- Pharmaceuticals

- Dermal Fillers Market

Dermal Fillers Market Size, Share, and Growth Forecast 2026 - 2033

Dermal Fillers Market by Product (Absorbable, Non-Absorbable), Ingredient (Hyaluronic Acid, Poly-L-Lactic Acid, Calcium Hydroxylapatite, Polymethyl Methacrylate, Collagen), Application (Aesthetic Restoration, Dentistry, Reconstructive Surgery), End-user (Dermatology Clinics, Cosmetic & Aesthetic Clinics, Hospitals, Medical Spas), and Regional Analysis, 2026–2033

Dermal Fillers Market Share and Trends Analysis

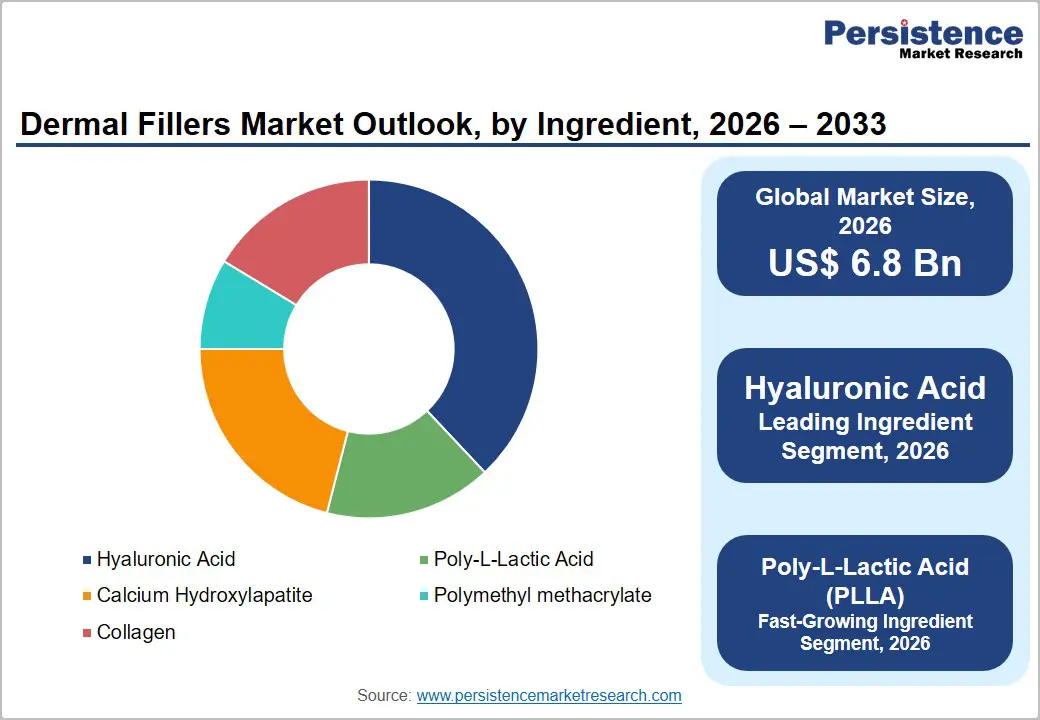

The global dermal fillers market size is expected to be valued at US$ 6.8 billion in 2026 and projected to reach US$ 13 billion, growing at a CAGR of 9.7% between 2026 and 2033.

Increasing demand for minimally invasive aesthetic procedures and rising consumer focus on facial appearance and anti-aging treatments. Dermal fillers are widely used for wrinkle reduction, lip enhancement, facial contouring, and skin rejuvenation, offering faster recovery and natural-looking results compared to surgical alternatives. The growing influence of social media, celebrity endorsements, and expanding medical spa networks is further supporting market adoption globally. Technological advancements in hyaluronic acid and biostimulatory filler formulations are improving treatment safety and longevity.

Key Industry Highlights

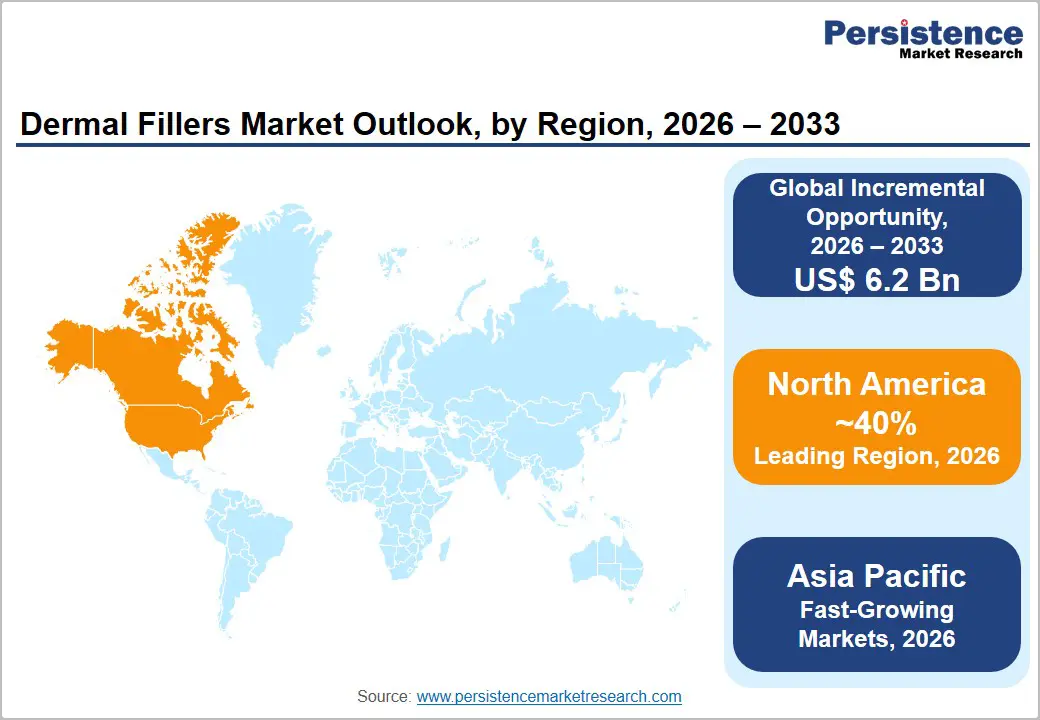

- Leading Region: North America is likely to leads the global market with 40% share in 2026, anchored by 3.4 million ASPS-documented filler procedures in the U.S. in 2022, 8,800+ AmSpa-reported medical spas, and AbbVie and Galderma’s commercially dominant Juvéderm® and Restylane® portfolios.

- Fast-Growing Market: Asia Pacific is projected to have the highest CAGR driven by South Korea’s global aesthetic innovation leadership, China’s NMPA-approved domestic HA filler expansion at 30%+ annual procedure growth, and medical tourism-driven filler demand across Thailand, Singapore, and India.

- Dominant Ingredient Segment: Hyaluronic Acid leads the ingredient category with 38% market share in 2025, supported by its reversibility profile, the broadest FDA-approved indication set of any filler ingredient, and dominant commercial portfolios from Juvéderm® (AbbVie) and Restylane® (Galderma) with sustained injector loyalty globally.

- Fast-Growing Ingredient Segment: Poly-L-Lactic Acid (PLLA) is the fastest growing ingredient over 2026–2033, driven by Galderma’s March 2025 FDA approval of Sculptra® for body contouring, consumer preference for 2–3 year duration results versus HA’s 6–12 months, and expanding non-facial biostimulator indications.

Market Dynamics

Drivers - Aging Global Demographics Generating Dual Aesthetic and Reconstructive Filler Demand

The accelerating global aging trend is generating structurally compounding demand for dermal fillers across both cosmetic volume restoration and medical reconstructive indications. The United Nations projects the global population aged 60 and above will nearly double from 1 billion in 2020 to 2.1 billion by 2050, with this demographic exhibiting the highest per-capita spending on aesthetic procedures. Age-related volume loss in the mid-face, temples, and perioral regions is the primary clinical driver of hyaluronic acid (HA) and calcium hydroxylapatite (CaHA) filler utilization.

Simultaneously, aging oncology and trauma patients requiring reconstructive soft tissue volume restoration, including post-mastectomy facial reconstruction and scar management, are expanding filler utility into clinical medicine. The American Academy of Dermatology (AAD) estimates over 85 million Americans aged 45 and above actively seek facial rejuvenation options, representing a consistently large and demographically self-renewing patient pool.

Social Media Influence and Medical Spa Proliferation Normalizing Aesthetic Filler Procedures

The growing influence of social media platforms and the rapid expansion of medical spas are significantly driving demand in the dermal fillers market. Platforms such as Instagram, TikTok, and YouTube have increased consumer awareness regarding facial aesthetics, anti-aging treatments, and minimally invasive cosmetic procedures by promoting beauty trends and before-and-after transformation content.

This rising digital exposure has normalized aesthetic enhancements among younger and middle-aged consumers, encouraging greater acceptance of filler procedures. Simultaneously, the increasing number of medical spas and aesthetic clinics offering convenient, personalized, and comparatively affordable cosmetic services has improved treatment accessibility across urban markets. Medical spas are also adopting advanced filler technologies and promotional packages to attract customers seeking non-surgical facial rejuvenation.

Restraints - Adverse Event Risk and Product Safety Concerns Limiting Consumer Confidence

Dermal filler-associated adverse events—including vascular occlusion, granulomas, biofilm infections, and rare but severe complications such as blindness from intravascular injection represent a meaningful barrier to consumer adoption and create reputational risk for the broader market. The U.S. Food and Drug Administration (FDA) has issued multiple safety communications regarding dermal filler risks, and the FDA’s MedWatch database has documented increasing adverse event reports correlated with the growth in procedure volumes. High-profile social media coverage of filler complications amplifies consumer anxiety and has contributed to increased demand for reversal agents (hyaluronidase), moderating net procedure growth in safety-aware patient populations.

Regulatory Complexity and Variable Market Authorization Across Key Geographies

Dermal fillers are classified as medical devices in the U.S. (FDA Class III)) and EU (Class III under MDR 2017/745), requiring rigorous pre-market approval or CE marking processes that represent significant time-to-market and compliance cost barriers for manufacturers. The transition to EU MDR from the legacy Medical Device Directive has significantly extended conformity assessment timelines, with multiple filler products facing temporary market withdrawal or delayed re-certification. Variable classification frameworks across Asia Pacific markets, where fillers may be classified as drugs or devices depending on jurisdiction, further fragment market access strategies and increase regulatory overhead for companies pursuing global commercial expansion.

Opportunities - Poly-L-Lactic Acid (PLLA) Biostimulators: Fastest Growing Ingredient Segment

Poly-L-Lactic Acid (PLLA) biostimulators represent the fastest growing ingredient segment in the dermal fillers market, driven by their mechanistically distinct mode of action that addresses the root cause of facial aging, collagen loss, rather than volumizing through a gel matrix. Sculptra® Aesthetic (AbbVie) and Sculptra® have established PLLA’s efficacy in clinical practice, while next-generation PLLA products are in development across multiple companies.

According to Revance Therapeutics, Inc., consumer preference research consistently indicates that longer-lasting results (2–3 years versus 6–12 months for most HA fillers) are among the highest-valued attributes in aesthetic procedure decision-making. PLLA’s efficacy in body contouring applications, including buttock augmentation and hand rejuvenation, is broadening its addressable indication set beyond facial aesthetics, creating significant expansion opportunities for manufacturers with established PLLA regulatory approvals and commercial infrastructure.

Category-wise Analysis

Product Insights

Absorbable dermal fillers dominate the global dermal fillers market by product type, likely to command a positive market share in 2026. Absorbable fillers, including hyaluronic acid, calcium hydroxylapatite, poly-L-lactic acid, and collagen-based products, are preferred by both clinicians and patients due to their natural degradation over time, reversibility of HA-based products via hyaluronidase, and absence of permanent foreign body retention risk. The reversibility profile of HA fillers in particular provides a critical safety reassurance that non-absorbable alternatives cannot offer, making them the standard recommendation under ASPS and British Association of Aesthetic Plastic Surgeons (BAAPS) clinical guidance frameworks.

Non-absorbable fillers, including polymethyl methacrylate (PMMA) products such as Bellafill®, retain a niche role in specific long-duration indication applications, but their potential for permanent complications limits broad adoption. The FDA’s conservative stance on permanent fillers, with PMMA being the only non-absorbable filler with current U.S. FDA approval, reinforces the overwhelming commercial dominance of absorbable products.

Ingredient Insights

Hyaluronic Acid (HA) is expected to lead the dermal fillers market by ingredient, accounting for approximately 38% share in 2026. HA’s market leadership is supported by an unrivaled combination of clinical attributes: natural biocompatibility as an endogenous extracellular matrix component, reversibility via hyaluronidase injection in the event of adverse outcomes, a wide range of available cross-linking technologies enabling product differentiation by viscosity and longevity, and the broadest FDA-approved indication set of any filler ingredient.

Major HA filler portfolios, including Juvéderm® (AbbVie), Restylane® (Galderma), Teosyal® (Teoxane SA), and RHA® Collection (Revance Therapeutics), collectively account for a dominant share of global filler procedure volumes. The HA segment benefits from continuous innovation, including Vycross™ technology (Allergan/AbbVie) and XpresHAn Technology™ (Galderma) that extends duration, improves natural movement, and broadens treatable anatomical regions, sustaining premium pricing and market leadership.

Application Insights

Aesthetic restoration represents the dominant application segment in the dermal fillers market in 2026, accounting for the substantial majority of global procedure volumes and revenues. This leadership reflects the core commercial proposition of dermal fillers as non-surgical facial rejuvenation and volumization tools, addressing indications including nasolabial folds, marionette lines, lip augmentation, cheek volumization, tear trough correction, and jawline definition.

According to the American Society for Aesthetic Plastic Surgery (ASAPS), facial filler injections consistently rank among the top-three most performed non-surgical aesthetic procedures in the U.S. by both volume and revenue. The aesthetic restoration segment’s breadth of clinical indication, compatibility with combination treatment protocols (neurotoxin + filler), and suitability for serial treatment on annual maintenance cycles sustains high per-patient lifetime value and consistent procedure revenue generation for aesthetic clinic operators globally.

End-user Insights

Cosmetic & aesthetic clinics represent the leading end-user segment in the dermal fillers market in 2026, driven by their role as the primary practice setting for elective aesthetic filler procedures globally. These dedicated aesthetic facilities offer specialized injector expertise, curated product portfolios, and optimized patient experience environments that command higher procedure fees and volume than hospital or general dermatology settings.

The AmSpa State of the Industry Report documented that the majority of medical spa and aesthetic clinic revenues in the U.S. derive from injectable treatments, including fillers and neurotoxins, reflecting the segment’s commercial centrality. In the Asia Pacific, the proliferation of dedicated aesthetic medicine clinics in South Korea, China, and Thailand, often vertically integrated from training to product supply, further reinforces cosmetic and aesthetic clinics as the anchor procurement and procedure channel globally.

Regional Insights

North America Dermal Fillers Market Trends and Insights

North America leads the global dermal fillers market with 40% share in 2026, anchored by the world’s highest per-capita aesthetic procedure spending, a mature medical spa ecosystem with over 8,800 facilities per AmSpa data, and the commercial leadership of AbbVie (Juvéderm®) and Galderma (Restylane®). FDA-regulated innovation pathways and U.S. Medicare/private insurance exclusions for elective aesthetics sustain premium market pricing that elevates average revenue per procedure above global benchmarks.

U.S. Dermal Fillers Market Size

The United States accounts for approximately 87% of North American market revenues, supported by over 3.4 million filler procedures performed in 2022 per ASPS data, a highly concentrated aesthetic specialist injector base, and the dominant commercial positions of Juvéderm® and Restylane®. FDA approval of Revance Therapeutics’ RHA® Collection and the expansion of Sculptra® indications are driving premium market segment growth.

Europe Dermal Fillers Market Trends and Insights

Europe is the second-largest dermal fillers market, characterized by high per-capita aesthetic procedure rates in France, Germany, and the U.K., a strong tradition of physician-administered aesthetic medicine, and the EU MDR (2017/745) regulatory framework establishing the world’s most stringent filler device safety and efficacy requirements. The ongoing ‘Korean wave’ of HA filler brands achieving CE marking is intensifying competitive dynamics across European aesthetic clinics.

Germany Dermal Fillers Market Size

Germany accounts for approximately 22% of European market revenues, driven by a large specialist aesthetic dermatology and plastic surgery community, high private health insurance penetration for aesthetic procedures, and strong domestic demand for Juvéderm® and Restylane® HA fillers. Merz Pharma GmbH & Co. KGaA’s Radiessse® and Belotero® portfolios benefit from domestic brand equity and an established injector training infrastructure.

U.K. Dermal Fillers Market Size

The U.K. contributes approximately 19% revenue share with demand underpinned by one of Europe’s highest medical spa densities and recent landmark regulatory action: the Health and Care Act 2022 restricted non-surgical cosmetic procedures, including filler injections, to qualified healthcare professionals only, effective 2023, consolidating procedure volumes toward registered aesthetic clinics and elevating average procedure quality and pricing.

France Dermal Fillers Market Size

France contributes approximately 14–16% of European market revenues, supported by a sophisticated aesthetic medicine culture with high rates of HA filler use among women aged from 35 to 55. France’s Agence Nationale de Sécurité du Médicament et des Produits de Santé (ANSM) enforces rigorous post-market surveillance of filler products, and Laboratoires Vivacy (makers of Stylage®) maintains strong domestic brand recognition among French aesthetic injectors.

Asia Pacific Dermal Fillers Market Trends and Insights

Asia Pacific is the fastest-growing regional market for dermal fillers, driven by South Korea’s globally recognized aesthetic medicine innovation ecosystem, China’s rapidly formalizing medical aesthetics market, and the normalization of filler procedures among younger consumer demographics across Japan, Thailand, and India. China’s NMPA has approved multiple domestic HA filler brands, with annual procedure volumes estimated to grow over 30% annually in tier-1 cities between 2019 and 2023, fueling rapid revenue expansion across the region.

India Dermal Fillers Market Size

India accounts for approximately 10% regional revenue share with demand driven by a rapidly expanding urban affluent consumer base, growing medical tourism for aesthetic procedures from Middle Eastern and South Asian diaspora patients, and an increasing number of NABH-accredited aesthetic clinics in metros offering Juvéderm® and Restylane® at competitive price points versus European and U.S. markets.

Competitive Landscape

The global dermal fillers market is highly competitive, driven by continuous innovation in aesthetic medicine and increasing consumer demand for minimally invasive cosmetic procedures. Market participants are focusing on developing longer-lasting, safer, and more natural-looking filler formulations to strengthen their market presence.

Competition is intensifying through frequent product launches, regulatory approvals, and expansion of aesthetic treatment portfolios targeting facial rejuvenation and anti-aging applications. Companies are also investing in physician training programs, digital marketing strategies, and partnerships with dermatology clinics and medical spas to enhance customer reach.

Key Developments:

- In May 2026, Evolus announced the commercial launch of its Estyme injectable hyaluronic acid dermal filler collection in Europe, marking the company’s entry into the international dermal fillers market. The portfolio included Estyme Smooth, Form, Lips, and Sculpt, designed for multiple facial aesthetic applications, including mid-face volumizing.

- In September 2025, Allergan Aesthetics launched the “Naturally You with Injectable Hyaluronic Acid Fillers” campaign to improve consumer awareness and education regarding hyaluronic acid (HA) injectable fillers. The initiative aimed to address misinformation surrounding dermal fillers and highlight their safety, effectiveness, and natural-looking aesthetic outcomes.

- In August 2024, Bolton Council, Bolton Youth Voices, and Itsjustforme.com launched a campaign to raise awareness about the dangers of cosmetic injections for under-18s, highlighting the illegality of such treatments. The campaign uses educational social media and videos on TikTok and Instagram.

- In June 2024, Evolus, a performance beauty company in the U.S., submitted the final module of its premarket approval application for Evolysse™ Lift and Evolysse™ Smooth dermal filler products for the nasolabial fold to the FDA, marking a significant milestone in the company's commitment to market-ready dermal filler products.

Global Dermal Fillers Market – Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.0 Billion |

| Current Market Value (2026) | US$ 6.8 Billion |

| Projected Market Value (2033) | US$ 13.0 Billion |

| CAGR (2026–2033) | 9.7% |

| Leading Region | North America, 40% market share (2026) |

| Dominant Product (Category-1) | Absorbable Fillers, leading share (2026) |

| Top-ranking Ingredient (Category-2) | Hyaluronic Acid, 38% market share (2026) |

| Incremental Opportunity | US$ 6.2 Billion (2026–2033) |

Companies Covered in Dermal Fillers Market

- AbbVie Inc.

- Galderma

- Merz Pharma GmbH & Co. KGaA

- Sinclair Pharma

- Teoxane SA

- Revance Therapeutics, Inc.

- Prollenium Medical Technologies Inc.

- Laboratoires Vivacy

- LG Chem Ltd.

- Medytox Inc.

- Anika Therapeutics, Inc.

- Suneva Medical, Inc.

- IBSA Farmaceutici Italia Srl

Frequently Asked Questions

The global dermal fillers market is projected to be valued at US$ 6.8 billion in 2026.

Growing awareness through social media, celebrity influence, and beauty trends is encouraging more individuals to undergo filler procedures for wrinkle reduction, lip enhancement, and facial contouring.

North America leads with approximately 40% share in 2026, anchored by the U.S. market’s 3.4 million annual filler procedures, the commercial dominance of AbbVie’s Juvéderm® and Galderma’s Restylane®, and an aesthetic clinic and medical spa density that is among the world’s highest, supported by FDA-regulated product innovation pathways enabling rapid new indication approvals.

Growing adoption of advanced biostimulatory and long-lasting fillers that provide natural-looking facial rejuvenation is further supporting future growth. In addition, the expansion of medical spas, aesthetic dermatology clinics, and online beauty consultation platforms is improving treatment accessibility.

AbbVie Inc., Galderma, Merz Pharma GmbH & Co. KGaA, and Sinclair Pharma.