- Food Packaging

- Ice Cream Packaging Market

Ice Cream Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Ice Cream Packaging Market By Material (Plastic, Paper & Paperboard, Others), Product Type (Cups, Stick packs, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

Ice Cream Packaging Market Size and Trends Analysis

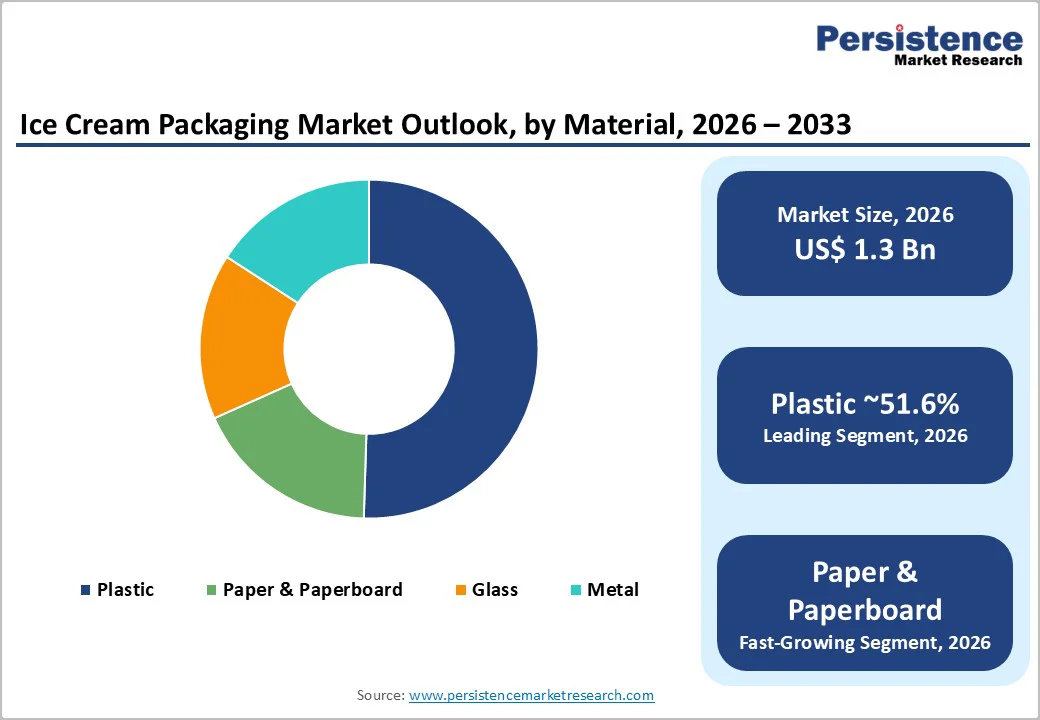

The global ice cream packaging market size is likely to be valued at US$1.3 billion in 2026. It is expected to reach US$1.8 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033, driven by rising global ice-cream consumption, broader retailer assortment strategies that favor both family-sized tubs and on-the-go single-serve formats, and a sustained industry shift toward sustainable packaging materials that balance barrier performance with recyclability.

Rising demand from convenience retail and e-commerce fulfillment is driving the need for durable, insulated, and resealable packaging. The market structure includes global packaging leaders, regional converters, and niche players focused on compostable and repulpable solutions.

Key Industry Highlights

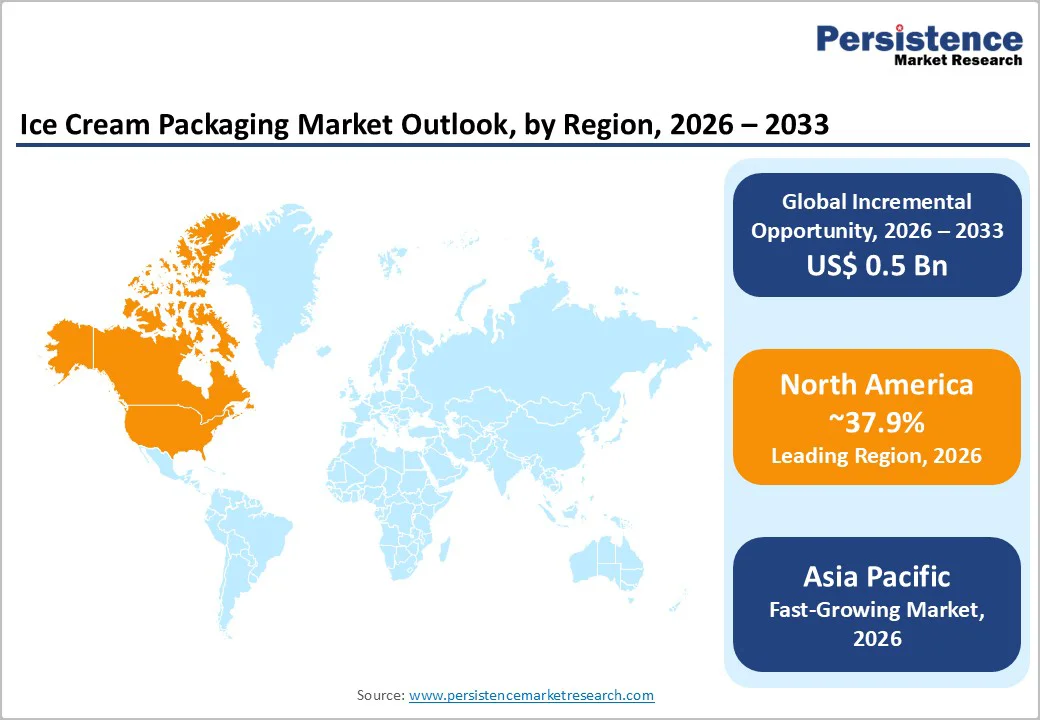

- Leading Region: North America is projected to account for 37.9% market share, supported by high per-capita ice-cream consumption, advanced cold-chain infrastructure, strong private-label penetration, and sustained demand for premium and impulse packaging formats across the U.S.

- Fastest-growing Region: Asia Pacific, driven by rising disposable incomes, rapid urbanization, expanding modern retail, and increasing consumption of single-serve and stick-based ice-cream products in China, India, and Southeast Asia.

- Investment Plans: Capital allocation is increasingly directed toward recyclable and fiber-based packaging solutions, including repulpable paper coatings, mono-material plastic structures, and lightweight high-barrier laminates, particularly in North America and Europe, to meet regulatory and retailer-led sustainability targets.

- Dominant Material: Plastic materials are anticipated to hold 51.6% market share, maintaining leadership due to cost efficiency, superior moisture and vapor barrier performance, lightweight logistics advantages, and compatibility with high-speed ice-cream filling and sealing lines.

- Leading Product Type: Cups are estimated to account for approximately 35.2% market share, driven by versatility across retail and foodservice channels, strong suitability for impulse and takeaway consumption, high SKU turnover, and extensive use in private-label and branded ice-cream offerings.

| Key Insights | Details |

|---|---|

| Ice Cream Packaging Market Size (2026E) | US$1.3 Bn |

| Market Value Forecast (2033F) | US$1.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Regulatory Pressure Driving Material Substitution

Consumers and regulators are accelerating a structural shift away from multi-layer, difficult-to-recycle packaging toward mono-material, fiber-based, and certified compostable alternatives. Packaging manufacturers are actively launching compostable ice-cream cups and paperboard tubs designed to replace traditional plastic-lined formats, demonstrating commercial readiness across multiple markets.

Regulatory pressure, particularly from single-use plastic restrictions and expanding Extended Producer Responsibility frameworks, is increasing end-of-life costs for non-recyclable materials and encouraging eco-design principles. As a result, sustainable packaging formats command higher average selling prices, while packaging suppliers are redirecting R&D investment toward advanced barrier coatings and fiber-compatible technologies.

Expansion of On-The-Go Consumption and Retail Channel Evolution

Retailers and foodservice operators are broadening their single-serve and impulse-oriented ice-cream offerings, including cups, stick packs, and small tubs, driven by convenience, snacking behavior, and premium single-serve launches. These formats represent a substantial share of packaging volumes due to high SKU turnover and frequent replenishment cycles.

At the same time, the growth of e-commerce and home delivery requires packaging engineered for transport durability, leak resistance, and thermal protection. This trend is increasing demand for insulated liners, cold-chain compatible tubs, reclosable lids, and secondary protective packaging systems.

Cold-Chain Expansion and Product Premiumization

The expansion of cold-chain infrastructure in developing markets, combined with the proliferation of premium and artisanal ice cream products, is driving demand for differentiated structural packaging. Laminated tubs, metallized finishes, and high-quality printing are increasingly used to reinforce premium brand positioning while protecting product integrity under frozen conditions.

Premium packaging formats generate higher per-unit revenues but also increase technical complexity for converters, requiring investment in barrier coatings, lamination processes, and cold-stable adhesives. Ongoing investment in coating and barrier innovation supports shelf-life extension and enables premium fiber-based packaging solutions.

Barrier Analysis - Cost and Performance Trade-Offs In Sustainable Materials

Transitioning to recyclable or compostable substrates often increases unit costs and may compromise moisture and oil barrier performance unless advanced coatings are applied. Packaging manufacturers face higher raw material costs, equipment modification expenses, and process inefficiencies during the conversion process.

In some cases, sustainable coatings increase unit costs by a meaningful margin compared to legacy laminates. Price pressure from private-label ice-cream products and commoditized single-serve formats limits the ability to fully pass these costs to customers, slowing adoption in price-sensitive markets.

Cold-Chain and Logistics Complexity

Ice-cream packaging must maintain performance under frozen storage and transportation conditions. Certain emerging materials, particularly uncoated fiber substrates, underperform in high-moisture environments unless combined with specialized linings.

Supply constraints related to coating capacity, specialty laminates, and uneven recycling or composting infrastructure further increase operational risk. These challenges require capital investment or strategic partnerships to ensure a reliable supply and consistent performance across regions.

Opportunity Analysis - Paper-Based Tubs with Repulpable Coatings

There is a growing demand for fiber-based tubs that combine premium print quality with improved end-of-life outcomes. Repulpable and low-plastic coating technologies present a significant retrofit opportunity for existing tub formats.

If a meaningful share of global tub volume transitions to repulpable fiber solutions over the next decade, the addressable opportunity represents a substantial portion of overall packaging spend. Suppliers capable of commercializing high-speed coating technologies and securing long-term supply agreements with major ice-cream brands are positioned to capture outsized value. Recent pilot programs confirm technical feasibility at an industrial scale.

E-Commerce and Insulated or Returnable Packaging Solutions

As online grocery and direct-to-consumer ice-cream distribution expands, demand is rising for insulated, reusable, or returnable packaging systems. Brands can monetize reusable insulated carriers and subscription-based chilled delivery models to increase customer lifetime value.

Packaging converters can capture incremental revenue by supplying thermal inserts, insulated liners, and tamper-evident features tailored for last-mile delivery. Even a modest shift of total volume toward e-commerce justifies dedicated production capacity for insulated packaging components.

Category-wise Analysis

Material Insights

Plastic is expected to be the dominant material, accounting for 51.6% market share, due to its cost efficiency, superior moisture and vapor barrier performance, and adaptability to high-speed filling and sealing lines. It is extensively used across single-serve cups, stick wrappers, and laminated tubs, where maintaining product integrity under frozen conditions is critical.

Plastic formats such as polypropylene and polyethylene provide consistent performance during cold storage and transport while supporting tight tolerances for lids, seals, and tamper-evident features.

From a logistics perspective, plastic’s lightweight profile and low breakage risk reduce transportation costs and product loss, particularly in high-volume retail distribution. Large multinational ice-cream brands continue to rely on plastic tubs and cups for family packs and private-label offerings, where pricing competitiveness and supply reliability remain key decision factors.

Despite sustainability pressures, plastic retains a strong position in markets where recycling infrastructure and cost sensitivity influence material choice.

Paper and paperboard are likely to be the fastest-growing materials in ice-cream packaging, driven by increasing regulatory scrutiny on plastic waste and growing consumer preference for fiber-based packaging. Technological advancements in water-resistant, grease-resistant, and repulpable coatings now enable paper-based formats to withstand frozen environments without compromising structural integrity.

These innovations allow paperboard tubs and cups to perform effectively while improving end-of-life recyclability. Paper-based packaging is particularly gaining traction in premium and branded ice-cream segments, where high-quality printing, matte finishes, and natural aesthetics enhance shelf appeal.

In North America and Europe, several national and private-label brands have introduced paperboard tubs as alternatives to plastic-lined containers to align with sustainability commitments. Suppliers offering mono-material paper solutions with certified food-contact coatings are increasingly preferred by retailers seeking compliant and environmentally aligned packaging options.

Product Type Insights

Cups are expected to be the largest product type, accounting for 35.2% of the market share due to their versatility across multiple consumption occasions, including takeaway desserts, impulse purchases, and foodservice servings.

They are produced in a wide range of sizes, from small portion-controlled formats to mid-sized premium cups, supporting diverse pricing and branding strategies. Cups also offer excellent surface area for high-quality graphics, promotional messaging, and seasonal designs.

In foodservice and convenience retail environments, cups are favored for their ease of handling, stackability, and compatibility with lids and spoons. Major quick-service restaurants and convenience store chains rely heavily on cup-based formats for soft-serve, sundaes, and limited-edition flavors, driving consistent replacement demand. High SKU turnover and frequent promotional cycles further reinforce cups as a stable and high-volume packaging category.

Stick packs are likely to be the fastest-growing product type, supported by rising demand for portable, single-serve ice-cream formats suited for on-the-go consumption. Their compact size, lower price point, and ease of use make them popular in impulse retail locations such as convenience stores, vending machines, and travel hubs.

Stick packs typically use flexible, high-barrier laminates to prevent moisture ingress and flavor loss during frozen storage. Brands increasingly use stick-based formats to introduce novelty products, seasonal flavors, and multi-pack assortments with limited operational risk.

Chocolate-coated bars, layered ice-cream novelties, and portion-controlled dessert sticks are expanding in both developed and emerging markets, contributing to higher growth rates compared with traditional tubs and jars. The format’s strong alignment with impulse buying behavior continues to drive its accelerated adoption.

Regional Insights

North America Ice Cream Packaging Market Trends - Private-Label Scale and Sustainability-Led Material Optimization

North America is expected to be the leading regional market, accounting for approximately 37.9% of global ice-cream packaging demand, supported by high per-capita ice-cream consumption, advanced cold-chain logistics, and strong penetration of premium and impulse formats.

The U.S. dominates regional demand due to its mature supermarket and convenience retail infrastructure, as well as extensive private-label activity from major retailers such as Walmart, Costco, and Kroger. These private-label programs require high-volume, cost-efficient packaging formats, reinforcing continued demand for plastic cups, tubs, and multilayer stick wrappers.

Regulatory oversight from the U.S. Food and Drug Administration governs food-contact materials, recycled content usage, and coating compliance, raising qualification costs for new packaging solutions. At the same time, retailer-led sustainability initiatives are reshaping material choices.

For example, Unilever’s North American ice-cream brands have transitioned several tub formats to recyclable polypropylene and reduced pigment use to improve recyclability, prompting suppliers to prioritize mono-material designs.

Investment activity in the region increasingly targets repulpable paper coatings, plastic-reduction initiatives, and lightweight barrier structures, particularly for premium pints and single-serve cups. Packaging converters with strong R&D and regulatory expertise continue to gain preference among brand owners navigating evolving compliance and sustainability requirements.

Europe Ice Cream Packaging Market Trends - Regulation-Driven Shift toward Fiber-Based and Circular Packaging

Europe represents a high-value and regulation-driven ice-cream packaging market, shaped by stringent packaging waste directives, extended producer responsibility schemes, and ambitious recycling targets. The European Union’s harmonized regulatory framework has accelerated the shift toward fiber-based and recyclable packaging formats, particularly in Western Europe.

Germany and the U.K. lead the adoption of paperboard tubs and recyclable plastic alternatives, supported by advanced collection and recycling infrastructure. At the same time, France and Spain show strong demand for premium, design-led packaging aligned with artisanal and indulgent positioning.

Several major European ice-cream producers have adjusted packaging strategies in response to regulatory pressure. Nestlé has rolled out paper-based ice-cream tubs across multiple European markets, replacing traditional plastic containers to meet recyclability commitments, directly influencing supplier demand for coated paperboard solutions.

Private-label ice-cream ranges in the U.K. have also increased the use of simplified mono-material lids and reduced the use of composite structures. Investments across the region focus on fiber-based barrier technologies, recyclable flexible films for stick packs, and circular supply-chain partnerships that integrate packaging producers with waste-management operators. Compliance-driven innovation remains a defining feature of Europe’s ice-cream packaging landscape.

Asia Pacific Ice Cream Packaging Market Trends - Rapid Consumption Growth Supported by Local Manufacturing Expansion

Asia Pacific is estimated to be the fastest-growing regional market for ice-cream packaging, driven by rising disposable incomes, urbanization, expanding middle-class consumption, and rapid growth of modern retail formats.

China, India, and Southeast Asia account for the majority of incremental demand, supported by expanding domestic ice-cream brands and increasing penetration of single-serve and impulse products. Japan remains a premium-focused market, where packaging quality, portion control, and visual presentation are critical differentiators.

Regional growth is reinforced by ongoing investment in cold-chain infrastructure and large-scale local manufacturing. In China, leading domestic ice-cream brands have expanded production capacity for stick-based and novelty formats, increasing demand for high-barrier flexible laminates and cost-efficient wrappers.

In India, the rapid growth of impulse ice-cream brands has driven higher consumption of small cups and stick packs optimized for affordability and high-volume distribution.

Southeast Asian markets benefit from converter cost advantages and fast customization cycles, enabling rapid brand launches. However, regulatory frameworks vary significantly across countries, requiring localized packaging strategies that balance cost, performance, and evolving waste-management capabilities, shaping material choices differently across the region.

Competitive Landscape

The global ice cream packaging market is moderately concentrated, with global packaging companies supplying large brands alongside numerous regional converters serving local markets. Competitive differentiation increasingly centers on sustainable materials, high-speed printing, food-contact compliance, and cold-chain expertise.

Consolidation favors suppliers with advanced coating capabilities and scale advantages. Leading players focus on sustainable material innovation, regional capacity expansion, and channel-specific packaging solutions. Key differentiators include regulatory compliance capabilities, circularity documentation, and cold-chain performance expertise.

Key Industry Developments

- In July 2025, Huhtamaki announced the launch of new compostable ice-cream cups made from certified paperboard with a bio-based barrier coating, reducing plastic content to less than 10% while maintaining performance, expanding sustainable packaging options for global ice-cream brands.

- In April 2025, Sealed Air entered a strategic collaboration with Tetra Pak to co-develop recyclable, paper-based ice-cream cups and lids, aiming to replace traditional plastic-coated formats and accelerate the adoption of circular packaging structures.

Companies Covered in Ice Cream Packaging Market

- Amcor Plc

- Berry Global Group, Inc.

- Huhtamaki Oyj

- Sonoco Products Company

- Tetra Laval Group

- Stora Enso

- Graphic Packaging International

- Dart Container

- Winpak Ltd.

- Sealed Air Corporation

- StanPac Inc.

- ITC Packaging

- Insta Polypack

- Sirane Group

Frequently Asked Questions

The global ice cream packaging market is estimated to be valued at US$1.3 billion in 2026, supported by steady demand from retail, foodservice, and impulse ice-cream consumption across developed and emerging markets.

By 2033, the ice cream packaging market is forecast to reach US$1.8 billion, driven by expanding cold-chain infrastructure, growth in premium and single-serve ice cream formats, and increasing adoption of sustainable packaging solutions.

Key trends include rising adoption of recyclable and fiber-based packaging, increased use of mono-material plastic structures, growing demand for single-serve and stick-based formats, and higher investment in barrier technologies that maintain product integrity under frozen conditions while improving sustainability performance.

Plastic packaging is the leading material segment, accounting for approximately 51.6% of total market share, due to its cost efficiency, strong moisture and vapor barrier properties, and widespread use across cups, tubs, and stick wrappers.

The ice cream packaging market is projected to grow at a CAGR of 4.5% between 2026 and 2033, reflecting steady demand growth supported by innovation in sustainable materials, expansion in Asia Pacific, and continued strength in impulse and private-label ice cream segments.

Major players with strong packaging portfolios for frozen desserts include Amcor, Berry Global, Huhtamaki, Graphic Packaging International, and Sealed Air, each offering a broad range of rigid and flexible packaging solutions tailored to ice-cream applications.