- Food Ingredients & Additives

- Green Banana Flour Market

Green Banana Flour Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Green Banana Flour Market by Product Type (Organic and Conventional), Indications (Spray Dried, Sun-Dried, Freeze-Dried, Others), Sales Channel (Convenience Store, Specialty Store, and Online Retailers), and Regional Analysis for 2026 to 2033

Green Banana Flour Market Share and Trend Analysis

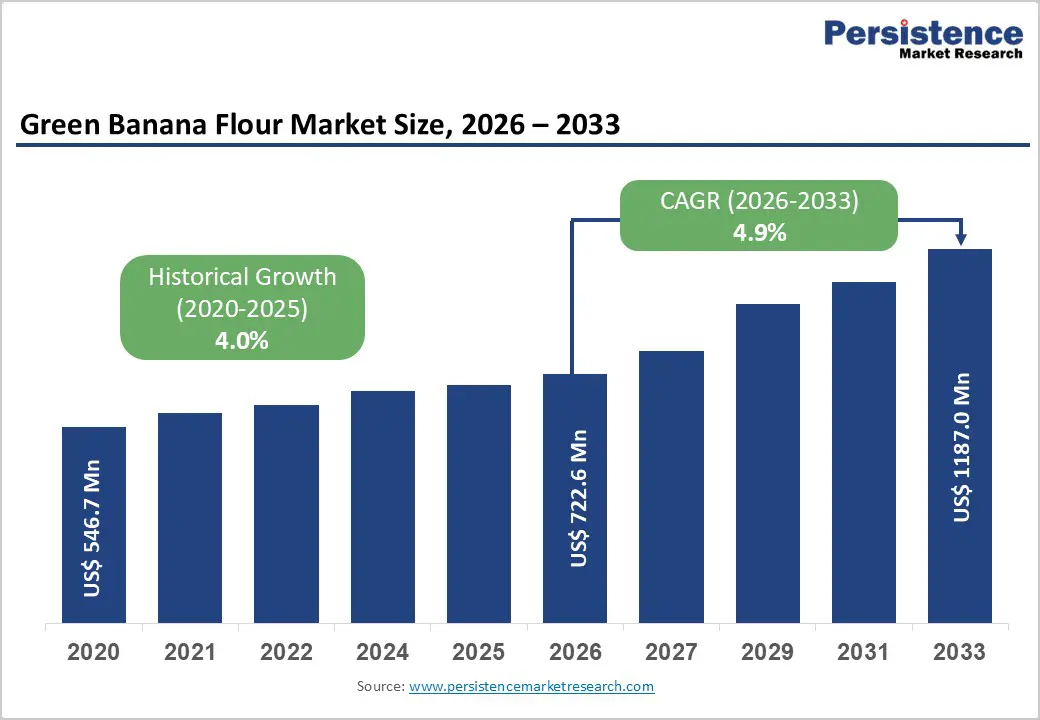

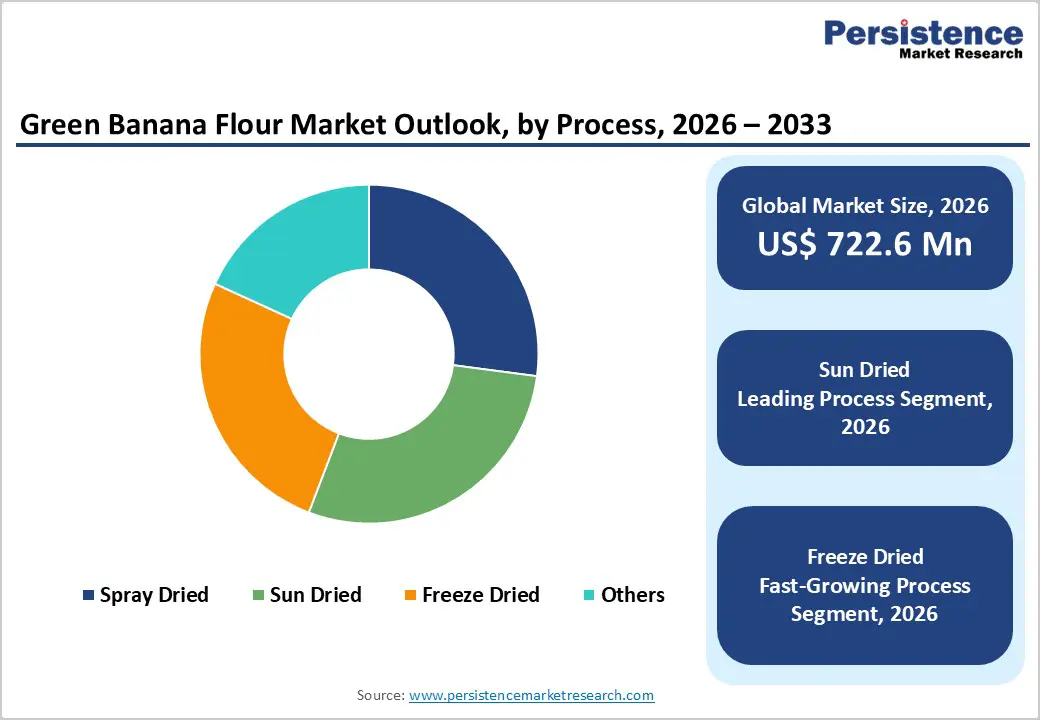

The global green banana flour market size is estimated to grow from US$ 722.6 million in 2026 to US$ 1187.0 millin by 2033. The market is projected to record a CAGR of 4.9% during the forecast period from 2026 to 2033.

Global demand for green banana flour is rising steadily, driven by increasing consumer preference for gluten-free alternatives, growing awareness of digestive health, and expanding demand for functional food ingredients. Consumers are increasingly incorporating resistant starch-rich foods into their diets to support gut microbiome balance, glycemic control, and metabolic health. Green banana flour is gaining traction across bakery, beverage, snack, and dietary supplement applications due to its clean-label positioning and plant-based origin. Rising incidence of lifestyle-related conditions such as obesity and diabetes, along with broader adoption of preventive nutrition strategies, is reinforcing sustained demand.

Key Industry Highlights:

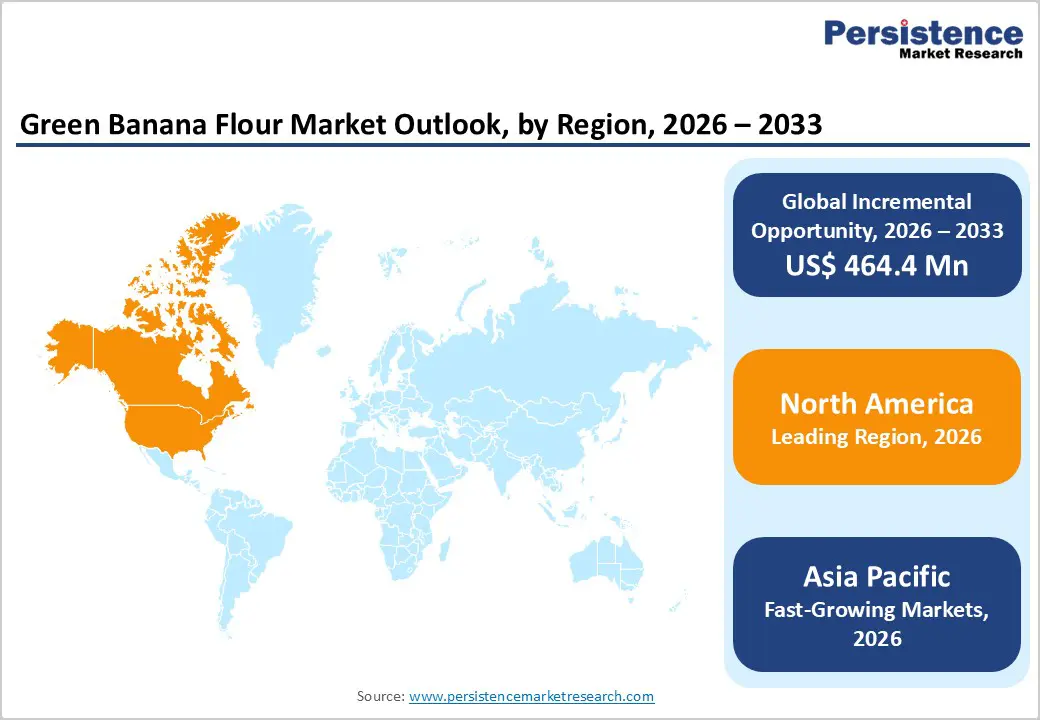

- Leading Region: North America holds the largest share at 46.7%, supported by strong consumer awareness of gluten-free and functional foods, advanced food processing infrastructure, high health-conscious population density, established retail networks, and the presence of major specialty flour manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid urbanization, rising disposable incomes, increasing health awareness, a strong banana production base, and expanding food processing capabilities.

- Leading Product Segment: Conventional products are dominant due to cost efficiency, wider availability, scalability for industrial food production, and strong integration into mainstream gluten-free bakery and snack formulations.

- Fastest-Growing Product: Organic products are expanding rapidly as demand increases for certified clean-label, non-GMO, and sustainably sourced ingredients among premium health-focused consumers.

- Leading Process Segment: Sun-dried remains the top application, driven by low production cost, widespread adoption in banana-producing regions, minimal capital requirements, and strong alignment with traditional and minimally processed food trends.

- Fastest-Growing Process Segment: Freeze-dried is scaling quickly due to increasing demand for premium-quality flour with higher nutrient retention, improved texture functionality, longer shelf life, and suitability for high-value functional and nutraceutical applications.

| Key Insights | Details |

|---|---|

| Green Banana Flour Market Size (2026E) | US$ 722.6 Mn |

| Market Value Forecast (2033F) | US$ 1187.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.0% |

Market Dynamics

Driver - Rising Demand for Gluten-Free, Functional, and Gut-Health-Oriented Food Ingredients

Increasing consumer focus on preventive healthcare and functional nutrition is a primary force accelerating demand for green banana flour globally. Growing awareness of digestive health, glycemic control, and clean-label diets has significantly boosted interest in resistant starch-rich ingredients. Green banana flour is widely recognized for its prebiotic properties, low glycemic index, and suitability for gluten-free formulations, making it attractive for health-conscious consumers and individuals with celiac disease or gluten sensitivity. The expanding prevalence of lifestyle-related disorders such as obesity, diabetes, and metabolic syndrome further amplifies demand for functional carbohydrate alternatives. Food manufacturers are incorporating green banana flour into bakery products, snacks, beverages, and dietary supplements to enhance fiber content and improve nutritional profiles.

Rising adoption of plant-based diets and minimally processed ingredients also strengthens market momentum. Additionally, growing urbanization, increased disposable incomes, and the rapid expansion of modern retail and e-commerce platforms are improving product accessibility. As food companies increasingly prioritize reformulation strategies to reduce refined wheat dependency and enhance functional value, green banana flour is emerging as a strategic ingredient rather than a niche substitute.

Restraints - Supply Chain Constraints, Price Volatility, and Limited Consumer Awareness in Emerging Regions

Despite strong growth potential, several structural challenges continue to restrain broader market penetration. Green banana flour production depends heavily on agricultural yield, seasonal availability, and climate conditions in banana-producing regions. Fluctuations in raw banana supply, post-harvest losses, and transportation inefficiencies can disrupt manufacturing consistency and impact pricing stability. Processing infrastructure limitations, particularly in developing economies, may affect product quality standardization and scalability. While sun-dried and small-scale production methods reduce capital requirements, they can lead to variability in moisture content and resistant starch levels.

Additionally, organic certification and export compliance requirements increase operational costs for producers targeting premium markets. Consumer awareness remains uneven across regions, especially in price-sensitive markets where conventional wheat flour alternatives dominate. Limited knowledge regarding resistant starch benefits and digestive health advantages may restrict mass-market adoption. Competition from other gluten-free and functional flours, such as almond, coconut, and cassava flour, further intensifies pricing pressure. These combined factors create entry barriers and may slow market expansion in less mature food ecosystems.

Opportunity - Product Innovation, Functional Food Expansion, and Emerging Market Penetration

Evolving consumer dietary patterns and food innovation trends are opening substantial opportunities for the green banana flour market. Increasing demand for functional foods, fortified bakery products, plant-based snacks, and nutraceutical blends is creating new application avenues. Manufacturers are exploring customized flour blends with enhanced fiber content, improved texture functionality, and optimized resistant starch retention to differentiate product offerings. Rapid expansion of e-commerce grocery platforms and direct-to-consumer health brands provides scalable distribution opportunities, particularly for specialty and organic variants. Emerging markets present strong long-term growth potential due to rising middle-class populations, improving food processing infrastructure, and growing awareness of preventive nutrition.

Government initiatives supporting agro-processing, food export development, and value-added agricultural products further strengthen supply chain capabilities. Innovation in sustainable sourcing, eco-friendly packaging, and clean-label certifications enhances brand positioning in premium markets. Strategic partnerships between ingredient suppliers, food manufacturers, and private-label retailers are expanding product integration across mainstream food categories. As consumer preference shifts toward natural, fiber-rich, and metabolically beneficial ingredients, green banana flour is well-positioned to benefit from both volume expansion in staple food reformulation and value growth in specialized functional nutrition applications.

Category-wise Analysis

By Product Type, Conventional Leads Due to Cost Efficiency, Wider Availability, and Industrial-Scale Adoption

The conventional segment is projected to dominate the global green banana flour market in 2026, capturing a revenue share of 71.7%. This leadership is primarily driven by its cost-effectiveness, broader raw material availability, and suitability for large-scale food manufacturing applications. Conventional green banana flour is widely used in bakery, snacks, beverages, and thickening applications due to stable supply chains and competitive pricing. Food manufacturers prefer conventional variants for bulk procurement, consistent starch composition, and compatibility with gluten-free product formulations. Compared to organic alternatives, conventional products offer higher production volumes and lower certification costs, making them attractive for private-label brands and mass-market distribution. Their integration into mainstream retail and foodservice channels further strengthens adoption. Continuous improvements in processing efficiency and quality standardization, combined with rising demand for gluten-free and functional food ingredients, reinforce the dominance of the conventional segment globally.

By Process, Sun-Dried Leads Due to Cost-Effectiveness and Traditional Processing Preference

The sun-dried segment is expected to lead the global green banana flour market in 2026, accounting for a 30.0% revenue share. This dominance is driven by its low processing cost, widespread use in banana-producing regions, and minimal technological requirements. Sun drying remains a preferred method among small- and mid-scale processors due to reduced capital investment and energy consumption. The method preserves resistant starch content effectively while maintaining natural product positioning, which aligns with clean-label trends. Many manufacturers in Latin America, Africa, and the Asia Pacific rely on sun drying to produce bulk volumes for export markets. Additionally, growing demand for minimally processed and traditionally prepared functional ingredients supports segment expansion. Its affordability and scalability continue to sustain leadership within the processing category.

By Sale Channel, Online Retailers Lead Due to Expanding E-commerce Penetration and Health-Focused Consumer Buying

Online retailers are projected to dominate the global green banana flour market in 2026, capturing a 55.0% revenue share. This leadership is driven by increasing consumer preference for purchasing specialty health ingredients through digital platforms. Green banana flour is often positioned as a functional, gluten-free, and gut-health-supporting product, making it highly visible on e-commerce marketplaces and health-focused websites. Online channels provide broader product variety, consumer reviews, subscription models, and direct-to-consumer brand engagement. Manufacturers benefit from reduced intermediary costs and targeted digital marketing strategies. The growth of cross-border e-commerce and rising health-conscious urban populations further strengthen this channel’s dominance. Additionally, private-label and niche organic brands leverage online platforms for faster market penetration, reinforcing sustained expansion.

Regional Insights

North America Green Banana Flour Market Trends

North America is expected to dominate the global green banana flour market in 2026, accounting for a 46.7% value share, largely driven by the United States. The region benefits from high consumer awareness regarding gluten intolerance, digestive wellness, and metabolic health, which has accelerated the adoption of alternative flours rich in resistant starch. The increasing prevalence of celiac disease, non-celiac gluten sensitivity, and lifestyle-driven dietary shifts toward plant-based nutrition continues to stimulate demand across retail and foodservice channels.

The U.S. market demonstrates strong penetration in gluten-free bakery, functional snacks, smoothie blends, and dietary supplement formulations. Consumers actively seek clean-label, non-GMO, and minimally processed ingredients, positioning green banana flour as a premium functional carbohydrate source. Well-established food processing infrastructure, sophisticated cold chain logistics, and mature e-commerce ecosystems further support market scalability. Additionally, private-label brands and specialty health retailers are expanding shelf space for alternative flours, enhancing accessibility. Continuous product innovation, including fortified and blended flour variants, combined with strong digital marketing and direct-to-consumer strategies, reinforces North America’s sustained market leadership.

Europe Green Banana Flour Market Trends

Europe’s green banana flour market is expected to witness steady growth in 2026, supported by increasing demand for organic, allergen-free, and sustainably sourced food ingredients. Countries including Germany, the U.K., France, Italy, Spain, and the Netherlands represent key consumption hubs due to their well-developed health food sectors and high regulatory standards for food safety and labeling transparency. European consumers demonstrate strong preference for certified organic and ethically sourced products, encouraging manufacturers to align with EU organic certification frameworks and sustainable sourcing practices. The bakery and specialty bread segment remains a major application area, particularly for gluten-free artisan products and functional snack innovations.

Additionally, the growing vegan and flexitarian population supports demand for plant-based flour alternatives. Retail distribution is dominated by specialty health stores, organic supermarkets, and expanding online grocery platforms. Stringent traceability requirements and sustainability initiatives, including eco-friendly packaging and carbon footprint reduction, significantly influence procurement strategies. Furthermore, food manufacturers across Europe are integrating resistant starch ingredients into reformulation strategies aimed at improving fiber content and glycemic response. These structural factors contribute to stable long-term market expansion across the region.

Asia Pacific Green Banana Flour Market Trends

The Asia Pacific green banana flour market is projected to register a higher CAGR of around 6.6% between 2026 and 2033, positioning it as the fastest-growing regional market. Growth is driven by expanding food processing industries, rising disposable incomes, urbanization, and increasing consumer awareness regarding digestive health and functional foods. Countries such as China, India, Japan, South Korea, and Australia are witnessing heightened demand for gluten-free and plant-based ingredients, particularly among urban middle-class populations. The region benefits from abundant banana cultivation in countries such as India, the Philippines, Indonesia, and Thailand, enabling cost-efficient raw material sourcing and local value addition. Governments are increasingly supporting agro-processing initiatives, food export programs, and small-scale food manufacturing enterprises, strengthening domestic production capabilities. Modern retail expansion, rapid growth of online grocery platforms, and rising cross-border trade are enhancing product accessibility.

Additionally, multinational and regional manufacturers are investing in processing facilities and strategic partnerships to scale operations and meet export-quality standards. Increasing adoption in bakery reformulations, nutraceutical blends, infant nutrition products, and diabetic-friendly food applications further accelerates demand. These structural, demographic, and economic factors collectively position Asia Pacific as the primary growth engine for the global green banana flour market over the forecast period.

Competitive Landscape

The global green banana flour market is highly competitive, with strong participation from Natural Evolution Green, NuNaturals Ltd., Kanegrade, Woodland Foods, and Banamin Healthcare. These players leverage diversified sourcing networks across banana-producing regions, integrated processing capabilities, strong relationships with food manufacturers and health-focused retailers, and continuous innovation in gluten-free formulations, resistant starch optimization, clean-label positioning, and functional ingredient development to cater to bakery, beverage, dietary supplement, and infant nutrition applications.

Rising consumer awareness of gut health, increasing demand for gluten-free and plant-based alternatives, growth in functional food consumption, and expanding health-conscious populations are driving product innovation in the market. Manufacturers are focusing on organic certifications, minimally processed and sustainably sourced variants, improved solubility and texture profiles, private-label collaborations, and e-commerce expansion, while strengthening distribution in emerging markets and sustaining R&D investments to deliver nutritionally enhanced, application-specific, and value-added green banana flour solutions.

Key Industry Developments:

- In April 2025, Terova launched NuBana™, a new portfolio of green banana powders designed to support innovation across food, beverage, and nutraceutical applications. This gluten-free ingredient enhances formulations while promoting gut health, without the digestive tolerance concerns often linked to other fiber sources. NuBana™ reflects Terova’s focus on quality, transparency, and responsible sourcing, providing manufacturers with a multifunctional ingredient delivering both health and performance advantages.

- In July 2024, International Agriculture Group (IAG) introduced NuBana N200 Green Banana Flour, a high-resistant starch ingredient containing a minimum of 65% RS2. The product supports digestive and metabolic health, with moderate intake (10-15 grams daily) promoting regularity, satiety, and fat metabolism, while higher consumption (20-35 grams) enhances insulin sensitivity and overall gut health benefits.

Companies Covered in Green Banana Flour Market

- Natural Evolution Green

- NuNaturals Ltd.

- Kanegrade

- Woodland Foods

- Banamin Healthcare.

- NihKan

- Stawi Foods

- SOL ORGANICA, S.A.

- Alami Global

- OrgFarm

- Homefresh Organics

- Pure & Sure

- Great Earth Pty Ltd.

- TOOTSI IMPEX Inc.

- Others

Frequently Asked Questions

The global green banana flour market is projected to be valued at US$ 722.6 Mn in 2026.

Increasing consumer demand for gluten-free, plant-based, and functional foods is driven by health consciousness, resistant starch benefits (gut health), and clean-label trends globally.

The global green banana flour market is poised to witness a CAGR of 4.9%between 2026 and 2033.

Expanding applications in functional foods, nutraceuticals, sports nutrition, infant foods, and sustainable product innovations with broader distribution channels.

Natural Evolution Green, NuNaturals Ltd., Kanegrade, Woodland Foods, and Banamin Healthcare, are some of the key players in the green banana flour market.