- Power Generation, Transmission, & Distribution

- Green Power Transformer Market

Green Power Transformer Market Size, Share, and Growth Forecast, 2025 - 2032

Green Power Transformer Market By Transformer Type (Three Phase, Single Phase), Voltage Rating (Low Voltage, Medium Voltage, High Voltage), Application (Renewable Energy Integration, Energy Transmission & Distribution, Others), and Regional Analysis for 2025 - 2032

Green Power Transformer Market Share and Trends Analysis

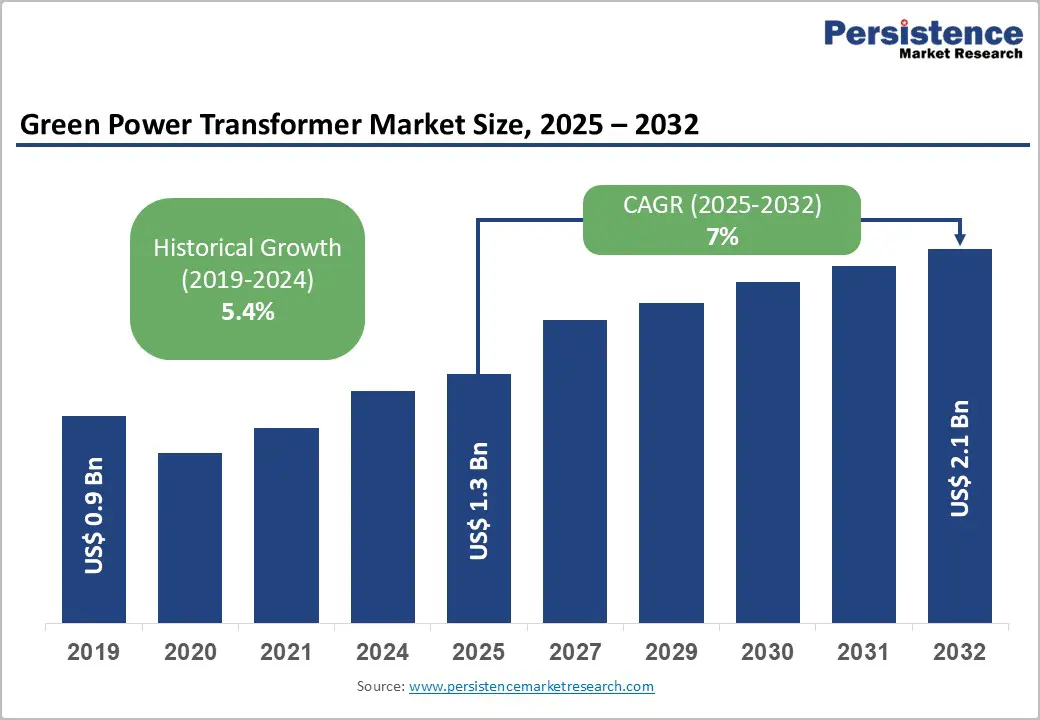

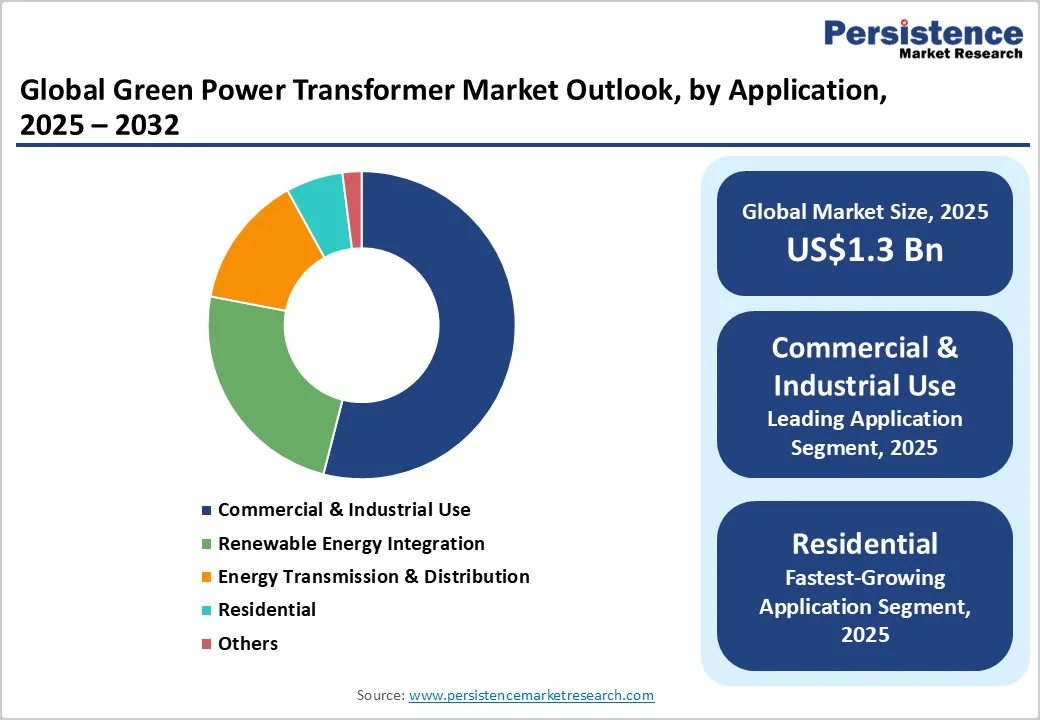

The global green power transformer market size is likely to be valued at US$1.3 Billion in 2025, and is estimated to reach US$2.1 Billion by 2032, growing at a CAGR of 7% during the forecast period 2025 - 2032, driven by the rising integration of renewable energy sources requiring efficient, low-loss transformers for sustainable grid applications.

The market is driven by renewable energy integration, grid modernization, regulatory mandates for efficiency and carbon reduction, infrastructure upgrades in emerging economies, and innovations in transformer materials and smart grid technologies, enhancing stability, reliability, and sustainability.

Key Industry Highlights

- Leading Transformer Type: Three-phase transformers hold nearly 65% market share in 2025, reflecting dominance in industrial and utility applications.

- Fastest-growing Transformer Type: The single phase segment is the fastest-growing from 2025 to 2032, fueled by widening renewable adoption in the residential sector.

- Dominant Voltage Rating Segments: Medium voltage transformers lead with over 50% market share in 2025, while high-voltage transformers exhibit the fastest growth through 2032.

- Application Leadership: Commercial and industrial applications represent close to 54% of the market in 2025, with residential applications growing the fastest between 2025 and 2032.

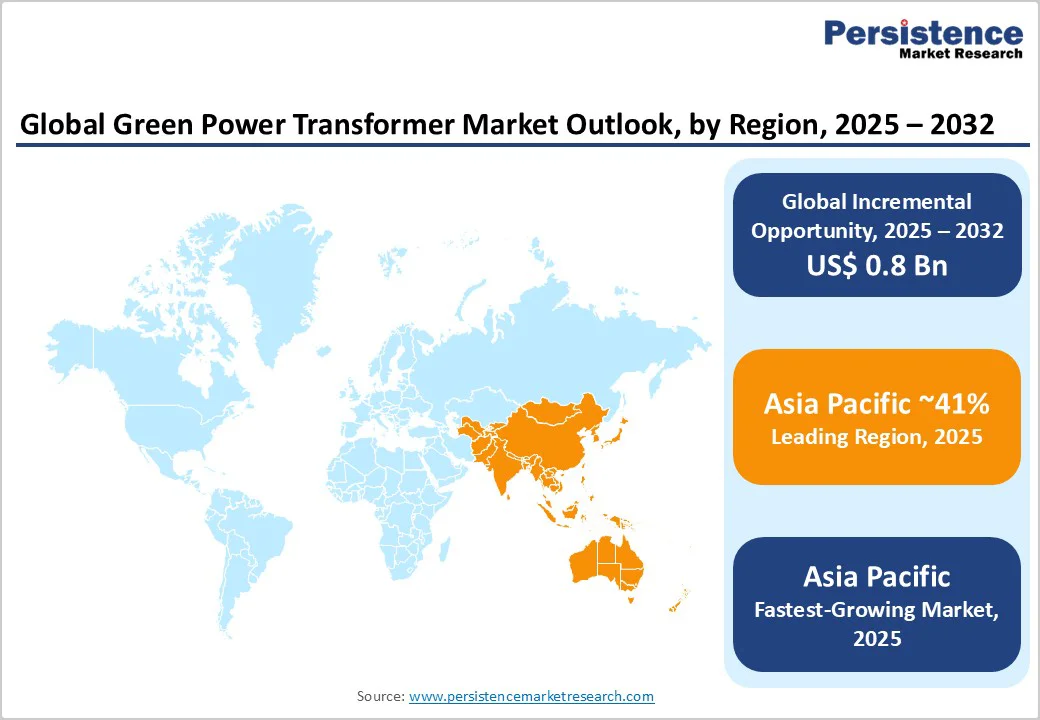

- Regional Dominance: Asia Pacific dominates at approximately 41% in 2025, and the regional market grows the fastest through 2032, propelled by massive energy consumption and renewable capacity expansion in China and India.

- Key Developments: Major industry developments include advanced amorphous transformer launches, strategic acquisitions in Asia, and partnership expansions in Latin America.

- May 2025: GE Vernova was selected by the Power Grid Corporation of India Limited (POWERGRID) to supply over 70 extra high-voltage (765 kV class) transformers and shunt reactors for critical power transmission projects supporting renewable energy corridors across India.

| Key Insights | Details |

|---|---|

| Green Power Transformer Market Size (2025E) | US$1.3 Bn |

| Market Value Forecast (2032F) | US$2.1 Bn |

| Projected Growth (CAGR 2025 to 2032) | 7% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Advancements in Amorphous Metal Core Transformers

The growing adoption of amorphous metal core transformers is a key driver shaping the green power transformer market. These cores drastically reduce no-load and operational losses compared to traditional silicon steel cores, boosting energy efficiency and lowering electricity costs. According to the International Energy Agency (IEA), transformers account for a significant portion of global electricity losses.

Employing amorphous cores can cut these losses considerably, yielding substantial energy savings and emissions reductions across utilities and industrial sectors. As energy efficiency regulations tighten, regulators such as the U.S. Department of Energy mandate loss reduction standards, propelling demand for these advanced transformer materials. This trend enhances market prospects by aligning it with global decarbonization commitments, offering utilities and industries cost-effective routes to compliance and sustainability.

High Initial Capital Costs and Supply Chain Complexity

Exorbitant upfront capital costs represent a crippling restraint for the green power transformer market growth, particularly in emerging economies. Amorphous core transformers, coupled with advanced cooling and insulation technologies, can cost 20-30% more than conventional units. Coupled with supply chain complexity for rare materials, exacerbated by geopolitical tensions and logistics disruption risks, this limits widespread deployment speed.

The extended procurement lead times affect project timelines and budget forecasting. Regulatory frameworks focusing on cost control and grid reliability prioritize immediate capital expenditure savings, disadvantaging higher-cost green transformers in some regions. Risk mitigation strategies that market players need to consider include fostering closer supplier relationships and investing in localized manufacturing, but barriers remain significant in cost-sensitive and infrastructure-deficient regions.

Renewable Infrastructure Buildout in Developing Economies

Developing markets, especially in Asia Pacific and Latin America, present a lucrative growth opportunity tied to large-scale renewable energy infrastructure projects. Countries such as India and Brazil are aggressively expanding their solar and wind capacities to meet escalating electricity demands and fulfil climate commitments. For instance, India’s Ministry of New and Renewable Energy estimates that by the end of 2025, the country will have added 43 GW of renewable energy generation capacity.

Favorable government policies, including subsidies, tax incentives, and green finance initiatives, are catalyzing investments in energy-efficient grid components such as green power transformers. The opportunity is further accentuated by increasing electrification in rural areas, necessitating robust, sustainable power distribution. Investors and manufacturers focusing on scalable, affordable green transformer models tailored for these markets can capitalize on these trends, achieving both growth and sustainability impacts.

Category-wise Analysis

Transformer Type Insights

In 2025, the three phase segment is expected to command an estimated 64.8% of the green power transformer market revenue share. This segment’s dominance is driven by its critical role in industrial-scale and utility-scale renewable power integration, where balanced load distribution and high power capacity are necessary.

Its suitability for managing large electricity flows makes it the preferred choice in commercial and grid applications aimed at enhancing green energy transmission efficiency. Leading manufacturers have focused investments on improving core materials and cooling systems for three phase units, further solidifying their market position.

The single-phase segment is slated to be the fastest growing, projected to register a high CAGR from 2025 to 2032. This growth is propelled by the increasing deployment of residential solar systems and microgrid applications that require compact, efficient transformers.

The rise of distributed energy resources and prosumer markets, especially in emerging economies, is stimulating demand. Enhanced smart grid technologies facilitating two-way power flows are also increasing reliance on single phase transformers designed for localized load management, making this segment a key target for future innovation and market expansion.

Voltage Rating Insights

Medium voltage (1 kV to 36 kV) transformers hold the largest revenue share in 2025, accounting for over 50% of the market. Their central role in connecting high-voltage transmission lines to lower-voltage distribution networks underscores their importance in grid modernization efforts worldwide.

These transformers are crucial for effectively managing power flow between renewable energy sources and end-users while maintaining grid stability. As utility-scale renewables expand, medium voltage transformers are indispensable for balancing generation and consumption.

The high voltage (36 kV to 765 kV) segment is anticipated to register the highest CAGR. The demand arises from the scaling up of grid infrastructure and increasing requirements for high-capacity transformers capable of minimizing losses in large industrial and commercial installations.

Technologies improving thermal management and insulation are enhancing the efficiency and lifespan of high-capacity transformers, making them increasingly attractive for green energy projects and future-proofing power grids.

Application Insights

The commercial & industrial use segment is poised to dominate the market in 2025, with a revenue share of nearly 54%. The leadership of this application area is associated with heightened pressures on industrial sectors worldwide to improve energy efficiency and reduce carbon emissions.

Large enterprises and commercial complexes are investing in green transformers to meet regulatory requirements and sustainability goals while benefiting from long-term operational savings derived from reduced energy losses. The segment also benefits from extensive regulatory frameworks encouraging energy-efficient practices in commercial power usage globally.

The residential segment is predicted to exhibit the highest CAGR from 2025 to 2032. Growth drivers include widespread adoption of rooftop solar installations driven by government incentives, net metering policies, and rising consumer awareness of sustainability.

Distributed generation and energy storage systems integrated into homes are increasing the demand for efficient single phase transformers capable of supporting two-way power flows in smart grids. This segment is especially pronounced in emerging economies undergoing electrification and green infrastructure expansion.

Regional Insights

North America Green Power Transformer Market Trends

North America is projected to grow moderately, with the U.S. serving as the primary growth engine. Federal initiatives such as the Infrastructure Investment and Jobs Act, which allocates substantial funding for grid modernization and renewable energy integration, are the foremost growth determinants for this regional market. Stringent energy efficiency standards enforced by the Department of Energy have incentivized utilities and manufacturers to adopt advanced, low-loss transformers aligned with sustainability goals.

The regulatory environment in North America fosters innovation, which emphasizes smart grid technologies and predictive maintenance capabilities embedded in next-generation transformers. The North America market is characterized by a competitive ecosystem with prominent R&D investment from leading global manufacturers focusing on digital integration and energy management solutions. Investment trends indicate increased public-private partnerships and venture capital interest in green grid infrastructure, signaling a progressively robust market environment.

Europe Green Power Transformer Market Trends

Europe is forecast to grow, led by Germany, the U.K., France, and Spain, fueled by the European Green Deal and Renewable Energy Directive, which mandate high energy efficiency standards and substantial increases in renewable capacity. Regulatory harmonization across member states facilitates market entry and accelerates the adoption of compliant transformer technologies.

The competitive landscape in Europe features a strong presence of domestic manufacturers leveraging advanced materials and innovative cooling technologies to meet the strict eco-design requirements of the European Union (EU). Investment flows in Europe focus on upgrading aging grid infrastructure, decentralized generation integration, and smart grid deployments. These initiatives are supported by regional funding mechanisms and green bonds, creating a fertile environment for sustainable transformer market growth.

Asia Pacific Green Power Transformer Market Trends

Asia Pacific stands as the largest and fastest-growing regional market for green power transformers, capturing around 41% market share in 2025. China leads the market with massive investments in solar, wind, and hydroelectric power projects, reinforced by government policies such as the 14th Five-Year Plan, emphasizing green energy transition. India follows closely with strong renewable capacity targets and grid modernization programs.

The regional market stands to gain tremendously from unparalleled manufacturing advantages, including lower production costs and extensive industrial ecosystems, supporting export-oriented growth. Japan and South Korea are spearheading cutting-edge power technology innovations, especially in digital transformer management and smart grid applications. Competitive dynamics in Asia Pacific are shaped by joint ventures, government incentives, and rapid urbanization, which cumulatively create significant investment opportunities in green transformer technologies.

Competitive Landscape

The global green power transformer market structure is moderately consolidated, dominated by a handful of multinational corporations. Hitachi Energy, ABB, Siemens Energy, Schneider Electric, GE Grid Solutions, Eaton, and CG Power collectively control around 60% of the market revenue, demonstrating a balance between concentration and competitive diversity.

Market leaders leverage strong patents, R&D capabilities, and extensive distribution networks to maintain competitive advantages in efficiency and product innovation.

Competitive positioning of market participants is shaped by differentiated product portfolios, including amorphous core transformers, eco-friendly insulating oils, and intelligent monitoring systems. Regional manufacturers and emerging players focus on tailored solutions for local markets, emphasizing cost-effectiveness and compliance with national regulations.

Long-term collaborations, acquisitions, and investments in smart grid technology integration are the main strategies being implemented by companies in an attempt to cement their market position amidst evolving customer demands.

Key Industry Developments

- In September 2025, Waaree Energies acquired a 64% stake in Kotsons Pvt. Ltd. for INR 192 crore (US$23.13 Million) and full ownership of Impactgrid Renewables Pvt. Ltd., enhancing its transformer and renewable energy portfolio, strengthening vertical integration, expanding market reach, and enabling end-to-end clean energy solutions for sustainable growth and global energy transition leadership.

- In September 2025, Siemens Energy invested €220 Million (US$254.4 Million) to expand its Nuremberg transformer factory, boosting capacity by 50% and creating 350 jobs. Supported by €20 Million (US$23.1 Million) in Bavarian funding, the expansion addresses rising global demand for large transformers, strengthens Nuremberg as an energy innovation hub, and ensures supply by 2028.

- In May 2025, Hitachi Energy supplied rectifier transformers to China’s Songyuan green hydrogen project, enabling stable power for water electrolysis. Backed by a 3 GW renewable facility, the project targets 800,000 tons of green ammonia and methanol annually, advancing industrial decarbonization under Jilin Province’s “Hydrogen Powering Jilin” initiative.

Companies Covered in Green Power Transformer Market

- Hitachi Energy

- ABB

- Siemens Energy

- Schneider Electric

- GE Grid Solutions

- Eaton

- CG Power and Industrial Solutions

- Hyosung Heavy Industries

- Ormazabal

- Alstom Grid

- Westrafo

- Toshiba Energy Systems & Solutions Corporation

- Mitsubishi Electric Corporation

- Fuji Electric Co., Ltd.

- Sumitomo Corporation

Frequently Asked Questions

The global green power transformer market is projected to reach US$1.3 Billion in 2025.

The growing integration of renewable energy sources into existing grid operations and the modernization of electrical grids driven by regulatory mandates aiming at energy efficiency, operational cost reduction, and carbon footprint mitigation are driving the market.

The green power transformer market is poised to witness a CAGR of 7% from 2025 to 2032.

Energy infrastructure upgrades across emerging economies, and innovations in transformer materials and smart grid functionalities, which collectively enhance grid stability and reliability while aligning with global sustainability goals, are key market opportunities.

Hitachi Energy, ABB, Siemens Energy, and Schneider Electric are some of the key players in the market.