- Biotechnology

- Red Biotechnology Market

Red Biotechnology Market Size, Share, and Growth Forecast, 2025 - 2032

Red Biotechnology Market By Product Type (Monoclonal Antibodies, Others), Therapeutic Area (Oncology, Others), End-user (Pharmaceutical & Biotechnology Companies, Others), and Regional Analysis for 2025 - 2032

Red Biotechnology Market Share and Trends Analysis

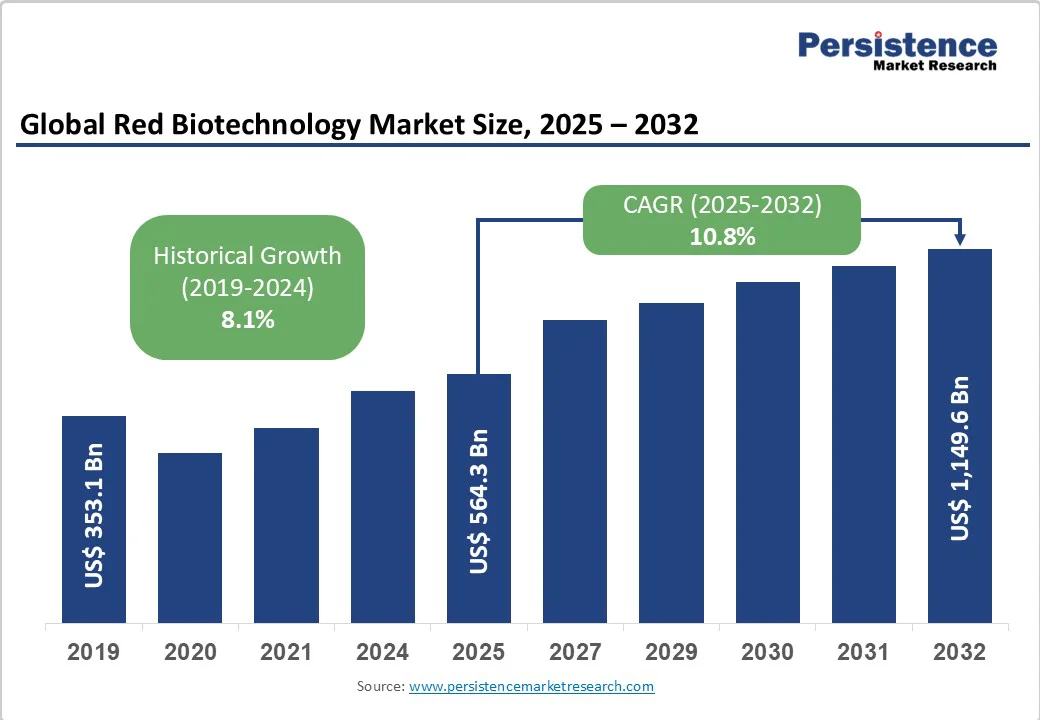

The global red biotechnology market size is likely to be valued at US$564.3 billion in 2025. It is estimated to reach US$1,149.6 billion by 2032, growing at a CAGR of 10.8% during the forecast period from 2025 to 2032, driven by the accelerating adoption of gene and cell therapies, rapid biopharmaceutical innovation, and favorable regulatory reform.

The market outlook is also driven by strong investments in advanced therapeutics, the expansion of mRNA and CRISPR technologies, and rising demand for precision medicine, supported by active R&D pipelines, government incentives, and increasing prevalence of chronic and rare diseases.

Key Industry Highlights

- Leading Product Types: Monoclonal antibodies are projected to account for about 49.6% of market revenue in 2025, driven by their widespread therapeutic use, extensive regulatory approvals, and strong patent portfolios held by leading market players.

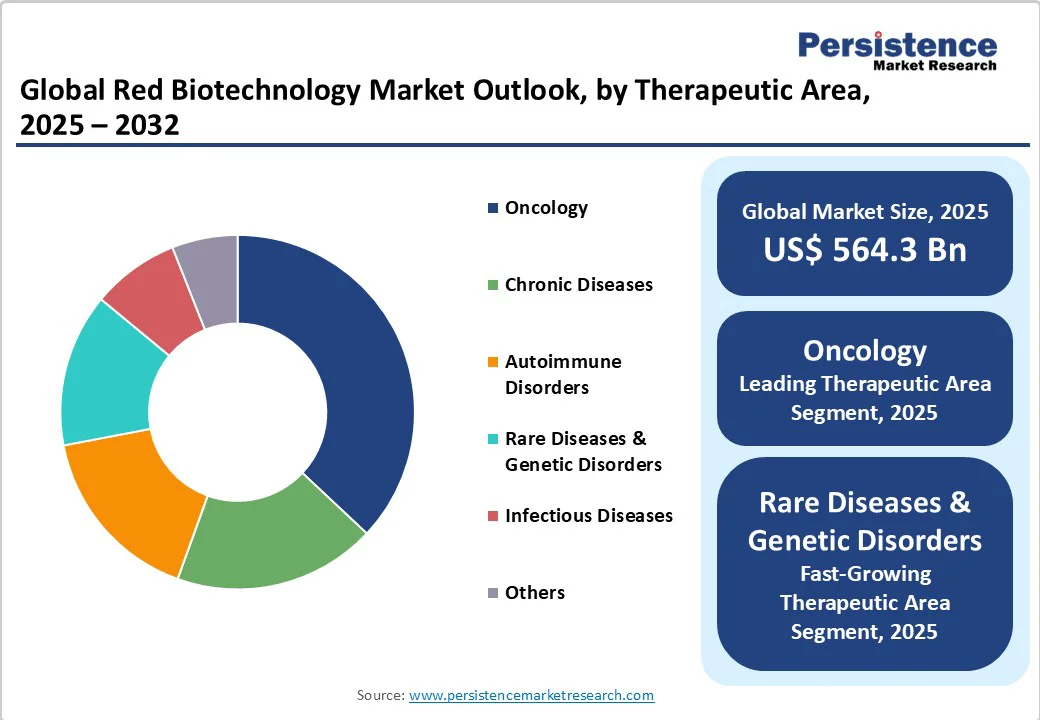

- Leading & Fastest-growing Therapeutic Areas: Oncology is set to lead with a projected 37% market share in 2025, underpinned by sustained pharmaceutical R&D expenditure.

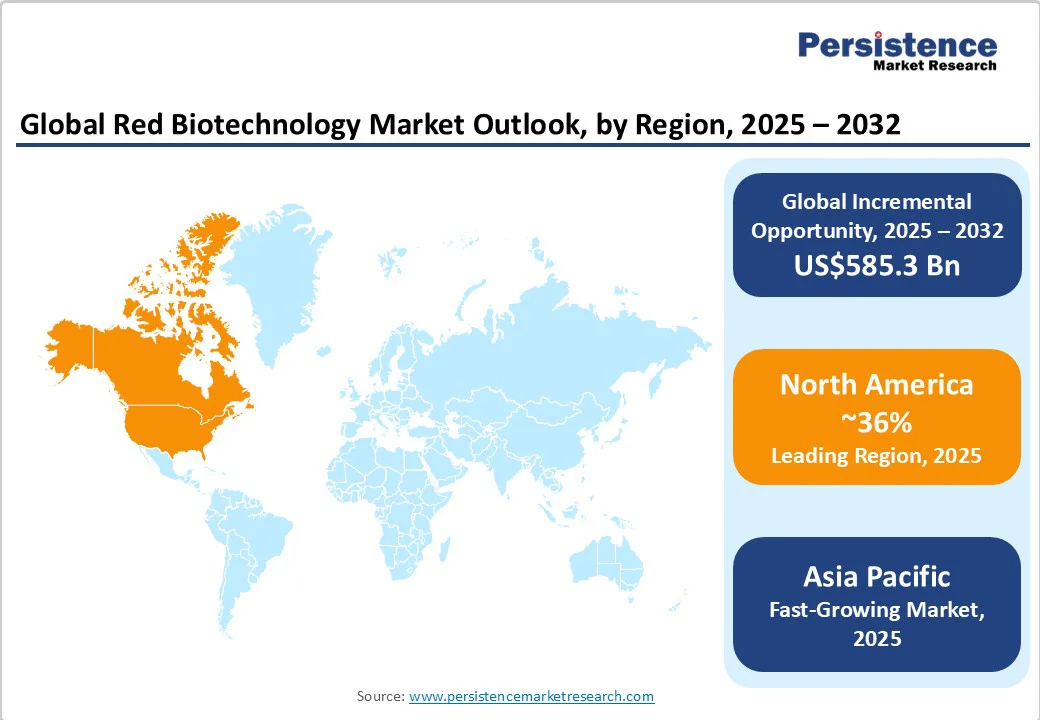

- Dominant Region & Fastest-growing Regional Market: North America is anticipated to dominate with around 36% market share in 2025, while Asia Pacific will outpace growth at a 16% CAGR between 2025 and 2032.

- Dominant & Fastest-growing End-users: Pharmaceutical and biotechnology companies will capture the largest end-user share, at approximately 46% in 2025, whereas academic and research institutes will report the fastest CAGR during the forecast period, 2025 -2032.

- October 2025: Ellis Bio Inc., a genomics biotech company spun out of the University of Chicago, announced the development of Ultra-Mild Bisulfite Sequencing (UMBS), a new method that enables highly accurate DNA methylation detection with minimal DNA damage.

| Key Insights | Details |

|---|---|

| Red Biotechnology Market Size (2025E) | US$564.3 Bn |

| Market Value Forecast (2032F) | US$1,149.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 10.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Promising Advancements in Cell and Gene Therapies

Rapid progress in personalized cell and gene therapies is creating a transformative impact on the global market, as stakeholders leverage advances in genomics and biomarker discovery to address unmet clinical needs.

By 2024, the U.S. Food and Drug Administration had approved over 30 cell and gene therapy products, with more than 2,000 candidates under investigation worldwide, signaling a robust innovation pipeline. A distinctive driver is the emergence of bespoke ex vivo gene editing solutions, particularly CRISPR-modified autologous cell therapies targeting rare hematological and immunological disorders.

For example, the successful regulatory approval of CRISPR-based sickle cell disease therapies in both the U.S. (December 2023) and the European Union (EU) (January 2024) has catalyzed unprecedented investment into platform technologies enabling patient-specific product development.

This shift is evidenced by the growing number of 'N-of-1' trials, currently numbering over 80 across North America and Europe, which capitalize on rapid manufacturing, modular bioprocessing, and digital diagnostics to generate custom therapies in a matter of weeks.

Biomanufacturing Capacity Limitations and Cost Constraints

The market growth faces persistent constraints from limited global biomanufacturing capacity and rising per-therapy production costs, impeding scalability and profitability. The unprecedented demand surges during the COVID-19 pandemic exposed critical bottlenecks in single-use bioprocessing equipment, viral vector production, and GMP-certified workforce availability, with some contract manufacturing organizations (CMOs) reporting asset utilization rates above 95% in 2023.

As CMO and CRO outsourcing grows, market participants are experiencing upward cost pressures for raw materials, logistics, and compliance audits, as reported by the International Society for Pharmaceutical Engineering (ISPE).

This dynamic is particularly acute for small & medium enterprises (SMEs) and emerging-market producers who face the risk of project delays, quality control (QC)/quality analysis (QA) backlog, and regulatory penalties due to supply interruptions.

Market players must prioritize investment in modular, continuous bioprocessing and dual-sourcing strategies to insulate mission-critical operations from future shocks, while advocating for harmonized GMP frameworks to ensure flexibility and cost competitiveness.

AI-powered Drug Discovery and Development

Artificial intelligence (AI) is rapidly reshaping drug discovery and development paradigms in the red biotechnology sector, offering a unique opportunity to achieve significant time-to-market and cost advantages. According to industry studies, the application of AI-enabled modeling, predictive analytics, and bioinformatics could reduce early drug discovery timelines by 50-70% and cut preclinical R&D expenses by up to US$3 Billion annually across the healthcare industry.

Partnerships between biopharma leaders and AI startups have demonstrated measurable progress in generating novel monoclonal antibodies and gene-editing candidates.

The U.S. National Institutes of Health (NIH) launched the Bridge2AI initiative, with US$130 Million having been committed till 2026, to integrate machine learning (ML) with real-world omics data, boosting translational research outcomes and regulatory interoperability. In this backdrop, the most lucrative opportunities will be realized by companies that merge advanced analytics with high-throughput genomic sequencing to pursue rare disease, oncology, and regenerative medicine verticals.

Category-wise Analysis

Product Type Insights

Monoclonal antibodies are expected to command the largest share of the market, estimated to contribute approximately 49.6% of the global revenue in 2025. This leadership derives from entrenched therapeutic adoption, a broad spectrum of regulatory approvals, and deep patent portfolios among market incumbents.

As of 2025, over 200 monoclonal antibody products have been approved worldwide, serving indications ranging from oncology and autoimmune disorders to infectious diseases. This segment's maturity ensures resilient cash flows for established biopharmaceutical players and provides a foundational revenue base for the entire sector.

The gene therapy product category is set to emerge as the fastest-growing segment, forecast to expand at a CAGR of about 24% between 2025 and 2032. Factors fueling this acceleration include breakthrough regulatory approvals in the U.S., the EU, & advanced Asian markets, dramatic reductions in gene sequencing and synthesis costs, and the proliferation of dedicated gene therapy contract manufacturing capabilities. Venture capital investment in cell and gene therapy reached US$9.8 Billion in 2023, and there are over 2,000 clinical pipeline candidates.

Therapeutic Area Insights

Oncology is slated to represent the dominant therapeutic application for red biotechnology, likely to account for approximately 37% of the market revenue in 2025. Market leadership in oncology is underpinned by sustained pharmaceutical R&D expenditure, which stood at nearly US$69 Billion globally in 2023, the prevalence of combination biologic regimens, and the launch of targeted immunotherapies, including next-generation antibody-drug conjugates and immune checkpoint inhibitors.

Strong incidence trends, with over 1.75 million new cancer diagnoses annually in the U.S. alone and nearly 10 million globally in 2022, as per the International Agency for Cancer Research (IARC), further amplify demand for innovative red biotechnology solutions in this therapeutic area.

Rare diseases and genetic disorders, on the other hand, are likely to be the fastest-growing therapeutic area from 2025 to 2032. Policy incentives such as orphan drug exclusivity, rising genetic diagnostic rates, and premium reimbursement models have catalyzed the rapid evolution of gene therapy pipelines targeting rare conditions.

Over 300 gene or cell therapies focused on rare diseases are in late-stage development, and the global addressable rare disease population is projected to exceed 300 million by 2030, emphasizing both the commercial and social imperatives for focused investment in this segment.

End-user Insights

Pharmaceutical and biotechnology companies are anticipated to remain the primary end-user segment in 2025, commanding an estimated 45.7% of global consumption by market value. Strategic dominance is supported by high-volume bioproduction, advanced pipeline management, and sustained regulatory engagement, particularly in North America and Western Europe.

These companies often benefit from robust vertical integration, enabling rapid market adaptation and supply chain resilience in response to emerging therapeutics and global health threats.

Academic and research institutes, however, are projected as the fastest-growing end-user segment, expanding at an estimated CAGR through 2032. This trend is being propelled by collaborative research initiatives, expanding translational infrastructure, and national-level funding for public-private biomedical innovation.

The proliferation of university hospital biobanks, high-throughput omics platforms, and institutional partnerships with private sector leaders signals a transition toward shared R&D risk and accelerated commercialization cycles for early-stage red biotechnology breakthroughs.

Regional Insights

North America Red Biotechnology Market Trends

North America is poised to retain its leadership position, accounting for approximately 36% of the red biotechnology market share in 2025. The United States spearheads regional dominance, propelled by a mature regulatory framework set in place by the Food and Drug Administration (FDA) and the Centers for Medicare & Medicaid Services (CMS), substantial biopharmaceutical R&D investments, and a highly developed clinical trial ecosystem.

The U.S. commanded nearly US$200 Billion in red biotechnology revenues in 2024, with over 900 active clinical trials at the close of 2023. Near-term growth is sustained by landmark regulatory events in the form of accelerated gene therapy approvals, strong protection of intellectual property (IP), and interoperable digital health infrastructure.

Over the next decade, the North America market is likely to be driven by the increasing commercialization of rare disease therapies, payer-driven value-based pricing, and robust biomanufacturing expansion, notably in Boston, San Diego, and Toronto.

Europe Red Biotechnology Market Trends

The Europe red biotechnology market is predicted to represent around 27% of global revenue in 2025, supported by strong performance in Germany, the U.K., France, and Spain. The presence of high-caliber research clusters, such as BioRN and MedCity, collaborative initiatives such as the Innovative Medicines Initiative, and the stringent yet harmonized European Medicines Agency (EMA) regulatory framework provide a conducive landscape for innovation and cross-border investment.

Germany alone accounted for over US$34 Billion in red biotech output in 2024, while the U.K. reported more than 70 active licensed cell and gene therapy trials as of mid-2024. Europe is forecast to achieve a robust 2025 - 2032 CAGR, with future market acceleration tied to EU-level funding under long-term programs such as Horizon Europe, agile orphan designation reviews, and digital transformation across manufacturing and healthcare delivery.

Asia Pacific Red Biotechnology Market Trends

Asia Pacific is expected to be the fastest-growing regional market. China, Japan, and India anchor demand, supported by high-volume biomanufacturing, progressive policy frameworks, and rapid clinical adoption of advanced biologics. China’s red biotechnology sector grew to over US$55 Billion in 2024, benefiting from government funding initiatives that have led to the establishment of more than 300 biopark projects and streamlined regulatory processes via the National Medical Products Administration (NMPA).

In Japan, the emphasis of the government and private players is on regenerative medicine, while India has made pivotal strides as a cost-competitive manufacturing hub over the last few decades. Strikingly, ASEAN countries are scaling regional GMP production and clinical trial capacity, further lowering go-to-market timelines. Investment in R&D zones, talent pools, and cross-border M&A is shaping a dynamic, innovation-driven competitive landscape that will catalyze sustained regional market performance.

Competitive Landscape

The global red biotechnology market structure remains moderately consolidated. The top five players, F. Hoffmann-La Roche AG, Amgen Inc., Pfizer Inc., Novartis AG, and Johnson & Johnson Services Inc., currently collectively accounting for approximately 32% of global revenues.

A further 25-35% share is distributed among established leaders such as Gilead Sciences, Bristol-Myers Squibb, and Eli Lilly and Company, while rapid growth in gene therapy, mRNA, and cell-based segments is fostering the entry and expansion of specialized and mid-sized biotechnology innovators.

Competitive positioning is driven by product pipeline depth, manufacturing scalability, global regulatory reach, and the ability to form strategic partnerships for accelerated development. The sector’s moderate level of concentration continues to foster aggressive cross-licensing, vertical integration, and hybridization of traditional and emerging modalities, ensuring both innovation and portfolio resilience throughout the forecast period.

Key Industry Developments

- In September 2025, U.K.-based NRG Therapeutics raised US$67 Million to advance its lead drug, NRG-5051, targeting mitochondrial protein complexes implicated in Parkinson’s and ALS, with clinical trials slated for early 2026 and strong preclinical evidence supporting neuroprotective potential.

- In September 2025, the FDA launched the Rare Disease Evidence Principles (RDEP) program to expedite therapies for ultra-rare genetic diseases, allowing approvals based on single-arm trials with supportive evidence, enhancing regulatory flexibility, and accelerating patient access to life-saving treatments.

- In July 2025, Sanofi acquired U.K.-based biotech Vicebio Ltd. for US$1.15 Billion, gaining access to its RSV-hMPV combination vaccine candidate and Molecular Clamp technology, which enhances immune response and production efficiency, strengthening Sanofi’s next-gen, non-mRNA vaccine portfolio for older adults.

Companies Covered in Red Biotechnology Market

- F. Hoffmann-La Roche AG

- Amgen Inc.

- Pfizer Inc.

- Novartis AG

- Johnson & Johnson Services Inc.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Gilead Sciences, Inc.

- Merck & Co., Inc.

- Sanofi SA

- Biogen Inc.

- Regeneron Pharmaceuticals Inc.

- Vertex Pharmaceuticals Incorporated

- Bayer AG

- Takeda Pharmaceutical Company Limited

Frequently Asked Questions

The red biotechnology market is projected to reach US$564.3 Billion in 2025.

Robust R&D pipelines of biopharmaceutical products, government incentives for novel therapies, and the growing prevalence of chronic and rare diseases globally are driving the red biotechnology market.

The red biotechnology market is poised to witness a CAGR of 10.8% from 2025 to 2032.

Sustained investments in advanced therapeutics, the scale-up of innovative production technologies such as mRNA platforms and CRISPR gene editing, and rising demand for precision medicine across both developed and developing economies are key market opportunities.

F. Hoffmann-La Roche AG, Amgen Inc., and Pfizer Inc. are some of the key players.