- Smart Packaging

- Fast Food Reusable Packaging Market

Fast Food Reusable Packaging Market Size, Share, and Growth Forecast 2026 - 2033

Fast Food Reusable Packaging Market by Material Type (Plastic, Metal, Glass, Other), Product Type (Containers, Cups, Cutlery, Straws, Other), Application (Beverages, Food), End-user (Restaurants, Cafes, Food Trucks, Other), and Regional Analysis for 2026 - 2033

Fast Food Reusable Packaging Market Size and Trend Analysis

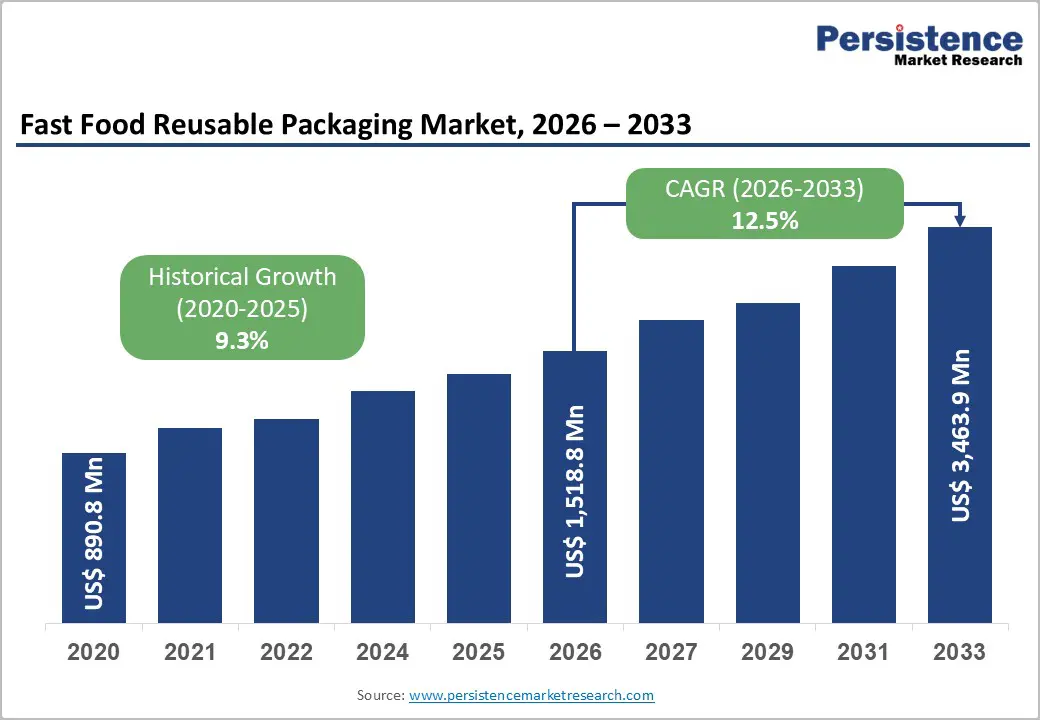

The global fast food reusable packaging market size is supposed to be valued at US$ 1,518.8 million in 2026 and is projected to reach US$ 3,463.9 million by 2033, growing at a CAGR of 12.5% between 2026 and 2033.

The market's robust expansion is primarily driven by stringent regulatory mandates targeting single-use plastics across multiple jurisdictions, as well as escalating consumer demand for environmentally responsible dining solutions. The European Union's Packaging and Packaging Waste Regulation (PPWR), which mandates that 10% of beverages be offered in reusable packaging by 2030 and 40% by 2040, alongside similar restrictions across 60 jurisdictions in North America, is compelling fast-food operators to accelerate their transition toward circular-economy models. Corporate sustainability commitments from major quick-service restaurant (QSR) chains, combined with the economic imperative of reducing the $24 billion annual expenditure on disposable packaging, are further catalyzing market growth.

Key Industry Highlights:

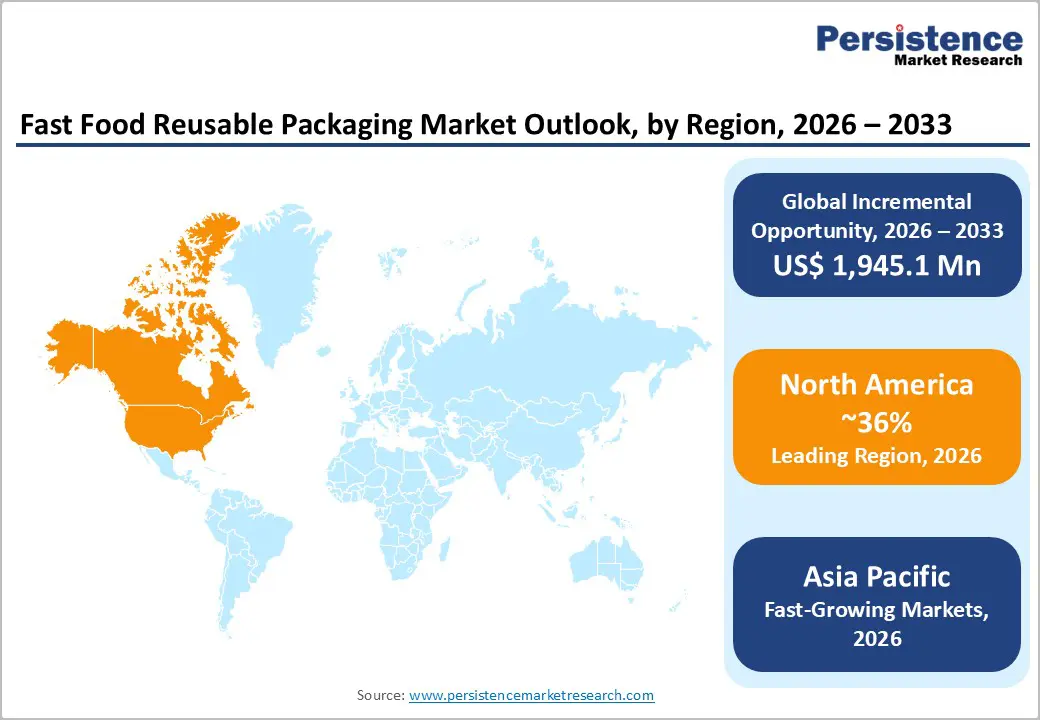

- Regional Leader: North America leads the fast-food reusable packaging market with 36% market share, driven by robust U.S. regulations and infrastructure that are driving adoption among major chains.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, fueled by urbanization in China, India, and Japan, for sustainable solutions.

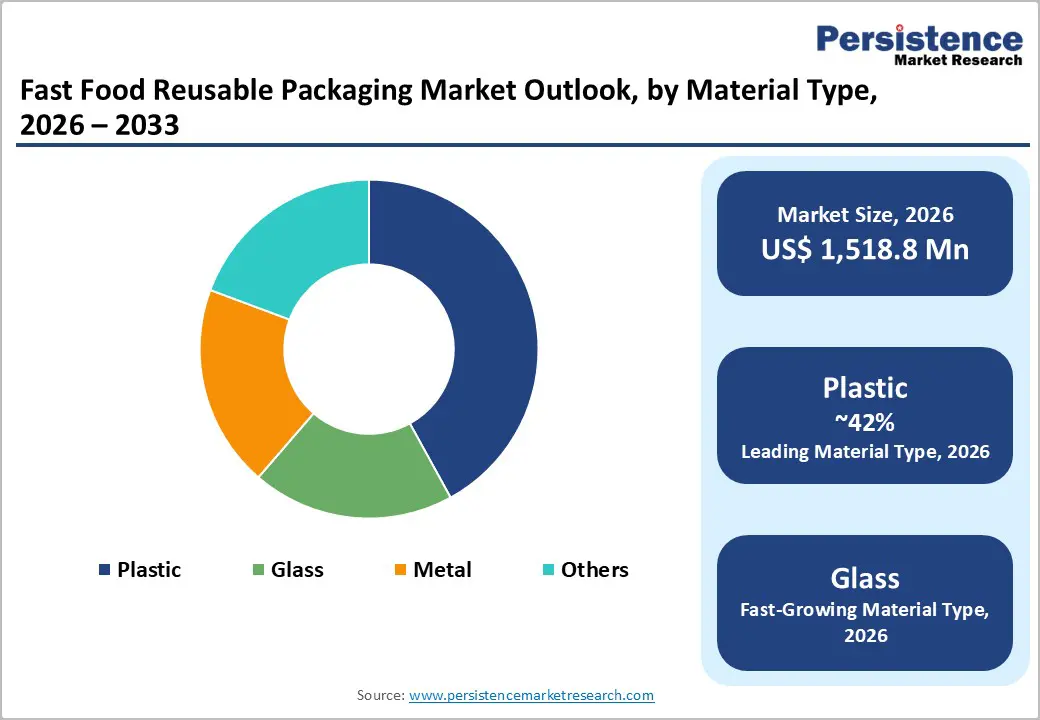

- Leading Segment: Plastic dominates Material Type with a 42% share, valued for its superior durability-to-weight ratio, cost-effectiveness, design versatility, and proven performance in 200+ use-cycle applications.

- Fastest-Growing Segment: Containers constitute the fastest-growing product segment with projected above-market growth rates, driven by explicit HORECA sector regulatory mandates requiring 10% reusable container offerings within 36 months under EU PPWR and universal applicability across diverse menu formats.

- Key Market Opportunity: Integration of smart tracking technologies using QR codes, RFID tags, and IoT sensors represents the most significant market opportunity, enabling deposit-refund mechanisms, real-time inventory optimization, predictive analytics, and blockchain-based food safety verification, addressing hygiene concerns.

| Key Insights | Details |

|---|---|

| Fast Food Reusable Packaging Market Size (2026E) | US$ 1,518.8 Mn |

| Market Value Forecast (2033F) | US$ 3,463.9 Mn |

| Projected Growth CAGR (2026 - 2033) | 12.5% |

| Historical Market Growth (2020 - 2025) | 9.3% |

Market Dynamics

Drivers - Rise in Consumer Demand for Sustainability

Growing awareness of plastic pollution has accelerated the adoption of reusable packaging solutions among fast-food chains. Surveys reveal that more than 65% of environmentally conscious consumers prefer glass or metal packaging due to its safety and recyclability. This trend aligns with the broader sustainable packaging movement, where brands strengthen customer loyalty by reducing waste.

Leading quick-service restaurant (QSR) chains such as McDonald’s and Starbucks have advanced significant initiatives through the NextGen Consortium, investing $10 million to develop reusable systems and enhance recycling infrastructure. Burger King’s pilot of returnable cups with up to 200 reuse cycles underscores the technical feasibility of durable solutions. Manufacturers, including Tetra Pak, are further driving momentum by designing renewable and recyclable packaging. Increasing consumer focus on circular economy principles positions reusable systems as strategic differentiators rather than mere compliance measures.

Stringent Government Regulations on Single-Use Plastics

The enforcement of comprehensive legislation restricting single-use plastics is a pivotal growth driver for the fast-food reusable packaging market. The European Union’s Packaging and Packaging Waste Regulation (PPWR), adopted in December 2024, mandates that operators in the HORECA (Hotel, Restaurant, Catering) sector allow customers to use their own reusable containers without additional charges and ensure that at least 10% of products are offered in reusable formats within 36 months of implementation.

Similarly, in North America, California’s SB 54, effective January 1, 2025, prohibits the use of expanded polystyrene foam containers in restaurants. Furthermore, jurisdictions such as Seattle, Washington, D.C. and approximately 60 others have enacted bans on plastic straws and utensils. These measures, taken together, eliminate reliance on single-use packaging, creating a mandatory demand for reusable alternatives.

Restraint - High Initial Investment Costs

Transitioning to reusable packaging systems requires significant upfront investment, including container procurement, tracking technologies, washing facilities, and reverse logistics infrastructure. Unlike single-use packaging with predictable per-unit costs, reusable models demand capital for IoT-enabled tracking devices, industrial-grade washing equipment compliant with food safety standards, and collection point networks. Restaurants face challenges such as uncertain demand and return patterns, which complicate inventory management and can lead to shortages during peak periods or to excess idle stock. The lack of standardized packaging formats limits economies of scale, while customer behavior changes needed for container returns add operational complexity. Additionally, maintaining hygiene across multiple use cycles necessitates validated cleaning protocols and robust quality assurance systems, further increasing costs and implementation hurdles.

Insufficient Recycling Infrastructure and Regional Regulatory Fragmentation

The success of reusable packaging systems relies heavily on robust collection, cleaning, and redistribution infrastructure, which remains underdeveloped in many regions. The National Restaurant Association has emphasized that insufficient recycling and composting facilities pose a major barrier, noting that comprehensive infrastructure must precede effective regulatory enforcement. Regulatory fragmentation further complicates compliance for multi-location operators, as requirements vary significantly across jurisdictions.

While the European Union seeks harmonization through PPWR, markets such as China face challenges due to the absence of standardized regulations despite rapid urbanization driving demand. Cultural differences also influence return rates, with preferences in countries like Japan creating adoption hurdles despite advanced technology and environmental awareness. This infrastructure gap is most pronounced in emerging economies, where limited waste management systems restrict the scalability of reusable packaging programs.

Opportunity - Advancements in Smart Tracking Technologies

The adoption of smart tracking technologies, such as QR codes, RFID tags, and IoT sensors, offers a transformative opportunity to streamline reusable packaging operations while generating actionable data insights. These systems provide real-time visibility into container location, usage patterns, and return rates, enabling dynamic inventory management and reducing losses that have historically impacted system economics. Digital platforms also support deposit-refund programs via mobile applications, incentivizing customer participation and automating transactions. Data collected from tracked containers facilitates predictive analytics for demand forecasting and inventory optimization.

Furthermore, blockchain-based verification ensures the integrity of the cleaning cycle and compliance with food safety standards, addressing key hygiene concerns. Sustainability-focused start-ups are collaborating with food service providers to create integrated solutions combining tracking, customer engagement, and logistics optimization, positioning early adopters for data-driven competitive advantage and regulatory alignment.

Expansion in Emerging Urban Markets

Asia Pacific offers significant growth potential for the fast food reusable packaging market, driven by rapid urbanization, a growing middle class, and stricter environmental regulations. China, with a 15% growth momentum, combines government initiatives to curb plastic waste with the world’s largest food service market, creating substantial demand. India is experiencing the fastest regional expansion, supported by rising food delivery penetration, café proliferation, and the adoption of reusable solutions.

Japan’s advanced technology ecosystem and sustainability-focused consumers, reinforced by the Packaging Recycling Act and EPR mandates, create a premium segment. Regulatory measures in cities like Shanghai and Seoul mandating biodegradable or compostable packaging further favor reusable alternatives. Dense urban centers enhance the efficiency of return logistics, while Australia’s 2024 regulatory overhaul on recycled content accelerates restaurant adoption of reusable programs.

Category-wise Analysis

Material Type Insights

Plastic materials account for approximately 42% of the fast food reusable packaging market, driven by their durability-to-weight ratio, cost efficiency, and design flexibility. Polypropylene (PP) and high-density polyethylene (HDPE) dominate container production due to their thermal resistance, chemical stability across diverse food types, and compatibility with industrial dishwashing processes. Industry leaders such as Amcor are advancing sustainability by incorporating 10% post-consumer recycled (PCR) plastic by 2025, supported by significant procurement of recycled materials.

Innovations like Burger King’s returnable cups, designed for up to 200 reuse cycles, highlight the potential of advanced plastic formulations for extended service life. However, regulatory pressures, such as the EU’s PFAS ban effective August 2026, pose challenges by eliminating certain grease-resistant coatings. Ongoing developments in plastic packaging continue to enhance recyclability and end-of-life processing.

Product Type Insights

Containers account for approximately 38% of the fast food reusable packaging market, serving as the core component of reusable systems due to their versatility across diverse menu items and meal formats. Their dominance reflects the widespread use of bowl and clamshell designs for entrees, sides, and combination meals, ensuring secure transport for delivery and takeaway. Innovations such as Graphic Packaging International’s insulated, double-walled fiber containers for Chick-fil-A highlight the technical sophistication required to meet operational needs, including heat retention, structural integrity, and customer convenience.

Premium glass containers complement this segment for health-focused and upscale quick-service concepts, reinforcing quality positioning. To support multiple reuse cycles, containers must maintain durability, aesthetic appeal, and resistance to staining and odor. Regulatory mandates targeting single-use containers and smart technologies like tracking chips further enhance functionality through deposit-refund systems and inventory management.

Application Insights

Food applications account for approximately 59% of the fast-food reusable packaging market, driven by the greater complexity and contamination risks associated with solid menu items compared to beverages. Food packaging must withstand temperature variations, prevent cross-contamination, resist oil and sauce penetration, and maintain structural integrity during transport, making its performance requirements more demanding than those for beverage containers. The $24 billion in annual disposables expenditure, primarily for food packaging, underscores the economic significance of this segment.

Regulatory measures have focused on food packaging, with bans on single-use items such as expanded polystyrene containers and plastic cutlery. Transitioning to reusable solutions requires addressing hygiene concerns, as direct food contact heightens sanitation issues. Innovations such as barrier coatings, compartmentalized designs, and ventilation features aim to preserve food quality, though most advances still target single-use formats.

End-user Insights

Restaurants account for approximately 46% of the fast food reusable packaging end-user market, making them the largest and most established channel for implementing reusable systems. Full-service and quick-service restaurants possess operational infrastructure such as dishwashing facilities, storage capacity, and trained staff, enabling efficient adoption. Leading chains, including McDonald’s, have pledged to source 100% of guest packaging from renewable, recycled, or certified materials by 2025, with reusable solutions forming a key strategy to achieve these goals.

The NextGen Consortium’s $10 million investment in partnerships with Starbucks and McDonald’s underscores the sector’s leadership in advancing reusable systems and supporting infrastructure. Controlled environments and historical use of reusable service ware reduce implementation barriers, while EU PPWR regulations mandate reusable options for takeaway, making compliance essential. Restaurants also leverage deposit-refund programs, incentives, and customer education to drive container returns, facilitating system viability and economies of scale.

Regional Insights

North America Fast Food Reusable Packaging Market Trends

North America leads in fast food reusable packaging innovation, driven by the United States’ proactive regulatory frameworks, strong corporate sustainability commitments, and well-established environmental advocacy. California set the precedent with AB 1162, effective January 1, 2024, banning single-use plastic bags and expanded polystyrene containers while introducing a 10-cent fee on paper bags. This model has since been adopted by approximately 60 jurisdictions, with Seattle pioneering the first major ban on plastic straws and utensils in 2008, followed by Washington D.C. and municipalities across California, Florida, and New York.

The region’s innovation ecosystem is reinforced by the NextGen Consortium, which unites leading brands such as McDonald’s and Starbucks through a $10 million investment to advance reusable systems and recycling infrastructure. With U.S. food-service businesses spending $24 billion annually on disposables, potential savings exceeding $10 billion create strong economic incentives for adoption, while industry groups actively engage policymakers to align regulatory timelines with infrastructure development.

Europe Fast Food Reusable Packaging Market Trends

Europe is at the forefront of global fast food reusable packaging regulation, driven by the European Union’s Packaging and Packaging Waste Regulation (PPWR), adopted on December 16, 2024. This framework introduces the world’s most ambitious mandatory targets, requiring final distributors to offer at least 10% of beverages in reusable packaging by January 1, 2030, rising to 40% by 2040. The regulation also mandates that HORECA operators accommodate customer-provided containers at no additional cost and that takeaway outlets provide 10% of products in reusable formats within 36 months of enforcement.

Germany, the U.K., France, and Spain exhibit varied implementation strategies, with Germany leading through deposit-refund systems. Additional measures include a PFAS ban effective August 12, 2026, and forthcoming minimization standards in Q4 2026. Municipal initiatives in cities such as Paris and Brussels further strengthen infrastructure, positioning Europe as the fastest-growing market for reusable packaging adoption.

Asia Pacific Fast Food Reusable Packaging Trends

The Asia Pacific region is projected to experience the fastest growth in the fast food reusable packaging market, driven by rapid urbanization, a rising middle class, and increasingly stringent environmental regulations. China’s initiatives to reduce plastic waste and promote eco-friendly practices, alongside mandates in cities such as Shanghai requiring biodegradable or compostable packaging in public institutions, are creating strong regulatory momentum despite the absence of uniform national standards.

Japan combines advanced technology integration with sustainability-focused consumer preferences, supported by the Packaging Recycling Act and extended producer responsibility (EPR) mandates, enabling premium reusable packaging solutions despite cultural challenges related to hygiene and convenience. India leads regional growth with expanding urbanization, food delivery penetration, and café proliferation, while Vietnam and China’s EPR mandates further align with global frameworks, reinforcing regulatory drivers comparable to Europe.

Competitive Landscape

The fast food reusable packaging market is moderately fragmented, with established packaging manufacturers expanding into reusable solutions while specialized circular economy start-ups develop integrated tracking and logistics platforms. Companies are prioritizing R&D in food-safe, durable materials, smart tracking integration, and multi-cycle designs, supported by collaborations between restaurant chains and packaging suppliers to accelerate innovation. Emerging models such as packaging-as-a-service shift capital costs from restaurants to providers, while strategic partnerships with waste management firms, tech platforms, and industry consortia address systemic infrastructure challenges.

Key Market Developments:

- March 2025: Eco-Products partnered with Ozzi to launch an integrated initiative making reusable foodservice containers more accessible to businesses, colleges, and hospitals across the United States, combining Veda brand durable containers with Ozzi's automated tracking and collection technology.

- January 2025: Huhtamaki India hosted the 2nd Edition Think Circle event in collaboration with the Embassy of Finland and Confederation of Indian Industry, launching Design for Recycling Guidance for Films and Flexible Packaging that advances circular economy practices in India.

- December 2024: Circus and Vytal forged a global partnership to pioneer sustainable packaging systems, with Circus offering reusable packaging as the default in their CA-1 robot, actively supporting United Nations sustainability goals.

Top Companies in Fast Food Reusable Packaging Market

- Amcor Pty Ltd. (Melbourne, Australia) operates as a global leader in packaging solutions with extensive capabilities across flexible and rigid formats, positioning the company to address fast food reusable packaging demand through its comprehensive material science expertise and established customer relationships with major QSR brands. The company's 2024 sustainability achievements, including 94% of flexible packaging having recycle-ready solutions and 95% of rigid packaging being recyclable, demonstrate technical competency applicable to reusable systems requiring both recyclability and durability. Amcor's progress toward 10% post-consumer recycled plastic incorporation, supported by purchasing more than 224,000 metric tons of recycled material, evidences supply chain capa;bilities for sustainable material sourcing.

- Tetra Pak (Lausanne, Switzerland) leverages its leadership in aseptic carton packaging and beverage container innovation to address fast food reusable packaging opportunities, particularly in beverage applications where the company's portion pack solutions for juice, milk, coffee, and tea provide food safety advantages. The company's commitment to designing packaging from renewable materials with recyclability features aligns with the sustainability requirements driving reusable packaging adoption.

- Huhtamaki (Espoo, Finland) demonstrates material innovation leadership through its introduction of paperboard solutions with reduced plastic coating and paperboard-based packaging replacing plastics in food applications, capabilities directly applicable to reusable container development requiring sustainable material profiles. The company's expansion of recyclable flexible packaging production and focus on sustainability performance, including increased renewable energy usage, reflects strategic prioritization of environmental credentials increasingly demanded in reusable packaging procurement decisions.

Companies Covered in Fast Food Reusable Packaging Market

- Amcor Pty Ltd.

- Sealed Air Corporation

- BASF

- WestRock Co.

- Evergreen Packaging

- Rehrig Pacific Company

- Swedbrand Groups

- IPL Plastics

- Vetropack Holdings

- Schutz Gmbh & Co.

- Tetra Pak

- Loop Industries

- Huhtamaki

- DS Smith

- Berry Global Inc.

Frequently Asked Questions

The global fast food reusable packaging market is valued at US$ 1,518.8 Mn in 2026 and is projected to reach US$ 3,463.9 Mn by 2033, growing at a CAGR of 12.5% during the forecast period.

The fast food reusable packaging market is primarily driven by stringent regulatory mandates, including the European Union's PPWR, requiring 10% reusable beverage packaging by 2030 and single-use plastic bans across 60 North American jurisdictions

Plastic materials command approximately 42% market share due to their superior durability-to-weight ratio, cost-effectiveness, and design versatility.

North America leads the market through early-mover regulatory frameworks, corporate sustainability investments, including $10 million by the NextGen Consortium, and established environmental advocacy infrastructure.

The integration of smart tracking technologies using QR codes, RFID tags, and IoT sensors represents the most significant opportunity, enabling deposit-refund mechanisms, real-time inventory optimization, and blockchain-based food safety verification.

Leading market participants include Amcor Pty Ltd., Tetra Pak, Huhtamaki, and Sealed Air Corporation, with companies pursuing strategies emphasizing material innovation, smart tracking integration, and turnkey solution offerings.