- Pharmaceuticals

- Global Flu RNA Vaccines Market

Global Flu RNA Vaccines Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Flu RNA Vaccines Market by Vaccine Type (Non‑replicating mRNA, Self‑replicating mRNA, Dendritic cell mRNA, Others), by Application (Hospitals, Vaccination centers, Clinics, Pharmacies), by Service, by Distribution Channel, and Regional Analysis from 2026 to 2033

Flu RNA Vaccines Market Size and Trend Analysis

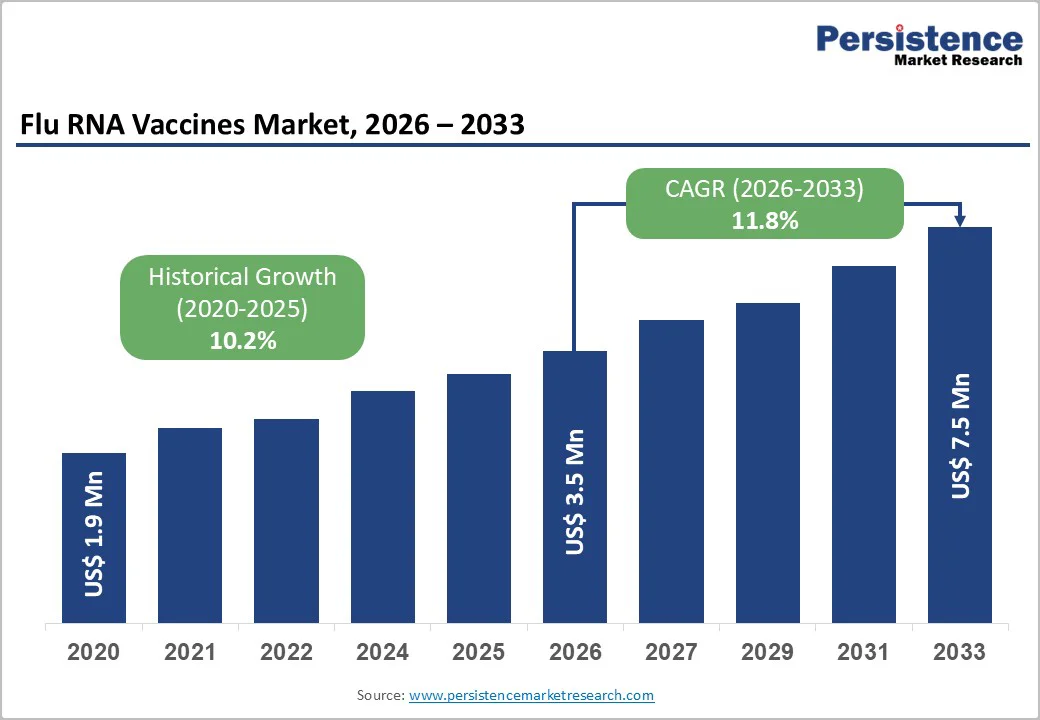

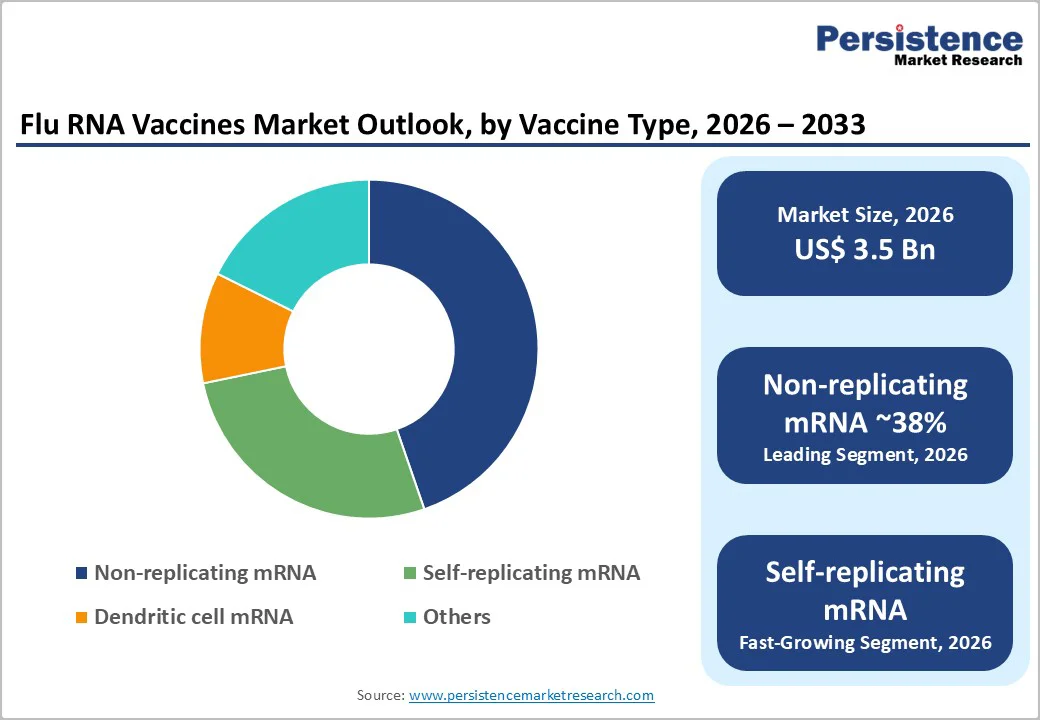

The global flu RNA vaccines market is estimated to grow from US$3.5 billion in 2026 to US$7.5 billion by 2033. The market is projected to record a CAGR of 11.8% during the forecast period from 2026 to 2033.

The flu RNA vaccines industry is an emerging segment within the global influenza vaccine industry, driven by advancements in mRNA technology and growing demand for rapid, effective flu-prevention solutions. RNA-based vaccines offer advantages such as faster development, higher precision, and the ability to target multiple influenza strains simultaneously. The market encompasses non-replicating and self-amplifying mRNA vaccines, targeting hospitals, clinics, and vaccination centers worldwide.

Key Industry Highlights

- mRNA vaccines offer precise targeting of multiple influenza strains, potentially improving immune response and protection rates.

- Companies like Moderna, Pfizer, and BioNTech are conducting extensive trials to validate safety and efficacy globally.

- The market includes both non-replicating and self-amplifying RNA vaccines, catering to different therapeutic and immune response needs.

- The market is expanding rapidly, driven by rising influenza prevalence and growing awareness of advanced preventive solutions.

- Partnerships between pharma giants and biotech firms are strengthening pipelines and accelerating the commercialization of RNA flu vaccines.

| Global Market Attributes | Key Insights |

|---|---|

| Flu RNA Vaccines Market Size (2026E) | US$3.5 Bn |

| Market Value Forecast (2033F) | US$7.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 10.2% |

Market Dynamics

Driver – Rising Influenza Incidence

Rising Influenza Incidence is a major driver of the Flu RNA vaccines market, as seasonal flu continues to impose a significant global health burden. Each year, millions of people worldwide are affected by influenza, resulting in hospitalizations, complications, and economic losses. The virus’s high mutation rate and the emergence of new strains make traditional vaccines less effective, highlighting the urgent need for more adaptive and precise preventive solutions. RNA-based vaccines are uniquely positioned to address this challenge, offering rapid development cycles that can be quickly modified to target circulating strains. This flexibility is especially crucial in regions experiencing frequent influenza outbreaks, where timely immunization can prevent large-scale morbidity and mortality. Additionally, increased urbanization, international travel, and climate-related changes in viral transmission patterns contribute to higher infection rates, further elevating the demand for innovative vaccines. Public awareness of flu-related risks has grown significantly, encouraging individuals and governments to seek more effective vaccination strategies. As a result, healthcare systems and policymakers are increasingly investing in RNA vaccine platforms, recognizing their potential to provide faster, safer, and more efficacious protection against evolving influenza viruses. Rising influenza incidence, therefore, directly accelerates research, production, and adoption of RNA-based flu vaccines globally.

Restraints – Intellectual Property Barriers in the Flu RNA Vaccines Market

Intellectual property (IP) barriers present a significant challenge in the development and commercialization of flu RNA vaccines. The RNA vaccine landscape is highly technology-intensive, with key innovations such as mRNA sequence optimization, lipid nanoparticle delivery systems, and self-amplifying RNA platforms protected by patents. These proprietary technologies are often held by leading biotech and pharmaceutical companies like Moderna, BioNTech, and CureVac. As a result, smaller biotechnology firms or new entrants face substantial obstacles when attempting to develop competitive RNA-based flu vaccines. Licensing agreements for these patented technologies can be costly and time-consuming, limiting the ability of smaller players to scale operations or innovate independently.

Additionally, the complexity of navigating global patent laws and regulatory frameworks further complicates market entry. The risk of patent infringement claims may deter investment in research and development for emerging companies, reducing competition and slowing the overall growth of the market. Consequently, while RNA vaccines hold immense promise for rapid, effective influenza prevention, intellectual property restrictions create a high barrier to entry, concentrating technological capabilities and market control among a few dominant players, and potentially delaying broader adoption and accessibility in lower-income regions.

Opportunity – Universal Flu Vaccine Development Opportunity

One of the most promising opportunities in the Flu RNA Vaccines Market is the development of a universal influenza vaccine. Traditional flu vaccines are strain-specific, requiring annual updates based on predictive models of circulating influenza strains. This approach often leads to mismatches, reducing vaccine efficacy. RNA vaccine technology, however, provides the flexibility to target multiple viral antigens simultaneously, allowing researchers to design vaccines that could protect against a broad spectrum of influenza strains, including seasonal, pandemic, and emerging variants. The use of mRNA platforms enables rapid modification of vaccine sequences, allowing a quick response to new or mutated strains without starting from scratch. Additionally, RNA vaccines can induce both humoral and cellular immune responses, offering stronger and longer-lasting protection compared to conventional vaccines.

A universal flu vaccine would reduce the need for yearly vaccination campaigns, lower public health costs, and enhance global pandemic preparedness. With increasing government support, private sector investment, and advanced clinical research, this approach represents a transformative opportunity to revolutionize influenza prevention and significantly reduce flu-related morbidity and mortality worldwide.

Category-wise Analysis

By Vaccine Type, the Non?Replicating Segment is leading in the Market

Non-replicating mRNA vaccines currently hold the largest share in the Flu RNA Vaccines Market due to their proven safety, scalability, and clinical advancement. Unlike self-replicating mRNA or dendritic cell-based vaccines, non-replicating mRNA platforms deliver the genetic sequence of the influenza antigen directly into host cells without further amplification, simplifying development and reducing the risk of adverse effects. Their success in the COVID-19 pandemic has validated this technology, demonstrating high efficacy and manageable side effects, which has accelerated regulatory approvals and increased investor confidence. Additionally, manufacturing non-replicating mRNA vaccines is more straightforward, allowing for rapid scale-up and broad distribution, essential for global immunization campaigns. In contrast, self-replicating mRNA vaccines, while potentially more immunogenic, are complex to produce and still under early clinical evaluation, limiting their current market penetration. Dendritic cell mRNA vaccines require personalized processing and are labor-intensive, restricting large-scale use. “Other” RNA platforms, including experimental formulations, remain niche with minimal adoption. Consequently, the combination of established clinical success, ease of production, and global acceptance positions non-replicating mRNA vaccines as the dominant segment in the flu RNA vaccine market today.

By Application, the Hospitals Segment Leads the Market

Hospitals currently account for the highest share in the Flu RNA Vaccines Market due to their advanced infrastructure and critical role in vaccine delivery. RNA-based flu vaccines require strict cold-chain management, specialized storage conditions, and trained medical staff for safe administration, all of which are readily available in hospital settings. Hospitals also serve as key centers for clinical trials, early vaccine rollouts, and post-vaccination monitoring, especially for newer technologies such as mRNA vaccines. In addition, government immunization programs and pandemic preparedness initiatives often rely on hospitals as primary distribution and administration hubs, further strengthening their market dominance. Hospitals manage large patient volumes, including high-risk groups such as the elderly, immunocompromised, and those with chronic conditions, who are prioritized for advanced influenza vaccination. Compared to clinics, vaccination centers, and pharmacies, hospitals offer greater trust, regulatory compliance, and emergency care support, making them the preferred choice for administering novel flu RNA vaccines and sustaining the largest share of applications.

Region-wise Insights

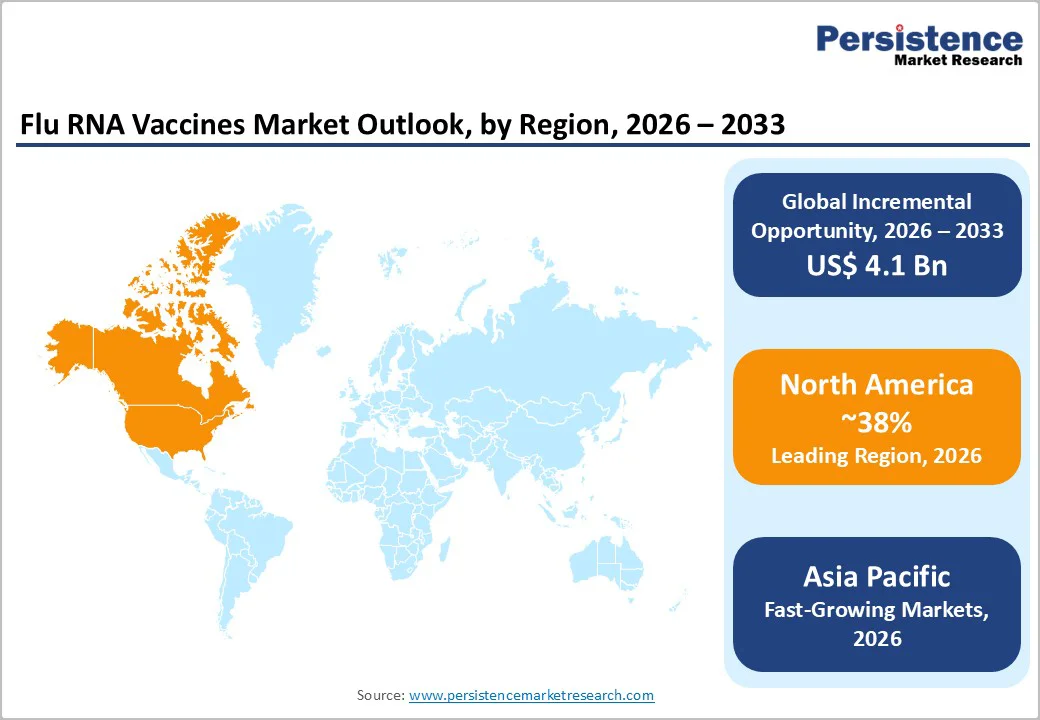

North America Flu RNA Vaccines Trends

North America leads the Flu RNA Vaccines Market due to its strong biotechnology ecosystem, early adoption of advanced vaccine technologies, and robust public health infrastructure. The region benefits from the presence of major RNA vaccine developers, active clinical trial networks, and well-established regulatory pathways that accelerate innovation and approval processes. Increased government funding for pandemic preparedness and influenza prevention has significantly supported RNA-based vaccine research and manufacturing capacity. Seasonal influenza burden, combined with high awareness of vaccination benefits, drives strong demand across hospitals and vaccination programs. Additionally, collaborations among biotech firms, pharmaceutical companies, and research institutions are driving rapid advances in multivalent and next-generation flu RNA vaccines. The region is also witnessing growing investment in cold-chain logistics and mRNA manufacturing facilities, ensuring scalability and rapid deployment. These trends position North America at the forefront of flu RNA vaccine development, commercialization readiness, and long-term market leadership.

Asia Pacific Flu RNA Vaccines Market Trends

Asia Pacific is emerging as a high-growth region in the Flu RNA Vaccines Market, driven by expanding healthcare infrastructure, rising influenza awareness, and increasing government focus on disease prevention. Countries such as China, India, Japan, and South Korea are investing heavily in biotechnology research, vaccine manufacturing, and domestic self-reliance, creating favorable conditions for the adoption of RNA vaccines. Growing population size, high influenza incidence, and rapid urbanization are increasing the demand for effective and scalable vaccination solutions. The region is also witnessing a surge in public–private partnerships, technology transfer agreements, and collaborations with global pharmaceutical companies to accelerate RNA vaccine development. Improvements in regulatory frameworks and faster clinical trial approvals are further supporting market growth. Additionally, expanding cold-chain logistics, increasing healthcare spending, and government-led immunization programs are enhancing accessibility. These factors collectively position the Asia Pacific as a promising emerging market for flu RNA vaccines with strong long-term growth potential.

Market Competitive Landscape

The Flu RNA Vaccines Market features a dynamic and evolving competitive landscape shaped by rapid technological innovation and ongoing clinical advancements. Market participants are primarily focused on developing safe, effective, and scalable RNA-based influenza vaccines, with strong emphasis on improving immune response, stability, and multivalent capabilities. Competition is driven by progress in clinical trials, intellectual property strength, manufacturing capacity, and regulatory readiness. Strategic collaborations, licensing agreements, and research partnerships are commonly used to accelerate development and reduce time to market. Players are also investing heavily in advanced delivery systems, cold-chain optimization, and next-generation RNA platforms.

Key Industry Developments:

- In November 2025, A clinical trial funded by Pfizer tested a new influenza vaccine based on messenger RNA (mRNA). The phase 3 trial included more than 18,000 participants aged 18 to 64, with half receiving the new vaccine candidate and the other half receiving a conventional influenza vaccine.

- In November 2025, Pfizer’s mRNA flu vaccine outperformed the standard flu shot in a Phase 3 clinical trial, according to results that were published in the New England Journal of Medicine. The vaccine used the same messenger RNA technology as Pfizer’s COVID-19 vaccine, demonstrating the potential of this platform for influenza

Companies Covered in Global Flu RNA Vaccines Market

- Moderna, Inc.

- Pfizer Inc.

- BioNTech SE

- Sanofi S.A.

- GlaxoSmithKline plc (GSK)

- CureVac N.V.

- Novavax, Inc.

- CSL Limited / Seqirus

- Arcturus Therapeutics

- Sinovac Biotech Ltd.

- Others