- Non-food Packaging

- Healthcare Rigid Plastic Packaging Market

Healthcare Rigid Plastic Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Healthcare Rigid Plastic Packaging Market by Materials (Polypropylene (PP), Polyethylene (PE), Others), Packaging Types (Bottles, Boxes, Others), Applications, and Regional Analysis for 2026 - 2033

Healthcare Rigid Plastic Packaging Market Size and Trends Analysis

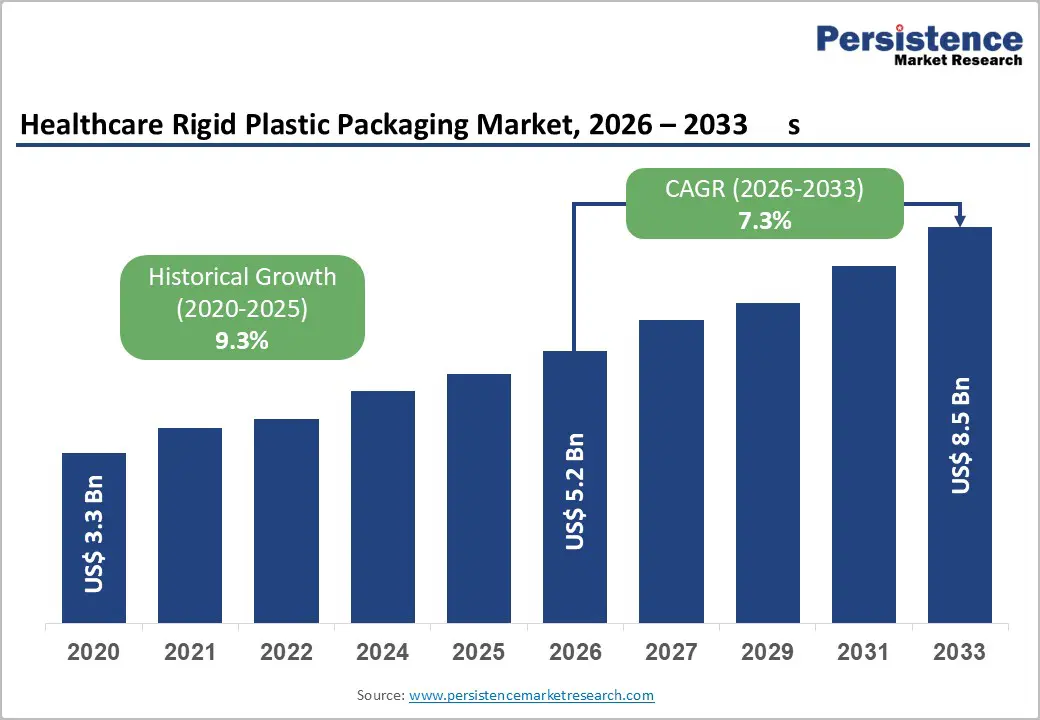

The global healthcare rigid plastic packaging market size is likely to be valued at US$5.2 billion in 2026 and is expected to reach US$8.5 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033, driven by rising pharmaceutical output, increased biologics commercialization, and stronger regulatory enforcement around sterility and traceability.

Demand for cost-efficient polymers such as polypropylene (PP) and polyethylene (PE), combined with large-scale manufacturing capacity in Asia Pacific, sustains competitive pricing and scalable supply. Structural healthcare expansion, regulatory compliance requirements, and innovation in medical-grade polymers collectively underpin long-term growth stability.

Key Industry Highlights:

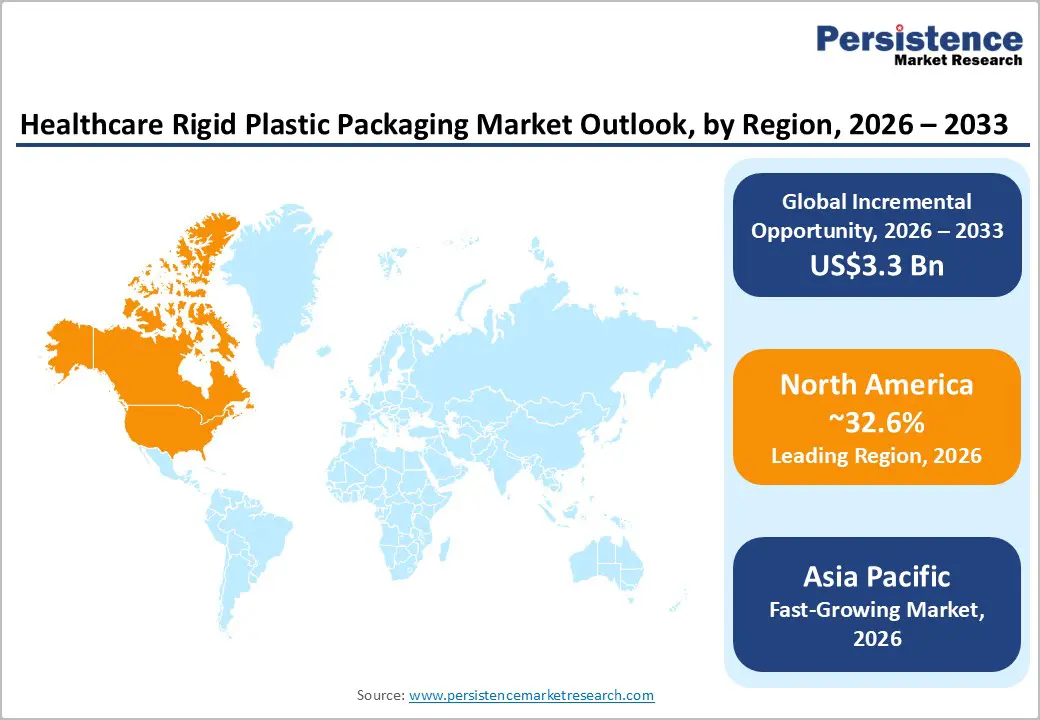

- Leading Region: North America is projected to account for approximately 32.6% of market share, supported by strong pharmaceutical innovation, biologics production expansion, and stringent U.S. FDA container-closure compliance standards.

- Fastest-growing Region: Asia Pacific leads growth momentum with the highest projected CAGR, driven by expanding pharmaceutical manufacturing in China and India, localized sterile packaging investments, and rising cleanroom-certified production capacity.

- Investment Plans: Major packaging players are expanding healthcare-focused cleanroom capacity and consolidating market presence. The announced acquisition of Berry Global by Amcor in 2024 reflects strategic scale-building, while regional investments emphasize sterilization validation and sustainable polymer integration.

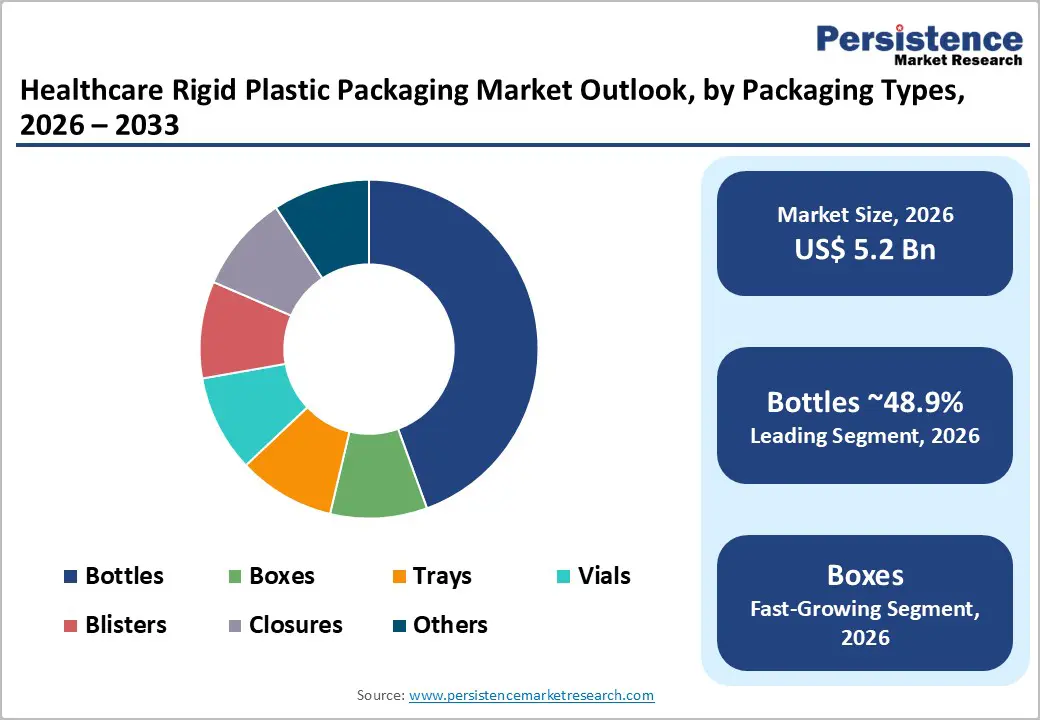

- Dominant Materials: Polypropylene (PP) leads the materials segment with an anticipated 39.3% market share, driven by cost efficiency, chemical resistance, and compatibility with sterilization processes and injection molding.

- Leading Packaging Type: Bottles are estimated to account for over 48.9% of market share, supported by high-volume oral solid and liquid pharmaceutical demand, established global supply chains, and regulatory familiarity.

| Key Insights | Details |

|---|---|

| Healthcare Rigid Plastic Packaging Market Size (2026E) | US$5.2 Bn |

| Market Value Forecast (2033F) | US$8.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Biologics, Injectables, and Single-Use Medical Devices

The pharmaceutical industry continues shifting from traditional small-molecule drugs to biologics, biosimilars, and complex injectable therapies. These products require specialized sterile primary packaging systems such as vials, syringes, rigid trays, and closures manufactured from validated medical-grade plastics. Biologics typically demand higher-value packaging due to sensitivity to moisture, light, and contamination. Single-use medical devices and combination products further increase packaging complexity, integrating drug delivery systems with protective rigid components. As pharmaceutical companies prioritize safety, sterility, and traceability, rigid plastic packaging solutions capable of aseptic compatibility and barrier integrity capture premium pricing and steady demand. This structural transition strengthens long-term growth visibility across the healthcare value chain.

Stringent Regulatory and Sterility Requirements

Regulatory authorities worldwide enforce strict standards for container-closure integrity, sterility assurance, and labeling compliance. Updated guidelines for sterile medical devices and pharmaceutical products require manufacturers to validate packaging materials against extractable, leachable, and microbial contamination risks. These requirements elevate the importance of certified rigid plastic systems compatible with sterilization technologies such as ethylene oxide (EO), gamma irradiation, and e-beam processing. As compliance complexity increases, pharmaceutical companies and contract packagers prefer established suppliers with audited facilities and proven validation expertise. This regulatory rigor raises average selling prices, encourages investment in cleanroom production infrastructure, and strengthens the competitive advantage of suppliers capable of delivering regulatory engineering support alongside physical packaging products.

Sustainability Mandates and Circular Economy Transition

Environmental regulations and corporate ESG commitments are reshaping packaging material selection. Governments increasingly promote recyclability, reduced plastic waste, and minimum recycled-content targets. Healthcare packaging presents unique challenges because sterility and patient safety cannot be compromised. Suppliers are also investing in mono-material rigid designs, chemical recycling technologies, and certified post-consumer recycled (PCR) resins that meet medical-grade requirements. Pharmaceutical procurement teams increasingly evaluate sustainability credentials during supplier selection. Rigid plastic manufacturers that develop recyclable formats while maintaining regulatory compliance gain competitive positioning advantages. Sustainability-driven innovation thus evolves from a compliance obligation into a strategic growth lever within the healthcare packaging ecosystem.

Barrier Analysis - High Validation and Compliance Costs

Healthcare packaging suppliers must comply with rigorous regulatory standards, including cleanroom manufacturing, sterilization validation, and extensive documentation for extractables and leachables testing. These requirements involve significant capital expenditure in certified facilities and quality management systems. Product qualification timelines can extend between 6 and 18 months, increasing time-to-market and development costs. Smaller converters face financial barriers in upgrading infrastructure and maintaining regulatory audits. The high cost of compliance limits new entrants, narrows supplier pools for complex sterile formats, and reinforces market concentration among established players with robust validation capabilities.

Raw Material Volatility and Supply Chain Risks

Medical-grade polymers such as polypropylene, polyethylene, and polycarbonate rely on petrochemical feedstocks subject to price fluctuations and geopolitical disruptions. Resin supply constraints can extend lead times and increase procurement uncertainty. For validated packaging formats, any material substitution requires requalification, further complicating supply management. Sudden resin price spikes can reduce margins by several percentage points if cost pass-through mechanisms are delayed. These structural risks require suppliers to maintain diversified sourcing strategies and long-term procurement agreements to mitigate financial volatility.

Opportunity Analysis - Conversion from Glass to High-Performance Polymers

Although glass remains dominant for many injectable drugs, high-performance polymers such as polycarbonate and engineered polypropylene increasingly serve as viable alternatives in selected applications. Advantages include lighter weight, shatter resistance, improved design flexibility, and compatibility with integrated delivery systems. Even a modest conversion of 5-10% from glass-based primary packaging to validated rigid plastic systems during the 2026-2033 period would generate several hundred million dollars in incremental market demand. Suppliers investing in regulatory dossiers and polymer innovation stand to capture conversion-driven growth, particularly in biologics and combination-device packaging.

Localization of Supply Chains in Emerging Markets

Asia Pacific and parts of Eastern Europe are expanding domestic pharmaceutical and medical device production. Localized manufacturing of biosimilars and generic injectables increases demand for regionally compliant rigid packaging solutions. Procurement strategies increasingly prioritize supply resilience and shorter lead times. Capturing 20-30% of incremental annual rigid packaging demand in fast-growing APAC markets presents meaningful growth potential. Strategic investments in certified cleanroom facilities and localized quality teams enable suppliers to secure long-term partnerships with multinational pharmaceutical firms and domestic producers.

Category-wise Analysis

Materials Insights

Polypropylene (PP) is anticipated to account for approximately 39.3% of market share in 2026 over the forecast period, maintaining its leadership position. Its dominance stems from cost efficiency, strong chemical resistance, thermal stability, and compatibility with high-speed injection molding and thermoforming processes. PP demonstrates reliable performance under sterilization methods such as ethylene oxide (EO) and selected autoclave conditions, making it suitable for pharmaceutical and device-related applications.

Manufacturers widely use PP in bottles for oral solid doses, diagnostic sample containers, closures, caps, and rigid trays for medical devices. For example, child-resistant caps for prescription medications and tamper-evident closures frequently rely on medical-grade PP due to its strength-to-weight ratio and durability. In device packaging, PP trays protect surgical instruments during sterilization and transportation. Medical-grade PP formulations with certified drug-contact compliance and low extractable profiles further support its adoption across regulated pharmaceutical environments. Its balance of affordability, processing flexibility, and validated performance ensures sustained leadership in the materials segment.

Polyethylene (PE) is anticipated to witness the fastest growth within the materials category. Demand growth is driven by increasing use of blow-molded bottles, rigid containers for liquid formulations, and barrier-enhanced packaging formats. High-density polyethylene (HDPE) offers excellent moisture resistance, chemical stability, and impact strength, making it suitable for syrups, topical medications, and diagnostic reagents.

For example, HDPE bottles are commonly used for over-the-counter (OTC) liquid medications and antiseptic solutions due to their lightweight and shatter-resistant properties. Co-extrusion technologies incorporating oxygen or moisture barrier layers enhance PE’s suitability for sensitive formulations. Innovations in low-extractable and medical-grade PE resins further expand their application in sterile packaging systems. Its compatibility with established recycling streams also aligns with sustainability mandates, strengthening long-term growth prospects across pharmaceutical and diagnostic packaging applications.

Packaging Types

Bottles are anticipated to retain over 48.9% share in 2026 within healthcare applications, reinforcing their dominant position. High-volume oral solid medications and liquid pharmaceutical formulations drive consistent demand for blow-molded plastic bottles. These bottles are typically paired with tamper-evident, child-resistant, and induction-sealed closures to ensure product safety and regulatory compliance.

For instance, prescription pill bottles and OTC vitamin containers predominantly use HDPE or PP bottles due to durability and cost efficiency. In hospital settings, rigid bottles also serve as secondary containment for certain sterile products. Their scalability in mass production, dimensional accuracy, and well-established supply chains support cost optimization. Pharmaceutical distributors favor bottle formats because of ease of labeling, serialization integration, and compatibility with automated filling lines. These factors collectively sustain the segment’s market leadership.

Rigid boxes and protective enclosures are anticipated to be the fastest-growing packaging type during the forecast period. Growth is particularly strong in medical device and procedure kit packaging, where product protection, sterility, and organization are critical. Precision thermoformed trays and rigid casings protect implantable devices, surgical tools, and diagnostic instruments from mechanical damage and contamination.

For example, orthopedic implant kits and catheter delivery systems are frequently packaged in custom rigid trays with compartmentalized layouts that facilitate operating-room efficiency. These formats integrate sterile barriers, labeling compliance, and tamper-evidence features. Compared to standard bottles, protective enclosures command a higher per-unit value due to engineering complexity and validation requirements. Suppliers capable of offering customized design solutions, integrated sterilization compatibility, and rapid prototyping gain a competitive advantage, contributing to faster revenue expansion within this segment.

Regional Insights

North America Healthcare Rigid Plastic Packaging Market Trends - Biologics-Driven Sterile Packaging Expansion and FDA Compliance

North America is projected to lead, holding approximately 32.6% of market share in 2026, led by the U.S., which anchors the region through its strong pharmaceutical innovation ecosystem, advanced biologics production capacity, and mature contract packaging infrastructure. Major drug developers such as Pfizer, Johnson & Johnson, and Moderna continue expanding biologics and injectable portfolios, increasing demand for validated sterile rigid packaging components, including bottles, trays, and closures. The U.S. also hosts a dense network of contract development and manufacturing organizations (CDMOs), which rely on compliant, high-throughput rigid packaging systems to meet regulatory timelines.

Regulatory oversight from the U.S. Food and Drug Administration reinforces strict container-closure integrity standards and sterilization validation requirements. This environment favors suppliers with ISO 13485-certified cleanroom facilities and established sterilization compatibility. Strategic consolidation has further reshaped the competitive landscape. Amcor announced the acquisition of Berry Global, strengthening its North American healthcare packaging footprint and expanding medical-grade rigid capabilities. The transaction reflects ongoing scale-driven competition and investment in sterile production capacity. Sustainability initiatives are also influencing procurement.

Companies such as West Pharmaceutical Services continue investing in high-performance containment solutions for injectable drugs, while packaging leaders expand PCR-compatible rigid formats in response to pharmaceutical ESG targets. Cleanroom expansions across U.S. manufacturing hubs, including the Midwest and Northeast, support increased domestic sourcing. Companies entering this market must prioritize regulatory readiness, validated sterilization pathways (EO, gamma, e-beam), and sustainable polymer integration to compete effectively.

Europe Healthcare Rigid Plastic Packaging Market Trends - EU Regulatory Harmonization and Sustainable Medical-Grade Polymer Innovation

Europe maintains a significant share of the healthcare rigid plastic packaging market, supported by advanced medical device manufacturing and precision polymer engineering capabilities. Germany leads in high-precision medical component production, with companies such as Gerresheimer expanding pharmaceutical containment systems that include both glass and engineered plastic solutions. Germany’s strong medtech ecosystem supports demand for thermoformed trays and protective rigid enclosures used in implantable and surgical device packaging. The regulatory framework shaped by the European Union’s updated packaging and medical device regulations has increased compliance requirements related to recyclability, traceability, and conformity assessment. These rules directly affect healthcare rigid plastics, encouraging mono-material designs and PCR integration.

For example, SCHOTT and other containment suppliers have emphasized advanced polymer innovations to complement traditional materials and align with sustainability directives. Similarly, pharmaceutical packaging operations in the U.K. and France increasingly integrate lifecycle environmental assessments into procurement criteria. Investment trends reflect environmental alignment. Converters across Spain and Central Europe have expanded certified cleanroom capacity while pursuing recyclable rigid tray solutions for device OEMs. European customers now assess environmental impact alongside sterility and performance standards, pushing suppliers toward validated PCR resins and chemical recycling collaborations. This regulatory harmonization elevates compliance costs but strengthens long-term innovation and differentiation opportunities within the region.

Asia Pacific Healthcare Rigid Plastic Packaging Market Trends - Pharmaceutical Localization and Cost-Competitive Sterile Manufacturing Growth

Asia Pacific is the fastest-growing region in the market, supported by rapid pharmaceutical capacity expansion and cost-competitive manufacturing. China continues scaling biologics and injectable production, driving demand for sterile rigid bottles, trays, and protective enclosures. Domestic pharmaceutical leaders and multinational manufacturers operating in China increasingly localize packaging procurement to reduce lead times and improve supply chain resilience. In India, government initiatives promoting domestic pharmaceutical manufacturing and biosimilar development have strengthened demand for regionally compliant packaging systems. Indian CDMOs expand sterile filling and packaging capabilities, increasing consumption of validated rigid plastic components.

Japan focuses on high-precision polymer technologies and advanced device packaging. Japanese manufacturers emphasize engineering excellence in thermoformed trays and protective enclosures for diagnostic and implantable devices. Global packaging companies have responded with regional investments. Firms such as Amcor and Berry Global have expanded healthcare manufacturing capabilities across Asia Pacific to support multinational pharmaceutical clients. Regional governments encourage foreign direct investment in healthcare manufacturing zones, reinforcing localization strategies. The combination of lower production costs, expanding pharmaceutical output, and growing regulatory alignment with international standards positions Asia Pacific as a strategic growth engine. Suppliers that establish validated cleanroom facilities and regulatory support teams within the region gain a competitive advantage in serving both domestic producers and global healthcare brands seeking diversified supply chains.

Competitive Landscape

The global healthcare rigid plastic packaging market demonstrates moderate concentration. Global packaging leaders compete alongside regional specialized thermoformers. High regulatory barriers limit new entrants in the sterile packaging segments. Consolidation through mergers and acquisitions enhances scale, technology capabilities, and sustainability investments. Competitive differentiation centers on regulatory compliance, sterilization expertise, and innovation in recyclable medical-grade polymers.

Leading companies emphasize regulatory differentiation, sustainable polymer development, and geographic expansion. Investment in validated cleanroom capacity, PCR-capable materials, and integrated kitting services enhances competitive positioning. Strategic consolidation supports scale efficiencies and broader healthcare customer coverage.

Key Industry Developments:

- In October 2025, Olympus partnered with DuPont to incorporate DuPont’s Tyvek with RA material into the sterile packaging of more than 100 categories of single-use medical devices from 2026, aiming to reduce waste and enhance material performance.

Companies Covered in Healthcare Rigid Plastic Packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- SCHOTT AG

- AptarGroup, Inc.

- Sealed Air Corporation

- Constantia Flexibles

- Sonoco Products Company

- Alpla Group

- Nipro Corporation

- Bormioli Pharma S.p.A.

- Tekni-Plex, Inc.

- Plastipak Holdings, Inc.

- UFP Technologies, Inc.

- Silgan Holdings Inc.

- DuPont

- Honeywell International Inc.

Frequently Asked Questions

The global healthcare rigid plastic packaging market is likely to be valued at US$5.2 billion in 2026.

The healthcare rigid plastic packaging market is expected to reach US$8.5 billion by 2033.

The healthcare rigid plastic packaging market is projected to grow at a CAGR of 7.3% between 2026 and 2033.

Key trends include increasing adoption of polypropylene (PP) and high-density polyethylene (HDPE) for sterile pharmaceutical packaging and integration of PCR (post-consumer recycled) content in compliance with sustainability mandates.

Among materials, polypropylene (PP) leads with approximately 39.3% market share, owing to its cost efficiency and sterilization compatibility. Within packaging types, bottles dominate with over 48.9% share, supported by high-volume oral solid and liquid pharmaceutical applications.

Major companies include Amcor plc, Berry Global Group, Inc., Gerresheimer AG, West Pharmaceutical Services, Inc., and SCHOTT AG.