- Electric Mobility

- EV Fuse Market

EV Fuse Market Size, Share, and Growth Forecast, 2025 - 2032

Electric Vehicle Fuse Market by Fuse Type (High Voltage Fuses, Low Voltage Fuses, Medium Voltage Fuses), Material (Ceramic, Plastic, Glass), Voltage Rating (Up to 600V, 601V to 1000V, Above 1000V), Application (Electrical Vehicles, Battery Management Systems, Charging Stations), and Regional Analysis for 2025 - 2032

EV Fuse Market Size and Trend Analysis

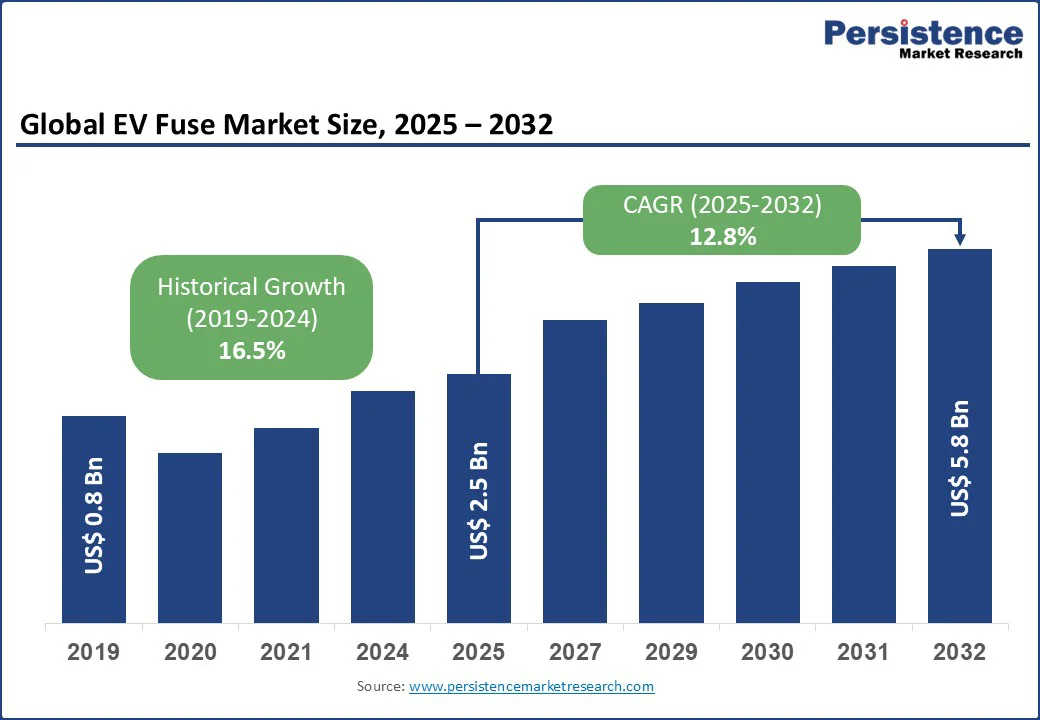

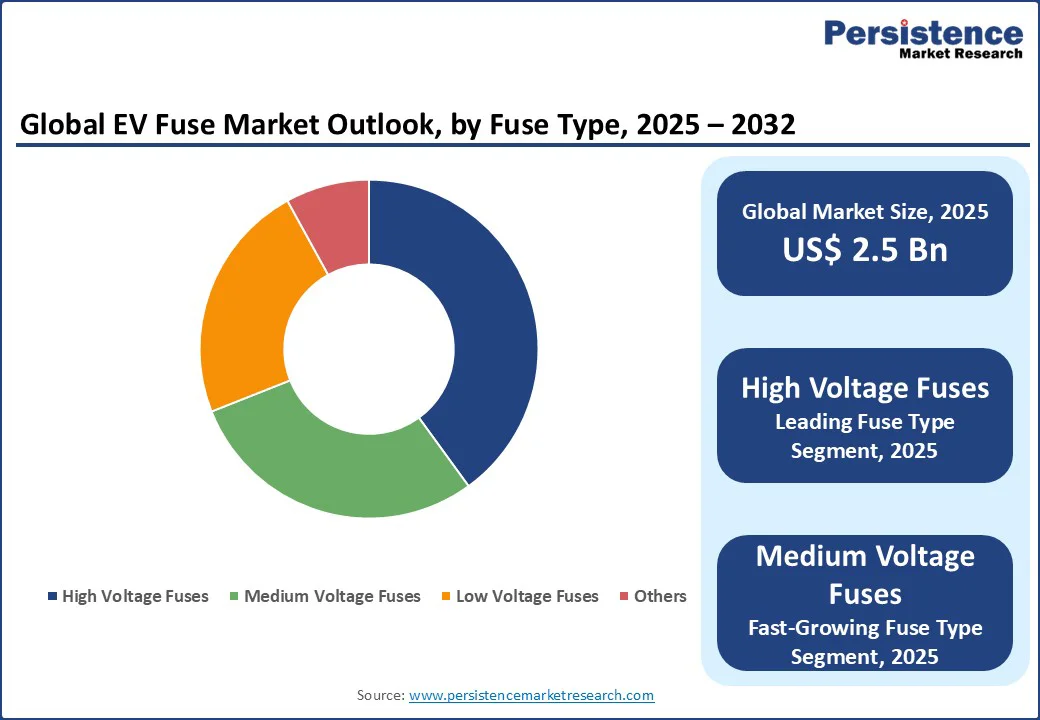

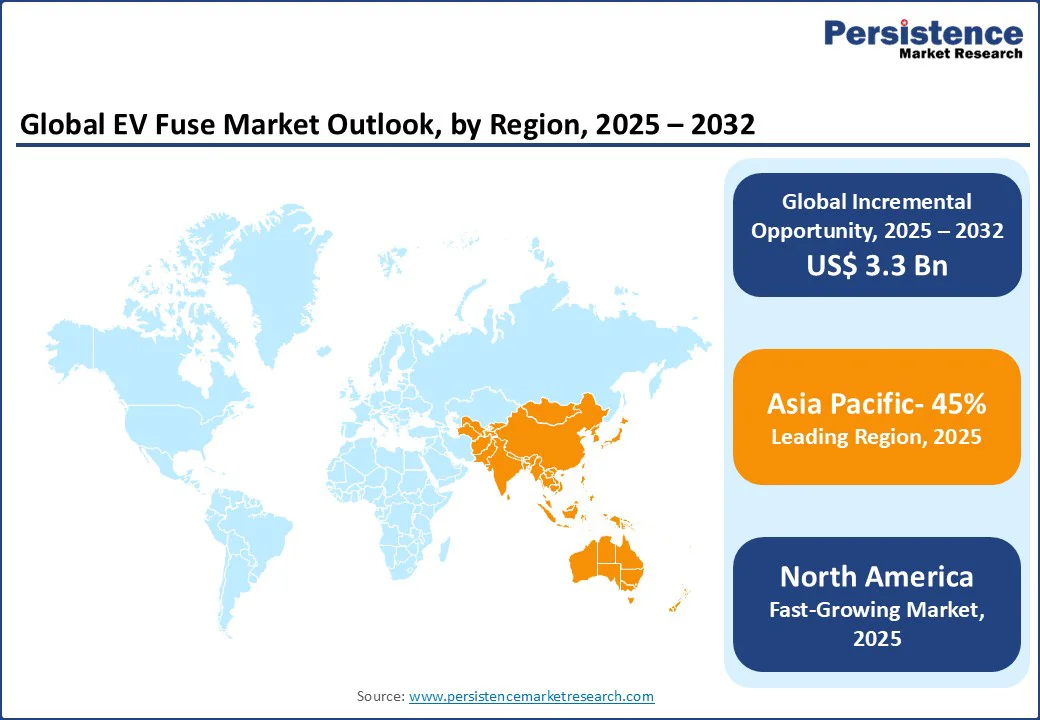

The EV fuse market is likely to be valued at US$2.5 bn in 2025 and is estimated to reach US$5.8 bn by 2032, growing at a CAGR of 12.8% during the forecast period from 2025 to 2032.

This growth is driven by the accelerating adoption of electric vehicles, coupled with large-scale investments in charging infrastructure that demand advanced protection components.

Key Market Highlights

- Leading Region: Asia Pacific held 45% of the global EV fuse market share in 2025, driven by China’s strong EV production base.

- Fastest-Growing Region: North America is the fastest-growing market in 2025, supported by EV adoption, government incentives, and expansion of charging infrastructure through programs like NEVI.

- Dominant Fuse Type: High-voltage fuses led with a 40% share, essential for safeguarding EV battery systems and power electronics.

- Leading Material: Ceramic fuses accounted for 50% market share, favored for their durability and ability to withstand high thermal stress.

- Leading Voltage Rating: Up to 600V fuses dominate with 55% share, widely used in EV battery management and auxiliary circuits.

- Leading Application: Electric vehicles represented 60% of demand in 2024, fueled by rising global EV sales.

- Key Developments: In 2024, Littelfuse launched the 871 Series Ultra-High Amperage SMD Fuse, while Eaton introduced advanced EV fuse solutions at ACT Expo.

|

Global Market Attribute |

Key Insights |

|

EV Fuse Market Size (2025E) |

US$2.5 Bn |

|

Market Value Forecast (2032F) |

US$5.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

16.5% |

Increasing deployment of high-voltage battery systems and power electronics in EVs requires reliable fuse solutions to ensure safety and performance. Government policies supporting EV manufacturing and fast-charging rollout further reinforce demand. As automakers transition to higher-capacity platforms and emerging markets embrace electrification, the EV fuse market continues to expand as a critical enabler of safe and efficient mobility.

Market Dynamics

Driver: Surge in Electric Vehicle Adoption and Charging Infrastructure

The rising adoption of electric vehicles (EVs), supported by favorable policies and subsidies, is a major growth driver for the electric vehicle fuse market. As global EV sales increase, the demand for high-voltage fuse solutions that protect power electronics and ensure reliable operation is gaining momentum.

In India, sales surpassed 1.9 million units in 2024, aided by government initiatives such as the FAME-II scheme and the PM E-DRIVE program, which focus on both EV penetration and charging network expansion. This alignment of adoption and infrastructure is creating strong opportunities for advanced fuse technologies in EV safety systems.

Government investment in charging networks further accelerates the need for robust EV fast-charging fuse solutions. For instance, India’s Ministry of Heavy Industries sanctioned more than 22,000 public charging stations under FAME-II by 2024, with a large share deployed along highways and in dense urban centers.

These installations demand reliable fuses to manage higher current loads, variable charging speeds, and fault protection. Similar initiatives, such as the U.S. National Electric Vehicle Infrastructure (NEVI) program and Europe’s Alternative Fuels Infrastructure Regulation (AFIR), are also reinforcing global EV charging infrastructure, positioning fuse technology as a critical enabler of safe and scalable electrified mobility.

Restraint: High Costs and Competition from Circuit Breakers

One of the key restraints for the electric vehicle fuse market is the relatively high cost of advanced high-voltage fuses. As EVs require specialized fuse solutions capable of handling fast-charging and elevated power demands, manufacturing complexity and use of advanced materials drive up costs compared to conventional automotive fuses. This price challenge limits large-scale adoption, especially in cost-sensitive markets, where automakers prioritize affordability and seek alternatives for power electronics protection.

Another restraint is the growing competition from circuit breakers, which offer resettable protection and longer service life. Unlike fuses that require replacement after operation, circuit breakers can be reused, making them attractive for EV charging infrastructure and battery management systems. This substitution risk poses a challenge for the electric vehicle fuse market, potentially slowing fuse adoption in specific high-performance EV applications.

Opportunity: Smart Fuse Technologies and Emerging Markets

The emergence of smart fuse technologies presents a strong growth opportunity for the electric vehicle fuse market. Unlike conventional fuses, smart fuses integrate monitoring, diagnostics, and predictive maintenance features that enhance EV safety and efficiency.

These intelligent fuse solutions can detect overcurrent risks, provide real-time data, and support advanced battery management systems. As EVs become increasingly software-driven and connected, demand for such next-generation fuse solutions is expected to accelerate, particularly in premium electric vehicles and fast-charging applications.

Emerging markets also offer significant potential for EV fuse adoption. Countries across the Asia Pacific, Latin America, and Africa are rapidly scaling EV adoption through policy support and infrastructure investment. As these regions expand public charging networks and local EV manufacturing, the need for high-voltage and smart fuse solutions will rise. This creates long-term opportunities for manufacturers to tap into untapped geographies and strengthen their presence in the global electric vehicle fuse market.

Category-wise Insights

Fuse Type Insights

High-voltage fuses continue to dominate the electric vehicle fuse market, holding around 40% share in 2025. Their leadership is attributed to their critical role in safeguarding EV battery packs, inverters, and power electronics from overcurrent risks. With most modern EVs operating on systems above 400V, manufacturers are increasingly prioritizing high-voltage fuse integration to ensure safety, reliability, and compliance with stringent automotive standards. In 2024, nearly 65% of EV manufacturers incorporated these fuses into their designs, reinforcing their position as the preferred protection solution.

Medium-voltage fuses are emerging as the fastest-growing segment in the EV fuse market. Their rapid adoption is largely driven by expanding EV charging infrastructure, particularly fast-charging stations operating between 400-1000V. In 2024, installations of medium-voltage fuses in charging facilities grew by 25%, reflecting their growing importance in enabling safe, efficient, and reliable power delivery. As charging networks expand globally, medium-voltage fuses are expected to capture a larger share of the EV fuse market, complementing the dominance of high-voltage solutions.

Material Insights

Ceramic fuses led the electric vehicle fuse market with around 50% share in 2025, maintaining their dominance due to superior thermal resistance and long-term durability. These characteristics make them the preferred choice for protecting EV battery systems and high-power electronics. In 2024, nearly 70% of high-voltage fuses were manufactured using ceramic materials, as they can reliably withstand high currents and extreme operating conditions, ensuring safety and performance in modern EV architectures.

Plastic fuses represent the fastest-growing segment, driven by their lightweight design and cost-effectiveness. Their adoption is particularly strong in price-sensitive markets and low-cost EV models. In 2024, plastic fuses saw nearly 20% growth in adoption, reflecting their increasing importance as automakers seek affordable protection solutions without compromising safety. As EV penetration deepens in emerging economies, plastic fuses are expected to gain wider acceptance, complementing the established role of ceramic fuses.

Voltage Rating Insights

Fuses rated up to 600V dominate the electric vehicle fuse market, holding about 55% share in 2025. Their widespread use in EV battery management systems, auxiliary circuits, and onboard electronics makes them the most common protection solution. In 2024, nearly 60% of EVs integrated up to 600V fuses, reflecting their cost-effectiveness and ability to deliver reliable performance in mainstream electric cars. Their balance of affordability and safety continues to drive strong adoption across mass-market EV segments.

Fuses in the 601V to 1000V range represent the fastest-growing segment, supported by the rapid expansion of EV fast-charging infrastructure. In 2024, installations of these fuses in high-power charging stations grew by 30%, underscoring their critical role in handling higher voltages and faster charging cycles. As automakers introduce advanced EV platforms with higher energy requirements, demand for 601V to 1000V fuses is expected to accelerate, complementing the dominance of up to 600V solutions.

Application Insights

Electric vehicles remain the leading application segment in the electric vehicle fuse market, accounting for about 60% share in 2025. Rising global EV sales and the increasing need for reliable circuit protection across battery systems, inverters, and power electronics drive this dominance. In 2024, nearly 80% of EV battery systems incorporated fuses to safeguard against overcurrent risks, underscoring their critical role in enhancing safety, reliability, and overall vehicle performance.

Charging stations represent the fastest-growing application for EV fuses, supported by the rapid rollout of public charging infrastructure worldwide. In 2024 alone, around 2 million new charging points were deployed, particularly across Europe and Asia, to meet surging EV demand. These installations require advanced fuse solutions to ensure grid stability, manage high current loads, and maintain safe, uninterrupted power delivery, making charging stations a key driver of future market expansion.

Regional Insights

North America EV Fuse Market Trends

North America is emerging as the fastest-growing region in the electric vehicle fuse market in 2025, driven by strong EV adoption, expanding charging infrastructure, and supportive government policies. The rollout of the National Electric Vehicle Infrastructure (NEVI) program in the U.S. is accelerating the installation of fast-charging stations, boosting demand for high-voltage fuse solutions that ensure safety and reliability.

In addition, leading automakers are scaling up EV production, creating greater need for advanced circuit protection in battery systems and power electronics. With rising investment in electrification, North America is set to play a pivotal role in shaping the EV fuse industry.

Europe EV Fuse Market Trends

Europe holds a significant share of the electric vehicle fuse market in 2025, supported by strong EV penetration, strict emission regulations, and rapid expansion of charging networks. The region’s commitment to carbon neutrality and adoption of the Alternative Fuels Infrastructure Regulation (AFIR) are driving large-scale deployment of fast-charging stations, which require reliable high-voltage fuse solutions.

Major automotive hubs such as Germany, France, and the UK are leading in EV production, further increasing demand for advanced fuse technologies to safeguard battery systems and power electronics. This strong regulatory and industrial foundation ensures Europe’s continued dominance in the EV fuse industry.

Asia Pacific EV Fuse Market Trends

Asia Pacific dominates the electric vehicle fuse market in 2025, accounting for around 45% share, driven by the region’s rapid EV adoption, large-scale battery manufacturing, and government-led electrification programs. China remains the global leader in EV production and charging infrastructure, creating massive demand for high-voltage fuses in battery systems and fast-charging networks.

Countries such as Japan, South Korea, and India are accelerating investments in EV manufacturing and public charging deployment, further strengthening the EV fuse market outlook. The region’s cost-competitive manufacturing ecosystem and strong supply chain integration make Asia Pacific the central hub for EV fuse production and consumption, reinforcing its leadership position.

Competitive Landscape

The global EV fuse market in 2025 is moderately consolidated, with leading manufacturers holding more than 70% of the global share. Competition centers on the development of high-voltage fuses, fast-charging fuse solutions, and smart fuse technologies that enhance battery safety and power electronics protection.

Companies are focusing on strategic collaborations with automakers and investments in EV charging infrastructure to strengthen market presence. Growing demand across Asia Pacific and emerging economies is driving further competition, encouraging manufacturers to scale production and deliver cost-efficient fuse solutions.

Key Developments

- October 2024: Littelfuse introduced the 871 Series Ultra-High Amperage SMD Fuse with 150A and 200A ratings for EV applications, designed to reduce the need for multiple parallel fuses.

- May 2024: Eaton unveiled a new portfolio of high-power EV fuses at ACT Expo 2024, engineered to enhance protection in commercial electric vehicles with ratings up to 1,400A and 900V.

Companies Covered in EV Fuse Market

- Littelfuse

- Bel Fuse

- Mersen

- Honeywell

- Mitsubishi Electric

- Fuseco

- TE Connectivity

- Eaton

- General Electric

- SIBA

- Phoenix Contact

- ABB

- Schneider Electric

- Siemens

- Rockwell Automation

- Others

Frequently Asked Questions

The EV fuse market is projected to reach US$2.5 bn in 2025, driven by EV adoption and charging infrastructure growth.

Rising EV sales, charging station expansion, and smart fuse innovations fuel market growth.

The EV fuse market will grow from US$2.5 bn in 2025 to US$5.8 bn by 2032, with a CAGR of 12.8%.

Smart fuse technologies and emerging market expansion drive growth in EV and charging applications.

Leading players include Littelfuse, Eaton, Mersen, ABB, and Schneider Electric.