- Smart Packaging

- Recycled Glass Market

Recycled Glass Market Size, Share, and Growth Forecast, 2026 - 2033

Recycled Glass Market By Product Type (Cullet, Glass Powder, Crushed Glass), Application (Glass Bottles & Containers, Fiberglass, Others), Source, and Regional Analysis for 2026 - 2033

Recycled Glass Market Size and Trends Analysis

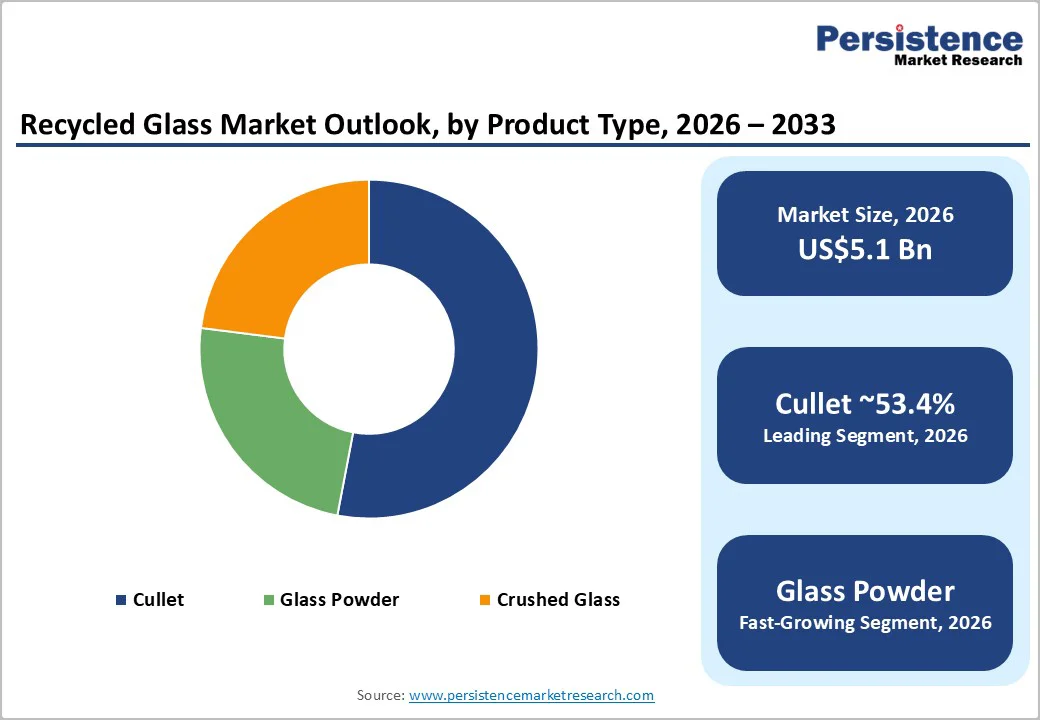

The global recycled glass market size is likely to be valued at US$5.1 billion in 2026 and is expected to reach US$7.5 billion by 2033, growing at a CAGR of 5.7% between 2026 and 2033, driven by stricter packaging regulations, expanding circular-economy mandates, and rising glass collection and remelt rates across developed economies.

Rising use of cullet in container glass, construction, and insulation supports steady demand growth. Recycled glass lowers energy use and carbon emissions, improving manufacturers’ cost competitiveness, while industry consolidation boosts operational efficiency. Although contamination and transport costs remain challenges, investments in advanced sorting and partnerships are expanding remelt capacity and strengthening long-term market stability.

Key Industry Highlights

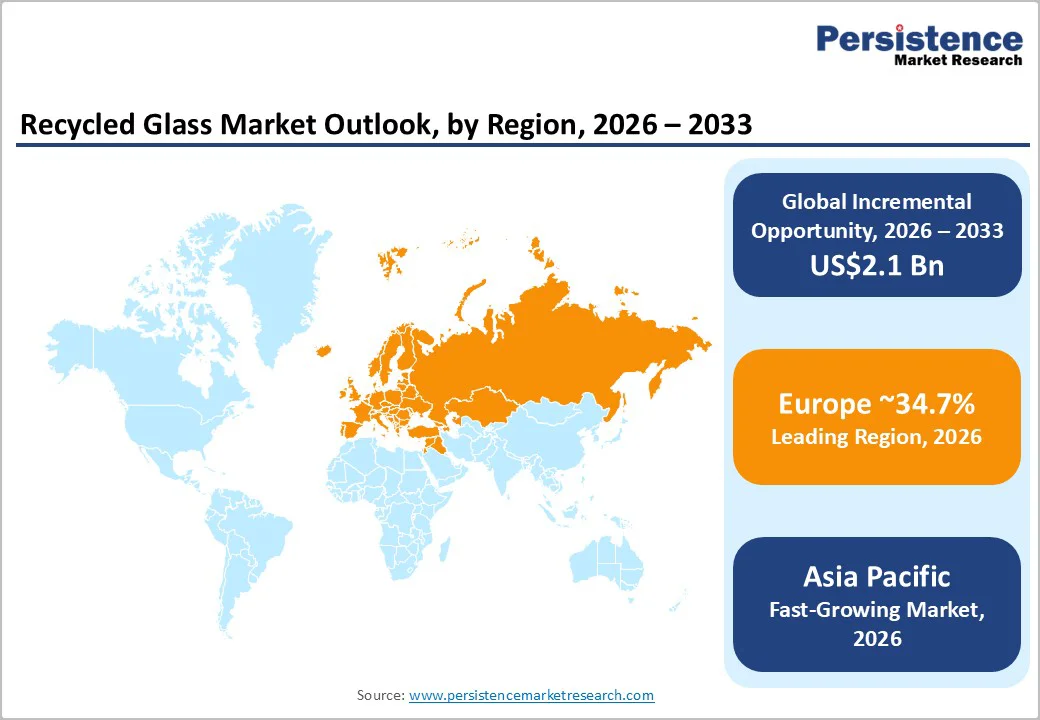

- Leading Region: Europe is projected to account for approximately 34.7% of global market share, driven by high glass collection rates, well-established deposit return systems, and harmonized EU packaging and circular economy regulations that ensure consistent, high-quality cullet supply.

- Fastest-growing Region: Asia Pacific, to record the highest growth rate globally, supported by rapid urbanization, expanding packaged food and beverage consumption, and increasing use of recycled glass in containers, fiberglass, and construction applications across China, Japan, India, and ASEAN.

- Investment Plans: Ongoing investments are concentrated in advanced sorting, color separation, and furnace upgrades, particularly in Europe and North America, where glass manufacturers are increasing recycled content levels to 60% or higher. Asia Pacific is attracting capital into new sorting facilities and public-private recycling partnerships, supporting long-term feedstock availability.

- Dominant Product Type: Cullet is anticipated to represent approximately 53.4% of market share, supported by its direct use in container glass manufacturing, lower processing costs, and energy savings of up to 20-30% during glass melting operations.

- Leading Application: Glass bottles & containers are estimated to account for around 50% of total end-user consumption, driven by beverage and food packaging demand, recycled content mandates, and long-term supply contracts between recyclers and container glass manufacturers.

| Key Insights | Details |

|---|---|

| Recycled Glass Market Size (2026E) | US$5.1 Bn |

| Market Value Forecast (2033F) | US$7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Push for Circular Packaging and High Collection Targets

Government-led circular economy initiatives and packaging waste regulations have significantly increased recycled glass demand, particularly in Europe. National deposit-return systems and extended producer responsibility frameworks have raised glass collection and remelt targets, directly increasing the supply and use of high-quality cullet. Europe accounts for approximately 34.7% of the global market share, reflecting its regulatory leadership and mature recycling infrastructure. Countries with deposit schemes regularly achieve glass collection rates above 70-80%, ensuring consistent feedstock availability for remelters. These regulatory measures reduce reliance on virgin raw materials and create a stable demand environment for recycled glass processors, strengthening long-term investment confidence across the value chain.

Energy and Carbon Efficiency Advantages in Glass Manufacturing

Using recycled glass in place of virgin raw materials delivers substantial energy and emissions benefits in glass manufacturing. High cullet input levels can reduce furnace energy consumption by 20-30%, while also lowering carbon dioxide emissions associated with raw material extraction and melting. These operational efficiencies translate into direct cost savings for glass manufacturers and support compliance with corporate emissions reduction targets. As companies expand net-zero and Scope 3 emissions commitments, demand for certified recycled inputs continues to rise. This trend favors cullet and high-quality recycled glass powder across container, flat glass, and industrial applications, reinforcing recycled glass as a strategic material input.

Expansion of Industrial and Construction Applications

Recycled glass applications have expanded well beyond container remelting into fiberglass insulation, construction aggregates, highway beads, abrasives, and fillers. Growth in energy-efficient buildings and infrastructure spending has increased demand for fiberglass and sustainable construction materials, which absorb large volumes of processed recycled glass. These higher-value applications support investments in glass powder and crushed glass production, reducing dependence on traditional container markets. While packaging remains the largest application, faster growth in fiberglass and construction uses is structurally increasing the total addressable market and improving margin potential for processors with diversified product portfolios.

Barrier Analysis - Contamination and Quality Challenges in Collection Streams

Glass contamination remains a critical constraint for recycled glass processing. Ceramics, stones, mixed colors, and organic residues reduce remelt yields and increase sorting costs, often forcing processors to downcycle material into lower-value applications. Advanced sorting and washing technologies can significantly reduce contamination, but these systems require substantial capital investment, limiting adoption among smaller operators. In regions with poor source separation, effective remelt volumes can be 10-25% lower than in best-practice systems, constraining overall supply efficiency and profitability.

Transportation and Logistics Cost Pressures

Glass is heavy and relatively low in value per ton, making transportation costs a major determinant of profitability. Rising fuel prices and freight costs erode margins, particularly when cullet must be transported over long distances. These logistics challenges favor localized consumption and regional processing hubs, limiting the scalability of centralized recycling operations. While processors increasingly invest in localized collection networks and partnerships to manage costs, infrastructure gaps in certain regions restrict rapid market expansion.

Opportunity Analysis - Advanced Sorting Systems and Digital Traceability

Investments in advanced optical sorting, artificial intelligence-driven quality control, and digital traceability systems present a strong growth opportunity. These technologies improve remelt yields and enable processors to supply certified low-contamination cullet at premium pricing. Markets adopting sensor-based sorting can increase remelt-quality glass output by 15-20%, enhancing overall supply efficiency. Co-investment models involving municipalities, beverage companies, and recyclers are emerging as practical pathways to finance these upgrades while securing long-term feedstock agreements.

Growth in Fiberglass and High-Value Industrial Feedstocks

Fiberglass market manufacturing represents the fastest-growing end-use segment for recycled glass. Rising insulation demand driven by building efficiency regulations is increasing the need for recycled glass powder and processed cullet. Converting just 5-10% of existing cullet volumes into fiberglass feedstock could generate a multi-hundred-million-dollar market by 2030. Processors that invest in grinding, micronization, and quality control capabilities can capture higher margins and reduce exposure to cyclical container glass demand.

Category-wise Analysis

Product Type Insights

Cullet is anticipated to dominate, accounting for 53.4% of the revenue share, primarily due to its direct and large-scale use in container glass manufacturing and industrial furnaces. Beverage and food packaging producers increasingly incorporate high cullet ratios to comply with recycled-content mandates and reduce melting temperatures.

For example, beer, wine, and non-alcoholic beverage bottles commonly contain 30-70% recycled glass, depending on color and quality requirements. The relatively simple processing steps involved in cullet production, such as crushing, cleaning, and color sorting, enhance cost efficiency compared with more refined recycled glass products. Large integrated processors manage end-to-end operations covering collection, processing, and logistics, enabling consistent cullet quality and reliable supply. This operational scale allows glass manufacturers to increase recycled content while achieving energy savings of up to 20-30% per production cycle, reinforcing cullet’s leadership position.

Glass powder is likely to be the fastest-growing recycled glass product type, supported by rising demand from fiberglass insulation, polymer fillers, and specialty construction materials. Micronized recycled glass is increasingly used as a substitute for silica sand and other mineral fillers in applications such as thermal insulation panels, reinforced plastics, paints, and coatings.

In the construction sector, glass powder is also incorporated into cement blends, terrazzo flooring, and architectural concrete to improve durability and sustainability profiles. Higher unit pricing, combined with value-added processing such as grinding and micronization, improves profit margins relative to bulk cullet. These advantages make glass powder an attractive diversification pathway for mid-sized recyclers seeking to reduce exposure to cyclical container glass demand while serving higher-growth industrial markets.

Application Insights

Glass bottles and containers are expected to lead, accounting for 50% of the revenue share, reflecting the glass industry’s high reliance on cullet as a furnace feedstock. Beverage and food manufacturers, including soft drinks, beer, spirits, sauces, and preserved foods, increasingly specify minimum recycled content levels to meet sustainability commitments and regulatory requirements.

Long-term supply contracts between bottle manufacturers and recyclers ensure consistent cullet availability, particularly for amber and green glass, which tolerate higher recycled content ratios. Regulatory pressure in regions with advanced collection systems further reinforces this segment’s dominance, as manufacturers prioritize recycled inputs to lower energy use, reduce raw material costs, and achieve packaging circularity targets.

Fiberglass is likely to be the fastest-growing end-use segment for recycled glass, driven by expanding demand for thermal and acoustic insulation in residential, commercial, and industrial construction. Insulation manufacturers increasingly replace virgin raw materials with recycled glass powder to reduce emissions and improve environmental credentials. Examples include wall insulation, ceiling panels, pipe insulation, and HVAC duct liners, all of which consume significant volumes of processed recycled glass.

Stricter building energy codes and green construction standards are accelerating adoption, particularly in large-scale housing and infrastructure projects. These trends are encouraging long-term supply agreements and targeted investments in specialized glass powder production, strengthening recycled glass integration into the fiberglass value chain.

Regional Insights

North America Recycled Glass Market Trends - Corporate-Led Demand Growth and Infrastructure Modernization

North America represents a strategically important recycled glass market, led overwhelmingly by the U.S., which accounts for the majority of regional demand and processing capacity. While the region’s overall market share trails Europe, the U.S. supplies substantial volumes of cullet to container glass, fiberglass, and industrial end-users. National glass recycling rates remain in the low-to-mid 30% range, reflecting uneven collection systems, although states with container deposit legislation, such as California, Oregon, and Michigan, consistently achieve recycling rates exceeding 75-80%. This structural disparity directly influences cullet quality and regional pricing dynamics.

Market growth is increasingly driven by corporate sustainability commitments and infrastructure investment rather than federal mandates. Major glass manufacturers such as Owens-Illinois (O-I Glass) and Ardagh Group have expanded recycled content targets across their North American container portfolios, increasing demand for furnace-ready cullet. In response, recyclers, including Strategic Materials (a Nexeo company) and Momentum Recycling, have invested in advanced optical sorting and cleaning systems to reduce contamination and improve color separation. These investments improve cullet yield and enable higher recycled content ratios, particularly for amber and flint glass.

Industry consolidation is reshaping the competitive landscape, improving scale efficiencies and logistics integration. Partnerships between municipalities and private processors are becoming more common, particularly in states seeking to modernize material recovery facilities (MRFs). For example, Closed Loop Partners has supported financing for recycling infrastructure upgrades, indirectly strengthening cullet supply reliability. Together, these developments are stabilizing long-term supply contracts and supporting moderate but consistent regional market growth.

Europe Recycled Glass Market Trends - High-Collection Systems and Regulation-Backed Remelt Dominance

Europe is projected to lead the market with approximately 34.7% share, underpinned by high collection rates, deposit return systems, and harmonized packaging regulations under the EU Circular Economy framework. Glass packaging collection rates across the region typically exceed 75-80%, providing a reliable supply of high-quality cullet. This structural advantage supports large-scale remelt operations and positions recycled glass as a core input rather than a supplementary material.

Germany, the U.K., France, and Spain anchor regional performance through robust regulatory enforcement and advanced recycling infrastructure. Germany’s long-established deposit return scheme (Pfand) delivers exceptionally clean cullet streams, enabling glass manufacturers to achieve recycled content levels above 60% in many container applications. In France, extended producer responsibility (EPR) obligations have pushed brand owners to increase recycled glass usage, benefiting processors such as Verallia, which has invested heavily in furnace upgrades to accommodate higher cullet ratios.

Recent developments reflect continued capital investment across the value chain. Saint-Gobain has expanded recycled glass utilization in both flat glass and insulation manufacturing, linking recycled feedstock directly to emissions reduction targets. Similarly, Vetropack Group announced investments in modernizing furnaces in Southern Europe to improve energy efficiency and recycled content integration. These initiatives reinforce Europe’s leadership by aligning regulation, industrial capacity, and sustainability goals, ensuring stable long-term growth rather than cyclical expansion.

Asia Pacific Recycled Glass Market Trends - Urbanization-Fueled Volume Growth and Upgrading Cullet Utilization

Asia Pacific is likely to be the fastest-growing recycled glass market, driven by rapid urbanization, rising packaged food and beverage consumption, and industrial expansion across China, Japan, India, and ASEAN economies. Although per-capita recycling rates remain below European levels, the region’s scale and population growth generate increasing absolute volumes of recoverable glass. This dynamic positions Asia Pacific as a critical growth engine for the global recycled glass industry.

China plays a central role, with policy initiatives promoting waste reduction and industrial efficiency, encouraging greater use of recycled inputs. Leading container glass producers such as China Glass Holdings and Xinyi Glass have expanded cullet utilization to lower energy costs and comply with environmental performance benchmarks. In Japan, high consumer participation in waste separation and advanced processing technologies support consistent cullet quality, benefiting companies such as AGC Inc., which integrates recycled glass across flat glass and construction applications.

India and Southeast Asia represent emerging opportunity markets, where private-public partnerships are accelerating infrastructure development. In India, companies such as Asahi India Glass (AIS) have increased recycled glass use in automotive and architectural glass as urban construction expands. ASEAN countries, including Thailand and Vietnam, are attracting investment in sorting facilities as multinational beverage brands push for higher recycled content in packaging. Collectively, these developments are shifting Asia Pacific from low-value cullet use toward higher-value applications, reinforcing its position as the fastest-growing regional market.

Competitive Landscape

The global recycled glass market is moderately fragmented, consisting of large integrated processors and numerous regional recyclers. Market concentration is increasing through acquisitions and vertical integration, as companies seek scale advantages in logistics, sorting technology, and supply consistency.

Large-scale acquisitions have strengthened vertical integration and expanded geographic processing capacity. Higher reported glass collection rates in Europe have accelerated investments in remelt and sorting infrastructure. Partnerships between recyclers and insulation manufacturers have expanded glass powder and fiberglass feedstock supply chains.

Key strategies include vertical integration across collection and processing, investment in advanced sorting and micronization technologies, and long-term offtake agreements with container and fiberglass manufacturers. Traceability and consistent quality remain primary competitive differentiators.

Key Industry Developments

- In August 2025, Verallia launched a new line of 100% post-consumer recycled glass packaging, reinforcing its sustainability strategy and reducing the environmental footprint of its products for beverage and food brands.

- In April 2025, Visy, New Zealand’s sole glass manufacturer, achieved an average of 70% recycled glass content in its locally produced bottles and jars, marking a major regional milestone for circular packaging adoption.

Frequently Asked Questions

The global recycled glass market is estimated to be valued at US$5.1 billion in 2026.

By 2033, the recycled glass market is projected to reach US$7.2 billion.

Key trends include higher recycled content mandates in glass packaging, growing adoption of recycled glass in fiberglass and construction materials, investments in advanced sorting and color separation technologies, and increasing long-term supply contracts between recyclers and glass manufacturers to ensure consistent cullet quality.

Cullet is the leading product segment, accounting for around 53.4% of total market share, due to its direct use in container glass manufacturing and energy-saving benefits during remelting.

The market is expected to grow at a CAGR of 5.7% between 2026 and 2033.

Major players with strong global and regional portfolios include Sibelco, Strategic Materials, Inc., Owens-Illinois, Ardagh Group, and Verallia.