- Automotive Components & Materials

- Automotive Fasteners Market

Automotive Fasteners Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Fasteners Market by Design (Threaded, Non-Threaded), Material (Metal, Plastic), Vehicle Type (Passenger Cars (PCs), Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Two Wheelers), Characteristic (Removable, Permanent), and Regional Analysis for 2026-2033

Automotive Fasteners Market Size and Trend Analysis

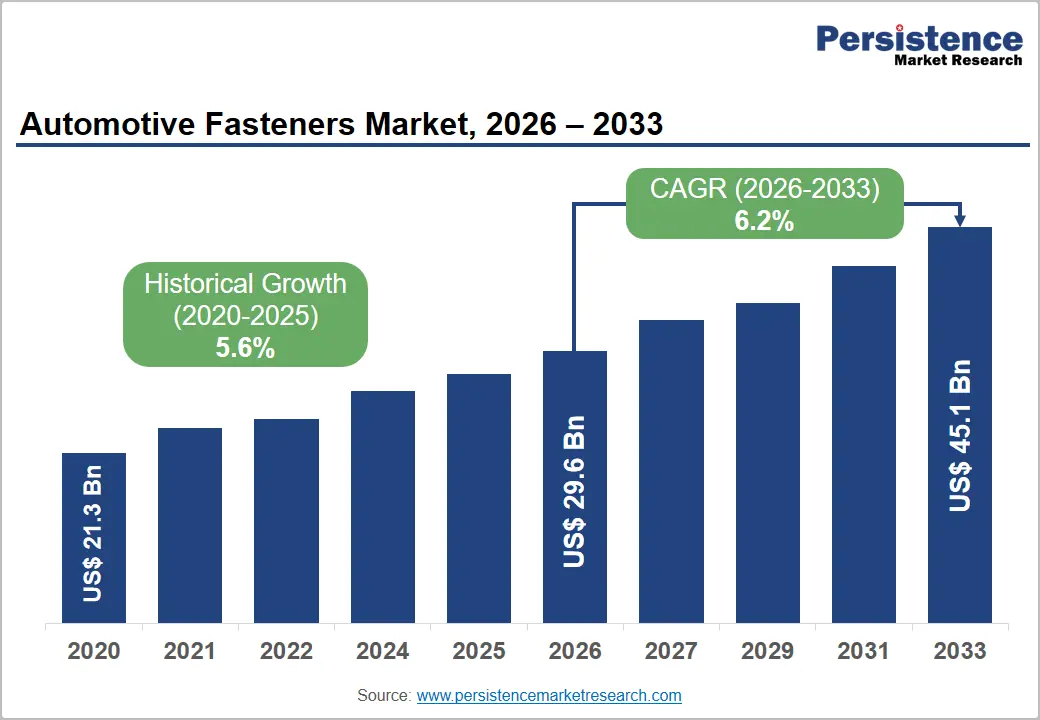

The global automotive fasteners market is valued at US$ 29.1 Bn in 2026 and is projected to reach US$ 45.1 Bn by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

The market's robust expansion is primarily driven by the global resurgence in vehicle production and the accelerating shift toward electric and lightweight vehicles. The International Organization of Motor Vehicle Manufacturers (OICA) reported global vehicle production exceeding 93 million units in 2023, recovering steadily post-pandemic and necessitating higher volumes of precision fastening components.

Key Industry Highlights:

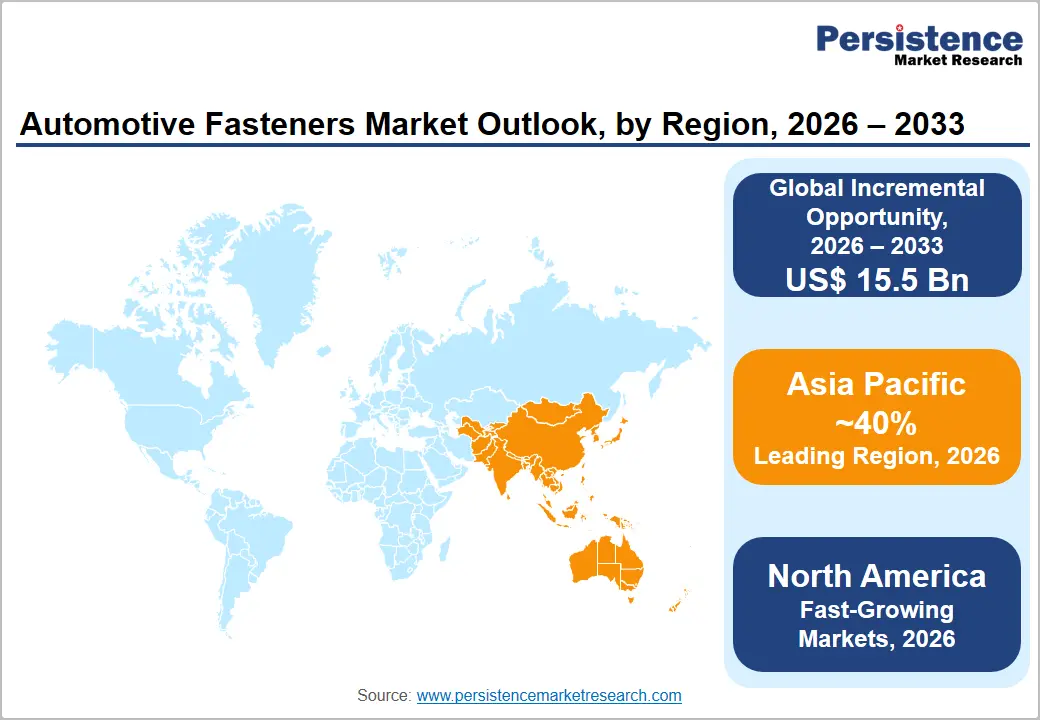

- Leading Region: Asia Pacific leads the global automotive fasteners market, driven by China's dominance in vehicle production, particularly new energy vehicles, along with robust manufacturing ecosystems in Japan, South Korea, and India. The region accounts for approximately 40% of global market revenue.

- Fastest Growing Region: North America represents one of the most mature and consolidated automotive fasteners markets globally, driven by the well-established vehicle manufacturing bases in the United States, Canada, and Mexico.

- Dominant Segment: Threaded fasteners are the dominant segment by design, holding approximately 72% market share, owing to their indispensable role across engine, chassis, and body assembly operations, and compatibility with automated torque assembly systems used across global OEM production lines.

- Fast-Growing Material Segment: Plastic fasteners represent the fastest-growing material segment, benefitting from the global lightweighting trend, rising interior trim complexity, and increasing use of non-corrosive clip-type fasteners in electric vehicle body assemblies and underbody panels.

- Key Opportunity: The development and commercialization of smart, sensor-integrated fasteners for connected and autonomous vehicle platforms offers a high-value opportunity for market participants, converging structural fastening with real-time structural health monitoring in next-generation automotive architectures.

DRO Analysis

Drivers - Rising Global Vehicle Production and Electrification of Automotive Platforms

The steady recovery and growth of global automobile manufacturing remain the foremost driver for the automotive fasteners market. According to OICA, global light vehicle production surpassed 90 million units in 2022 and is projected to continue rising in the forecast period. Each modern passenger vehicle contains approximately 3,000 to 4,000 fasteners, while commercial and electric vehicles require even higher counts due to complex powertrain architectures and battery enclosures.

The global transition toward battery electric vehicles (BEVs) is particularly impactful; BEV platforms integrate large structural battery packs requiring hundreds of precision-engineered bolts and screws with strict torque specifications. The International Energy Agency (IEA) reported that global EV sales surpassed 14 million units in 2023, a trend that continues to elevate demand for specialized automotive fasteners designed for thermal and electrical insulation performance.

Stringent Lightweighting Regulations and Multi-Material Vehicle Design Trends

Global emissions standards, including the Euro 7 framework in Europe and the updated CAFE (Corporate Average Fuel Economy) standards in the United States, are compelling automakers to reduce vehicle curb weight. This has led to increasing adoption of mixed-material designs using aluminum, magnesium, carbon fibre reinforced polymers, and advanced high-strength steels.

Multi-material assemblies require purpose-designed fasteners capable of joining dissimilar materials without inducing galvanic corrosion or compromising joint integrity. According to the European Aluminium Association, aluminum content per vehicle in Europe is projected to grow to 196 kg by 2025, up from 152 kg in 2016. This shift directly expands the addressable market for flow-drill screws, self-piercing rivets, and blind fasteners that accommodate aluminum-intensive body structures.

Restraints - Volatility in Raw Material Prices and Supply Chain Disruptions

Steel and aluminum constitute the primary raw materials for automotive fasteners, and price volatility in these commodities poses a significant challenge for manufacturers. The World Steel Association reported that global hot-rolled coil steel prices witnessed fluctuations exceeding 40% between 2021 and 2023 due to geopolitical conflicts, energy cost surges, and logistical bottlenecks.

Fastener producers operating on thin margins find it increasingly difficult to absorb such cost increases without passing them on to OEMs, thereby eroding price competitiveness. Additionally, disruptions in global shipping routes have led to extended lead times and inventory shortages, making it harder for tier-1 and tier-2 suppliers to maintain just-in-time delivery schedules, a cornerstone of automotive manufacturing efficiency.

Growing Adoption of Adhesive Bonding and Structural Joining Technologies

A notable challenge to traditional fastener demand comes from the growing substitution of mechanical fastening with structural adhesives and laser welding in automotive body assemblies. Leading automakers such as BMW, Volkswagen, and Tesla have progressively integrated adhesive bonding and friction stirred welding in body-in-white applications, reducing the number of fastener installation points per assembly.

According to the Fraunhofer Institute for Manufacturing Technology and Advanced Materials (IFAM), structural adhesives in automotive use have grown at double-digit rates, with direct implications for bolted joint utilization in certain sub-assemblies, limiting volumetric fastener demand growth in premium and EV segments.

Market Opportunities - Expansion of EV and Hybrid Vehicle Manufacturing Ecosystems in Emerging Markets

The rapid scaling of electric and hybrid vehicle manufacturing across China, India, and Southeast Asia presents a transformative opportunity for automotive fastener suppliers. China alone accounted for over 60% of global EV production in 2023, according to the China Association of Automobile Manufacturers (CAAM).

EV platforms, particularly those featuring large-format structural battery packs and skateboard architectures, require significantly more fasteners per unit compared to internal combustion engine (ICE) vehicles, owing to the need for secure, vibration-resistant enclosures.

Growing Demand for Smart and Sensor-Integrated Fasteners in Connected Vehicles

The emergence of intelligent or smart fasteners, embedding torque sensors, strain gauges, and RFID chips within fastening elements, opens a high-value product category for market participants. As modern vehicles incorporate an increasing density of electronics and structural monitoring systems, fasteners that can simultaneously secure components and transmit real-time structural health data represent a convergence of mechanical and electronic engineering.

The Society of Automotive Engineers (SAE International) has published multiple technical papers highlighting the growing application of sensor-integrated bolts in chassis, suspension, and powertrain sub-assemblies. The global connected car market was valued at approximately US$ 63 billion in 2023, according to GSMA.The growth of connected vehicles is indirectly increasing demand for intelligent fastening solutions that support vehicle telematics, safety systems, and structural integrity monitoring, especially in premium and commercial vehicles.

Category-wise Analysis

Design Insights

Threaded fasteners account for the leading share in the automotive fasteners market by design, commanding approximately 72% of overall market revenue. This dominance is attributed to the widespread application of bolts, screws, studs, and nuts across virtually every major vehicle sub-assembly, including engine blocks, transmission systems, chassis frames, and body-in-white structures.

Threaded fasteners offer distinct advantages in automotive manufacturing, including ease of disassembly for maintenance, superior load distribution, and compatibility with automated torque-controlled assembly lines. The Automotive Industry Action Group (AIAG) highlights that threaded fastening remains the predominant joining method across North American vehicle assembly plants, supported by established torque audit and quality control protocols.

Material Insights

Metal fasteners represent the dominant segment in the automotive fasteners market by material, holding approximately 85% of the total market share. The superiority of metal fasteners, primarily manufactured from carbon steel, stainless steel, and aluminum alloys, stems from their unmatched mechanical strength, thermal resistance, and fatigue durability, all of which are essential for safety-critical automotive applications.

High-strength steel fasteners conforming to ISO 898-1 property class standards (e.g., Class 8.8, 10.9, and 12.9) are extensively used in powertrain and structural assemblies. According to the World Steel Association, automotive-grade steel accounts for a substantial portion of global flat steel demand, with fastener applications constituting a consistent sub-segment.

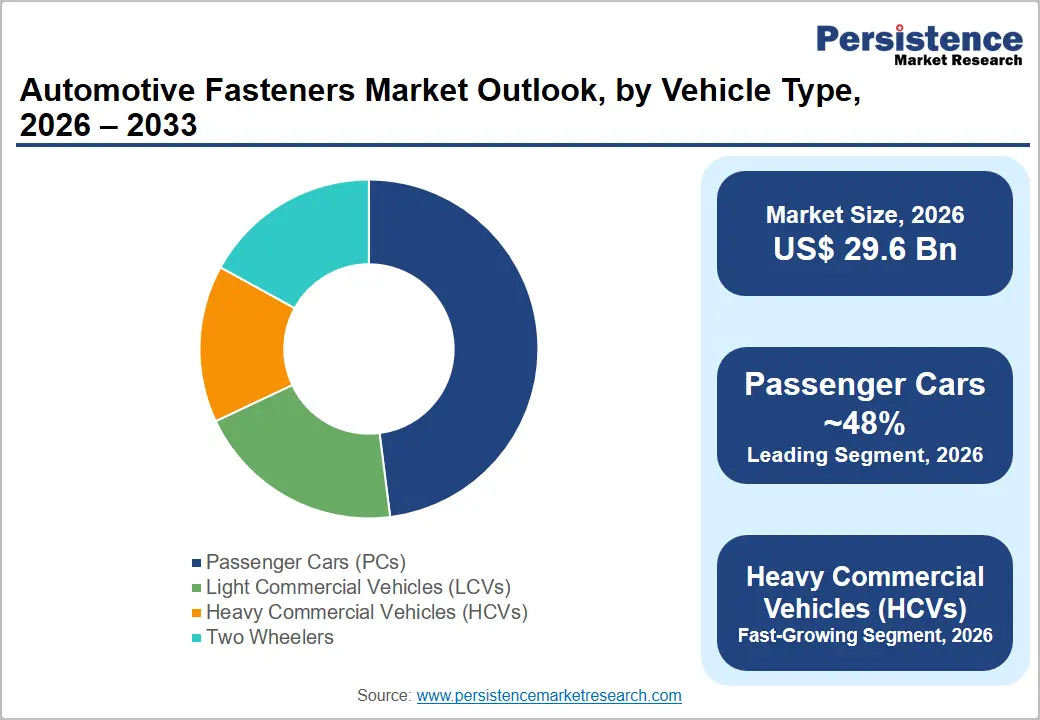

Vehicle Type Insights

Passenger Cars (PCs) dominate the vehicle type segmentation, contributing an estimated 48% of total market revenue. The global passenger car fleet continues to expand, with OICA reporting that passenger vehicles accounted for approximately 75% of total motor vehicle production globally in 2023.

Each passenger car requires several thousand fasteners across its body, powertrain, suspension, and interior systems, making this segment the highest-volume end-use category. The increasing consumer preference for feature-rich, technologically advanced passenger vehicles further increases fastener content per unit as OEMs integrate additional systems such as ADAS sensors, sunroofs, and multi-link suspension configurations.

Characteristic Insights

Removable fasteners hold the majority share in the market by characteristic, estimated at approximately 66% of total market share. The preference for removable fasteners, including threaded bolts, nuts, and screws, is rooted in the fundamental serviceability requirements of motor vehicles.

Automotive assembly standards worldwide prioritize designs that enable field maintenance, component replacement, and end-of-life recycling, all of which necessitate removable joining solutions. Regulatory frameworks in the European Union, particularly the End-of-Life Vehicles (ELV) Directive, mandate that vehicles be designed for efficient disassembly and material recovery, further entrenching the use of removable fasteners.

Regional Analysis

North America Automotive Fasteners Market Trends & Analysis

North America represents one of the most mature and consolidated automotive fasteners markets globally, driven by the well-established vehicle manufacturing bases in the United States, Canada, and Mexico. The region benefits from strong OEM demand from automakers including General Motors, Ford Motor Company, and Stellantis, all of which maintain extensive assembly operations across the continent.

The United States-Mexico-Canada Agreement (USMCA) reinforces regional supply chain integration, incentivizing domestic fastener sourcing. The growing adoption of electric vehicles under programs such as the U.S. Inflation Reduction Act (IRA) is creating incremental fastener demand, particularly for battery enclosure and structural applications. North America is projected to account for approximately 22% of the global automotive fasteners market throughout the forecast period.

U.S. Automotive Fasteners Market Size

The U.S. automotive fasteners market is projected to reach approximately US$ 5.8 billion in 2026, driven by the continued expansion of electric vehicle (EV) production, increasing reshoring of automotive manufacturing activities, and robust domestic vehicle demand. The United States remains one of the world's largest automotive production hubs, with light trucks, pickup trucks, and SUVs accounting for most vehicle sales. These vehicle segments require substantial volumes of structural, chassis, powertrain, and interior fasteners, supporting consistent market demand. Additionally, growing investments in EV assembly plants, battery manufacturing facilities, and advanced lightweight vehicle architectures are creating new opportunities for specialized and high-performance fastening solutions across the automotive value chain.

Europe Automotive Fasteners Market Trends, Drivers & Insights

Europe remains a key market for automotive fasteners, underpinned by the region's legacy of premium automotive engineering and the presence of major OEM headquarters including Volkswagen Group, BMW Group, Mercedes-Benz, Stellantis, and Renault Group. The region's stringent regulatory environment, driven by the European Green Deal and Euro 7 emissions norms, is accelerating electrification and lightweighting, creating sustained demand for high-performance fasteners.

Germany Automotive Fasteners Market Size

Germany's automotive fasteners market is estimated at approximately US$ 3.5 billion in 2026, reflecting the country's status as Europe's largest automotive manufacturing hub and a global leader in premium vehicle production. Home to renowned automotive brands such as BMW, Mercedes-Benz, Volkswagen, Audi, and Porsche, Germany generates substantial demand for high-precision fastening solutions used in powertrain systems, chassis assemblies, body structures, interiors, and advanced electronic components. The country's strong emphasis on engineering excellence, product quality, and vehicle safety supports the adoption of specialized, high-strength fasteners designed for demanding automotive applications.

U.K. Automotive Fasteners Market Size

The U.K. automotive fasteners market is estimated at approximately US$ 0.9 billion in 2026, supported by the presence of major vehicle manufacturing facilities operated by Jaguar Land Rover, Nissan, Toyota, BMW Mini, and other automotive producers. The country's automotive sector generates consistent demand for a wide range of fastening solutions used in vehicle assembly, powertrain systems, chassis components, and interior applications. Additionally, the U.K.'s growing focus on electric vehicle production is creating new opportunities for specialized fasteners designed for battery packs, lightweight structures, and advanced electronic systems.

France Automotive Fasteners Market Size

France's automotive fasteners market is estimated at approximately US$ 1.1 billion in 2026, supported by the extensive manufacturing operations of Renault Group and Stellantis, which maintain significant vehicle production capacity across the country. France also benefits from a well-developed network of tier-1 and tier-2 automotive suppliers that contribute to strong domestic demand for fastening solutions used in vehicle assembly, powertrain systems, body structures, and electronic components. The country's commitment to reducing vehicle emissions and accelerating electrification under national and European climate policies is driving investments in electric vehicle production and battery manufacturing.

Asia Pacific Automotive Fasteners Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing regional market for automotive fasteners, accounting for an estimated 40% of global market value. The region's dominance is rooted in the sheer scale of its vehicle production ecosystem, led by China, Japan, South Korea, and India. China alone produced over 30 million vehicles in 2023 according to CAAM, with an increasing proportion being new energy vehicles (NEVs), each requiring substantial quantities of precision fasteners. India's rapidly expanding automotive sector, supported by the Production Linked Incentive (PLI) Scheme for automobiles and auto components, presents strong growth prospects for fastener demand across both conventional and electric platforms.

China Automotive Fasteners Market Size

China's automotive fasteners market is estimated at approximately US$ 7.2 billion in 2026, making it the largest national market globally. The market is primarily driven by China's dominant position in automotive manufacturing, particularly in New Energy Vehicles (NEVs), where the country accounts for the majority of global EV production and sales. Leading domestic automakers such as BYD, SAIC Motor, Geely, Changan, and Great Wall Motor, alongside international OEM joint ventures, generate substantial demand for automotive fasteners across vehicle body structures, battery systems, powertrains, and electronic components. China's extensive supplier ecosystem and vertically integrated manufacturing base further strengthen market growth.

India Automotive Fasteners Market Size

India's automotive fasteners market is estimated at approximately US$ 1.8 billion in 2026, driven by the country's position as the world's largest two-wheeler manufacturing hub and one of the fastest-growing automotive markets globally. Strong production volumes across motorcycles, passenger vehicles, commercial vehicles, and three-wheelers generate substantial demand for a wide range of fastening solutions. Domestic automakers such as Tata Motors, Mahindra & Mahindra, Ashok Leyland, and TVS Motor, alongside major international manufacturers including Maruti Suzuki, Hyundai, Kia, Toyota, and Honda, continue to expand production capacity in response to rising vehicle demand.

Japan Automotive Fasteners Market Size

Japan's automotive fasteners market is estimated at approximately US$ 2.6 billion in 2026, reflecting the country's long-standing leadership in precision manufacturing and advanced automotive engineering. As the home of global automotive giants such as Toyota, Honda, Nissan, Subaru, Mazda, and Mitsubishi, Japan maintains a highly integrated supply chain that supports consistent demand for high-quality fastening solutions. The country's renowned fastener manufacturers are deeply embedded within OEM production networks, supplying specialized components for powertrains, chassis systems, vehicle electronics, and lightweight body structures.

Competitive Landscape

The global automotive fasteners market exhibits a moderately fragmented competitive structure, with a mix of large multinational corporations and regional specialized manufacturers. Leading global players maintain a competitive advantage through extensive product portfolios, metallurgical expertise, and long-term OEM supply agreements. Key strategies include geographic expansion into Asia Pacific markets, particularly India and Vietnam, investment in automated manufacturing for precision and consistency, and R&D in corrosion-resistant coatings and lightweight alloy fasteners.

Key Developments:

- In June 2025, ARaymond completed its full acquisition of FACIL, a key global fastener supplier for OEMs and commercial vehicle manufacturers. FACIL’s strong presence in North America and EMEA boosts ARaymond’s global footprint.

- In March 2025, Fontana Gruppo agreed to acquire a 60% stake in India-based Right Tight Fasteners for around INR 1,000 crore, strengthening its position in the country’s expanding vehicle-manufacturing hub.

Global Automotive Fasteners Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 21.3 Bn |

|

Current Market Value (2026) |

US$29.6 Bn |

|

Projected Market Value (2033) |

US$ 45.1 Bn |

|

CAGR (2026-2033) |

6.2% |

|

Leading Region |

Asia Pacific, 40% share |

|

Dominant Application |

Passenger Cars, 48% share |

|

Top-ranking Product |

Removable fasteners, 66% |

|

Incremental Opportunity |

US$ 15.5 Bn |

Companies Covered in Automotive Fasteners Market

- Illinois Tool Works Inc. (ITW)

- Bulten AB

- LISI Group

- Sundram Fasteners Limited

- Precision Castparts Corp.

- Nifco Inc.

- Penn Engineering & Manufacturing Corp.

- Fontana Gruppo

- KAMAX Holding GmbH & Co. KG

- Boltun Corporation

- Aoyama Seisakusho Co., Ltd.

- SPS Technologies

- Böllhoff Group

- Acument Global Technologies

- Meidoh Co., Ltd.

Frequently Asked Questions

The global Automotive Fasteners market is valued at US$ 29.1 Bn in 2026 and is forecast to reach US$ 45.1 Bn, expanding at a CAGR of 6.2% by 2033.

The primary growth drivers include the rapid global expansion of electric and hybrid vehicle production, particularly in China and India, rising automotive manufacturing volumes, and increasingly strict lightweighting regulations such as Euro 7 and updated U.S. CAFE standards, which demand advanced material-compatible fastening solutions.

Threaded fasteners dominate the market by design, commanding approximately 72% of total revenue. Their dominance is driven by their universal applicability across powertrain, chassis, and body assembly operations, compatibility with automated torque assembly systems, and serviceability advantages that align with regulatory disassembly requirements, particularly under the EU's ELV Directive.

Asia Pacific is the leading region, accounting for approximately 40% of global market revenue. This is driven by China's position as the world's largest vehicle producer, with over 30 million vehicles produced in 2023 according to CAAM, alongside strong automotive sectors in Japan, South Korea, and rapidly growing India.

Leading companies in the global Automotive Fasteners market include Illinois Tool Works Inc. (ITW), Bulten AB, LISI Group, Sundram Fasteners Limited, KAMAX Holding GmbH & Co. KG, Nifco Inc., Aoyama Seisakusho Co., Ltd., and Böllhoff Group, among others.