- Semiconductor Materials & Components

- Fast Rectifier Market

Fast Rectifier Market Size, Share, and Growth Forecast 2026 - 2033

Fast Rectifier Market by Forward Voltage (Less than 1.0V, >1.0V - 1.5V, More than 1.5V), Material Type (Standard Fast Recovery Diodes (FRD), Ultra-Fast Recovery Diodes (UFRD), Schottky Diodes, Others), Industry (Automotive, Consumer Electronics, Telecommunication, Energy & Utilities, Industrial, Others, and Regional Analysis, 2026 - 2033

Fast Rectifier Market Size and Trend Analysis

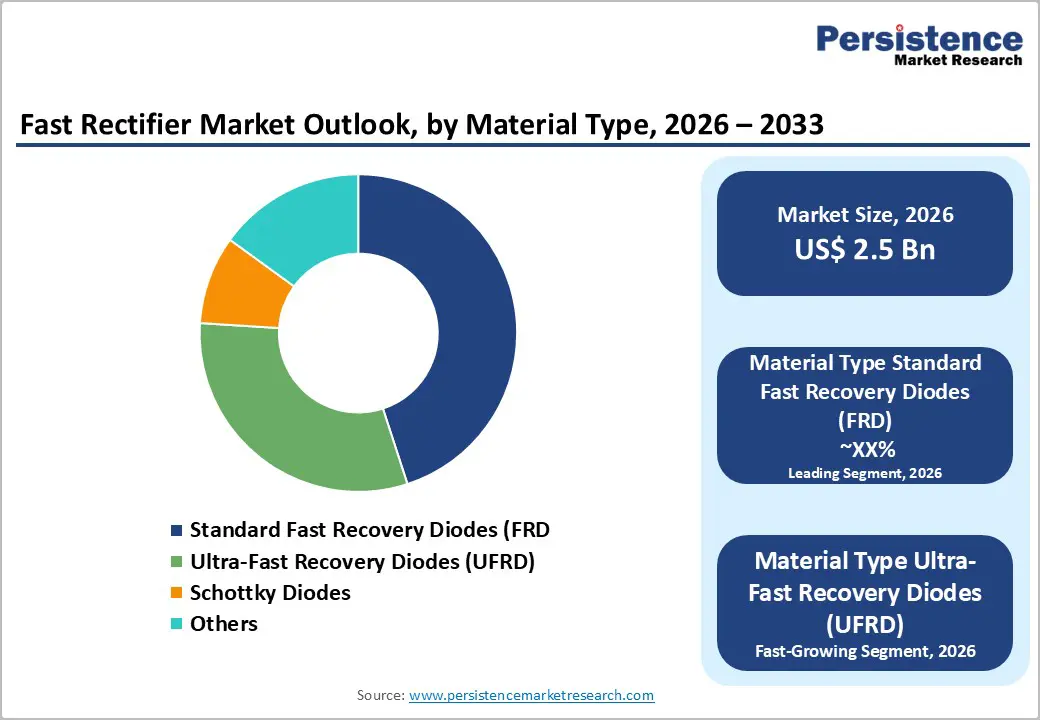

The global fast rectifier market size is projected to reach US$ 2.5 billion by 2026 and reach US$ 3.1 billion by 2033, registering a CAGR of 3.1% from 2026 to 2033.

The growth is primarily fueled by the rapid global shift toward electric vehicles and renewable energy systems, where efficient, low-loss power conversion is essential. Increasing integration of advanced electronic systems in automotive applications and stricter energy-efficiency regulations across major economies are further strengthening demand. As industries prioritize high-frequency, energy-efficient power control, fast rectifiers continue to play a critical role in next-generation power electronics.

Key Industry Highlights:

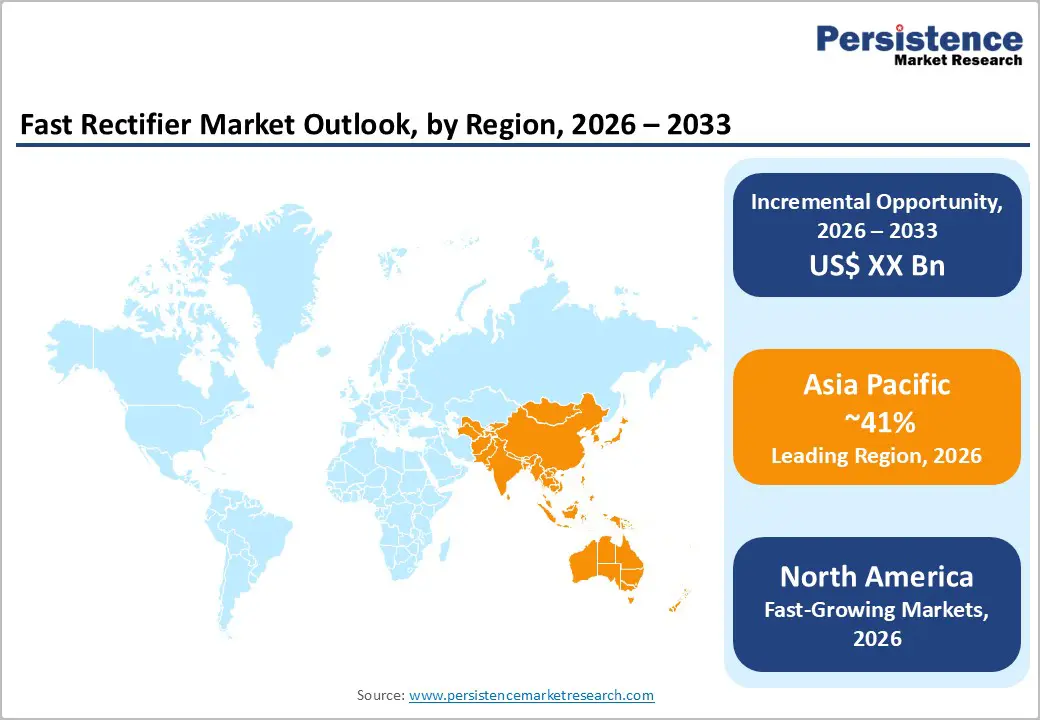

- Leading Region: Asia Pacific holds the largest ~41% share and is the fastest-growing region, supported by escalating EV adoption, expanding semiconductor manufacturing, and rising industrial automation.

- Fastest-Growing Region: North America leads the market with ~36% share, driven by major semiconductor investments, strong automotive electrification, and concentrated innovation ecosystems.

- Leading Category: Standard Fast Recovery Diodes dominate with ~52% share, owing to proven reliability, mature manufacturing, and broad compatibility across key electronics applications.

- Fastest-Growing Category: Ultra-Fast Recovery Diodes are the fastest-growing material segment, supported by rising demand for sub-100 ns recovery performance in advanced automotive and high-frequency systems.

- Key Market Opportunity: EV powertrains and renewable energy infrastructure remain key demand drivers, creating strong opportunities for high-efficiency rectifiers that reduce switching losses in modern power systems.

| Key Insights | Details |

|---|---|

|

Fast Rectifier Market Size (2026E) |

US$ 2.5 Billion |

|

Market Value Forecast (2033F) |

US$ 3.1 Billion |

|

Projected Growth CAGR (2026-2033) |

3.1% |

|

Historical Market Growth (2020-2025) |

2.5% |

Market Dynamics

Drivers - Accelerating Electric Vehicle Adoption and Powertrains Electrification

The fast rectifier market is experiencing strong growth driven by rapid EV adoption and the shift toward high-voltage, energy-efficient powertrains. Modern electric vehicles rely on advanced power electronics that minimize switching losses, creating a demand for fast rectifiers. The increasing penetration of Silicon Carbide (SiC) devices from under 20% in 2022 to an expected 60% by 2030 is further amplifying this need.

As automakers transition from 400V to 800V battery systems, the requirement for high-performance rectifiers in onboard chargers, inverters, and battery management units continues to rise. Leading automotive and semiconductor companies are investing heavily in tailored rectifier technologies for elevated-voltage architectures, reshaping competition and opening high-value opportunities across the EV ecosystem.

Renewable Energy Integration and Smart Grid Infrastructure Development

The global push toward solar, wind, and distributed renewable systems is creating substantial demand for efficient power conversion components, placing fast rectifiers at the center of modern energy infrastructure. Solar PV systems projected to grow at a CAGR of around 20% through 2032 require high-efficiency rectifiers to optimize inverter operations and support stable grid connectivity.

Smart grids and advanced energy management systems further rely on rectifiers capable of handling fluctuating loads and bidirectional power flow. Government-backed initiatives such as the U.S. Inflation Reduction Act and EU renewable energy policies are accelerating investment in clean-energy infrastructure, driving ongoing adoption of fast rectifiers that minimize energy loss and enhance system performance.

Restraints - High Manufacturing Costs and Capital-Intensive Production Requirements

The production of ultra-fast recovery rectifiers requires highly specialized processes, including advanced doping, precise epitaxial growth, and tightly controlled fabrication conditions. Setting up facilities capable of maintaining these stringent tolerances typically demands over $50 million in initial capital, creating barriers for new entrants and limiting participation to financially strong manufacturers. Rising labor and technology expenses further strain operational budgets.

Volatility in raw material prices and structural cost pressures make large-scale cost reduction difficult without significant redesigns of manufacturing methodologies. As a result, many producers face shrinking profit margins despite growing demand. These financial and technical complexities restrict industry growth potential and consolidate market power among established players with deep production capabilities.

Supply Chain Vulnerabilities and Trade Restriction Complexities

Evolving geopolitical tensions and fluctuating trade policies continue to disrupt global semiconductor supply chains, increasing uncertainty for fast rectifier manufacturers. Tariffs imposed during U.S.–China trade conflicts have raised sourcing and production costs, compelling companies to diversify their supplier base or relocate production that requires extensive time, planning, and investment. These disruptions complicate procurement strategies across the industry.

Since advanced semiconductor manufacturing remains concentrated in specific regions, the market is highly vulnerable to local disruptions from natural disasters, pandemics, or regulatory shifts. Smaller manufacturers, with limited geographic spread and lower resilience, face higher operational risks and elevated costs. These supply chain challenges collectively hinder efficiency and slow the market’s ability to respond to rising global demand.

Opportunity - Rapid Expansion of Industrial Automation and IoT-Enabled Systems

Industrial automation and IoT ecosystems are creating strong demand for fast rectifiers as industries shift toward high-efficiency, high-speed power components. Ultrafast recovery diodes now account for nearly 37% of the industrial motor drive segment, favored for offering around 20% lower costs with comparable performance to silicon carbide devices. Robotic welding systems using UFRD-based rectifiers achieve up to 19% faster cycle times, significantly improving throughput.

As global industrial energy consumption is expected to rise by 1.3% annually through 2030, reducing electromagnetic interference, heat generation, and switching losses becomes increasingly important. This positions ultrafast rectifiers as essential components for sustainable automation. The opportunity lies in developing application-specific rectifiers for manufacturing machinery, advanced robotics, material-handling systems, and connected industrial equipment.

Wide-Bandgap Semiconductor Technologies and Next-Generation Power Electronics

Silicon carbide (SiC) and gallium nitride (GaN) technologies represent a major opportunity for the fast rectifier market, enabling higher efficiency, lower losses, and improved thermal performance. Infineon’s release of its first 200mm SiC-based products to customers in Q1 2025 underscores the commercial maturity and accelerating adoption of wide-bandgap rectification technologies across industries. Their advantages make them ideal for high-voltage and high-frequency applications.

With the global SiC power semiconductor market forecast to grow at a 9.5% CAGR through 2030, significantly outpacing traditional silicon rectifiers, manufacturers investing in SiC and GaN production can capture high-value demand in EV infrastructure, renewable energy systems, and advanced industrial power electronics. Companies building strong wide-bandgap portfolios stand to secure premium margins and reinforce long-term competitive strength.

Category-wise Analysis

Forward Voltage Insights

The 1.0V–1.5V forward voltage range leads the market with nearly 45% share, supported by its balanced switching efficiency, stable thermal behavior, and broad suitability across automotive power electronics, consumer device chargers, and telecom power supplies. Its long-standing adoption, mature production ecosystem, and high customer qualification rates further reinforce its dominant position across established high-volume applications.

Demand is gradually shifting toward rectifiers with forward voltages above 1.5V, driven by next-generation EV platforms and renewable energy systems that prioritize reduced switching losses and superior thermal performance. As power architectures evolve toward higher voltages and faster switching, this category is emerging as the preferred choice for advanced conversion circuits, making it the fastest-growing segment within forward-voltage classifications.

Material Type Insights

Standard Fast Recovery Diodes (FRD) continue to hold the largest share at around 52%, backed by decades of proven reliability, cost efficiency, and seamless compatibility with existing automotive, industrial, and consumer electronics designs. Their dependable performance in high-frequency switching and well-established manufacturing base enable FRDs to remain the backbone of mainstream rectification applications worldwide.

Ultra-Fast Recovery Diodes (UFRD) and Schottky diodes represent the most rapidly expanding material categories as modern applications demand lower reverse-recovery times, superior efficiency, and enhanced thermal characteristics. Their rising adoption in high-frequency automotive systems, compact power supplies, and advanced electronics positions these premium technologies at the forefront of next-generation power conversion requirements.

Industry Insights

Automotive applications dominate the market with roughly 48% share, driven by accelerating EV adoption, electrified powertrains, and widespread integration of advanced driver-assistance systems. The sector’s reliance on high-efficiency power management, including onboard chargers, inverters, BMS units, and auxiliary conversion systems, ensures consistent and robust demand for fast rectifier technologies tailored to evolving vehicle electrical architectures.

The fastest-growing opportunities are emerging in renewable-focused industrial systems, advanced automation equipment, and next-generation communication electronics. As industries modernize machinery, scale clean-energy infrastructure, and expand IoT and high-frequency communication networks, the need for efficient, high-speed rectification grows rapidly. These segments increasingly favor advanced rectifiers that enhance system reliability, reduce power losses, and support demanding high-performance operating environments.

Regional Insights

North America Fast Rectifier Market Trends

North America leads the global fast rectifier market with around 36% share, supported by strong semiconductor manufacturing investments driven by the U.S. CHIPS and Science Act. Its established automotive ecosystem spanning the Great Lakes and Midwest creates consistent demand for high-efficiency rectifiers used in EV powertrains, onboard chargers, and power management systems. Federal and state EV policies further reinforce technology adoption.

The region also benefits from a high concentration of semiconductor design centers and R&D hubs across Silicon Valley and other innovation corridors. Strict qualification standards within the automotive and industrial supply chains favor established manufacturers with advanced manufacturing capabilities, ensuring sustained technological advancement and stable long-term demand for fast rectifier solutions.

Europe Fast Rectifier Market Trends

Europe remains a strategically important market, expanding at a CAGR of about 3.4%, driven by strong electrification in the automotive sector and robust renewable energy deployment mandates. Germany anchors the region’s leadership through its dense concentration of automotive OEMs and semiconductor innovators, with companies like Infineon advancing cutting-edge silicon, SiC, and GaN rectifier technologies showcased at PCIM Europe 2025.

Harmonized regulatory frameworks, energy transition programs, and high-quality manufacturing standards support market consolidation and favor suppliers with established European production bases. Additional demand comes from France and the United Kingdom, where accelerating EV initiatives, growing industrial automation, and expanding data center infrastructure drive adoption of advanced fast rectifier components.

Asia Pacific Fast Rectifier Market Trends

Asia Pacific dominates growth momentum and holds about 41% of global market share, underpinned by rapid electrification in China, the world’s largest EV market and expansive semiconductor manufacturing across Taiwan, Malaysia, Vietnam, and growing facilities in India. Cost-competitive production and vertically integrated supply chains provide unmatched scale advantages for fast rectifier suppliers.

The region’s semiconductor market is accelerating, supported by large-scale investments, including Japan’s $2.7 billion power device manufacturing collaboration and India’s $10 billion semiconductor mission. These initiatives, combined with rising domestic electronics consumption and export-focused manufacturing growth, position the Asia Pacific as the fastest-expanding market with substantial long-term opportunities in EVs, renewable energy, consumer electronics, and industrial automation.

Competitive Landscape

The global fast rectifier market is moderately consolidated, with international manufacturers holding substantial influence through vertically integrated operations, broad product portfolios, and long-standing customer relationships across automotive, industrial, and consumer electronics sectors. These companies anchor the competition through continuous investments in advanced semiconductor materials, innovative packaging techniques, and next-generation power-electronics architectures.

Regional players and emerging specialists contribute additional competition by offering niche product designs, localized technical support, and targeted application expertise. Industry dynamics increasingly favor firms investing in wide-bandgap technologies and expanded manufacturing capabilities, with consolidation, joint ventures, and rising R&D expenditure shaping long-term competitive positioning and technological leadership.

Key Industry Developments:

- In November 2024, Vishay Intertechnology unveiled four new automotive-grade eSMP solutions featuring the SMF (DO-219AB) package, demonstrating continuous innovation in rectifier technology and reinforcing the company's commitment to automotive segment leadership as vehicle electrification accelerates globally.

- In February 2025, Infineon Technologies AG made significant progress on its silicon carbide roadmap by releasing its first products manufactured using advanced 200mm SiC technology to customers in Q1 2025, providing first-class SiC power technology for high-voltage applications, including renewable energy, trains, and electric vehicles.

- In May 2025, Nexperia closed the 2024 financial year with total revenue of $2.06 billion, increasing market share in defined markets to 9.7% from 8.9% in the previous year, while making substantial investments in next-generation manufacturing capabilities, specifically in Silicon Carbide and Gallium Nitride technologies, underscoring its commitment to long-term growth.

Companies Covered in Fast Rectifier Market

- Vishay Intertechnology

- STMicroelectronics

- Infineon Technologies

- ON Semiconductor (onsemi)

- ROHM Semiconductor

- Diodes Incorporated

- Nexperia

- Toshiba Electronic Devices

- Microchip Technology (Microsemi)

- Littelfuse

- IXYS

- Central Semiconductor

- Semikron

- PANJIT International

- Fuji Electric

Frequently Asked Questions

The global fast rectifier market is expected to grow from US$ 2.5 billion in 2026 to US$ 3.1 billion by 2033, reflecting a 3.1% CAGR driven by EV electrification, renewable energy growth, and expanding industrial automation.

Demand is driven by EV adoption, 800V powertrain shift, renewable energy expansion, energy-efficiency mandates, and rising automation and high-frequency power electronics requirements.

Standard Fast Recovery Diodes (FRD) lead the market with ~52% share, supported by proven reliability, mature manufacturing, and broad design compatibility.

Asia Pacific leads with ~41% share, followed by North America at ~36%, driven by strong EV adoption, large-scale semiconductor production, and expanding electronics manufacturing.

Key opportunities include industrial automation growth, wide-bandgap (SiC & GaN) adoption, 800V EV platforms, and renewable energy infrastructure expansion requiring high-efficiency power conversion.