include agricultural mechanization expansion, renewable energy infrastructure development, and advanced material technology development including thermoplastic hoses.

Key market players include Parker Hannifin Corp. (Cleveland, Ohio), Gates Corporation (Denver, Colorado), Continental AG (Fairlawn, Ohio), Eaton Corporation Plc., Trelleborg AB, Manuli Hydraulics Group, Alfagomma Group, and Transfer Oil Group.