- Industrial Goods & Service

- Glass Seal Market

Glass Seal Market Size, Share, and Growth Forecast 2026 – 2033

Glass Seal Market by Product Type (Low Temperature Sealing Glass and High Temperature Sealing Glass), Technology (Sealing (Standard), Hermetic Sealing, and Non-Hermetic Sealing), Material (Borosilicate Glass, Aluminosilicate Glass, Lead-Free Glass, and Other Specialty Glasses), Application (Electrical & Electronics, Automotive, and Others), and Regional Analysis

Glass Seal Market Size and Share Analysis

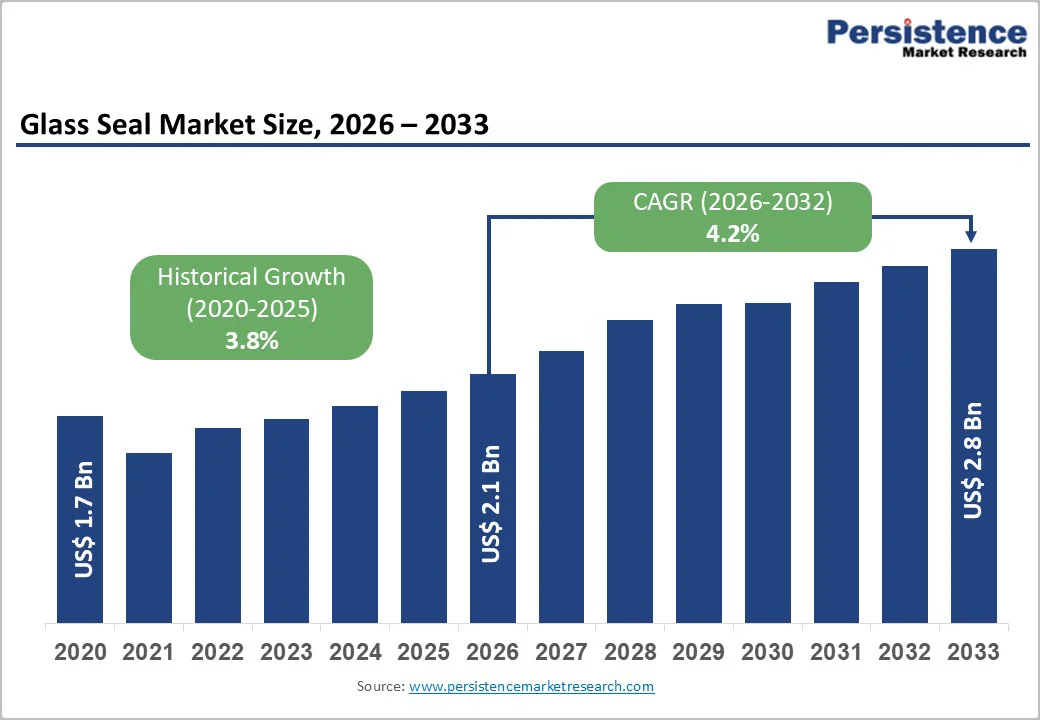

The global Glass Seal Market size was valued at US$ 2.1 Bn in 2026 and is projected to reach US$ 2.8 Bn by 2033, growing at a CAGR of 4.2% between 2026 and 2033. Market expansion is driven by exponential demand for advanced sealing solutions across aerospace and defense sectors experiencing 8% CAGR growth supported by global defense spending exceeding US$ 740 billion in 2024 and aerospace market projected to reach US$ 1 trillion by 2034. Automotive industry electrification generating substantial demand for hermetically sealed sensors and power modules in electric vehicles, with leading manufacturers integrating 18+ hermetic sensors per vehicle, establishes critical growth driver supporting market expansion.

Key Market Highlights

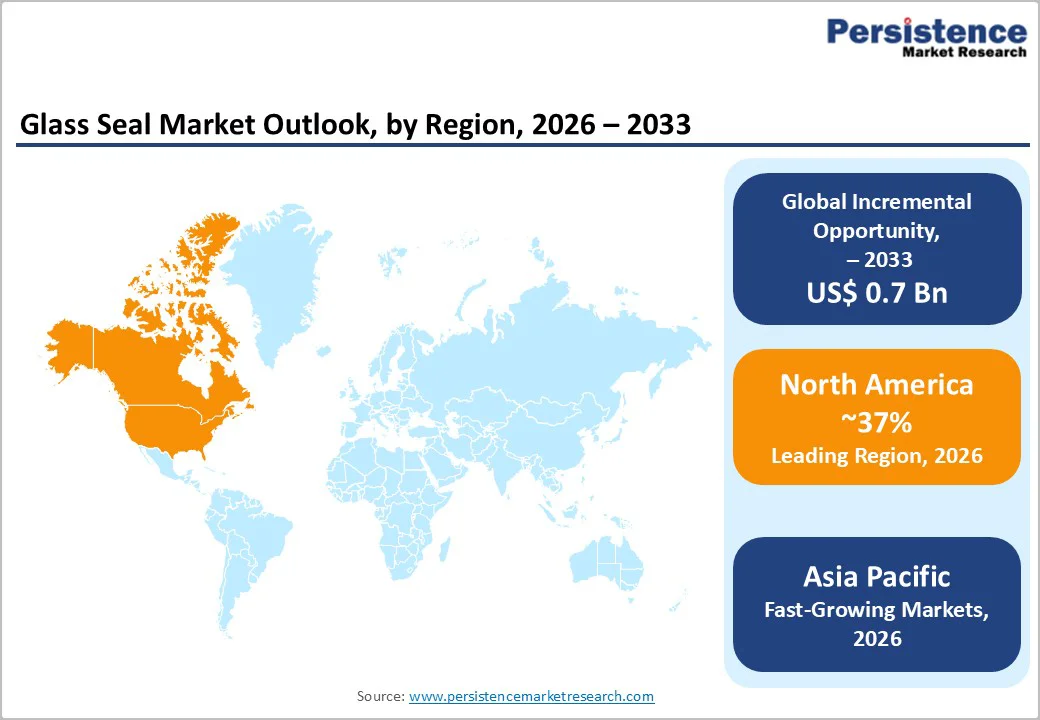

- Leading Region: North America maintains market leadership anchored by United States aerospace and defense dominance, advanced electronics manufacturing base, significant medical device concentration, and strong regulatory framework supporting high-performance glass seal adoption.

- Fastest Growing Region: Asia-Pacific commands fastest expansion driven by China's manufacturing dominance and electronics fabrication growth at 4.2% CAGR, coupled with India emerging as world's fastest-growing market through rapid industrialization and electronics sector expansion.

- Dominant Application: Aerospace and defense applications command market leadership with 25% market share in 2024, driven by extreme-environment reliability requirements, critical component performance specifications, and sustained defense spending exceeding US$ 740 billion annually.

- Growing Application: Aerospace and defense applications experiencing fastest expansion at 8% CAGR, propelled by aerospace market projected reach of US$ 1 trillion by 2034, military system modernization, and next-generation aircraft development programs.

- Key Market Opportunity: 5G infrastructure deployment and advanced communication technology expansion, combined with IoT device proliferation and medical device innovation, create exceptional growth potential through telecommunications ecosystem expansion and implantable sensor development.

| Key Insights | Details |

|---|---|

| Global Glass Seal Market Size (2026E) | US$ 2.1 Bn |

| Market Value Forecast (2033F) | US$ 2.8 Bn |

| Projected Growth CAGR(2026-2033) | 4.2% |

| Historical Market Growth (2020-2025) | 3.8% |

Market Dynamics

Market Growth Drivers

Rising Demand for Hermetic Sealing in Electronics, Automotive, and Aerospace Applications

The growing demand for hermetic and high-reliability sealing solutions across electronics, automotive, aerospace, and defense industries is one of the primary drivers of the global glass seal market is. Glass seals, particularly glass-to-metal seals, are essential in applications requiring airtight, moisture-proof, and corrosion-resistant performance under extreme operating conditions such as high temperatures, pressure differentials, vibration, and exposure to aggressive chemicals. In the electronics sector, the rapid proliferation of sensors, connectors, semiconductors, and power electronics has increased the need for reliable sealing to protect sensitive components from environmental degradation and electrical failure. Advanced applications such as electric vehicles (EVs), autonomous driving systems, and industrial automation rely heavily on sealed sensors and control units, directly supporting glass seal demand.

In the automotive and aerospace sectors, stringent safety standards and long service-life requirements further reinforce adoption. Glass seals are widely used in engine sensors, ignition systems, fuel control units, avionics, and satellite components, where failure is not an option. As aerospace programs expand and defense modernization accelerates globally, demand for high-performance hermetic sealing continues to rise. Additionally, the miniaturization of electronic components increases sealing complexity, favoring glass seals due to their thermal expansion compatibility, mechanical strength, and long-term stability. These characteristics make glass seals a preferred solution over polymer-based alternatives, positioning high-reliability industrial and electronic applications as a sustained growth engine for the global glass seal market.

Expansion of Medical Devices and Healthcare Electronics

The rapid expansion of the medical devices and healthcare electronics industry is another major driver fueling growth in the global glass seal market. Medical applications demand exceptional reliability, biocompatibility, and contamination-free performance, making glass seals a critical component in devices such as implantable sensors, pacemakers, diagnostic equipment, imaging systems, and laboratory instrumentation. Glass seals provide hermetic protection that prevents moisture ingress, gas leakage, and microbial contamination, ensuring consistent device performance over extended lifecycles, an essential requirement in both implantable and life-supporting medical technologies.

Global healthcare expenditure growth, aging populations, and increasing prevalence of chronic diseases are driving demand for advanced medical electronics and monitoring systems. The shift toward minimally invasive procedures and wearable or implantable medical devices further accelerates adoption of compact, sealed electronic components. In addition, stricter regulatory standards governing medical device safety and reliability are compelling manufacturers to use proven, certified sealing technologies, strengthening the competitive position of glass seals over alternative Technologys.

The COVID-19 pandemic also highlighted the importance of reliable diagnostic and monitoring equipment, leading to long-term investment in healthcare infrastructure and medical technology innovation. Emerging markets are expanding healthcare access and domestic medical device manufacturing, creating incremental demand for sealing components. As healthcare technology continues to evolve toward precision, miniaturization, and long-term reliability, the medical sector is expected to remain a strong and resilient demand driver for the global glass seal market throughout the forecast period.

Market Restraints

High Manufacturing Costs and Technical Complexity Limiting Market Penetration

The high manufacturing cost associated with glass-to-metal and hermetic glass seals is one of the key restraints impacting the global glass seal market is. The production process requires precise Technology selection, controlled thermal expansion matching, and highly specialized equipment to ensure reliable bonding between glass and metal components. Any mismatch in coefficients of thermal expansion (CTE) can lead to cracking, seal failure, or reduced long-term reliability, increasing rejection rates and production losses. As a result, manufacturers must invest heavily in advanced furnaces, precision tooling, and stringent quality control systems, significantly elevating capital and operating expenditures.

In addition, glass seal manufacturing often involves customized designs tailored to specific Application applications, particularly in aerospace, medical devices, and electronics. This customization limits economies of scale and increases per-unit costs compared to standardized polymer or elastomer sealing solutions. Skilled labor requirements further add to cost pressures, as experienced technicians are needed to manage thermal cycles, Technology handling, and inspection procedures. These cost barriers can discourage small and mid-sized manufacturers from adopting glass seals, especially in cost-sensitive markets. For end users, higher component costs may limit adoption in non-critical applications, restraining broader market penetration despite the performance advantages of glass seals.

Competition from Alternative Sealing Technologies

The growing competition from alternative sealing technologies, including elastomer seals, polymer gaskets, and advanced epoxy-based sealing solutions is another major restraint for the global glass seal market is. These alternatives offer lower upfront costs, simpler installation, and greater design flexibility, making them attractive for applications where extreme hermeticity or high-temperature resistance is not essential. In consumer electronics, appliances, and certain industrial applications, manufacturers increasingly prefer polymer-based seals due to shorter production cycles and reduced Technology costs.

Advancements in high-performance polymers and composite Technologys have further intensified this competitive pressure. Modern elastomers now provide improved chemical resistance, thermal stability, and durability, narrowing the performance gap with glass seals in mid-range applications. Additionally, alternative sealing solutions allow for easier rework, replacement, and design modification, whereas glass seals are typically permanent and non-repairable once installed. This limits their appeal in fast-evolving product designs and short product lifecycles.

As industries focus on cost optimization and rapid innovation, many manufacturers opt for flexible sealing solutions unless strict regulatory or performance requirements mandate glass seals. This substitution risk continues to restrain market growth, particularly outside high-reliability sectors such as aerospace, medical, and defense applications.

Market Opportunities

5G Infrastructure Deployment and Advanced Communication Technology Expansion

Rapid expansion of 5G networks and increasing deployment of advanced communication technologies create substantial opportunity for glass seal suppliers providing solutions for telecommunications infrastructure components. Telecom companies continuing to invest heavily in developing next-generation technologies and communication infrastructure establish multi-year procurement cycles for reliable and sustainable seal solutions.

Integration of high-frequency components and advanced packaging technologies in 5G base stations and network equipment necessitates specialized glass sealing solutions offering superior electromagnetic compatibility and environmental protection. IoT device proliferation supporting 5G ecosystem expansion generates incremental sensor sealing demand across smart cities, industrial IoT, and consumer IoT applications, establishing sustained growth opportunity through forecast period.

Medical Device Innovation and Implantable Sensor Market Acceleration

Medical device industry expansion and implantable sensor development represent exceptional growth opportunity driven by aging global population and increasing prevalence of chronic diseases requiring continuous health monitoring. Implantable pulse generators including pacemakers requiring moisture ingress prevention meeting ISO 14708-1 standards with moisture ingress limited to 1 × 10 atm-cc-s establish performance requirements achievable exclusively through glass-to-metal sealing solutions.

Medtronic shipped 850,000 rhythm-management devices in 2024, with each device requiring titanium shell brazed to glass-to-metal feedthrough, establishing significant existing demand baseline with substantial growth potential as advanced implantable devices proliferate. Biocompatible sealing requirements and miniaturization trends in medical device design create market opportunity for specialized glass formulations supporting long-term biocompatibility and enhanced device miniaturization, establishing sustained growth momentum through forecast period.

Category-wise Insights

Product Type Analysis

Low-temperature sealing glass representing approximately 45% market share and growing faster than high-temperature alternatives reflects accelerating adoption in miniaturized electronics applications. LTSG melting and sealing at 400-700°C compared to traditional high-temperature glass requiring ~1000°C offers distinct advantage for temperature-sensitive component integration including MEMS devices, solid oxide fuel cells, OLED displays, and vacuum insulation panels. Continued innovation in glass-ceramic hybrid formulations and lead-free alternatives supporting regulatory compliance establishes sustained market expansion throughout forecast period.

Technology Analysis

Hermetic sealing represents highest-value market segment commanding 45% revenue share despite representing smaller unit volume relative to standard sealing solutions. Hermetic seals achieving leak rates below 1 × 10 mbar·l/s establish performance standard required for critical aerospace, defense, and medical applications where absolute hermeticity prevents catastrophic failure. Hermetic sealing technology development emphasizing sub-nanoleak performance with routine screening down to 1 × 10 atm-cc-s through helium bombing, residual-gas analysis, and automated micro-CT inspection demonstrates technology sophistication and quality assurance excellence.

Premium positioning enabled by superior hermeticity supports higher pricing and margin profiles attracting tier-one aerospace and defense contractors. Continued investment in hermetic sealing technology advancement combined with expanding application scope establishes sustained growth opportunity throughout forecast period.

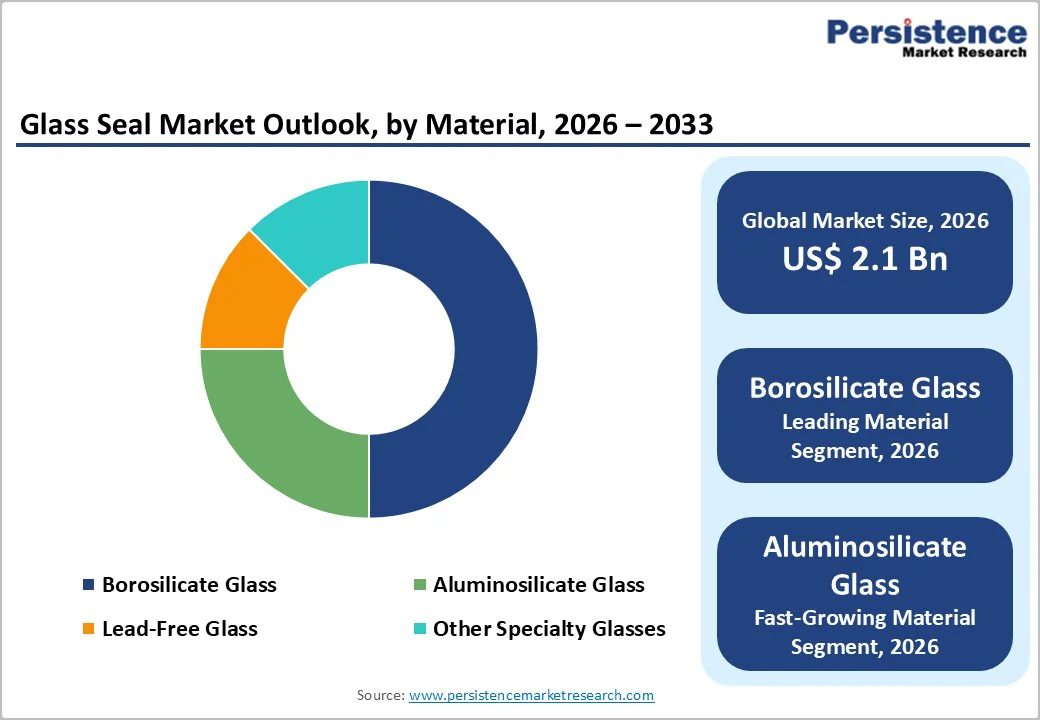

Material Type Analysis

Borosilicate glass maintains dominant Technology position commanding 70% market share driven by superior thermal expansion coefficient matching capabilities, exceptional chemical stability, high mechanical strength, and remarkable heat resistance supporting diverse application requirements. Borosilicate Technology composition flexibility enabling customized CTE matching across copper, steel, and specialty alloys establishes preferred solution for complex multi-Technology assemblies. Lead-free borosilicate formulations gaining market share reflecting RoHS and REACH regulatory compliance requirements particularly in consumer electronics and medical device applications.

Aluminosilicate glass capturing 20-25% market share reflects growing demand for specialized thermal expansion characteristics and enhanced performance optimization in demanding applications. Emerging glass-ceramic hybrid compositions incorporating nanoparticle enhancements establish innovation frontier supporting next-generation sealing performance and lower-temperature processing capabilities, ensuring sustained market expansion through forecast period.

Application Analysis

Aerospace and defense applications dominate glass seal market with 25% market share in 2026 and fastest-growing segment at 8% CAGR driven by critical reliability requirements in extreme-environment applications. Vacuum feedthrough, thermal sensor, and electronic package applications representing primary use cases in aerospace and defense sectors require absolute sealing integrity and superior long-term environmental stability. Military and defense system modernization combined with next-generation aircraft development establish multi-year procurement cycles supporting sustained revenue growth.

Automotive application segment experiencing 5.6% CAGR significantly below aerospace growth rate reflects emerging electrification opportunity offset by mature traditional sensor base. Medical and healthcare applications demonstrating 5.9% growth trajectory driven by implantable device advancement and diagnostic equipment miniaturization establish secondary high-growth opportunity segment.

Regional Insights

North America Glass Seal Trends

North America maintains developed market maturity with United States commanding regional leadership through strong aerospace and defense industry presence, advanced electronics manufacturing base, and significant medical device concentration. U.S. low-temperature sealing glass market estimated at USD 42.9 million in 2024 demonstrates substantial established demand base supporting technology innovation and commercialization activities. Aerospace and defense procurement concentration in California, Texas, and Florida establishes regional manufacturing clusters supporting local glass seal supplier ecosystem. Medical device innovation ecosystem particularly concentrated in Massachusetts, California, and Minnesota creates specialized demand for biocompatible and implantable sensor sealing solutions.

Europe Glass Seal Trends

Europe represents significant developed market with Germany and United Kingdom commanding regional leadership through established industrial base, advanced manufacturing expertise, and stringent regulatory environment. Germany experiencing 1.2% CAGR in low-temperature sealing glass segment reflects semiconductor packaging innovation focus and industrial automation advancement. RoHS and REACH regulatory frameworks establishing mandatory lead-free and eco-friendly requirements drive innovation in sustainable sealing glass formulations. Strong automotive manufacturing base particularly in Germany and UK supporting sensor integration advancement in vehicle electrification initiatives.

Asia Pacific Glass Seal Trends

Asia-Pacific commands fastest regional growth with China at 4.2% CAGR for low-temperature sealing glass and India emerging as fastest-growing market globally driven by rapid industrialization and electronics manufacturing expansion. China establishing position as global manufacturing hub for glass seal production through vertically integrated supply chains and manufacturing cost advantages supporting regional market expansion. Growing electronics manufacturing base across semiconductor fabrication and consumer electronics production generates substantial incremental demand for advanced sealing solutions. Japan maintaining mature market presence with 0.8% CAGR reflecting established industrial and consumer electronics sector reliance on high-quality glass sealing components.

Competitive Landscape for the Glass Seal Market

The glass seal market exhibits a moderately consolidated competitive structure dominated by global industrial leaders including Electrovac, AMETEK, Kyocera, Nippon Electric Glass, and Schott AG commanding substantial combined market share. Tier 1 manufacturers leveraging established technology platforms, manufacturing scale, and global distribution networks to maintain competitive advantage. Regional competitors including Egide Group, SGA Technologies, and Specialty Seal Group establish competitive positions through specialized product offerings and localized customer service.

Technology differentiation strategies emphasizing innovation in lead-free formulations, nanoparticle-enhanced frits, and glass-ceramic hybrids create competitive differentiation opportunities. R&D investment focus on low-temperature sealing, hermetic performance enhancement, and advanced Technology development establishes innovation-driven competition supporting sustained market growth.

Key Market Developments

- In September 2025, Schott AG unveiled cutting-edge glass solutions for advanced semiconductor packaging at SEMICON Taiwan 2025, demonstrating commitment to innovation in next-generation packaging technologies and high-performance glass applications.

- In July 2025, Kyocera Corporation expanded its soft glass seal product portfolio by launching a new range of high-temperature soft glass formulations designed for next-generation power electronics and automotive sensor applications, reinforcing the company’s focus on Technology innovation and performance optimization in demanding operational environments.

- In October 2025, Hermetic Solutions Group announced a strategic partnership with a leading aerospace OEM to co-develop customized soft glass seal assemblies for advanced avionics and satellite systems, enhancing reliability in extreme thermal cycles and highlighting the critical role of hermetic sealing in space-grade electronics.

Companies Covered in Glass Seal Market

- Electrovac

- AMETEK.Inc..

- KYOCERA Corporation

- EGIDE Group

- SGA Technologies

- Elan Technology

- Specialty Seal Group

- Nippon Electric Glass

- Schott AG

- Hermetic Solutions Group LLC

- Rosenberger

- Egide Group

- Concept Group LLC

- Elan Technology

- Emerson Fusite

Frequently Asked Questions

The global Glass Seal Market is projected to reach US$ 2.8 billion by 2033, expanding from US$ 2.1 billion in 2026 at a CAGR of 4.2%, driven by aerospace and defense expansion, automotive electrification, sensor proliferation, medical device innovation, and 5G infrastructure deployment.

Market demand growth is driven by multiple converging factors including aerospace and defense sector expansion, automotive electrification with 18+ hermetic sensors per vehicle, miniaturization megatrend in electronics requiring reliable sealing solutions, 5G infrastructure deployment, medical device innovation for implantable applications, extreme environment reliability requirements, and regulatory compliance mandates for RoHS and REACH lead-free formulations.

Aerospace and defense applications command market dominance with approximately 25% market share in 2026, driven by critical reliability requirements in extreme-environment applications, multi-million-dollar defense procurements, and next-generation aircraft programs requiring superior hermetic sealing solutions for vacuum feedthroughs, thermal sensors, and electronic packages.

North America maintains market leadership anchored by United States market dominance, supported by strong aerospace and defense industry presence, advanced electronics manufacturing base, significant medical device concentration, and stringent regulatory framework supporting high-performance glass seal adoption throughout developed market infrastructure.

Major market opportunities include 5G infrastructure deployment driving telecommunications equipment sealing demand; electric vehicle electrification requiring sensor and power module sealing solutions; implantable medical device innovation at ISO 14708-1 compliance standards; autonomous vehicle advancement requiring ADAS sensor integration.

Leading market players include Electrovac maintaining global leadership through hermetic package specialization; AMETEK Inc. commanding substantial market share through diversified aerospace and defense focus; Nippon Electric Glass establishing Asia-Pacific dominance; KYOCERA Corporation leveraging advanced materials expertise; and Schott AG driving semiconductor packaging innovation at SEMICON Taiwan 2025.