- Transportation & Logistics

- Green Logistics Market

Green Logistics Market Size, Share, and Growth Forecast, 2026 - 2033

Green Logistics Market by Service (Transportation & Fleet Management, Warehousing & Fulfilment, Packaging & Materials, Reverse & Circular Logistics, Infrastructure & Energy, Others), Technology (Electrification, Alternative Fuels, Operational Optimization, Renewable Energy Integration, Carbon Management, Others), Mode of Transport (Road, Rail, Sea, Air, Multimodal/Intermodal, Urban Micro-Logistics), and Regional Analysis for 2026 - 2033

Green Logistics Market Share and Trends Analysis

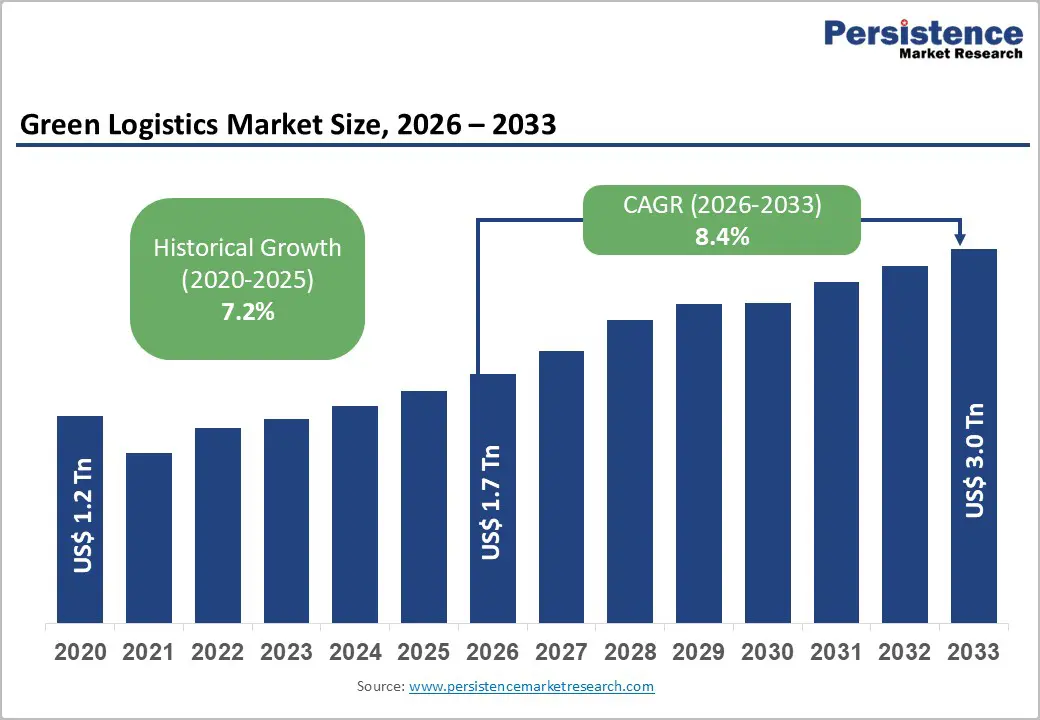

The global green logistics market size is likely to be valued at US$ 1.7 trillion in 2026, and is projected to reach US$ 3.0 trillion by 2033, growing at a CAGR of 8.4% during the forecast period 2026 - 2033.

Binding climate regulations, Scope-3 disclosure mandates, and accelerating electrification economics are driving the market. Regulatory enforcement is intensifying across major trade corridors, with mandatory emissions reporting and carbon pricing increasingly extending to freight transport and logistics procurement. Large shippers are actively internalizing logistics decarbonization as a Scope-3 risk-management priority, creating long-term demand for certified green logistics contracts rather than ad-hoc offsets. Technology cost curves are bending in favor of electric last-mile fleets, energy-positive warehouses, and software-driven route and load optimization. Value creation is shifting away from commoditized transport services toward integrated service platforms that combine low-emission assets, digital optimization, and verifiable emissions reporting. Market competition is therefore intensifying between incumbent global logistics providers and asset-light technology-enabled operators, while infrastructure investors are increasingly targeting charging networks, green warehouses, and intermodal hubs as stable long-duration assets.

Key Industry Highlights

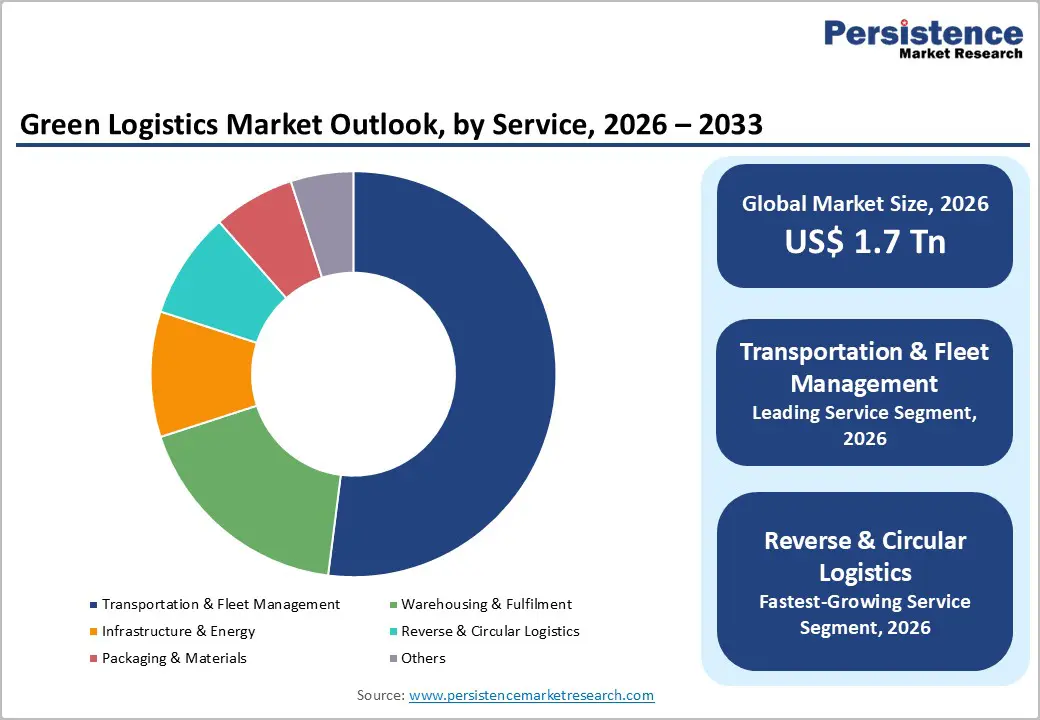

- Dominant Service: Transportation and fleet services are expected to account for approximately 52% of market revenue in 2026, reflecting their central role in freight decarbonization.

- Fastest-growing Service: Reverse and circular logistics services are projected to expand at the highest CAGR of around 10.1% during 2026 - 2033, driven by rising e-commerce return volumes.

- Technology Leadership: Electrification is anticipated to hold nearly 44% of revenue share in 2026, supported by declining battery costs and favorable total cost of ownership for last-mile fleets.

- Fastest-growing Technology: Carbon management is expected to record the fastest growth between 2026 and 2033, owing to mandatory reporting requirements.

- Fastest-growing Mode of Transport: Rail and intermodal logistics are expected to be the fastest-growing through 2033, supported by government-backed modal-shift policies.

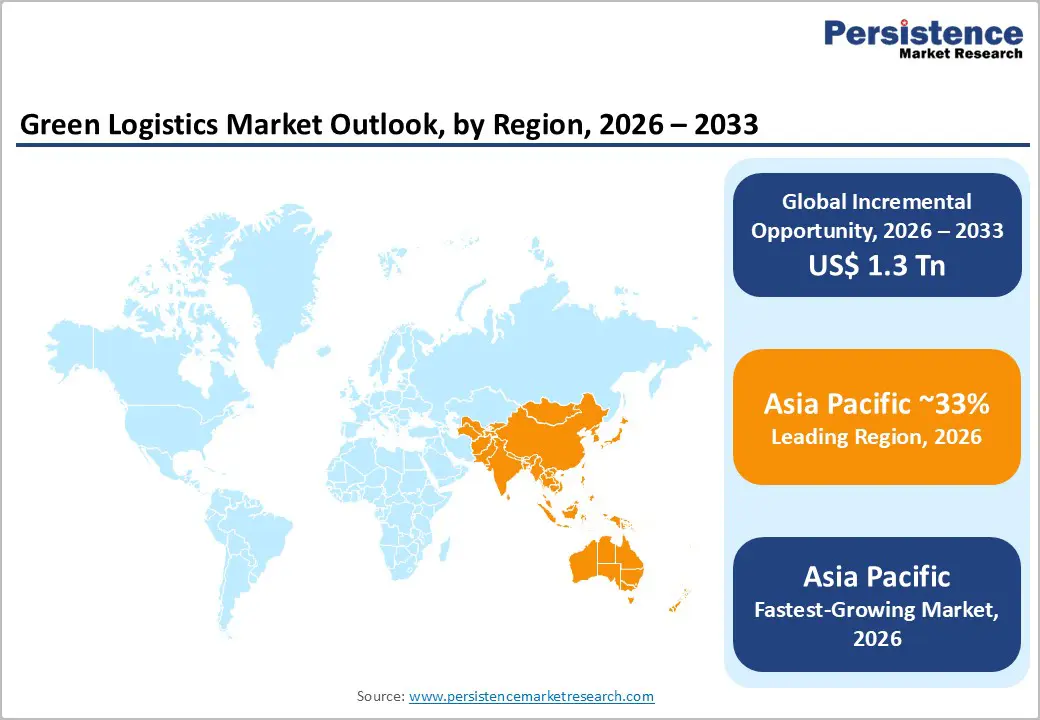

- Regional Dominance: Asia Pacific is projected to hold approximately 33% market share in 2026, driven by the rapid expansion of logistics capacity and large-scale urbanization.

- Fastest-growing Market: Asia Pacific is also expected to be the fastest-growing market through 2033, powered by sustained investments in urban last-mile electrification and expansion of intermodal freight corridors.

- June 2025: AM Green and the Port of Rotterdam Authority signed a MoU to develop a green hydrogen/low-carbon fuel supply chain from India to Northwestern Europe, enabling up to 1 million tons of annual exports of green ammonia/methanol.

| Key Insights | Details |

|---|---|

| Green Logistics Market Size (2026E) | US$ 1.7 Tn |

| Market Value Forecast (2033F) | US$ 3.0 Tn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Scope-3 Regulatory Convergence in Global Supply Chains

The most structurally important driver for green logistics is the rapid convergence of mandatory Scope 3 (indirect supply chain) emissions disclosure, carbon pricing mechanisms, and public procurement standards. These forces are increasingly compelling shippers to decarbonize their logistics operations rather than treating sustainability as an optional enhancement. Regulatory bodies in Europe and North America are tightening reporting and accountability requirements, while multinational buyers are cascading these obligations down their logistics supply chains. For example, the European Union (EU)'s Corporate Sustainability Reporting Directive (CSRD) is expanding mandatory Scope 3 emissions disclosure to more than 50,000 companies by 2026, directly increasing demand for verifiable low-carbon transport and warehousing services. Similar pressures are emerging through public procurement rules in the United States and carbon reporting frameworks aligned with the Greenhouse Gas (GHG) Protocol, which explicitly categorizes third-party logistics as a material Scope 3 category.

This shift is favoring logistics providers that can combine low-emission assets with auditable data systems, meaning that green logistics spending is not only growing in volume but also becoming longer-term and less price-sensitive. As a result, compliant providers are experiencing improved revenue visibility and stronger contract economics. Regulatory convergence is accelerating consolidation around certified green service offerings, raising entry barriers for smaller carriers that lack the necessary capital or data infrastructure. The transformation is also expanding the addressable market for digital carbon-accounting platforms and third-party verification services, reinforcing green logistics as a multi-layered value chain rather than a single transport segment. This evolution also signals that investment in emissions measurement, asset modernization, and certification infrastructure is becoming a competitive requirement rather than a discretionary initiative.

Capital Intensity and Infrastructure Mismatch in Freight Decarbonization

Despite strong demand signals, the green logistics market's growth continues to be constrained by persistent restraints, including high upfront capital requirements and uneven infrastructure readiness, particularly in the medium- and heavy-duty freight segments. Electrification and alternative-fuel adoption remain economically viable only in clearly defined use cases, resulting in uneven adoption across regions and transport modes. Electric trucks and hydrogen-based freight solutions continue to carry a significant cost premium compared with internal combustion engine vehicles, even after accounting for fuel and maintenance savings. Industry data from transport authorities and original equipment manufacturer (OEM) disclosures indicate that battery-electric heavy-duty trucks are still costing approximately 1.5 to 2 times as much as comparable diesel vehicles in 2025, while hydrogen fuel-cell trucks remain constrained by limited refueling infrastructure and elevated hydrogen production costs. This capital intensity is disproportionately affecting small and mid-sized logistics operators, which are continuing to represent a substantial share of global freight capacity.

Infrastructure readiness is further compounding this challenge and is slowing the pace of fleet decarbonization. Public fast-charging networks suitable for freight operations remain unevenly distributed, while grid constraints are delaying depot-level electrification projects in dense logistics hubs. According to international energy agencies, grid connection timelines for large logistics facilities in several regions are extending beyond 24 to 36 months, thereby delaying fleet electrification programs and increasing project risk. As a result, investors and logistics providers are increasingly facing execution risk when capital deployment is outpacing infrastructure availability. This environment is favoring phased adoption strategies, leasing and vehicle-as-a-service (VaaS) models, and asset-light partnerships, while simultaneously moderating near-term growth expectations for heavy freight decarbonization.

Integrated Green Logistics Platforms in Emerging Asia Pacific Corridors

The most commercially attractive opportunity in the market for green logistics is emerging across Asia Pacific trade and urban logistics corridors, where rapid logistics expansion is intersecting with tightening policy mandates and accelerated technology adoption. Unlike mature Western markets, several Asia Pacific economies are simultaneously expanding logistics capacity while embedding sustainability requirements into new infrastructure and service contracts, creating a favorable environment for integrated green logistics platforms rather than incremental retrofits. Governments in China, India, Southeast Asia, and Australia are increasingly aligning urban air quality objectives, national climate commitments, and industrial development strategies with logistics modernization programs. Policy measures such as national electric mobility initiatives, urban low-emission zones, and large-scale renewable energy deployment are actively supporting the rollout of electric last-mile fleets, energy-efficient warehousing facilities, and intermodal freight hubs.

Integrated service providers are increasingly combining low-emission transport assets, digital optimization tools, and verified emissions reporting capabilities to secure long-term contracts with multinational shippers that are prioritizing supply chain resilience and regulatory compliance. This opportunity is economically attractive because it allows providers to design green logistics systems at scale rather than retrofitting legacy assets, thereby improving cost efficiency and operational integration. For investors, the region offers exposure to higher-growth trajectories, infrastructure-linked revenue stability, and policy-supported demand, while also requiring careful management of execution risk and regulatory coordination across diverse markets.

Category-wise Analysis

Service Insights

Transportation and fleet services are set to dominate, accounting for approximately 52% of the green logistics market revenue share in 2026. This leadership is primarily driven by the high emissions intensity of freight transport and the increasing focus of regulators and corporate buyers on vehicle electrification and fuel switching. Large shippers are increasingly contracting low-emission linehaul and last-mile services through multi-year agreements, improving revenue visibility and contract stability for leading logistics providers. Road freight remains the largest contributor within this segment, as electric and alternative-fuel urban delivery fleets are offering faster payback periods, operational flexibility, and scalable deployment across dense consumption centers.

Reverse and circular logistics are likely to be the fastest-growing service segment, with an estimated CAGR of around 10.1% between 2026 and 2033. Growth is being driven by rising e-commerce return volumes, extended producer responsibility frameworks, and stronger corporate commitments to circular economy models. Activities such as battery recycling, reusable packaging circulation, and product refurbishment logistics are increasingly becoming embedded within long-term green logistics contracts. This segment is attracting strategic interest because it delivers higher margins, lower fuel intensity, and stronger regulatory alignment than traditional freight services. As a result, reverse and circular logistics are becoming a priority expansion area for both incumbent logistics providers and specialized service operators seeking differentiated growth.

Technology Insights

Electrification and energy-efficient assets are poised to be the leading segment, expected to account for approximately 44%of total technology-related revenue generation in 2026. Electrification technologies such as battery-electric vehicles and energy-efficient warehousing infrastructure are benefiting from declining battery costs, longer vehicle driving ranges, and increasingly favorable total cost of ownership dynamics. Adoption is accelerating most visibly in last-mile and regional distribution operations, where duty cycles are predictable and charging integration is more feasible. In parallel, warehouse electrification initiatives and renewable energy integration are supporting immediate Scope 2 emissions reductions, which are strengthening the business case for logistics operators that are prioritizing rapid and measurable decarbonization outcomes.

Carbon management and logistics optimization software are slated to emerge as the fastest-growing technology segment during the 2026 - 2033 forecast period. This expansion is owing to mandatory emissions reporting requirements and increasing buyer demand for auditable and standardized emissions data across logistics operations. These digital platforms are enabling capabilities such as route optimization, load consolidation, and supplier performance benchmarking, which are directly improving cost efficiency and regulatory compliance. Their asset-light operating models, high scalability, and recurring revenue structures are making them particularly attractive to investors, while logistics providers are increasingly viewing these tools as essential infrastructure rather than optional add-ons.

Mode of Transport Insights

Road transport is set to remain the dominant mode, accounting for around 68% of the green logistics market share in 2026. This dominance reflects the structural importance of road networks in supporting both long-haul freight movements and last-mile delivery operations across global supply chains. Electrification and renewable diesel adoption are progressively improving emissions performance while allowing logistics operators to continue using existing distribution networks and operational models. The relative ease of integrating low-emission road vehicles compared with other modes is reinforcing road transport’s leading position in near- and medium-term green logistics strategies.

Rail and intermodal logistics are poised to be the transport modes with the highest CAGR for 2026 - 2033. The growth of this segment is being stimulated by sustained government investment in rail infrastructure, the inherently lower emissions intensity of rail freight, and increasing interest from shippers in modal shift strategies for long-distance cargo movement. Intermodal solutions enable logistics providers to combine the efficiency of rail with the flexibility of road transport, strengthening their value proposition for carbon-sensitive supply chains. As regulatory pressure on long-haul emissions continues to increase, rail and intermodal logistics are becoming a strategic priority for freight decarbonization initiatives.

Regional Insights

North America Green Logistics Market Trends

North America is expected to account for approximately 27% of the total market value in 2026. Market expansion here is being supported by the accelerating adoption of electrified last-mile delivery fleets, increasing deployment of warehouse automation, and the growing integration of sustainability criteria into corporate procurement strategies. Regulatory incentives at the federal and state levels are supporting early adoption, while public and private investment in charging infrastructure is improving the feasibility of electric delivery operations in urban and suburban corridors. Strong e-commerce demand is further reinforcing the need for low-emission distribution networks that can operate at scale without compromising service levels.

Regional market growth is expected to moderate, driven by slower decarbonization in the medium- and heavy-duty freight segments, where vehicle costs and infrastructure readiness continue to pose constraints. Nevertheless, sustained investment in depot charging, renewable energy integration at logistics facilities, and digital emissions management systems is strengthening long-term market fundamentals. For logistics providers and investors, North America is offering a relatively stable growth environment with lower regulatory uncertainty, predictable demand from large enterprise customers, and increasing opportunities to scale proven green logistics solutions across established supply-chain networks.

Europe Green Logistics Market Trends

Europe is likely to be the second-largest regional market for green logistics, commanding about 30% of global market value in 2026. The adoption of sustainable logistics in the region is primarily driven by regulatory enforcement, including carbon pricing mechanisms, mandatory emissions reporting, and extensive public funding for rail and intermodal infrastructure. These measures are increasing the cost of non-compliant logistics operations while simultaneously improving the commercial viability of low-emission transport and energy-efficient warehousing solutions. As a result, shippers across industrial, retail, and e-commerce sectors are increasingly prioritizing certified green logistics providers to meet regulatory and disclosure requirements.

The European market is expected to expand at a notable rate throughout the 2026 - 2033 forecast period. The regional competitive landscape is becoming increasingly concentrated as leading logistics providers leverage scale, capital access, and compliance capabilities to consolidate market share. Smaller operators are facing increasingly stringent certification, reporting, and infrastructure requirements. For investors and service providers, Europe offers relatively predictable growth, supported by policy certainty, long-term public investment, and structurally embedded demand for low-emission logistics solutions across key trade corridors.

Asia Pacific Green Logistics Market Trends

Asia Pacific is slated to stand as the largest regional market for the green logistics market, projected to capture an estimated 33% market share in 2026. The unprecedented scale of urbanization, sustained development of logistics infrastructure, and strong policy support for electrification and energy-efficient supply-chain systems are the primary growth drivers for the market here. Governments across major economies, particularly India and China, are actively integrating green logistics into national mobility, air-quality, and industrial development frameworks, accelerating adoption across urban and regional freight networks. China and India are acting as primary volume drivers due to their scale, growing e-commerce penetration, and expanding manufacturing bases.

The Asia Pacific green logistics market is also expected to grow at the fastest pace at an approximate CAGR of 9.6% between 2026 and 2033. Southeast Asia is increasingly emerging as a key investment destination as multinational companies are diversifying supply chains and local governments are expanding incentives for electric mobility, green warehousing, and intermodal logistics hubs. The region offers strong long-term growth potential through a combination of policy-backed demand, large addressable markets, and opportunities to deploy integrated green logistics platforms at scale, though execution complexity and regulatory coordination remain important considerations for market participants.

Competitive Landscape

The global green logistics market structure is moderately fragmented, with the top ten service providers collectively controlling 38-42% of total market revenues. Large global logistics companies are continuing to leverage scale advantages, strong balance sheets, and integrated service portfolios to expand their green logistics offerings across multiple regions and customer segments. These players are increasingly investing in low-emission fleets, energy-efficient warehousing, and digital emissions management capabilities to meet regulatory and customer requirements. Regional and specialized operators are competing through focused technology partnerships, corridor-specific solutions, and niche service offerings that address local regulatory and operational needs.

Leading companies such as DHL Group, A.P. Moller - Maersk, Kuehne + Nagel, and DB Schenker are enhancing their ability to deliver end-to-end decarbonization solutions that combine low-emission transport assets, optimized network design, and auditable emissions reporting. Providers that are integrating physical logistics services with digital carbon management tools are strengthening client retention and contract duration. As a result, competition is moving away from price-based differentiation toward capability depth, compliance readiness, and the ability to support long-term sustainability objectives for global shippers.

Key Industry Developments

- In January 2026, AVG Logistics partnered with Nestlé India and Ashok Leyland to launch a dedicated green logistics corridor using 50 CNG trucks for Nestlé's supply chain, covering 2.75 lakh km monthly. The initiative will reduce CO2 emissions by 1.1 lakh kg annually, improving fuel efficiency and aligning with emission targets.

- In December 2025, Yusen Logistics and AllChiefs teamed up to develop "Alternative Fuel," a carbon in-setting offering focused on biofuels and electric trucks to reduce supply chain emissions. Through co-design sessions, customer insights, and internal training, the solution aligns with Yusen's 2030 goal to lead sustainable logistics from Asia.

- In October 2025, Acer renewed its partnership with Kuehne+Nagel for biofuel-based sea freight decarbonization and joined forces with DSV on Dutch routes, deploying electric trucks with a 400km range powered by renewables. These initiatives support Acer's SBTi-aligned Scope 3 emissions cut of 35% by 2030, emphasizing data tracking, reinvestment mechanisms, and supply chain collaboration.

Companies Covered in Green Logistics Market

- DHL Group

- A.P. Moller - Maersk

- Kuehne + Nagel International AG

- DB Schenker

- DSV A/S

- FedEx Corporation

- United Parcel Service, Inc.

- C.H. Robinson Worldwide, Inc.

- Nippon Express Holdings, Inc.

- XPO Logistics, Inc.

- Sinotrans Limited

- Ryder System, Inc.

- CEVA Logistics

- Expeditors International of Washington, Inc.

Frequently Asked Questions

The global green logistics market is projected to reach US$ 1.7 trillion in 2026.

Binding climate regulations, Scope-3 disclosure mandates, and escalating electrification drives are fueling the market.

The market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Extension of mandatory emissions reporting and carbon pricing to freight transport and logistics procurement and development of integrated service platforms that combine low-emission assets, digital optimization are key market opportunities.

DHL Group, A.P. Moller - Maersk, Kuehne + Nagel International AG, and DB Schenker are some of the key players in the market.