- Electric Mobility

- EV Lubricants Market

EV Lubricants Market Size, Trends, Share, and Growth Forecast 2025 - 2032

EV Lubricants Market by Product Type (Drive System Fluids, Electric Motor Cooling Fluids, Battery Thermal Management Fluids, Brake Fluids, Greases), Vehicle Type (Electric Two-Wheelers, Electric Three-Wheelers, Passenger Electric Vehicles, Light Commercial Electric Vehicles, Medium & Heavy Commercial Electric Vehicles, Others), Chemistry, Distribution Channel by Regional Analysis, 2025 - 2032

EV Lubricants Market Size and Trend Analysis

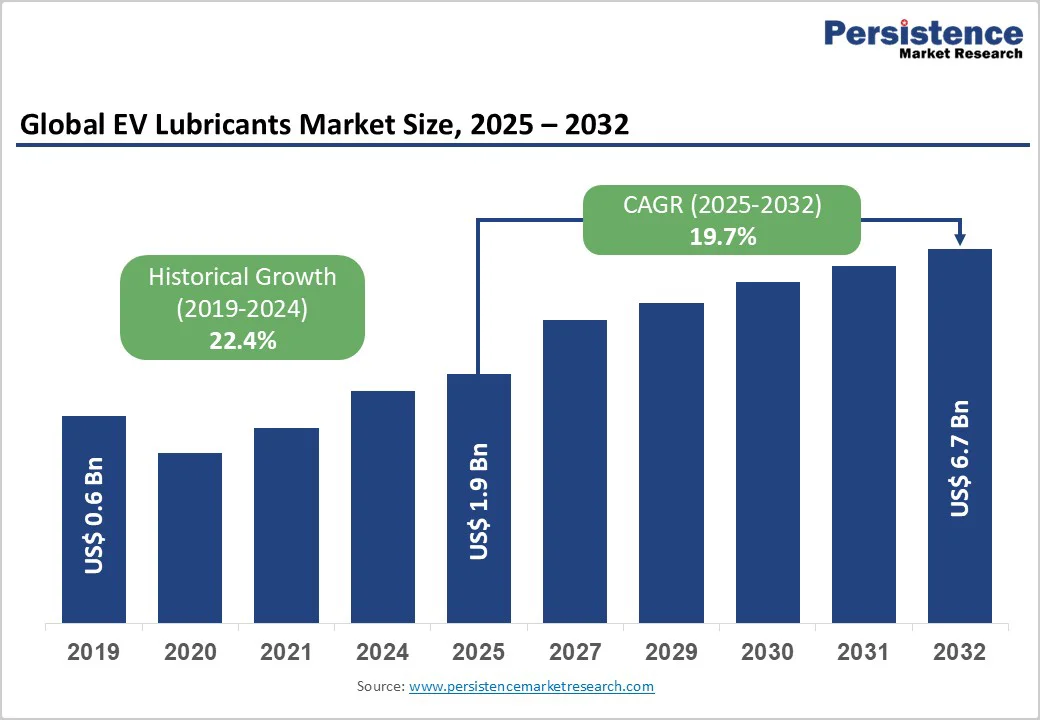

The global EV lubricants market size is likely to be valued at US$ 1.9 billion in 2025 and projected to reach US$ 6.7 billion by 2032, growing at a CAGR of 19.7% between 2025 and 2032.

The rapid growth of the EV market highlights a major shift from internal combustion engines to electric drivetrains, with global EV penetration reaching around 17% of passenger vehicle sales. Rising production of BEVs, PHEVs, and HEVs supported by strong government mandates and OEM electrification strategies is accelerating demand.

Key growth drivers include expanding investments in battery thermal management, increasing need for specialized drivetrain fluids, stricter emissions regulations, and ongoing innovation in fluid chemistries tailored to new EV architectures.

Key Market Highlights

- Leading Region: Asia Pacific dominates the EV lubricants market with 48% share and 22% CAGR, driven by China’s huge EV manufacturing facilities, India’s fastest-growing commercial EV segment, and accelerating Southeast Asia adoption.

- Fastest Growing Segment: Light Commercial Electric Vehicles represent the fastest-growing segment at 24% CAGR between 2025 - 2032, outpacing passenger vehicle growth as commercial operators prioritize total cost of ownership and operational efficiency.

- Dominant Segment: Battery Thermal Management Fluids command the dominant product type segment with 42% market share, reflecting critical importance to EV performance, range, safety, and battery longevity across all vehicle categories.

- Leading Segment: Passenger Electric Vehicles maintain leading vehicle type dominance with 66% market share, supported by concentrated OEM production, established supply chains, and regulatory mandates in developed markets.

- Key Opportunity: Battery Thermal Management and Direct Immersion Cooling Technologies represent the key market opportunity, enabling faster charging, extended driving range, and superior battery protection, driving premium fluid adoption.

| Key Insights | Details |

|---|---|

| EV Lubricants Market Size (2025E) | US$ 1.9 billion |

| Market Value Forecast (2032F) | US$ 6.7 billion |

| Projected Growth CAGR (2025 - 2032) | 19.7% |

| Historical Market Growth (2019 - 2024) | 22.4% |

Market Dynamics

Drivers - Rapid Electrification of Global Automotive Fleet and OEM Production Commitments

The global automotive industry is experiencing an unprecedented shift toward electrification, with electric vehicle (EV) sales representing about 17% of global new vehicle sales in 2024, up from approximately 9% in 2022. This acceleration reflects both consumer preference for sustainable mobility and binding regulatory mandates.

In Europe, the European Union’s CO2 emission standards require automakers to sell at least 20% electric vehicles starting January 1, 2025, to avoid penalties reaching US$ 15.76 billion.

Each new EV requires specialized lubricants and fluids fundamentally different from traditional automotive oils-including battery thermal management fluids, electric drivetrain fluids, motor cooling fluids, and high-performance greases. The surge in vehicle production directly translates to exponential demand for specialized EV lubricants across all vehicle categories.

Advanced Battery Technology Evolution and Thermal Management Criticality

Modern electric vehicle batteries, particularly lithium-ion pack architectures, generate significant heat during charging and discharging cycles, requiring sophisticated thermal management systems to maintain optimal operating temperatures between 0-45°C for maximum performance and battery longevity.

Battery thermal management fluids (TMFs) represent a critical category, as high battery temperatures compromise power output, reduce driving range, trigger premature degradation, and in extreme cases initiate thermal runaway events.

The Lubrizol Corporation developed its EVOGEN TM1000 Series specifically for immersion cooling applications, offering balanced static dissipation, strong corrosion inhibition, and excellent material compatibility.

These innovations reflect market recognition that superior thermal management directly enables longer battery range, faster charging, extended battery life, and enhanced overall vehicle efficiency-compelling automakers and fleet operators to specify premium, performance-engineered thermal fluids despite higher costs versus conventional automotive lubricants.

Restraints - High Development and Formulation Costs Combined with OEM Specification Stringency

EV lubricants represent a specialized category requiring extensive research and development investment to meet unprecedented technical requirements spanning electrical insulation, thermal conductivity, wear protection, oxidation stability, and material compatibility with diverse components. The OEM approval process can require 1-5 years of rigorous validation before commercial deployment, representing substantial R&D expenditure for lubricant manufacturers.

Furthermore, each automotive OEM develops proprietary fluid specifications aligned with their unique drivetrain architecture, motor design, and battery management system requirements. Smaller lubricant suppliers lack R&D infrastructure and OEM relationships to justify costly development programs, creating barriers to market entry and limiting competitive dynamics.

Additionally, the regulatory complexity surrounding fluid classification, labeling, safety data sheet compliance, and environmental regulations (including biodegradability requirements in certain jurisdictions) increases formulation complexity and commercialization timelines.

Market Uncertainty Regarding “Fill-for-Life” Adoption and Extended Service Intervals

A significant challenge constraining the EV lubricants aftermarket opportunity stems from widespread OEM adoption of “fill-for-life” policies for EV fluids, particularly battery thermal management fluids, transmission fluids, and greases. Unlike internal combustion engines requiring regular oil changes and maintenance, many EV manufacturers position transmission fluids and coolants as sealed, non-serviceable components throughout the vehicle lifetime.

Industry analysis indicates that BEV transmission fluids and coolants are increasingly designated as “fill for life” applications, reducing service fill demand in the immediate post-purchase period. The temporal gap between vehicle delivery and service fill requirement creates short-term revenue uncertainty and inventory management challenges for lubricant suppliers operating through aftermarket distribution channels.

Opportunity - Expansion of EV Commercial Vehicle and Light Commercial Vehicle Segments with Specialized Requirements

While passenger electric vehicles currently dominate market share, commercial and light commercial electric vehicles (LCEVs) represent the highest-growth opportunity segment, projected to achieve a positive CAGR between 2025-2032, significantly outpacing passenger vehicle growth rates.

This acceleration reflects fleet operator recognition that daily electric vehicle operation across last-mile delivery, urban logistics, and regional distribution generates superior returns on investment versus long-haul over-the-road trucking.

Companies such as Altigreen partnered with Gulf Oil Lubricants to develop customized EV fluids for electric three-wheelers and cargo vehicles, highlighting OEM commitment to specialized fluid solutions for this emerging segment. India’s commercial three-wheeler EV market, featuring operators like Piaggio Vehicles and Switch Mobility launching electric buses, demonstrates explosive growth potential.

The commercial vehicle opportunity presents higher-margin specialization possibilities as customers prioritize operational efficiency and total cost of ownership, justifying premium fluid investments for performance enhancement and downtime reduction.

Integration of Advanced Chemistry Innovations and Multi-Functional Fluid Solutions

Emerging fluid chemistry innovations create substantial market opportunities as lubricant manufacturers transition from adapting existing formulations toward developing purpose-engineered EV fluids incorporating novel base stock and additive technologies.

Polyalkylene glycols (PAGs) demonstrate superior thermal conductivity and energy efficiency versus traditional PAO base stocks. Polyol ester (POE) and fluorinated dielectric fluid technologies (HFE, HFO, HFPE) enable direct immersion cooling applications previously impossible with conventional mineral or PAO oils.

Manufacturers are developing multi-functional fluids combining lubrication, cooling, and dielectric properties within a single product, reducing component count and system complexity. Water-based lubricants formulated by companies like Total Energies address sustainability imperatives while maintaining performance specifications.

Bio-based and biodegradable fluid development accelerates in response to environmental regulations and OEM sustainability commitments. The regulatory tailwind surrounding Euro 7 emissions standards and equivalent regulations in Asia Pacific may further specify fluid requirements supporting the adoption of next-generation formulations.

Category-wise Analysis

Product Type Insights

Battery Thermal Management Fluids (TMFs) represent the leading product segment, capturing approximately 42% market share in 2025, driven by the fundamental criticality of battery temperature regulation to EV performance, range, safety, and longevity. Tesla, BYD, and other leading EV manufacturers have standardized on sophisticated liquid cooling systems, with direct immersion cooling increasingly replacing traditional indirect cooling architectures.

The development of advanced TMF formulations by Shell, ExxonMobil, Lubrizol, and Total Energies demonstrates market recognition of TMF centrality to overall vehicle efficiency. As EV production scales from millions to tens of millions of units annually, TMF demand grows proportionally.

Furthermore, the aftermarket service fill opportunity for TMF replacement (estimated at 7-8 years’ post-vehicle delivery) creates recurring revenue streams distinct from passenger vehicle engine oil replacement cycles.

Vehicle Type Analysis

Passenger Electric Vehicles (PEVs) encompassing both Battery Electric Cars (BEVs) and Plug-in Hybrid Electric Cars (PHEVs) dominate the market with 66% market share in 2025, reflecting the concentration of current EV sales and production within the personal mobility segment.

This leadership derives from multiple factors such as passenger vehicle production volumes dwarf commercial segments, with global light-duty vehicle production exceeding 80 million units annually versus commercial vehicle production of approximately 35 million units.

Passenger vehicle OEMs including Tesla, Volkswagen Group, BMW, Mercedes-Benz, Li Auto, NIO, and XPeng have established global EV supply chains with established lubricant supplier relationships. Passenger vehicle specifications define industry standards that subsequently cascade to commercial vehicle adoption.

Medium and heavy commercial electric vehicles (M&HCEVs), while currently representing modest volume, also exhibit accelerating adoption as battery technology improvements enable practical long-range commercial applications.

Chemistry Insights

Glycol-Based Fluids, encompassing both Polyalkylene Glycols (PAG) and aqueous ethylene/propylene glycol mixtures, capture the leading market share at approximately 38% in 2025, driven by exceptional thermal properties and widespread adoption in battery thermal management applications.

Glycol-based formulations offer superior heat capacity and thermal conductivity versus hydrocarbon basestocks, enabling efficient heat transfer from battery cells to external radiators. Polyalphaolefin (PAO) basestocks account for the second largest market share, representing the standard synthetic hydrocarbon baseline for traditional transmission fluids and motor cooling applications requiring lubrication properties combined with thermal management.

Polyol Esters (POE) derived from vegetable oils are favored for high-temperature applications and advanced immersion cooling systems due to exceptional oxidation stability and extended service life.

Silicone oils, fluorinated dielectric fluids (HFE, HFO, HFPE), and other specialty formulations represent fastest-growing segments due to their enabling advanced technologies like direct battery cell immersion cooling. The shifting chemistry mix reflects market progression from adapting conventional automotive fluids toward purpose-engineered EV formulations optimized for electrified powertrains.

Distribution Channel Insights

Original Equipment Manufacturer (OEM) channels dominate with approximately 78% market share in 2025, reflecting the fact that virtually all new electric vehicles incorporate factory-filled lubricants and thermal management fluids specified by vehicle manufacturers during assembly.

OEM relationships represent the highest-value, lowest-friction sales channel, as lubricant suppliers establish long-term agreements covering entire vehicle production runs. Major suppliers including Shell, ExxonMobil, Castrol (BP), TotalEnergies, FUCHS, and Kluber maintain dedicated OEM account relationships with leading EV manufacturers.

The Aftermarket channel, comprising independent service centers, authorized dealership service networks, and specialty EV service providers, captures the remaining 32% market share. Aftermarket growth accelerates gradually as the installed base of EVs matures and vehicles require maintenance interventions.

However, traditional aftermarket dynamics face disruption from “fill-for-life” policies, potentially creating significant aftermarket demand only after 7-8 years of vehicle operation.

Regional Insights

North America EV Lubricants Market Analysis

North America’s EV market is expanding rapidly, driving strong demand for EV-specific fluids. U.S. EV sales reached an estimated 1.6 million units in 2024, accounting for around 10% of new car sales.

Major automakers such as Tesla, GM, Ford, and Rivian continue to scale EV production. Federal incentives, including tax credits of up to USD 7,500, along with state-level policies and a fast-growing charging infrastructure exceeding 50,000 public stations, are accelerating adoption.

North American OEMs are advancing battery thermal management technologies, including immersion-cooled architectures and high-efficiency platforms, which require specialized coolants and lubricants. Key suppliers such as Shell, ExxonMobil, and Castrol maintain strong OEM partnerships.

While most EV fluids are designed for lifetime fill, which limits immediate aftermarket activity, long-term regulatory commitments like California’s 2035 zero-emission vehicle mandate continue to support substantial growth in EV lubricant demand.

Europe EV Lubricants Market Trends and Insights

Europe is one of the most mature EV markets, with the broader Europe Electric Vehicle Market projected to grow from US$ 174.2 billion in 2024 to US$ 489.3 billion by 2031, at a CAGR of 15.9%. This rapid growth is underpinned by ambitious EU decarbonization targets and strong OEM electrification strategies, with companies such as Volkswagen, BMW, and Mercedes-Benz heavily investing in EV platforms.

On the EV lubricant front, the region’s regulatory focus on sustainability is driving demand for biodegradable and circular economy aligned fluid solutions.

The majority of EV lubricant demand is generated through OEM channels, with major suppliers including Shell, TotalEnergies, FUCHS, and Klüber supporting thermal management and drivetrain fluid requirements. Europe’s well-developed service ecosystem and ageing vehicle fleet also create earlier opportunities for EV fluid replacement in the aftermarket compared to regions with newer EV parc.

Asia Pacific EV Lubricants Market Trends

Asia Pacific is the largest and fastest-growing EV lubricants market accounting for 48% share. The market is driven primarily by China, which accounted for nearly half of all new EVs sold globally in 2024.

China’s EV market surpassed 14 million cumulative EVs, supported by strong government mandates requiring increasing new-energy vehicle penetration. India is experiencing exponential EV adoption, with total EV sales approaching 2 million units in 2024, dominated by electric two-wheelers and three-wheelers and supported by rapid passenger EV growth.

Japan and South Korea continue to expand EV portfolios through hybrid, BEV, and fuel-cell models, with Hyundai-Kia and Toyota leading innovation in thermal management and energy-efficiency systems. Southeast Asia is also emerging, with Thailand exceeding 12% EV sales share in 2023 and becoming a regional manufacturing base.

Strong incentives, expanding charging networks, and tightening emissions norms continue to propel EV production and EV fluid demand across Asia Pacific.

Competitive Landscape

The EV lubricants market exhibits a moderate-to-high concentration structure, with approximately 6-8 major global suppliers controlling approximately more than 50% of market share and representing established leadership positions. Royal Dutch Shell, ExxonMobil, TotalEnergies, and BP Castrol leverage extensive R&D capabilities, global manufacturing infrastructure, and established OEM relationships accumulated over decades of traditional automotive lubricant supply.

Market dynamics increasingly emphasize R&D investment intensity, with leading players allocating significant share of R&D expenditure toward EV-focused development programs. Key differentiators include OEM approval portfolio breadth, technical specialization in specific applications, and geographic coverage.

Strategic partnerships between lubricant suppliers and automotive OEMs create competitive moats, with long-term supply agreements locking in market share and enabling suppliers to achieve scale economies.

Key Market Developments

- November 2024: Shell Lubricants announced a breakthrough in EV thermal management, introducing an immersion-cooled battery architecture that supports sub-10-minute fast charging using Shell EV-Plus Thermal Fluid formulated with PurePlus Technology. The company reports up to five times higher thermal performance compared to conventional cooling systems, enabling improved charging efficiency and extended vehicle range.

- September 2024: TotalEnergies launched its expanded Quartz EV Fluid and Hi-Perf EV Fluid series in India, targeting electric drivetrains, e-motors, and hybrid transmissions. The initiative strengthens the company’s position in one of the world’s fastest-growing EV markets and reflects rising demand for specialized fluids across both passenger and two-wheeler EV segments.

- March 2024: Gulf Oil Lubricants India entered into an exclusive partnership with Altigreen to supply custom-engineered EV fluids for electric three-wheelers and light cargo vehicles. The collaboration underscores the industry’s shift toward application-specific formulations and marks a strategic move to capture growth in India’s commercial EV segment.

Companies Covered in EV Lubricants Market

- Royal Dutch Shell Plc

- FUCHS Group

- ExxonMobil Corporation

- Kluber Lubrication

- Petronas

- Afton Chemicals

- Engineered Fluids

- M&I Materials Ltd.

- TotalEnergies SE

- Castrol Ltd

- 3M Inc.

- The Lubrizol Corporation

- BASF SE

- Valvoline Inc.

- Gulf Oil International Ltd

- BP (British Petroleum)

- Clariant AG

- Eneos Corporation

- SK Lubricants Co., Ltd.

- GS Caltex Corporation

- China National Petroleum Corporation (CNPC)

- China Petrochemical Corporation (Sinopec)

- Pentosin

- Idemitsu Kosan Co., Ltd.

Frequently Asked Questions

The global EV Lubricants Market is valued at US$ 1.9 billion in 2025 and is projected to reach US$ 6.7 billion by 2032, growing at a CAGR of 19.7%.

The EV Lubricants Market is driven by rapid electrification, regulatory mandates, rising passenger and commercial EV production, advancements in battery thermal management, emergence of immersion cooling technologies, and tightening emissions norms.

Battery Thermal Management Fluids lead the market with about 42% share in 2025 due to their critical role in maintaining EV performance, safety, and battery life.

Asia Pacific dominates the market with 48% share, driven by China’s scale, India’s fast-growing commercial EV segment, and expanding Southeast Asian manufacturing.

The biggest opportunity lies in advanced thermal management and immersion cooling technologies that support ultra-fast charging, improved range, and enhanced battery protection.

Leading players include Shell, ExxonMobil, TotalEnergies, Castrol, FUCHS, Klüber, Lubrizol, Afton, Petronas, BASF, Gulf Oil, CNPC, and Sinopec.