- Bulk Chemicals

- Industrial and Institutional Cleaning Chemicals Market

Industrial and Institutional Cleaning Chemicals Market Size, Share, and Growth Forecast, 2026 - 2033

Industrial and Institutional Cleaning Chemicals Market by Raw Material (Surfactants, Solvents, Others), Product Type (General Purpose Cleaners, Disinfectants and Sanitizers, Others), End-user Industry, and Regional Analysis for 2026 - 2033

Industrial and Institutional Cleaning Chemicals Market Size and Trends Analysis

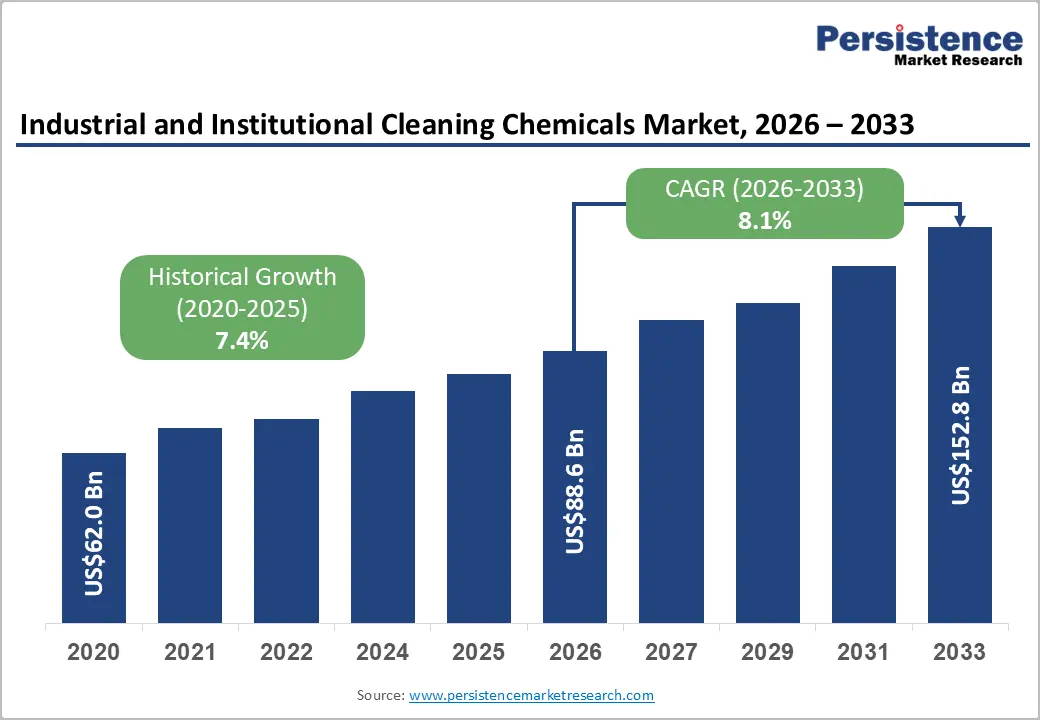

The global industrial and institutional cleaning chemicals market size is likely to be valued at US$88.6 billion in 2026 and is expected to reach US$152.8 billion by 2033, growing at a CAGR of 8.1% during the forecast period from 2026 to 2033, driven by increasingly stringent hygiene standards, rising adoption of environmentally responsible cleaning formulations, and sustained demand from healthcare, manufacturing, and commercial facilities.

Regulatory initiatives across major economies are encouraging the use of cleaning chemicals with improved biodegradability, reduced toxicity, and enhanced safety profiles.

Key Industry Highlights:

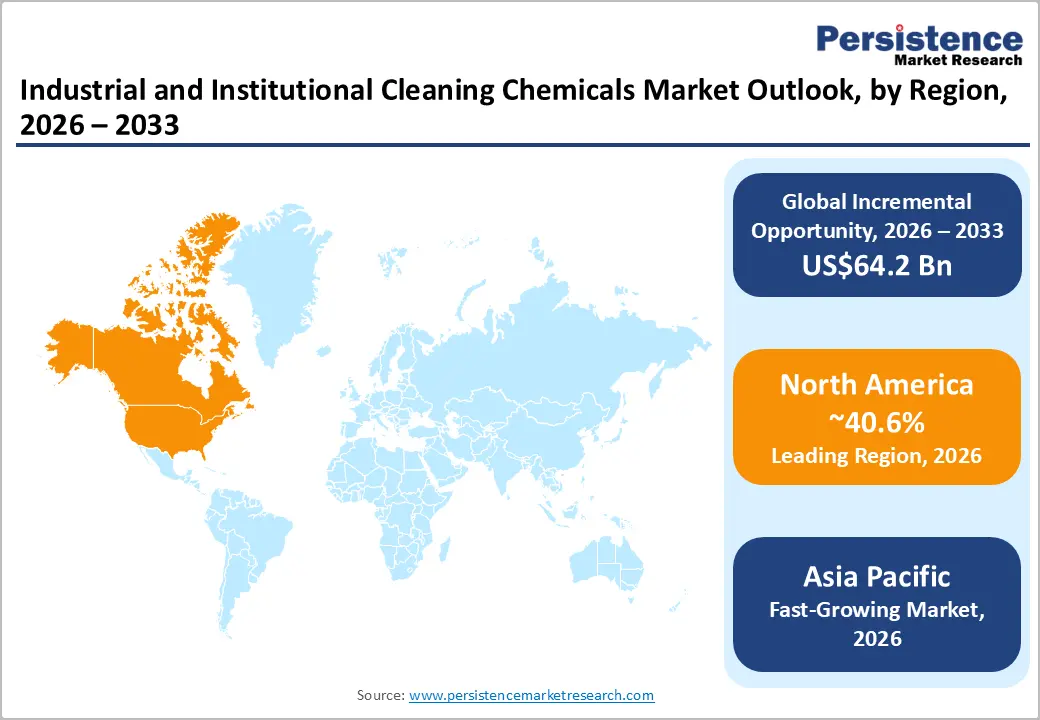

- Leading Region: North America is projected to account for approximately 40.6% of market revenue in 2026, supported by strong regulatory compliance requirements, advanced healthcare infrastructure, and widespread adoption of institutional cleaning solutions.

- Fastest-growing Region: Asia Pacific is expected to register the highest growth rate through 2033, driven by rapid industrialization, urbanization, healthcare infrastructure expansion, and increasing hygiene awareness across China, India, Japan, and ASEAN countries.

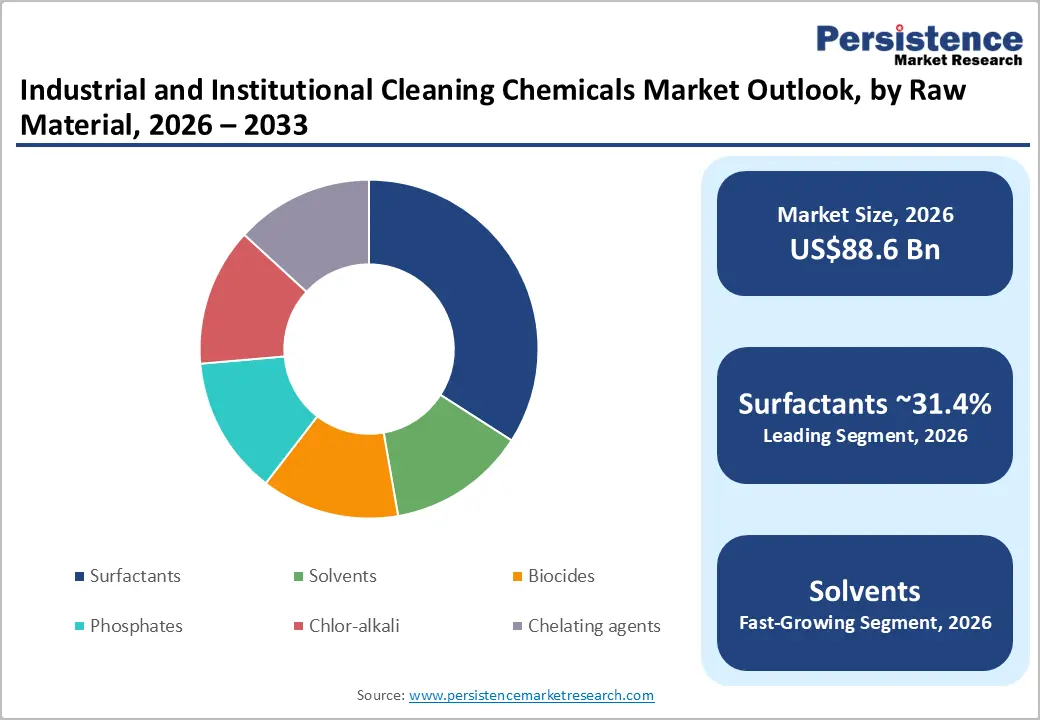

- Dominant Raw Material: Surfactants are projected to hold approximately 31.4% market share in 2026, supported by their critical role in cleaners, detergents, degreasers, disinfectants, and other institutional cleaning formulations.

- Leading Product Type: General purpose cleaners are estimated to account for approximately 35.2% of market revenue in 2026, driven by extensive use across commercial buildings, healthcare facilities, educational institutions, hospitality establishments, and public infrastructure.

DRO Analysis

Driver - Hygiene Compliance Becoming an Operational Requirement

Growing regulatory oversight and heightened sanitation requirements are transforming cleaning chemicals from a maintenance expense into an operational necessity across multiple industries. Government agencies and health organizations continue to emphasize environmental cleaning and disinfection as critical elements of workplace safety, infection prevention, and public health protection.

Healthcare facilities, food processing plants, educational institutions, and hospitality establishments are implementing more rigorous cleaning protocols to comply with evolving standards and maintain operational continuity. Organizations increasingly prioritize cleaning products that deliver proven efficacy, worker safety, and regulatory compliance. As a result, demand for industrial and institutional cleaning chemicals is becoming more consistent and less discretionary.

Sustainability and Advanced Formulation Technologies

Sustainability has become a major purchasing criterion across institutional and industrial cleaning applications. End users increasingly seek products formulated with biodegradable ingredients, lower volatile organic compound (VOC) content, and safer chemical profiles that align with environmental objectives and corporate sustainability commitments.

Manufacturers are investing heavily in green chemistry, renewable feedstocks, and advanced surfactant technologies to meet these expectations. At the same time, customers are demanding greater transparency regarding ingredient composition, product safety, and environmental impact.

The transition toward sustainable cleaning solutions is creating opportunities for premium products that combine cleaning performance with environmental responsibility. Companies capable of delivering innovative formulations while maintaining regulatory compliance are strengthening their competitive position and securing long-term customer relationships.

Restraint - Raw Material Volatility and Compliance Costs

The industry remains vulnerable to fluctuations in raw material costs, particularly for surfactants, solvents, biocides, chlor-alkali products, and specialty additives. Changes in feedstock pricing, transportation costs, and global supply chain conditions can significantly affect manufacturing economics and profitability.

Simultaneously, increasingly complex regulatory requirements are raising product development and compliance costs. Manufacturers must invest in extensive testing, documentation, reformulation efforts, and certification processes to meet evolving environmental and safety standards.

These challenges are particularly difficult for smaller suppliers that may lack the financial and technical resources needed to navigate complex regulatory environments. As compliance requirements continue to expand, market participants must balance innovation and sustainability objectives against rising operational costs.

Opportunity - Healthcare-Focused Cleaning and Disinfection Solutions

Healthcare remains one of the most attractive growth opportunities within the industrial and institutional cleaning chemicals market. Hospitals, clinics, long-term care facilities, and outpatient centers continue to strengthen infection prevention programs, creating sustained demand for specialized cleaning and disinfection products.

The market is increasingly shifting toward integrated hygiene systems that combine disinfectants, cleaning agents, dosing technologies, monitoring tools, and staff training programs. These comprehensive solutions help healthcare providers improve compliance, reduce labor requirements, and maintain consistent sanitation standards.

Sustainable Manufacturing and Growth in Asia Pacific

Asia Pacific represents a significant growth opportunity due to rapid industrial development, urbanization, healthcare infrastructure expansion, and rising sanitation standards. Countries such as China, India, and several Southeast Asian economies continue to invest heavily in manufacturing capacity, commercial facilities, and public infrastructure.

The region is also witnessing increasing adoption of sustainable manufacturing practices and environmentally responsible cleaning products. Global and regional manufacturers are expanding local production capabilities to improve supply reliability, reduce transportation costs, and support sustainability objectives.

Organizations that combine regional manufacturing capabilities with innovative, environmentally friendly formulations are expected to benefit from strong demand growth across institutional and industrial customer segments.

Category-wise Analysis

Raw Material Insights

Surfactants are anticipated to account for approximately 31.4% of the market share in 2026, maintaining their position as the leading raw material segment. Surfactants are the primary active ingredients in general-purpose cleaners, floor cleaners, laundry detergents, and degreasers because they effectively remove dirt, oils, and contaminants. Their widespread use across commercial buildings, hospitals, hotels, and manufacturing facilities continues to support market leadership. Examples include alcohol ethoxylates and linear alkylbenzene sulfonates commonly used in institutional cleaning formulations. Ongoing innovation in bio-based and low-foaming surfactants is further strengthening demand.

Solvents are projected to grow at the fastest CAGR of 8.3% through 2033. Growth is driven by increasing demand for precision cleaning in electronics manufacturing, pharmaceutical production, and industrial maintenance applications. Solvents are widely used in metal cleaning, equipment degreasing, and residue removal processes where rapid evaporation and high cleaning efficiency are required. The development of low-VOC and environmentally friendly solvent technologies is further accelerating adoption across regulated industries.

Product Type Insights

General purpose cleaners are anticipated to hold approximately 35.2% of market revenue in 2026, making them the largest product category. Their leadership is supported by broad applicability across offices, schools, healthcare facilities, retail stores, hotels, and public buildings. These cleaners are commonly used for daily maintenance of hard surfaces, countertops, washrooms, and common areas, helping organizations streamline procurement and cleaning operations. Their high usage frequency continues to make them the largest revenue-generating product segment.

Disinfectants and sanitizers are the fastest-growing segment. Demand is increasing due to stronger infection prevention requirements in hospitals, food processing facilities, hospitality establishments, and public institutions. Products such as quaternary ammonium compound disinfectants, alcohol-based sanitizers, and hydrogen peroxide-based formulations are gaining traction because they help organizations meet hygiene standards while improving operational efficiency.

Regional Insights

North America Industrial and Institutional Cleaning Chemicals Market Trends

North America is anticipated to account for approximately 40.6% of the market share in 2026, maintaining its position as the leading regional market. Growth is supported by stringent workplace safety regulations, strong hygiene standards, and widespread adoption of advanced cleaning technologies across commercial, healthcare, and industrial facilities. The region benefits from high spending on facility maintenance and increasing demand for sustainable cleaning solutions.

U.S. Industrial and Institutional Cleaning Chemicals Market Trends

The U.S. represents the largest market within North America, supported by its extensive healthcare infrastructure, large commercial building stock, and advanced manufacturing sector. Demand remains particularly strong in hospitals, food processing facilities, educational institutions, airports, and hospitality establishments. The increasing adoption of automated dispensing systems, environmentally friendly formulations, and infection-control solutions continues to support market expansion.

Canada Industrial and Institutional Cleaning Chemicals Market Trends

Canada contributes steadily to regional growth through increasing investments in healthcare facilities, commercial infrastructure, and sustainable building management. Growing adoption of green cleaning programs across public institutions and corporate facilities is driving demand for biodegradable and low-toxicity cleaning chemicals. The country's focus on workplace safety and environmental stewardship further supports market development.

Europe Industrial and Institutional Cleaning Chemicals Market Trends

Europe represents a mature yet highly influential market characterized by strong environmental regulations, sustainability initiatives, and advanced industrial hygiene practices. Demand is increasingly shifting toward biodegradable formulations, safer ingredients, and products that comply with evolving environmental standards. Healthcare, manufacturing, hospitality, and food processing remain the primary end-use sectors driving consumption.

Germany Industrial and Institutional Cleaning Chemicals Market Trends

Germany is the largest market in Europe due to its strong industrial base, extensive manufacturing activities, and high emphasis on workplace hygiene. The country's automotive, pharmaceutical, and food processing sectors generate substantial demand for specialized industrial cleaning chemicals. Investments in sustainable manufacturing and green chemistry continue to create opportunities for advanced cleaning formulations.

U.K. Industrial and Institutional Cleaning Chemicals Market Trends

The U.K. remains a key contributor to regional demand, supported by a large commercial services sector and expanding healthcare infrastructure. Growing focus on infection prevention, environmental compliance, and workplace cleanliness is increasing demand for disinfectants, sanitizers, and general-purpose cleaning products across public and private facilities.

France Industrial and Institutional Cleaning Chemicals Market Trends

France benefits from strong demand across healthcare institutions, hospitality facilities, and food processing operations. Sustainability objectives and circular economy initiatives are encouraging the adoption of environmentally responsible cleaning products. Manufacturers continue to invest in innovative formulations that balance cleaning performance with environmental compliance.

Spain Industrial and Institutional Cleaning Chemicals Market Trends

Spain is experiencing steady growth driven by its tourism industry, hospitality sector, and expanding commercial infrastructure. Hotels, restaurants, healthcare facilities, and educational institutions represent major consumers of institutional cleaning chemicals. Increased investment in sanitation standards and sustainable facility management supports long-term market opportunities.

Asia Pacific Industrial and Institutional Cleaning Chemicals Market Trends

Asia Pacific is anticipated to be the fastest-growing regional market throughout the forecast period. Rapid urbanization, industrial development, healthcare infrastructure expansion, and rising hygiene awareness are driving significant demand across both industrial and institutional applications. The region is also benefiting from increasing local manufacturing investments and expanding supply chain capabilities.

China Industrial and Institutional Cleaning Chemicals Market Trends

China represents the largest market within Asia Pacific due to its massive manufacturing base and extensive commercial infrastructure. Strong demand from electronics, automotive, pharmaceutical, and consumer goods industries continues to drive consumption of industrial cleaning chemicals. Government initiatives focused on environmental sustainability and workplace safety are accelerating the adoption of advanced cleaning solutions.

Japan Industrial and Institutional Cleaning Chemicals Market Trends

Japan remains a technologically advanced market characterized by high-quality cleaning standards and strict hygiene requirements. Demand is particularly strong in healthcare facilities, electronics manufacturing, food processing, and commercial buildings. The country's emphasis on automation and precision cleaning supports adoption of specialized cleaning formulations.

India Industrial and Institutional Cleaning Chemicals Market Trends

India is expected to register the fastest growth within the region, driven by rapid industrialization, healthcare expansion, urban development, and rising awareness of workplace hygiene. Government investments in healthcare infrastructure, smart cities, and manufacturing initiatives are creating substantial opportunities for industrial and institutional cleaning chemical suppliers.

Competitive Landscape

The global industrial and institutional cleaning chemicals market exhibits a moderately fragmented competitive structure. While several multinational companies maintain strong positions through extensive product portfolios, technological expertise, and global distribution networks, numerous regional and specialized suppliers also compete effectively in niche applications and local markets.

Competition is primarily based on product performance, regulatory compliance, sustainability credentials, pricing, technical support, and customer service capabilities. Innovation and formulation expertise continue to serve as key differentiators among leading market participants.

Leading companies are focusing on sustainable innovation, geographic expansion, supply chain localization, and value-added service offerings. Competitive advantage increasingly depends on the ability to combine high-performance formulations with environmental responsibility, regulatory compliance, digital technologies, and customer support solutions.

Key Industry Developments:

- In February 2025, Ecolab Inc. announced the expansion of its Ecolab Scientific Clean™ portfolio through its partnership with The Home Depot, including the planned launch of several new cleaning products and two entirely new cleaning categories during 2025, aimed at broadening its presence across commercial, industrial, and institutional cleaning applications in North America.

- In September 2025, BASF SE announced the delivery of its first biomass-balanced 3-(dimethylamino)propylamine (DMAPA) shipment in Asia Pacific to Galaxy Surfactants, supporting the production of lower-carbon surfactant ingredients and strengthening sustainable cleaning chemical supply chains across home care and industrial cleaning markets.

Companies Covered in Industrial and Institutional Cleaning Chemicals Market

- Ecolab Inc.

- Diversey Holdings Ltd.

- BASF SE

- Henkel AG & Co. KGaA

- The Clorox Company

- Reckitt Benckiser Group plc

- Procter & Gamble Company

- 3M Company

- Solenis LLC

- Stepan Company

- Clariant AG

- Croda International Plc

- Evonik Industries AG

- Solvay SA

- Dow Inc.

- Eastman Chemical Company

Frequently Asked Questions

The global industrial and institutional cleaning chemicals market is estimated to be valued at US$88.6 billion in 2026.

The industrial and institutional cleaning chemicals market is expected to reach US$152.8 billion by 2033.

Key trends include the growing adoption of eco-friendly cleaning formulations, increasing demand for disinfectants and sanitizers, expansion of automated dispensing systems, rising focus on infection prevention, and investments in sustainable and bio-based chemical technologies.

Surfactants are the leading raw material segment, accounting for 31.4% of market share, owing to their widespread use in cleaners, detergents, degreasers, and disinfectant formulations.

The industrial and institutional cleaning chemicals market is projected to grow at a CAGR of 8.1% between 2026 and 2033.

Major companies include Ecolab Inc., BASF SE, Henkel AG & Co. KGaA, The Clorox Company, and Diversey Holdings Ltd.