- Hardware & Software IT Services

- Integrated Facility Management Market

Integrated Facility Management Market Size, Share, and Growth Forecast, 2026 - 2033

Integrated Facility Management Market by Solution Type (Integrated Facility Management Platforms, Services), Deployment Model (In-House IFM, Outsourced / Third-Party IFM), Industry (IT & Telecom, BFSI (Banking, Financial Services & Insurance), Healthcare & Life Sciences, Retail, Manufacturing, Transportation & Logistics, Real Estate & Property Management, Government & Defense) and Regional Analysis for 2026 - 2033

Integrated Facility Management Market Size and Trends Analysis

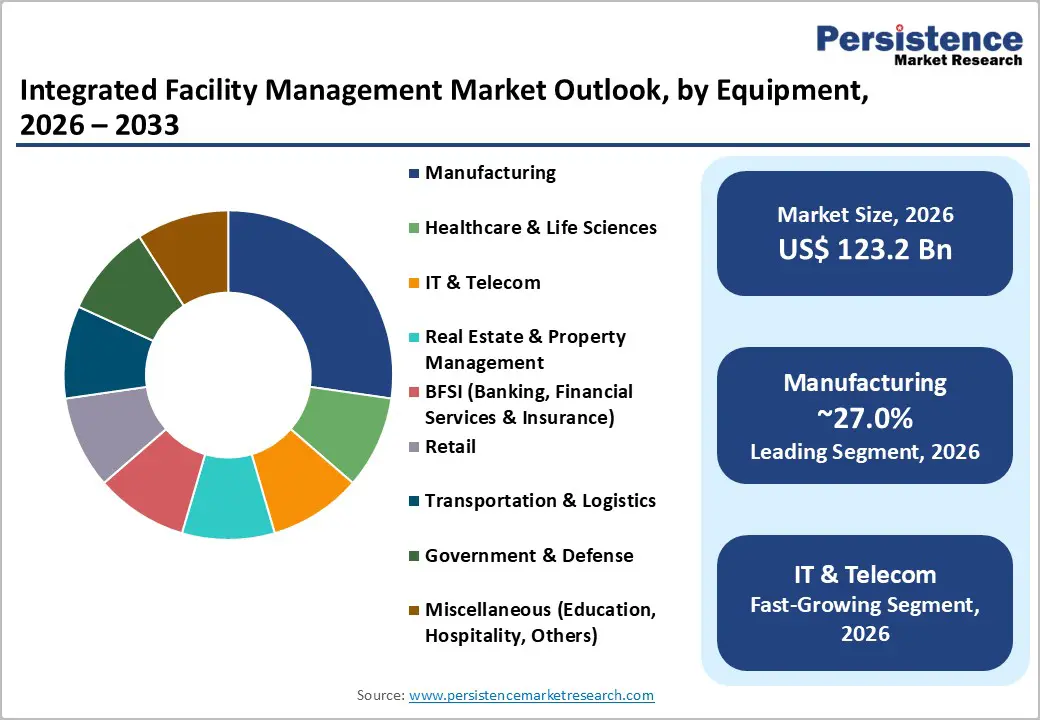

The global integrated facility management market size is likely to be valued at US$ 123.2 billion in 2026 and is projected to reach US$ 205.7 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

This trajectory is underpinned by accelerating enterprise demand for consolidated, technology-enabled facility operations that reduce overhead, improve sustainability compliance, and enhance occupant experience across commercial real estate, manufacturing, and public infrastructure. The market registered a historical CAGR of 6.8% between 2020 and 2026, scaling from US$ 82.4 billion in 2020 to US$ 123.2 billion in 2026, driven by the convergence of IoT adoption, AI-powered building management, and the global shift toward outsourced service delivery models. Policy mandates around energy efficiency, net-zero building targets, and digital workplace transformation are further reinforcing long-term demand fundamentals across all major geographies.

Key Industry Highlights:

- Regional Leadership: North America leads the global Integrated Facility Management Market with approximately 28% share, driven by high enterprise outsourcing penetration, US$ 2.2 trillion construction spending, large commercial real estate portfolios, and strong presence of global IFM majors.

- Fast-growing Region: Europe holds around 22% market share, supported by stringent regulatory frameworks such as energy performance mandates, GDPR compliance requirements, high IoT penetration (56% among large enterprises), and strong sustainability-driven procurement policies.

- Fast-growing Market: East Asia captures nearly 18% of the market, leveraging rapid urbanization, smart city initiatives, advanced digital infrastructure, 5G deployment, and large-scale manufacturing modernization across China, Japan, and South Korea.

- Dominant Solutions: Services account for approximately 72% of total market share, reflecting the labor-intensive and operations-centric nature of integrated technical and soft facility management contracts across enterprise portfolios

- Leading End-user: Manufacturing holds the largest industry share at around 18%, supported by high operational complexity, multi-site global footprints, strict compliance standards, and demand for standardized, digitally tracked IFM frameworks.

- Fastest-Growing Segment: IT & Telecom is the fastest-growing vertical, fueled by hyperscale data center expansion, 5G infrastructure rollout, and mission-critical uptime requirements that demand AI-driven predictive maintenance and energy optimization.

| Key Insights | Details |

|---|---|

| Integrated Facility Management Market Size (2026E) | US$ 123.2 Bn |

| Market Value Forecast (2033F) | US$ 205.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.8% |

Market Dynamics

Drivers - Digital Transformation and AI-Powered Smart Building Adoption

The rapid integration of artificial intelligence, IoT connectivity, and advanced analytics into building operations has fundamentally restructured the value proposition of the Integrated Facility Management Market, enabling facilities operators to deliver measurable performance outcomes rather than input-based service contracts. This driver reflects a systemic shift from manual, reactive maintenance toward data-driven, predictive operational models across enterprise, commercial, and institutional portfolios.

The scale of this transformation is illustrated by CBRE's deployment of its AI-powered Smart Facilities Management solution across more than 20,000 Global Workplace Solutions client sites, covering approximately 1 billion square feet globally. Powered by its Nexus AI platform, the solution leverages advanced analytics and building data to reduce maintenance costs and energy consumption by up to 20% and lower technician dispatches by 25%.

In the European Union, approximately 70% of EU citizens aged 16 to 74 reported using at least one internet-connected device in 2024, with IoT adoption in large enterprises running at 56% versus 26% in small enterprises, while condition-based maintenance adoption stands at 44% in large enterprises, directly supporting the business case for IoT-enabled IFM. The Integrated Facility Management Market benefits structurally from these dynamics as AI reduces the total cost of ownership while improving reliability, compliance, and sustainability performance.

Global Urbanization, Infrastructure Investment, and Real Estate Expansion

Accelerating urbanization and large-scale government infrastructure investment are generating a structural pipeline of new, complex facilities that require professionally managed, integrated operations support. At the core of this driver is the direct relationship between built-environment scale and demand for consolidated facility management across commercial, residential, industrial, and public infrastructure asset classes.

In the United States, total annual construction spending reached US$ 2.2 trillion in 2024, representing 4.5% of GDP, with 1.6 million new homes built in 2024 and 3.7 million construction businesses in operation as of 2023, underscoring the breadth of new facilities requiring ongoing management services. In India, government capital expenditure was raised 11.1% to US$ 133 billion in FY 2024-25, equivalent to 3.4% of GDP in the next two decades. India's organised security and IFM services sector registered a 13% CAGR over the four fiscals through March 2025, with Crisil Ratings projecting 10 to 12% revenue growth for the following fiscal year.

Sustainability Mandates and Energy Efficiency Imperatives

Regulatory pressure and voluntary corporate commitments to reduce carbon emissions, improve energy performance, and achieve net-zero building operations are directly stimulating demand for integrated, technology-enabled facility management services capable of delivering verified sustainability outcomes. This driver is particularly evident across Europe and the Middle East, where policy frameworks and national development agendas are prescribing measurable environmental performance standards for buildings.

In Saudi Arabia, CBRE launched a first-of-its-kind smart and sustainable IFM solutions package at its Vision 2030 Focus Forum, incorporating AI-driven technologies designed to reduce building energy costs by 8 to 10% while enhancing operational efficiency and workplace experience across client portfolios.

Across the European Union, Eurostat confirms that 94% of EU individuals used the internet in 2025, with one in three using generative AI tools, reflecting the digital maturity of the enterprise base that demands sustainability-integrated FM services. Coor's market analysis underscores that accelerating demand for sustainable and green facility solutions is a principal trend, noting that advancements in IoT and machine learning are driving the need for stronger operational technology security within smart buildings. These sustainability requirements elevate the Integrated Facility Management Market from a cost-center function to a strategic asset management discipline with board-level visibility.

Restraint - High Implementation Costs and Technology Integration Complexity

Transitioning legacy facility operations to fully integrated, digitally enabled IFM frameworks requires substantial upfront capital investment in IoT sensors, automation platforms, AI software, and workforce retraining costs that many mid-size enterprises and government bodies find prohibitive. Integration complexity is compounded by the need to synchronize disparate building management systems, legacy infrastructure, and multi-vendor service ecosystems into a single unified platform.

For operators managing multi-site portfolios across geographies, the challenge of standardizing service delivery while maintaining local compliance and operational continuity adds further friction to adoption timelines and total cost of transition within the integrated facility management market.

Data Security, Cybersecurity Risks, and Regulatory Compliance Burdens

The increasing connectivity of smart buildings through IoT devices, cloud platforms, and AI systems significantly expands the cybersecurity attack surface of facility operations, creating material operational and reputational risks for IFM providers and their enterprise clients. Coor explicitly identified cybersecurity integration in smart buildings as a top IFM market trend, noting that advancements in IoT and machine learning are simultaneously driving the need for stronger operational technology security frameworks.

Regulatory divergence across jurisdictions including GDPR in Europe, sector-specific data protection requirements in healthcare and defense and evolving national cybersecurity frameworks creates compliance complexity that elevates service delivery costs and extends procurement timelines, structurally constraining the pace of IFM adoption.

Opportunity - Emerging Markets and National Development-Led FM Demand

Rapid economic development, large-scale infrastructure buildout, and government-driven smart city initiatives across South Asia, Southeast Asia, and the Middle East are creating a substantial and underserved demand base for professional Integrated Facility Management services. This opportunity is rooted in the structural transition of these economies from informal, fragmented facility operations toward consolidated, compliance-driven, and technology-enabled service delivery.

Saudi Arabia exemplifies this opportunity through its Vision 2030 national transformation agenda, which is generating demand for world-class facility management across new urban projects, commercial real estate, and public infrastructure. JLL's acquisition of a significant stake in The Saudi Facility Management Company (FMTECH), a portfolio company of the Public Investment Fund (PIF), directly reflects the strategic value of gaining market position ahead of large-scale FM demand activation in the Kingdom.

In India, the Integrated Facility Management Market is supported by government capital expenditure of US$ 133 billion in FY 2024-25, with PMAY-U having sanctioned 1.18 crore houses and completed 86.6 lakh units, generating sustained residential and commercial FM demand across urban and peri-urban geographies. These emerging markets collectively represent the highest-growth geographical opportunity for IFM providers capable of scaling both service delivery infrastructure and digital platform capabilities simultaneously.

Technology-Enabled Service Convergence and Platform-Based Business Models

The convergence of IoT, digital twins, AI-driven analytics, and cloud-based facility management platforms is creating a transformative opportunity to shift the Integrated Facility Management Market from labor-intensive service delivery to scalable, platform-enabled operations that generate recurring revenue, superior margin profiles, and measurable outcome guarantees.

Surbana Jurong's deployment of one of Singapore's largest Digital IFM platforms at Temasek Polytechnic covering a 30-hectare campus with 49 buildings and integrating over 3,000 IoT sensors into a digital twin system for real-time HVAC, occupancy, and facility monitoring demonstrates the operational maturity this model can achieve at institutional scale.

YY Group's acquisition of the Managing Facilities Applications platform, rebranded as 24IFM, projects S$17.04 million in revenue contribution from subscription-based services including facility bookings, automated invoicing, and property insights illustrating the financial viability of platform-led IFM in high-density real estate markets. The shift toward outcome-based contracts, service marketplaces, and AI-driven operational transparency is enabling providers within the Integrated Facility Management Market to differentiate through technology stacks rather than labor arbitrage alone.

Category-wise Analysis

Solution Type Insights

The services segment dominates the global market, accounting for approximately 72% of the total market share in 2026. This leadership reflects the deeply service-intensive nature of IFM delivery, where enterprises across industries outsource a broad array of facility functions, including housekeeping, technical maintenance, security, HVAC management, waste management, and compliance to specialized providers under unified contracts. The integrated service model's value lies in consolidating multiple vendor relationships into a single accountable partner, delivering cost efficiency, operational simplicity, and performance consistency.

SILA's emphasis on a unified service delivery model that consolidates housekeeping, maintenance, security, HVAC, and waste management under a single contract reflects the architecture of this dominant segment, with demand increasingly characterized by real-time monitoring, automated reporting, and centralized accountability. ELITE PROPERTY's analysis further highlights IFM's strategic role in real estate, consolidating building maintenance, energy management, IT infrastructure, and compliance under a unified framework as asset portfolios become more complex and stakeholder expectations around sustainability and occupant experience intensify. Services will continue to anchor the integrated facility management market's revenue base as enterprise outsourcing deepens across emerging markets and institutional clients.

Integrated facility management platforms represent the fastest-growing solution category driven by enterprises seeking to shift from input-based FM procurement to outcome-driven, data-transparent operational management. These platforms integrate AI analytics, IoT sensor networks, digital twin capabilities, workflow automation, and compliance management into a single interface, enabling operators to monitor and optimize facility performance in real time across multi-site portfolios.

Application Insights

Manufacturing holds the leading end-use position in the Global Integrated Facility Management Market, with approximately 18% of total market share in 2026. Manufacturing facilities present some of the highest FM complexity among all end-use verticals, requiring the integration of technical maintenance, safety compliance, production environment management, energy optimization, and multi-shift operational support. The sector's global scale spanning automotive, electronics, pharmaceuticals, food processing, and heavy industry creates a structurally large and relatively captive demand base for specialized industrial IFM.

Leadec's IFM contract wins in Mexico and Brazil with an international technology and service company underscore how manufacturing's multi-geography operational footprint demands scalable, standardized FM frameworks underpinned by digital compliance tracking. Crisil Ratings' projection of 10 to 12% revenue growth for India's organised IFM sector specifically identifies manufacturing and warehousing among the primary demand drivers, supported by expanding factory footprints and stricter operational and safety compliance mandates. These dynamics position manufacturing as the highest-density revenue segment within the Integrated Facility Management Market, where contract values, renewal rates, and technical complexity are highest.

IT and Telecom is the fastest-growing end-use segment in the Integrated Facility Management Market, propelled by the sector's rapid physical infrastructure expansion, including data centers, hyperscale computing facilities, 5G network deployment, and corporate technology campuses, all of which generate high-intensity, continuous FM requirements around power management, cooling systems, physical security, and operational uptime.

Regional Insights and Trends

East Asia Integrated Facility Management Market Trends

East Asia accounts for approximately 18% of the Global Integrated Facility Management Market, with China, Japan, and South Korea collectively driving regional demand through rapid urban infrastructure development, digital economy expansion, and manufacturing modernization. China's digital ecosystem, which reached 1.108 billion internet users by December 2024 with internet penetration at 78.6% and 1.105 billion mobile internet users, is simultaneously generating vast smart building and IFM demand across commercial districts, hyperscale data centers, and industrial parks.

The deployment of 5G infrastructure and gigabit fiber broadband across both urban and rural China is advancing IoT-enabled building management adoption, while emerging applications, including online healthcare, connected vehicles, and generative AI used by 249 million users in China, are creating new facility types requiring professional IFM frameworks. In Japan and South Korea, the aging workforce is structurally accelerating demand for technology-substituted FM service delivery, as labor availability constrains traditional service models. South Korea's high-density smart city initiatives and Japan's corporate governance reforms mandating operational transparency are further embedding IFM platforms as strategic assets within the facility management procurement decisions of regional enterprises.

North America Integrated Facility Management Market Trends

North America leads the Global Integrated Facility Management Market with approximately 28% of total share, driven by the world's largest commercial real estate base, high enterprise FM outsourcing penetration, and sustained infrastructure investment across public and private sectors. The US construction sector recorded total spending of US$ 2.2 trillion in 2024 equivalent to 4.5% of GDP, with 1.6 million new homes completed and more than 8.2 million construction industry employees, generating a continuously expanding portfolio of managed facilities. The United States hosts the headquarters of the largest global IFM providers including CBRE, JLL, and Cushman and Wakefield, whose technology platforms, particularly CBRE's Nexus AI are setting global benchmarks for AI-enabled facility performance optimization. With US internet penetration approaching 93% in line with high-income country averages per ITU standards, North American enterprises operate within a fully digitized environment where IoT-enabled smart buildings and data-driven FM are standard expectations rather than differentiating features.

The region's technology sector, including hyperscale cloud providers, semiconductor manufacturers, and telecommunications operators is generating unprecedented IFM demand from data center construction, 5G tower deployments, and enterprise campus expansions, creating a premium service tier within the Integrated Facility Management Market where technology integration depth determines contract value and renewal probability.

Europe Integrated Facility Management Market Trends

Europe holds approximately 22% of the Global Integrated Facility Management Market, supported by strong regulatory drivers, advanced digital infrastructure, and the EU's broad sustainability and digital transformation agenda. In 2025, Eurostat confirmed that 94% of EU individuals used the internet, with 74% using mobile devices for connectivity and one in three individuals using generative AI tools, digital maturity levels that create robust enterprise demand for AI-enabled, outcome-based IFM services.

The EU's ICT sector generates €667 billion in value added across 1.4 million enterprises, with Germany alone contributing over 22% of EU-wide sectoral value added, underscoring the scale of corporate real estate and technology facility portfolios requiring integrated management. IoT adoption across EU enterprises runs at 56% penetration in large enterprises for general connected applications, with condition-based maintenance IoT usage at 44% in large enterprises versus 22% in small enterprises, a structural driver for IFM platform adoption.

The EU's regulatory environment, including GDPR, the Energy Performance of Buildings Directive, and net-zero building mandates, creates mandatory compliance requirements that are most efficiently addressed through integrated facility management frameworks, reinforcing enterprise procurement of IFM over fragmented vendor models. JLL's acquisition of a stake in FMTECH under Saudi Arabia's PIF reflects the broader cross-border IFM investment strategy European players are executing to leverage digital platform capabilities in high-growth adjacent geographies.

Competitive Landscape

The global integrated facility management (IFM) market is moderately consolidated in nature, dominated by a group of large multinational service providers that manage extensive global portfolios across commercial, industrial, healthcare, and infrastructure sectors. Key players such as CBRE Group, Inc., JLL, ISS A/S, Sodexo, Compass Group, and G4S (now part of Allied Universal) hold significant market shares due to their integrated service models and technology-driven capabilities. These companies compete on digital innovation, sustainability integration, bundled service offerings, and long-term enterprise contracts.

Despite the dominance of global leaders, regional and specialized providers remain active, particularly in emerging markets, contributing to competitive intensity. Mergers, acquisitions, and AI-enabled facility solutions are further shaping the market structure, reinforcing scale advantages at the top tier.

Key Developments:

- In December 2025, JLL announced the acquisition of a significant stake in The Saudi Facility Management Company (FMTECH), a portfolio company of Public Investment Fund (PIF), with PIF retaining a majority shareholding. The transaction strengthens JLL’s Integrated Facility Management footprint in Saudi Arabia by combining its global operational and digital FM platforms with FMTECH’s local market presence, aiming to enhance service quality, operational efficiency, and technology-driven transparency across the Kingdom’s rapidly expanding real estate and infrastructure sectors.

- In August, 2023, CBRE announced the large-scale deployment of its AI-powered Smart Facilities Management (FM) Solutions across more than 20,000 Global Workplace Solutions client sites, covering approximately 1 billion sq. ft. Powered by its Nexus AI platform, the solution leverages advanced analytics and building data to optimize maintenance workflows, reduce maintenance costs and energy consumption by up to 20%, and lower technician dispatches by 25%, marking a significant digital transformation milestone in the Integrated Facility Management market.

Companies Covered in Integrated Facility Management Market

- CBRE Group Inc

- Jones Lang LaSalle IP Inc.

- Sodexo Inc.

- ISS Facility Service

- EMCOR Facility Services

- Facilicom

- CBM Qatar LLC.

- Compass Group PLC

- Cushman and Wakefield

- AHI Facility Services Inc

Frequently Asked Questions

The global Integrated Facility Management Market is projected to be valued at US$ 123.2 Bn in 2026.

The Services (Traditional IFM packages) segment is expected to account for approximately 72% of the Global Integrated Facility Management Market by solution in 2026.

The integrated facility management market is expected to witness a CAGR of 7.8% from 2026 to 2033.

The Global Integrated Facility Management Market is driven by rapid digital transformation and AI-powered smart building adoption, expanding urban infrastructure and real estate development, and rising sustainability mandates that require energy-efficient, data-driven, and performance-based facility operations.

Key opportunities in the integrated facility management market lie in emerging economies driven by large-scale infrastructure and smart city investments (notably India and Saudi Arabia), alongside the rapid adoption of IoT, digital twins, AI-driven analytics, and platform-based IFM models that enable scalable, outcome-based, and recurring revenue service frameworks.

Key players in the Integrated Facility Management Market include CBRE Group, Inc., JLL, ISS A/S, Sodexo, Compass Group, and G4S (now part of Allied Universal).