- Retail

- Fast Food & Quick Service Restaurant Market

Fast Food & Quick Service Restaurant Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Fast Food & Quick Service Restaurant Market is segmented by Model (Independent, Branded/Franchise), by Cuisine (Italian, Chinese, Indian, Japanese, Korean, Mexican, and Others), by Location (Standalone, Retail, Leisure, Hotels, and Others), and by Regional Analysis, 2026 - 2033

Fast Food & Quick Service Restaurant Market Share and Trends Analysis

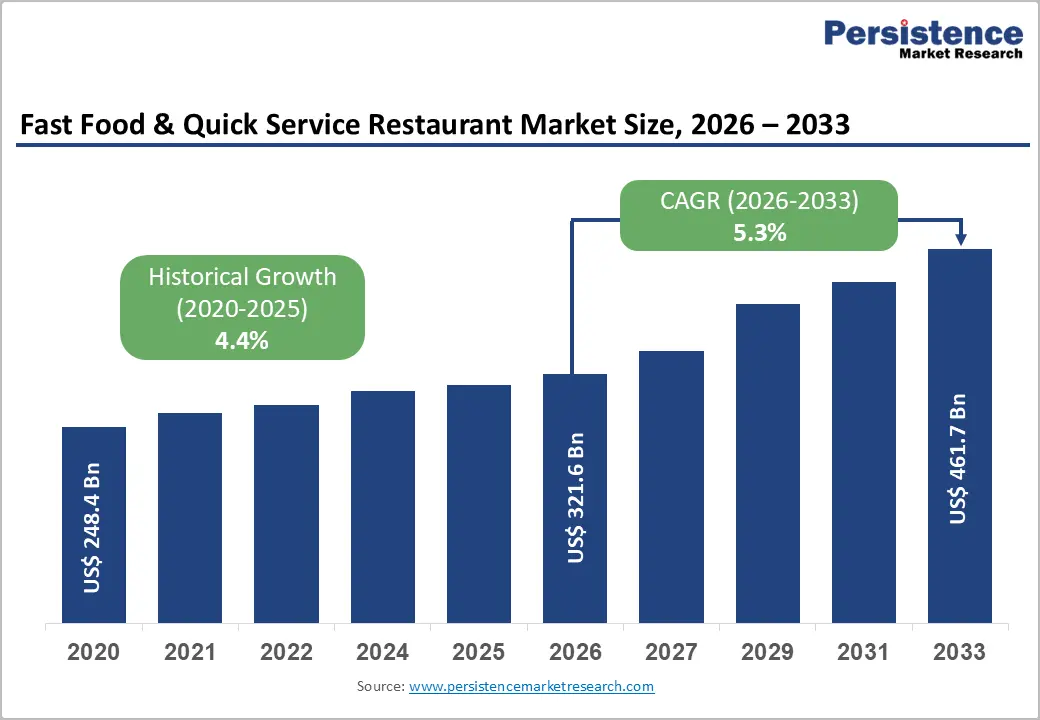

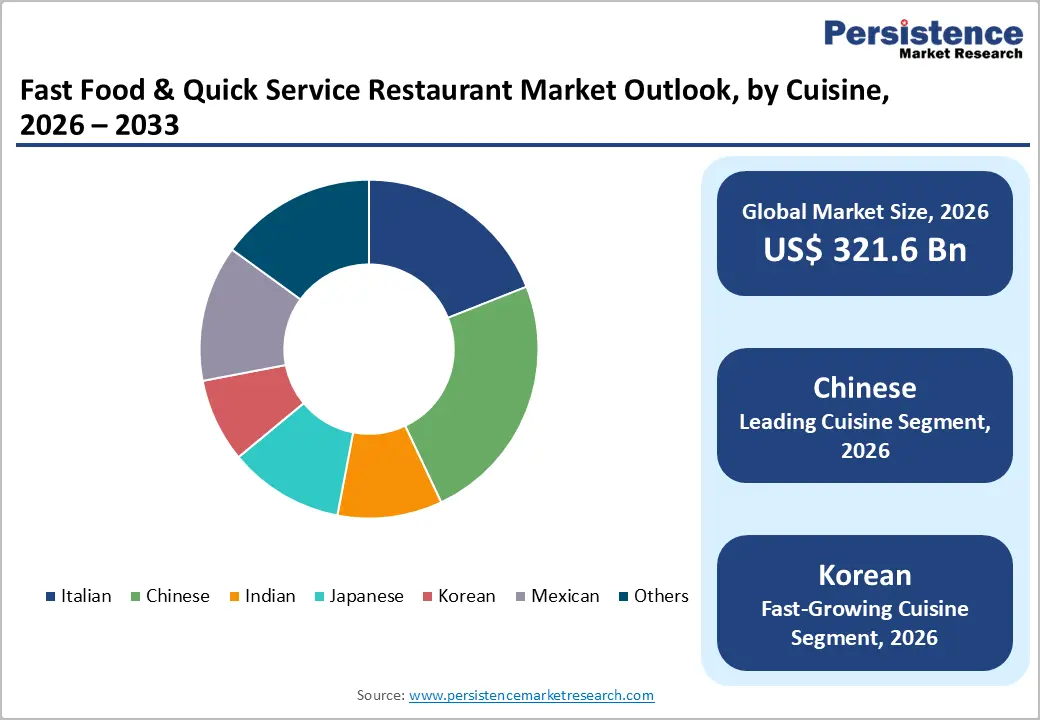

The global fast food & quick service restaurant market size is expected to be valued at US$ 321.6 billion in 2026 and projected to reach US$ 461.7 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033.

The market is predominantly driven by a structural shift in global eating patterns toward extreme convenience and the rapid digitization of food service ecosystems. Rising urban workforce participation, particularly in dual-income households, has transformed ready-to-eat meals from a discretionary treat into a daily necessity. Furthermore, the integration of high-speed delivery aggregators and the proliferation of cloud kitchens have enabled brands to scale operations without the overhead of massive dine-in infrastructure, while the entry of international chains into tier 2 and tier 3 cities in emerging economies continues to expand the total addressable audience.

Key Industry Highlights

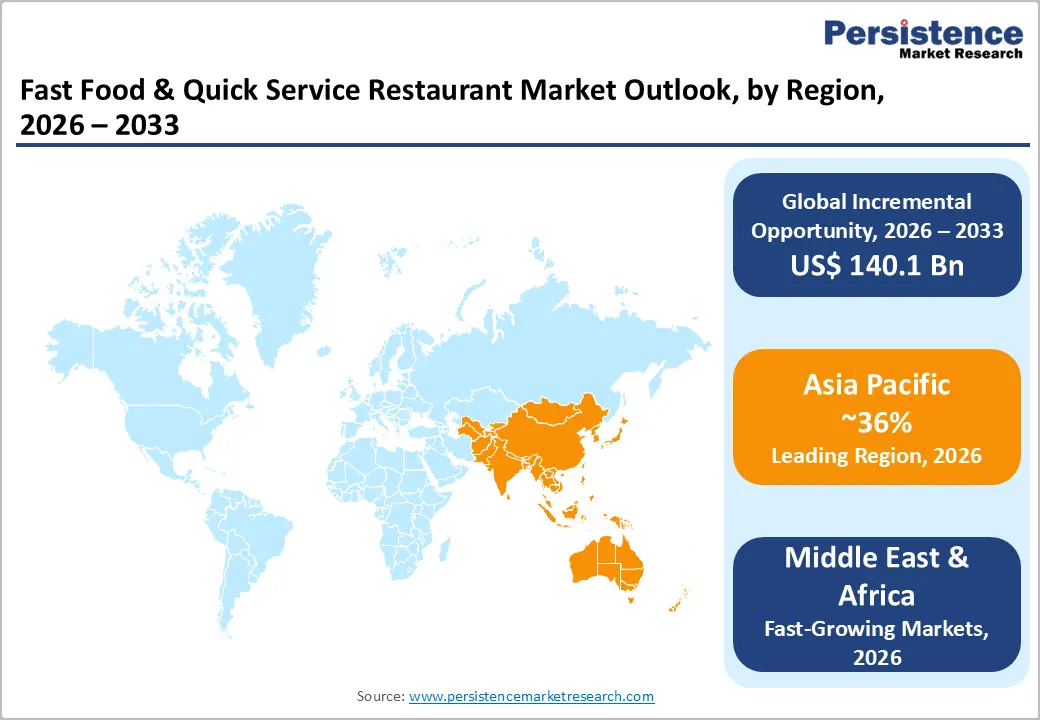

- Leading Region: Asia Pacific dominated the market in 2025 with a 36% share, driven by rapid urbanization and the rising digital participation of the world's largest youth population in China and India.

- Fastest Growing Region: Middle East & Africa is the fastest growing region through 2032, fueled by massive retail infrastructure investments and a surge in consumer demand for international dining options.

- Dominant Segment: Chinese cuisine held a 22% market share in 2025, remaining a staple due to its versatility, affordability, and established presence in the global quick service sector.

- Fastest Growing Segment: Korean cuisine is the fastest growing culinary segment, benefiting from the global popularity of Korean cultural trends and a rising appetite for spicy, fusion fast-food options.

- Key Market Opportunity: The expansion into Plant Based Proteins and Health Forward menus represents a significant avenue for brands to attract health-conscious demographics and meet regulatory health standards.

| Key Insights | Details |

|---|---|

| Global Fast Food & Quick Service Restaurant Market Size (2026E) | US$ 321.6 Bn |

| Market Value Forecast (2033F) | US$ 461.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Dynamics

Driver - Rising Urbanization and Demand for On the Go Convenience

Rapid urbanization remains the core growth engine of the Fast Food & Quick Service Restaurant (QSR) market. With over 56% of the global population now residing in urban areas, according to the World Bank, dense city living has fundamentally reshaped consumption habits. As commuting times lengthen and dual-income households become standard, consumers increasingly prioritize speed, accessibility, and affordability in meal choices. QSR formats are structurally positioned to meet this demand through standardized menus, optimized operations, and high-throughput service models that reduce preparation and waiting time.

The shift toward convenience-led dining is further validated by traffic trends. The National Restaurant Association’s 2025 report indicates that 75% of restaurant traffic now comes from takeout, underscoring the dominance of off-premise consumption. Digital ordering, drive-thru expansion, and delivery integrations reinforce this momentum. For time-constrained professionals and students, QSRs provide predictable pricing and consistent quality, making them the default foodservice solution in increasingly fast-paced urban economies.

Restraints - Escalating Operational Costs and Supply Chain Volatility

A key restraint in the Fast Food & Quick Service Restaurant (QSR) market is mounting cost pressure across the value chain. Volatility in global commodity prices particularly dairy, edible oils, poultry, and other core inputs has compressed operating margins. Rising fuel and logistics expenses further intensify procurement and distribution costs, limiting pricing flexibility. At the same time, persistent labor shortages in many developed markets are driving wage inflation, increasing the structural cost base for operators already managing thin margins.

Escalating real estate rentals in high-footfall urban locations add another layer of strain, particularly for independent outlets and emerging franchise networks. As operators attempt to offset these pressures through menu price increases, demand elasticity becomes a concern in inflation-sensitive environments. Price-conscious families may reduce visit frequency or trade down to lower-cost alternatives. Collectively, these factors slow outlet expansion, constrain profitability, and elevate consolidation risk across the competitive landscape.

Opportunity - Expansion into Plant Based and Health Forward Menu Innovations

A significant growth opportunity for QSR participants lies in the diversification of menus to include plant-based proteins and health-conscious alternatives. As of 2025, the demand for vegan, gluten free, and high protein meals has reached a tipping point, particularly among Gen Z and Millennial demographics. According to Persistence Market Research , approximately 8% to 14% of fast-food offerings in mature markets like Singapore and Australia are now plant based. Brands that introduce veggie burgers, rich protein bowls, and organic ingredient salads can capture a new demographic of flexitarians who seek convenience without compromising wellness. This strategic shift not only builds brand relevance but also addresses regulatory pressures for healthier food options, providing a long-term competitive edge in a crowded market.

Category-wise Analysis

Cuisine Insights

In 2025, Chinese cuisine remained a dominant segment in the global QSR landscape, accounting for a 22% market share. Its popularity is rooted in its inherent suitability for quick preparation and high demand for rice and noodle-based bowls in both Asia Pacific and Western markets. However, Korean cuisine is identified as the fastest growing segment for the forecast period. The global cultural influence of Korean media has led to a surge in demand for Korean fried chicken, kimchi infused burgers, and spicy bibimbap bowls. International chains are increasingly introducing Korean inspired limited time offerings to entice adventurous younger diners. Other segments like Mexican and Japanese also show robust growth, supported by the rising trend of global flavor exploration and fusion menus.

Location Insights

Standalone locations remain the leading segment by volume, particularly in suburban and highway areas where drive thru facilities drive a significant portion of revenue. However, the Retail segment, encompassing food courts in malls and shopping complexes, is witnessing high footfall as shopping centers evolve into leisure hubs. The Leisure and Hotels segments are also seeing increased QSR penetration, as travelers and tourists seek familiar and quick dining options. In 2025, the rising demand for travel and tourism was identified as a key driver for QSR growth in transit locations like airports and railway stations, where speed and operational efficiency are the highest priorities for customers.

Regional Insights

Asia Pacific Fast Food & Quick Service Restaurant Market Trends and Insights

Asia Pacific leads the global Fast Food & Quick Service Restaurant (QSR) market, accounting for approximately 36% of total revenue in 2025. The region’s dominance is anchored in the scale of urbanization across China and India, which together represent more than 320 million QSR consumers. Rapid income growth, expanding middle-class populations, and dense metropolitan clusters continue to fuel demand. Asia Pacific also stands at the forefront of digital integration, with mobile ordering platforms, super apps, and influencer-led marketing campaigns significantly increasing brand engagement and repeat purchases among Gen Z and millennial consumers.

Menu innovation in the region is heavily localized. International chains such as KFC and Starbucks have adapted offerings to reflect regional preferences, introducing rice-based meals, plant-forward options, and localized flavors. Meanwhile, domestic operators in China and Southeast Asia are scaling traditional noodle and dumpling concepts within standardized QSR formats. Cloud kitchens and improving logistics networks are further accelerating expansion into rural and semi-urban markets.

Middle East & Africa Fast Food & Quick Service Restaurant Market Trends and Insights

The Middle East & Africa is projected to be the fastest-growing Fast Food & Quick Service Restaurant (QSR) region during 2026 to 2033. Expansion is driven by accelerating urbanization and a rapidly growing youth demographic in key markets such as Saudi Arabia, Nigeria, and the UAE. Rising disposable incomes and a strong social culture centered on dining out continue to stimulate demand. Government-backed tourism development and retail infrastructure investments are further strengthening the commercial ecosystem. Strong domestic brands, including Al Baik, have built loyal consumer bases, intensifying competitive momentum across the region.

Local operators such as Chicken Cottage in Nigeria are effectively challenging multinational chains through menu customization tailored to regional flavor preferences. Urban hubs like Dubai and Riyadh exhibit high adoption of online food delivery platforms, reinforcing convenience-driven consumption. Meanwhile, growing awareness of obesity concerns is creating opportunities for healthier, nutrient-focused menu innovation aligned with public health initiatives.

Competitive Landscape

The Fast Food & Quick Service Restaurant Market is a moderately consolidated landscape, with global giants such as McDonald's Corporation, Yum! Brands, and Starbucks Corporation commanding significant market shares through extensive franchise networks. These market leaders employ strategies focused on digital transformation, utilizing automated ordering and customer analytics to drive personalized service and decision making. Key differentiators in the industry include speed of service, consistency of product quality, and the ability to rapidly roll out limited time promotional campaigns across global outlets.

Emerging business model trends show a significant pivot toward cloud kitchens and hybrid delivery models to minimize overhead and maximize geographic reach. Market leaders are also investing in R&D for future proof menus that align with health trends, such as plant based proteins and reduced preservatives. While large chains benefit from economies of scale, independent players are finding success through hyper local marketing and artisanal storytelling that resonates with younger consumers seeking unique culinary experiences.

Key Developments:

- In January 2026, Starbucks Coffee Company launched a reimagined Starbucks Rewards program, enhancing personalization and value for its 35.5 million active U.S. members to deepen engagement and frequency.

- In November 2025, Restaurant Brands International Inc. announced its participation in the Barclays 11th Annual Eat, Sleep, Play, Shop Conference, signaling continued investor outreach and strategic positioning within the global QSR landscape.

- In August 2025, Cricket South Africa (CSA) renewed its multi-year partnership with KFC, strengthening brand visibility across national cricket platforms and reinforcing long-term sports marketing alignment.

Companies Covered in Fast Food & Quick Service Restaurant Market

- McDonald's Corporation

- Yum! Brands

- Starbucks Corporation

- Restaurant Brands International

- Domino's Pizza Inc.

- Chipotle Mexican Grill

- Papa John's International

- Wendy's Company

- Subway

- Others

Frequently Asked Questions

The global Fast Food & Quick Service Restaurant market is projected to be valued at US$ 321.6 Bn in 2026.

Rising Urbanization and Demand for On the Go Convenience is driving global Fast Food & Quick Service Restaurant market.

The Global Fast Food & Quick Service Restaurant market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion into Plant Based and Health Forward Menu Innovations represents a significant market opportunity for companies in the Fast Food & Quick Service Restaurant market.

Major players in the Global Fast Food & Quick Service Restaurant market include McDonald's Corporation, Yum! Brands, Starbucks Corporation, Restaurant Brands International, Domino's Pizza Inc., Chipotle Mexican Grill, and others.