- Electrical Equipment & Services

- Heat Detector Tester Market

Heat Detector Tester Market Size, Share, and Growth Forecast 2026 – 2033

Heat Detector Tester Market by Power Source (Battery Powered, Hardwired with Battery Backup, Others), Product Type (Smoke Detector Tester, Others), Application (Residential, Commercial, Industrial), and Regional Analysis 2026 – 2033

Heat Detector Tester Market Size, Share, and Trends Analysis

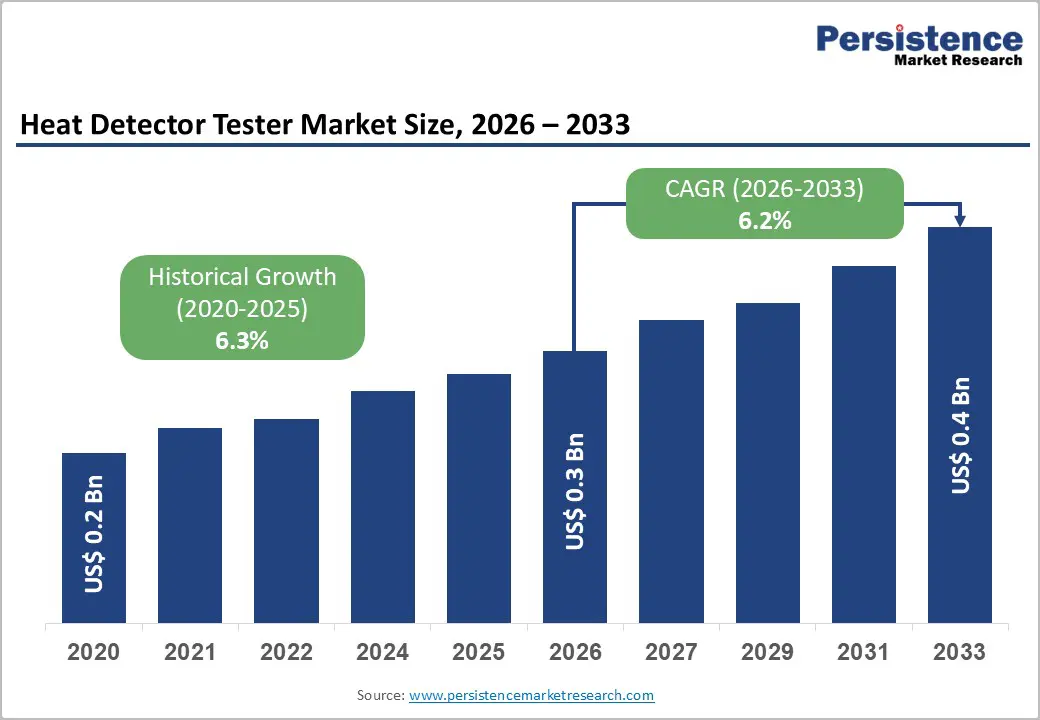

The global heat detector tester market size is likely to be valued at US$ 0.3 billion in 2026 and is expected to reach US$ 0.4 Bn by 2033, growing at a CAGR of 6.2% during the forecast period from 2026 to 2033, driven by stringent fire safety regulations mandated by organizations such as the National Fire Protection Association (NFPA) and International Code Council (ICC), requiring regular testing and maintenance of fire detection systems. Increasing construction activities in emerging economies, coupled with mandatory compliance standards for commercial and industrial facilities, are accelerating demand for reliable testing equipment. The rapid expansion of smart building infrastructure and the integration of IoT-enabled maintenance tools are compelling facility management firms to upgrade their testing equipment inventory.

Key Industry Highlights

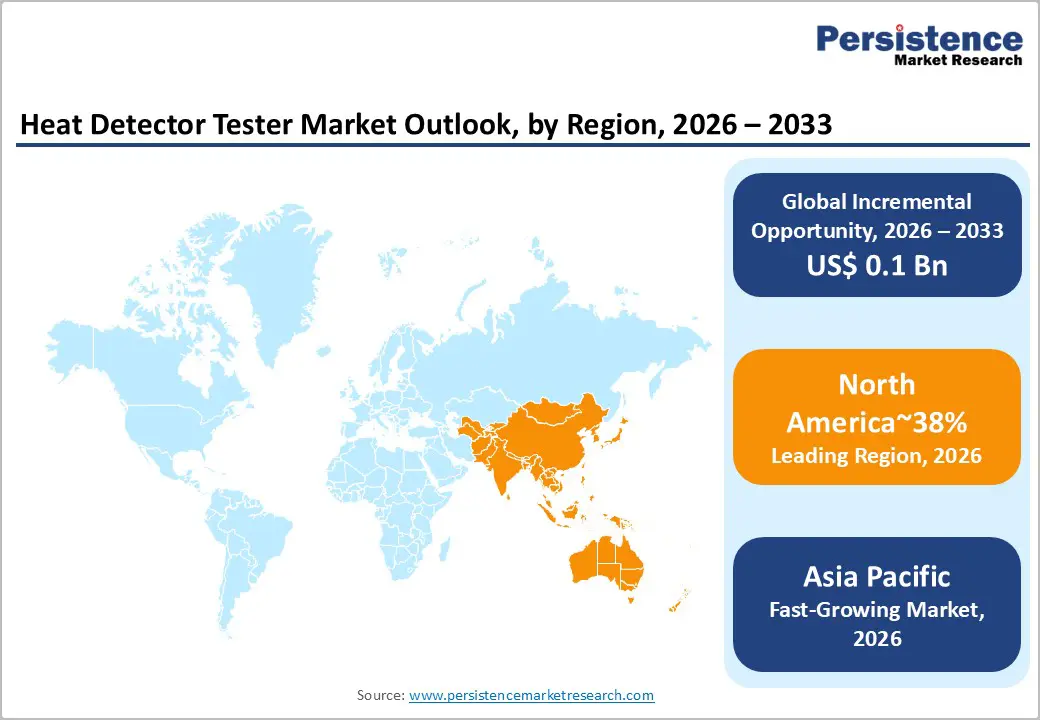

- Leading Region: North America is expected to lead with roughly 38% of global demand, anchored by mature regulatory frameworks, digital infrastructure, and early adoption of smart fire safety and compliance systems.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by urbanization, infrastructure expansion, stricter enforcement of fire safety codes, and rising adoption of cost-efficient and digitally enabled testers.

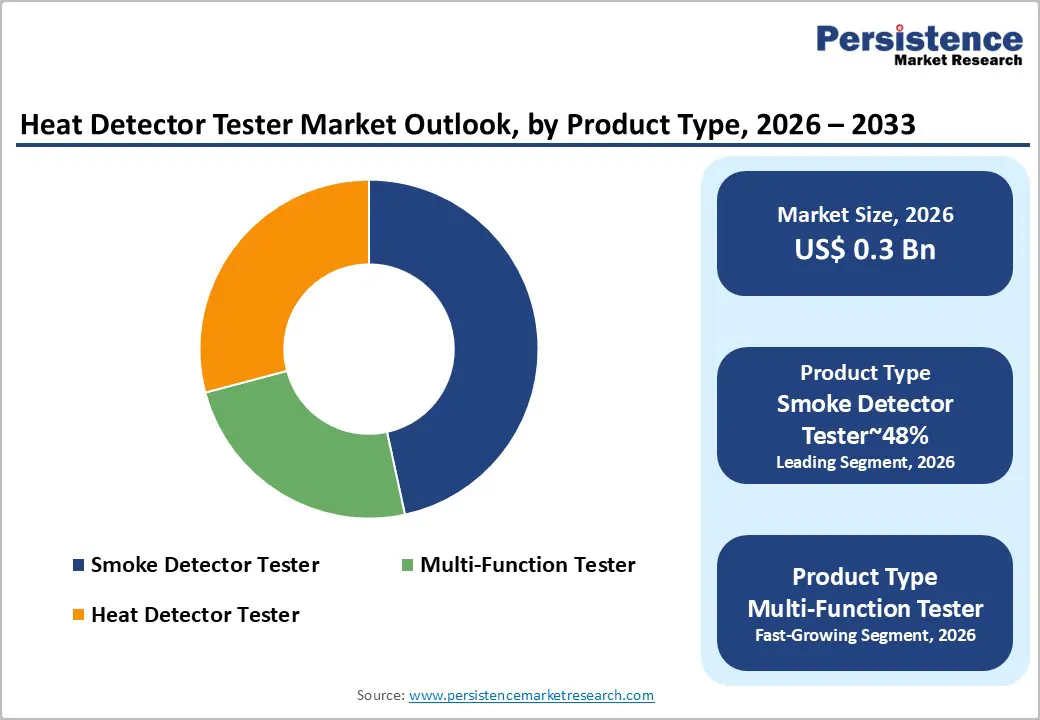

- Leading Product Type Smoke detector testers are estimated to lead, accounting for approximately 48% of the global demand, driven by regulatory mandates, high installation density across commercial and residential buildings, and recurring inspection cycles.

- Leading Power Source Type Hardwired with battery backup remains the leading configuration, representing around 62% share, anchored in regulatory compliance, integration with Building Management Systems, and uninterrupted operation during power outages.

- Key Industrial Development: In April 2025, Detectortesters launched the Testifire XTR2, a connected smoke/heat tester. The user bulletin highlighted the importance of app registration and integration, enabling seamless connected testing. This feature enhances accuracy, compliance, and efficiency by offering data logging and reporting for improved heat detector verification.

| Key Insights | Details |

|---|---|

|

Heat Detector Tester Market Size (2026E) |

US$0.3 Bn |

|

Market Value Forecast (2033F) |

US$0.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Proliferation of Multi-Sensor Fire Detectors and Testing Complexity

The accelerating adoption of multi-sensor fire detectors has become a key driver for the heat detector tester market. Modern fire alarm systems increasingly use combined optical smoke and heat sensors to improve detection accuracy and reduce nuisance alarms in complex environments like hospitals, airports, and high-rise buildings. However, this shift makes legacy testing methods, such as heat guns or hair dryers, obsolete and often insufficient for meeting manufacturer specifications and regulatory criteria.

This transition has fueled demand for advanced multi-function testers that can stimulate both heat and smoke sensors in a controlled, repeatable manner. For fire maintenance contractors, the ability to verify multiple detection parameters with a single device improves efficiency, reduces tool switching, and shortens testing time, resulting in significant productivity gains. In June 2025, SDi introduced the Testifire XTR2 at the NFPA Conference & Expo. This all-in-one connected tester provides functional testing and automated reporting, reducing errors and time while enhancing compliance documentation for heat detector maintenance.

Systemic Enforcement Gaps and Institutional Weakness in Emerging Markets

Limited regulatory enforcement and low institutional capacity present major barriers to the heat detector tester market in emerging economies. While fire safety codes exist, weak inspection systems, fragmented authority, and inconsistent penalties dilute their impact. Without routine audits or mandatory checks, compliance remains discretionary, allowing outdated testing practices to persist. This is further compounded by low awareness at the residential and small commercial levels, where testing is seen as optional. A shortage of trained fire safety technicians limits market development, leaving building operators without qualified service providers. This creates a cycle where weak enforcement hampers professionalization, and limited capacity undermines enforcement, leading to elongated sales cycles, fragmented demand, and price sensitivity.

Convergence with Predictive Maintenance and IoT-Enabled Facility Management

The shift from reactive servicing to predictive maintenance in large facilities presents a key opportunity for the heat detector tester market. As fire detection systems become critical to facility risk management, managers seek tools that offer continuous performance monitoring rather than just compliance checks. Next-gen testers that capture response time, thermal sensitivity, and test variances transform inspections into data-driven events, supporting early fault detection and lifecycle optimization.

This trend is boosted by the integration of IoT-enabled Building Management Systems (BMS), which allow fire safety data to be analyzed alongside other facility metrics such as energy use and occupancy. For manufacturers, this creates a move from hardware sales to recurring software-based revenue models, such as analytics subscriptions and predictive alerts. By embedding these testing tools into BMS platforms, suppliers position themselves for long-term growth as smart building infrastructure and data-driven maintenance become standard. In April 2025, Detectortesters launched connected solutions such as Testifire XTR2 and DT Connect, driving digital transformation in fire safety testing and enhancing predictive maintenance capabilities.

Category–wise Analysis

Power Source Type Insights

Hardwired with battery backup remains the leading power source configuration, accounting for approximately 62% share in 2026, reflecting its status as the regulatory and infrastructural standard across residential, commercial, and industrial fire safety systems. Its dominance is anchored in mandatory compliance with codes such as NFPA 72, which require secondary power continuity during outages, and its seamless integration with Building Management Systems for centralized monitoring.

Product evolution is focused on reliability rather than mobility, with a clear industry shift toward 10-year sealed lithium-ion backup batteries to eliminate routine maintenance and reduce failure risk. Widely deployed systems such as First Alert’s SMICO105-AC and Kidde’s HD135F exemplify this segment’s role in fixed, interconnected installations where uninterrupted operation and code adherence outweigh flexibility considerations.

Battery powered solutions are likely to be the fastest-growing power source type, driven by technician workflow optimization and the operational realities of modern inspection and maintenance environments. Cordless architectures eliminate trip hazards and mobility constraints during multi-story inspections, while advances in lithium-ion energy density now support all-day operation and extended vertical reach. Industrial parameters such as recharge cycles, portability index, and cross-device compatibility are shaping procurement decisions, particularly among professional service providers.

Tools such as the Solo 461 Cordless Kit, using modular battery batons for 9m-plus reach, and the Testifire 1001, which consolidates smoke, heat, and CO testing into a single battery-powered unit, illustrate how portability, multifunctionality, and digital readiness are redefining tester deployment standards.

Product Type Insights

Smoke detector testers are expected to be the leading product type, accounting for 48% share in 2026, underpinned by the sheer scale of regulatory mandates and installed base density across residential and commercial buildings. Fire codes such as NFPA 72 require routine testing of smoke alarms in nearly every occupied room, creating a structurally higher inspection frequency than any other detector type.

Volume demand is reinforced by the dominance of battery-powered residential smoke units, which drive recurring service cycles for contractors and housing authorities. Industrial momentum is evident in the shift toward non-flammable, HFC-free aerosol formulations such as the Solo A10, aligning compliance testing with tightening environmental regulations. A clear trend shaping this segment is the transition from basic functional checks to addressable system verification, with newer smoke testers integrating LCD feedback to confirm loop communication status in complex, networked fire alarm installations.

Multi-function testers are estimated to be the fastest-growing segment, reflecting accelerating demand for labor efficiency and digital compliance in mixed-detector environments. Facilities increasingly deploy smoke, heat, and CO detectors within the same asset footprint, favoring single-head platforms that eliminate tool changes and reduce equipment carry during inspections.

Products such as the Testifire 1001 and Testifire XTR2 exemplify this shift, combining multi-modal testing with Bluetooth and Wi-Fi connectivity to generate automated, timestamped maintenance logs. The defining trend is the rise of digital “proof of compliance,” driven by insurers and auditors that now recognize cloud-based testing records as a risk-reduction lever. This positions multi-function testers as operational infrastructure rather than standalone tools, embedding them directly into compliance and asset-management workflows.

Regional Analysis

North America Heat Detector Tester Market Trends

North America is expected to command the largest share of the heat detection systems market, accounting for approximately 38% of total demand in 2026. The region will retain its leadership due to a deeply embedded regulatory framework, advanced digital infrastructure, and early adoption of smart fire safety architectures. The U.S. will remain the primary growth engine, supported by continuous data center expansion, large-scale commercial retrofitting, and strict enforcement of NFPA-aligned building codes. Canada will sustain steady demand driven by cold-climate resilience requirements, while Mexico will see incremental growth from expanding industrial corridors and manufacturing investments. Across the region, regulatory consistency and liability-driven compliance will sustain high replacement and upgrade cycles.

Market growth will increasingly reflect modernization dynamics rather than new installations. Aging commercial and industrial infrastructure will drive sustained retrofit demand, particularly for digitally connected and documentation-enabled detection systems. Facility owners and insurers will push adoption of verifiable testing and predictive maintenance capabilities, reinforcing demand for advanced solutions. Innovation-led brands such as Honeywell, Johnson Controls, Siemens, and Potter Electric will shape product evolution by integrating IoT diagnostics, cybersecurity features, and building management interoperability. This convergence of regulation, liability pressure, and digital integration will keep North America structurally dominant through the forecast period.

Europe Heat Detector Tester Market Trends

Europe is anticipated to represent a mature and structurally stable market, accounting for approximately 34% of global demand, over the forecast period. The region will sustain its position through regulatory harmonization under EN 54 standards and strict national frameworks such as DIN 14675 in Germany, BS 5839 in the U.K., and aligned fire safety codes across France, Italy, and Spain. Germany will anchor regional demand due to its dense industrial base and widespread integration of automated safety systems within advanced manufacturing environments. The U.K. will continue to generate consistent replacement and retrofit demand across commercial buildings, high-rise residential stock, and data center infrastructure. France and Southern Europe will support steady volumes through compliance-driven upgrades in hospitality, healthcare, and public buildings.

Market evolution will focus on efficiency, sustainability, and productivity rather than volume expansion. European buyers will increasingly favor rechargeable, electronic heat testing solutions to reduce aerosol waste and battery disposal, aligning with environmental policy priorities. Labor shortages across Western Europe will accelerate the adoption of faster, technician-friendly testing tools. Innovation will remain regionally concentrated, with brands such as Detectortesters, Siemens, Bosch, and Honeywell shaping compact system design, wireless functionality, and building management integration. Retrofit-heavy demand, insurance-driven digital documentation requirements, and urban-centric deployment constraints will collectively reinforce Europe’s mature, compliance-led market trajectory.

Asia Pacific Heat Detector Tester Market Trends

Asia Pacific is expected to remain the fastest-growing regional market over the forecast period. Regional expansion will be driven by sustained urbanization, large-scale infrastructure programs, and rising enforcement of formal fire safety regimes across industrial and high-density residential assets. China is likely to continue dominating regional demand, supported by the nationwide implementation of GB 50116 across provincial jurisdictions and continuous additions to commercial, industrial, and public infrastructure.

Japan will maintain a technology-led, replacement-driven market profile, where amendments to the Fire Defense Law will reinforce structured testing documentation and accelerate upgrades toward automated, low-effort testing solutions. India is expected to emerge as the most dynamic growth engine, as National Building Code adoption, Smart Cities deployment, and stricter municipal enforcement progressively formalize testing practices across metros and Tier-1 cities.

The regional market will increasingly bifurcate by application and quality tier. China and parts of ASEAN are anticipated to support high-volume demand for cost-efficient, easy-to-operate testing tools aligned with large construction pipelines in manufacturing parks, transport infrastructure, and utilities. Japan, South Korea, Singapore, and Australia will continue to favor precision-oriented and digitally enabled equipment, reflecting mature compliance cultures and labor productivity constraints.

Asia Pacific is also likely to strengthen its role as a manufacturing base, with domestic brands expanding output and export reach, while Western brands retain influence in premium projects such as airports, data centers, and advanced industrial facilities. Overall growth will remain compliance-led, infrastructure-linked, and operationally pragmatic rather than innovation-saturated.

Competitive Landscape

The global heat detector tester market is moderately consolidated, with the top five players collectively controlling approximately 42 – 45% of the market. Detectortesters is the clear leader of the professional segment through its flagship brands Solo, Testifire, and Scorpion. The remainder of the market is fragmented among regional specialists and distributors such as SDi Fire in North America and Home Safeguard in Europe and APAC. Market positioning is bifurcated into premium/professional solutions, electronic, connected, IoT-enabled devices, and economy offerings, including aerosol and chemical testers. Premium players are increasingly focusing on technology-led solutions that integrate software ecosystems, while value-oriented suppliers compete on cost for price-sensitive institutional and small contractor segments.

Competitive dynamics are defined by differentiation in functionality, service, and compliance. Premium-tier manufacturers emphasize multi-functional features, IoT integration, and after-sales support, establishing strong loyalty among professional contractors who prioritize reliability and service network coverage. Institutional buyers, such as large facility operators and government agencies, favor solutions that ensure compliance certification and traceable testing documentation. Regional players maintain influence through localized distribution, tailored service offerings, and cost-competitive alternatives, particularly in emerging markets where price sensitivity and basic functionality drive adoption.

Key Industry Developments:

- In March 2025, Detectortesters Group acquired Global Vision Inc., strengthening its position in the fire test and measurement space. This acquisition expanded its technological capabilities and market presence in detector testing tools, including heat detectors, driving innovation and broader product offerings.

- In June 2025, SDi unveiled upgraded features for the DT Connect platform at NFPA 2025, including CSV uploads, asset filtering, and saved-site testing. These enhancements streamlined large-scale inspections, reduced manual entry, and enabled real-time PDF reports, improving workflow efficiency in heat detector testing.

- In September 2025, Detectortesters made the Testifire XTR2 widely available, following successful launch events. The product brought advanced connected testing to a broader user base, offering valuable insights and efficiency gains for heat detector compliance and maintenance.

Companies Covered in Heat Detector Tester Market

- Detectortesters

- SDi Fire

- Home Safeguard Industries, LLC

- Halma plc

- HSI Fire & Safety Group

- Scorpion (Detectortesters Brand)

- Enpro Safety

- Honeywell International Inc.

- Siemens AG

- Johnson Controls International plc

- Apollo Fire Detectors Ltd.

- System Sensor

- Hochiki Corporation

- Notifier

- Edwards Signaling

Frequently Asked Questions

The global heat detector tester market is projected to be valued at US$ 0.3 billion in 2026 and is expected to reach US$ 0.4 billion by 2033, driven by stringent fire safety regulations and the expansion of smart building infrastructure.

Growth is fundamentally driven by strict fire safety mandates from organizations such as the NFPA and ICC, which require regular testing and maintenance of fire detection systems, alongside increasing construction and the need for compliance in commercial and industrial facilities.

The heat detector tester market is forecast to grow at a CAGR of 6.2% from 2026 to 2033, reflecting steady demand from ongoing safety compliance and facility management upgrades.

Asia Pacific is the fastest-growing regional market, fueled by rapid urbanization, infrastructure expansion, stricter enforcement of fire safety codes, and the rising adoption of cost-efficient and digitally enabled testing equipment.

The heat detector tester market is moderately consolidated, with Detectortesters being the clear leader through brands such as Solo and Testifire. Other key players include SDi, Honeywell, Johnson Controls, and Siemens.