- Processed Food

- Roasted Green Coffee Market

Roasted Green Coffee Market Size, Share, and Growth Forecast, 2025 - 2032

Roasted Green Coffee Market By Product Type (Arabica, Robusta, Other), Application (Commercial, Retail), Form, Distribution Channel, and Regional Analysis for 2025 - 2032

Roasted Green Coffee Market Size and Trends Analysis

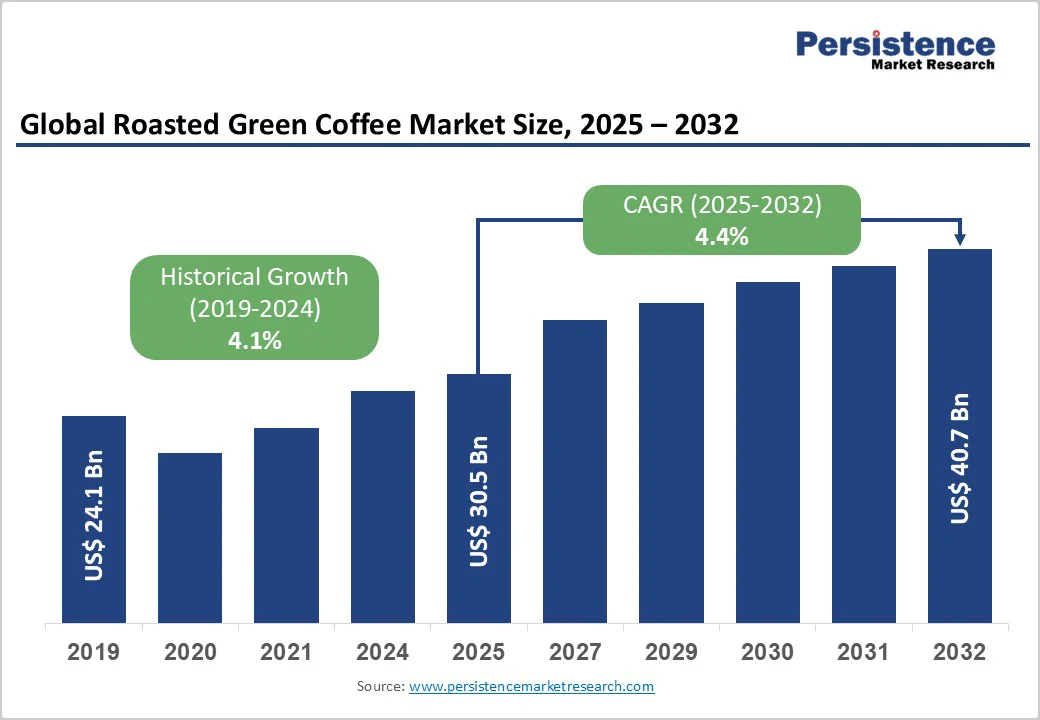

The global roasted green coffee market is expected to reach approximately US$30.5 billion in 2025. It is expected to reach about US$40.7 billion by 2032, growing at a CAGR of around 4.4% during the forecast period from 2025 to 2032, driven by premiumization and the adoption of specialty coffee in developed markets, rising consumer interest in health-positioned green-coffee ingredients and extracts, and expanding commercial use across food service and nutraceuticals.

Key Industry Highlights

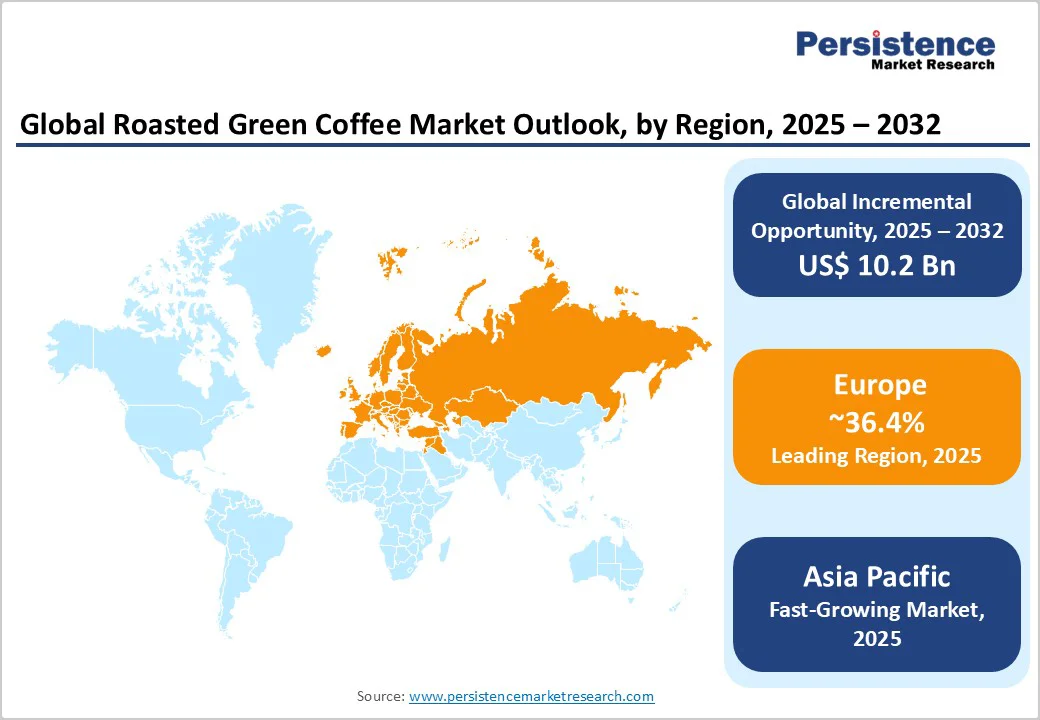

- Leading Region: Europe dominates the roasted green coffee market, accounting for 36.4% of global revenue in 2025, driven by strong café culture in countries such as Italy, Germany, and France, and high per-capita coffee consumption exceeding 5.5 kg annually.

- Fastest-growing Region: Asia Pacific, supported by expanding café chains in China, South Korea, and India, along with surging e-commerce coffee sales and rising middle-class consumption.

- Investment Plans: Global players such as Nestlé, Starbucks, and JDE Peet’s are investing in new roasting and packaging facilities across Southeast Asia and Eastern Europe, collectively exceeding US$450 million in planned expansions through 2028 to meet growing demand for premium and instant blends.

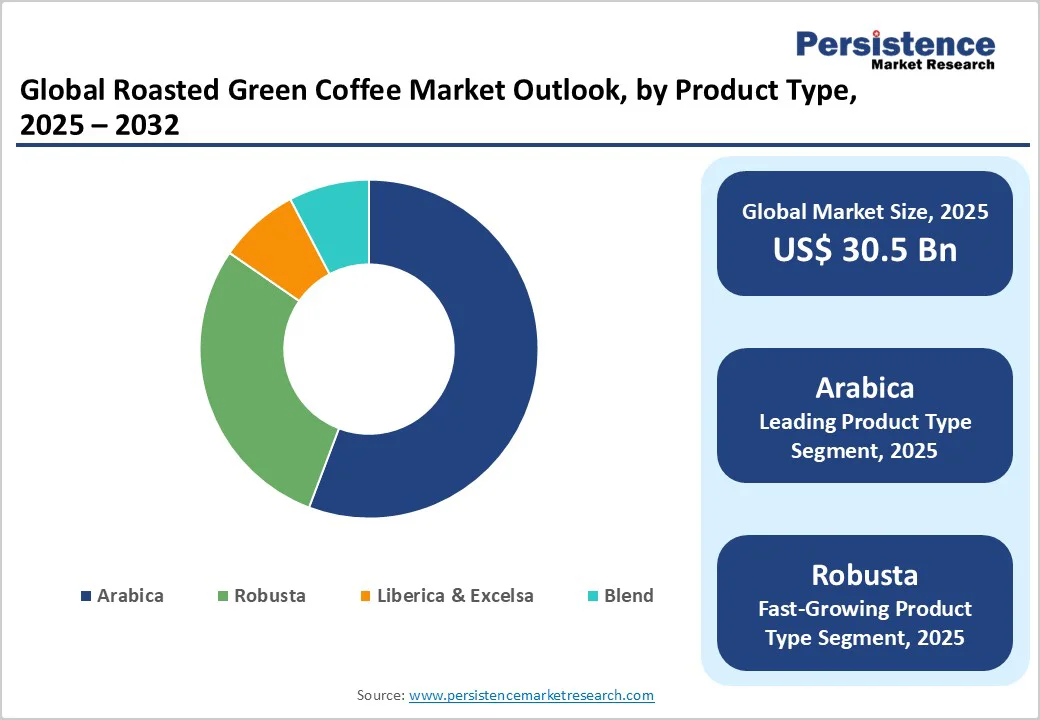

- Dominant Product Type: Arabica remains the leading product category, accounting for about 59% of total production and value, owing to its superior flavor profile, specialty appeal, and strong representation in premium roasts.

- Leading Application: The commercial segment captures approximately 62.5% of total roasted green coffee demand, driven by large-scale consumption in cafés, hotels, and industrial roasters, and by long-term procurement contracts.

| Key Insights | Details |

|---|---|

| Roasted Green Coffee Market Size (2025E) | US$30.5 Bn |

| Market Value Forecast (2032F) | US$40.7 Bn |

| Projected Growth (CAGR 2025 to 2032) | 4.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Specialty/Premiumization and At-Home Brewing Increase Value Capture

Consumers are trading up from commodity roast profiles to single-origin, micro-lot, and specialty roasted products. Roasters command higher retail and wholesale margins for traceable, sustainably sourced lots. This premiumization raises average realized prices and supports investment in roasting capacity and direct-trade sourcing.

The roasted-green segment benefits from both traditional roast-and-ground demand and a growing retail channel for specialty whole-bean sales. The mix shift increases market value faster than raw volume growth, driving higher average selling prices, improved margins for specialty roasters, and a greater willingness among retailers to pay for certified or single-origin lots.

Nutraceutical and Functional-Ingredient Demand

Green coffee (unroasted) and green coffee extracts rich in chlorogenic acids have found applications in dietary supplements, weight-management products, and functional beverages. This cross-category adoption converts a portion of the agricultural commodity into higher-value ingredient sales, broadening the addressable market beyond beverage consumption.

The green-coffee-extract sub-market is growing faster than commodity coffee, with nutraceutical demand sustaining price premiums and year-round buying. This diversification of end-use demand promotes longer-term contracts between extractors and ingredient buyers, increasing the overall dollar value per tonne of green coffee used in extract production.

Geographic Demand Growth in the Asia Pacific and Digital Retail Channels

Rising disposable incomes in China, India, and ASEAN markets, combined with increasing café penetration and e-commerce retail, are driving per-capita coffee consumption gains outside traditional markets. Digital distribution shortens time-to-market for specialty roasters and enables niche brands to scale up, accelerating value growth even as agricultural volumes grow modestly.

Investing in regional roasting and packaging near demand centers also reduces logistics costs and improves freshness, strengthening the competitive advantage of regional roasters. This results in faster revenue growth in APAC markets, new entrants via direct-to-consumer models, and increased participation of local roasters in global procurement chains.

Barrier Analysis - Green-Bean Price Volatility and Supply Risks

Coffee supply remains highly weather-sensitive. Frost, drought, and irregular rainfall in Brazil, Vietnam, and Colombia cause production shocks that drive price volatility and increase the cost of goods for roasters. Retail prices often lag these changes, squeezing margins.

Historical supply deficits have triggered price spikes and inventory shortages, forcing roasters to engage in forward buying or pay contract premiums, thereby increasing working capital needs. Export volumes and supply swings of several percent per year have historically translated into double-digit price movements during adverse events.

Regulatory and Standards Complexity for Nutraceutical Use

Green coffee extracts used in supplements face varying regulatory regimes and label-claim scrutiny across markets. Differing allowable claims and testing requirements add compliance costs and complicate market access for ingredient suppliers and finished-goods producers.

For firms pursuing cross-border nutraceutical sales, expenses related to clinical substantiation, stability testing, and local approvals can be significant and may delay product launches, narrowing commercialization windows for mid-sized suppliers.

Opportunity Analyses - Near-Roastery Investment and Cold-Chain Value Capture

Establishing regional roasting and packaging facilities near fast-growing demand centers in the Asia Pacific and Africa reduces logistics costs, enhances freshness, and enables higher value capture from whole-bean premiums.

If roasters achieve even 5-7% higher selling prices by roasting closer to end markets, regional roasted product revenues could expand substantially faster than green-bean import volumes. Suppliers and investors can explore brownfield expansions or toll-roasting partnerships, while large players with available capital can vertically integrate to lock in margins across the supply chain.

Ingredientization: Extracts and Functional Beverages

Converting green coffee into standardized extracts for supplements and ready-to-drink functional beverages offers a high-value growth avenue. The green coffee extract submarket is expanding at a faster CAGR than the raw green coffee market.

Capturing just 1-2% of the global botanical supplement ingredient market could yield significant incremental revenue for processors and specialty growers. Companies that certify active content (chlorogenic acids) and secure clinical validation will be favored partners for major consumer-packaged-goods brands.

Category-wise Analysis

Product Type Insights

Arabica dominates the roasted green coffee market with a 58.7% share, driven by its superior flavor, lower bitterness, and complex aroma that appeal to premium and specialty coffee consumers. Grown mainly in Brazil, Colombia, Ethiopia, and Central America, Arabica thrives in high-altitude, favorable climates.

Demand is strong in North America, Europe, and Japan, where single-origin and sustainably sourced coffees are prized. Major brands such as Starbucks and Blue Bottle Coffee highlight Arabica’s quality and certifications, including Rainforest Alliance and Fairtrade. Specialty lots have fetched over US$50 per kilogram at Cup of Excellence auctions, underscoring growing interest in artisanal, traceable coffee.

Robusta beans, meanwhile, are gaining momentum in the Asia Pacific and Africa, driven by instant coffee, RTD beverages, and espresso blends. Their resilience to pests and drought makes them a cost-efficient choice amid climate change. Vietnam, Uganda, and Indonesia lead global Robusta exports, with Vietnam accounting for nearly 40% of total exports.

Known for higher caffeine and crema, Robusta is increasingly used in home espresso and commercial blends by brands such as Nescafé and Lavazza. Innovations in roasting and fermentation are improving flavor quality, allowing “Fine Robusta” from India and Uganda to enter the specialty and premium coffee segments.

Application Insights

The commercial segment holds the largest market share at 62.5%, driven by cafés, restaurants, hotels, and large roasters that buy in bulk for consistency and cost efficiency. Global coffeehouse chains such as Starbucks, Costa Coffee, and Dunkin’, with over 80,000 outlets, sustain this demand through long-term sourcing contracts and stable supply chains.

Institutional consumption from offices and hospitality venues further supports steady growth. Major roasters such as JDE Peet’s and Tchibo depend on multi-season partnerships to maintain uniform quality, while expanding café chains in emerging markets, such as Café Coffee Day in India and Luckin Coffee in China, reinforce the segment’s dominance.

The retail segment is expanding rapidly, fueled by at-home brewing trends and e-commerce growth. Consumers are investing in grinders, espresso machines, and pour-over setups, boosting demand for premium roasted beans. The rise of remote work and digital retail has accelerated direct-to-consumer sales, with brands improving packaging and subscription offerings.

Platforms such as Amazon, Walmart.com, and Alibaba enable micro-roasters to reach global audiences. Artisanal brands such as Blue Tokai and Stumptown Coffee Roasters thrive through curated subscriptions highlighting origin and roast profiles. Premium single-origin coffees from Ethiopia, Kenya, and Peru are especially popular among younger consumers seeking quality and experiential home indulgence.

Regional Insights

North America Roasted Green Coffee Market Trends - Specialty Coffee Expansion and Functional Beverage Integration

North America, led by the U.S., is a major value market for roasted green coffee due to high per-capita consumption, mature specialty channels, and strong retail margins. The U.S. accounts for a large portion of premium roasted sales and global roasted-bean imports. Green-bean and roasted coffee sales in the U.S. are estimated in the single-digit tens of billions of dollars, reflecting strong domestic consumption and growing demand for green-coffee extracts.

The U.S. is the world’s largest importer of finished roasted products and a top consumer of specialty roasts. Demand is driven by single-origin coffees, premium blends, and functional beverages containing coffee extracts. The regulatory framework under the FDA offers structured pathways for compliance, especially for functional and dietary-ingredient products, though the process remains resource-intensive.

Growth is driven by the specialty coffee movement, demand for health-oriented beverages, and expanding subscription-based retail models. Urban café density and foodservice recovery post-pandemic further support the commercial segment. The competitive landscape includes major global brands alongside thousands of micro-roasters.

Private equity investment continues in roasting scale-ups, D2C technology, and traceability platforms. Notable trends include subscription service expansion, extract supply agreements, and origin partnerships for traceable sourcing.

Europe Roasted Green Coffee Market Trends - Sustainability-Driven Premiumization and Traceable Supply Chains

Europe is the largest regional market, accounting for approximately 33.6% of the global share in 2024. High per-capita consumption and extensive processing infrastructure make it a global hub for green-bean imports and roasted production. Germany serves as the continent’s central import and roasting hub, importing around 1.1 million tonnes of green coffee annually.

Italy and France lead in roasted-coffee consumption, while the U.K. is a strong retail and distribution market for premium packaged coffee and RTD beverages. Growth is fueled by deep specialty coffee culture, sustainability commitments, and mature foodservice channels.

European consumers emphasize certification and traceability, supporting premiumization but raising supplier costs. The EU’s regulatory and labeling standards, coupled with sustainability laws and due diligence requirements, are shaping sourcing and increasing certification costs.

The competitive landscape includes major trading houses (Neumann Kaffee Gruppe, Sucafina, Volcafe) and a large network of specialty roasters. Investment focuses on traceability technology, port-adjacent processing, and origin partnerships. Recent developments include increased certified imports, origin-country processing expansions under European contracts, and sustainability financing for replanting programs.

Asia Pacific Roasted Green Coffee Market Trends - Rapid Café Growth and Localized Roasting Investments

Asia Pacific is the fastest-growing region for roasted and green coffee, driven by urbanization and café proliferation. Though per-capita consumption is still below Europe or North America, regional growth rates are among the highest globally.

China shows rapid café chain expansion and growing demand for specialty beans. Japan remains a mature and high-consumption market, while India and Southeast Asia are experiencing significant growth due to middle-class expansion and evolving café culture. Vietnam and Indonesia are not only major producers but also growing domestic roasting centers.

Key growth drivers include the expanding middle class, increasing café density, and the rapid adoption of online retail for specialty coffee. Multinational and local roasters are investing in roasting and packaging closer to end markets, and joint ventures in RTD beverage manufacturing are rising.

While regulatory environments differ by country, evolving food-supplement regulations in China and India create both compliance challenges and high entry barriers for newcomers. Recent trends include new café chains, origin processing investments, and direct procurement partnerships between Asian roasters and farmer cooperatives.

Competitive Landscape

The global roasted green coffee market is moderately concentrated at the trading and processing level but fragmented among roasters and retailers. A handful of international traders and vertically integrated companies control large import volumes, while thousands of independent specialty roasters compete regionally. Europe’s processing hubs handle much of global trade flow, while brand competition remains diverse and localized.

Leading strategies include vertical integration across the value chain, premiumization through certified single-origin offerings, and diversification into digital and RTD channels. Key differentiators are traceability, quality assurance, and efficient logistics, with subscription-based roasters and ingredient-focused collaborations emerging as growth models.

Companies Covered in Roasted Green Coffee Market

- Starbucks Corporation

- Nestlé S.A.

- JDE Peet’s N.V.

- The Kraft Heinz Company

- Lavazza Group

- Tchibo GmbH

- Illycaffè S.p.A.

- Strauss Coffee B.V.

- UCC Ueshima Coffee Co., Ltd.

- Melitta Group

- Massimo Zanetti Beverage Group

- Luigi Lavazza S.p.A.

- Dunkin’ Brands Group

- Tata Coffee Limited

- Blue Bottle Coffee Inc.

- Peet’s Coffee

- Keurig Dr Pepper Inc.

- Luckin Coffee Inc.

- Café Coffee Day Enterprises Ltd.

- Paulig Group

Frequently Asked Questions

The roasted green coffee market size is estimated at US$30.5 Billion in 2025.

By 2032, the market is projected to reach US$40.7 Billion, reflecting steady consumption growth and premiumization trends.

Key trends include the rise of specialty and single-origin coffees, rapid expansion of e-commerce and direct-to-consumer channels, increasing adoption of sustainably sourced and certified beans, and growing consumption in Asia Pacific driven by café culture and premium instant coffee.

Arabica leads the market with nearly 59% share, supported by its superior flavor profile and dominant use in premium blends and specialty coffees.

The roasted green coffee market is anticipated to grow at a CAGR of 4.4% between 2025 and 2032.

Major companies include Starbucks Corporation, Nestlé S.A., JDE Peet’s N.V., Luigi Lavazza S.p.A., and Tchibo GmbH.