- Beverages

- Europe Sugar-Free Carbonated Drinks Market

Europe Sugar-Free Carbonated Drinks Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Europe Sugar-Free Carbonated Drinks Market by Product Type (Soft Drinks, Sports Drinks, Carbonated Water, Energy Drinks), Flavor (Lime, Cola, Lemonade, Orange, Others), Sales Channel (HoReCa, Convenience Stores, Hypermarkets/Supermarkets, E-commerce), and country wise analysis for 2026 to 2033

Europe Sugar-Free Carbonated Drinks Market Size and Share Analysis

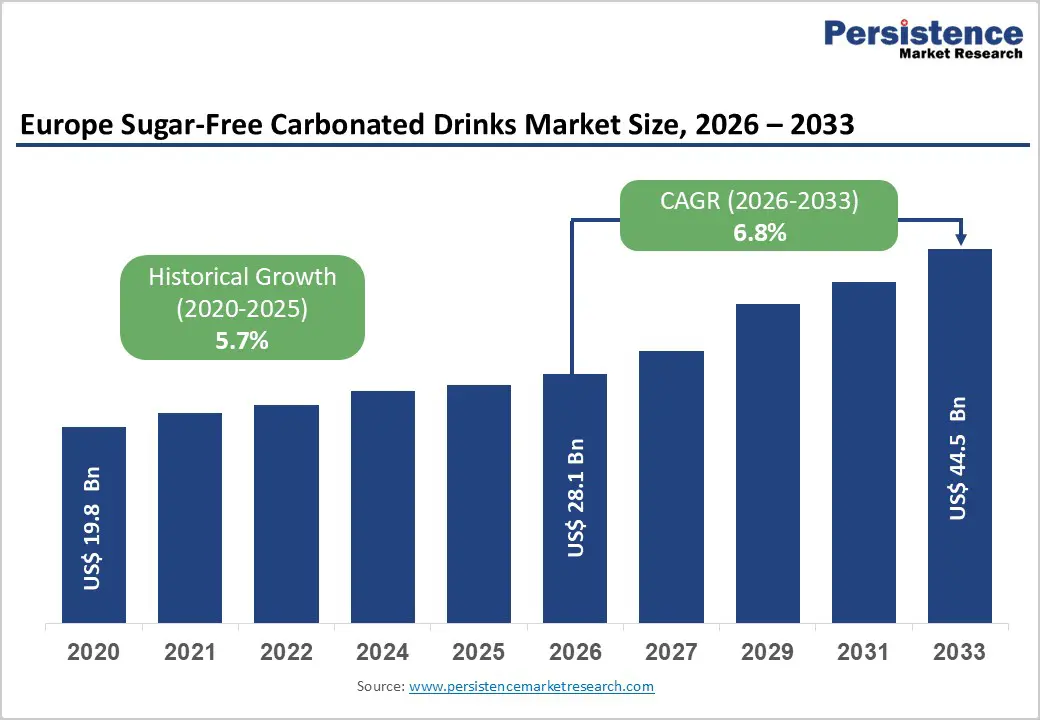

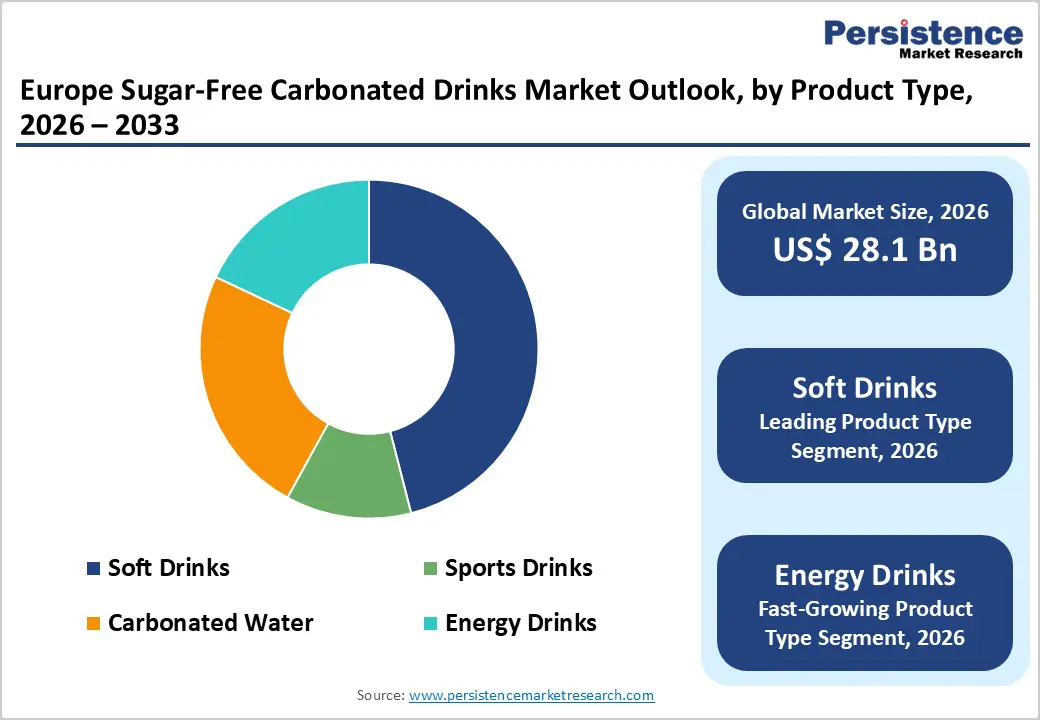

The Europe Sugar-Free Carbonated Drinks Market size is expected to be valued at US$ 28.1 billion in 2026 and projected to reach US$ 44.5 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2033

Europe’s sugar-free carbonated drinks market is shifting from diet substitutes to lifestyle beverages, driven by wellness-first consumption, clean-label expectations, and flavor-led innovation. Health, functionality, and indulgence are no longer trade-offs but coexisting demand drivers shaping category growth.

Key Industry Highlights

- Leading Country: U.K., accounting for the largest share of sugar-free carbonated drink consumption, driven by high health awareness, sugar levy impact, strong clean-label adoption, and rapid premiumization of zero-sugar sodas.

- Dominant Product Type Segment: Soft Drinks, holding around 46% market share, supported by strong brand loyalty toward zero-sugar colas and citrus sodas, frequent limited-edition launches, and aggressive reformulation by global beverage leaders.

- Fastest-Growing Sales Channel: Online Retail, expanding rapidly due to subscription models, bulk purchasing convenience, and growing preference for digital transparency around ingredients and functional benefits.

- Market Drivers: Strong consumer shift toward reduced-sugar and no-sugar beverages, fueled by rising concern over metabolic health, diabetes risk, dental erosion, and the growing rejection of liquid calories in daily diets.

- Market Restraints: Persistent taste and aftertaste challenges compared to full-sugar drinks, as high-intensity sweeteners often amplify bitterness and acidity, limiting adoption among flavor-first consumers.

- Key Opportunities: Targeting health-conscious and weight-management consumers through functional sugar-free carbonated drinks incorporating prebiotics, adaptogens, nootropics, and metabolism-supporting ingredients.

- Key Developments: In April 2025, Pepsi expanded its zero-sugar portfolio with new flavors and introduced the world’s first AI-designed sweetener system to enhance taste without caloric trade-offs; In February 2025, CANS entered the UK market as an unsweetened carbonated soft drink brand, targeting ingredient-minimalist and sugar-averse adult consumers.

| Key Insights | Details |

|---|---|

| Europe Sugar-Free Carbonated Drinks Market Size (2026E) | US$ 28.1 Bn |

| Market Value Forecast (2033F) | US$ 44.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.7% |

Market Dynamics

Driver – Strong consumer shift toward reduced-sugar and no-sugar beverages

The thirst for wellness has transformed carbonated water from a simple indulgence into a functional pillar of the modern European lifestyle. Individuals across the continent are increasingly scrutinizing labels, seeking to distance themselves from the metabolic risks associated with heavy glucose consumption.

This transition is fueled by a growing realization that liquid calories contribute significantly to lifestyle-related conditions like diabetes and dental erosion. Consequently, the preference for vibrant, fizzy experiences that align with metabolic health is no longer a niche trend but a dominant market force.

Innovative product developers are responding by leveraging plant-based sweetness to maintain the sensory appeal of traditional sodas. In the United States, a prominent industry example is the Coca-Cola Company's massive push for Coke Zero Sugar, which utilized an advanced AI-driven global campaign in 2024 to promote Taste That Speaks For Itself. By highlighting the flavor parity between full-sugar and zero-sugar variants, brands are successfully migrating loyal customers toward healthier alternatives. This strategic alignment ensures that taste remains the primary hook while health-conscious formulations drive sustained volume growth.

Restraints – Taste and aftertaste challenges versus full-sugar drinks

Replicating the complex mouthfeel and satisfying hit of sucrose remains a significant hurdle for beverage scientists. While natural and high-intensity sweeteners provide the necessary sweetness, they often leave lingering metallic or bitter notes that can alienate traditional soda drinkers.

The astringency and acidity typically masked by sugar become more pronounced in diet versions, sometimes exceeding the allowable sensory limit for casual consumers. These chemical discrepancies create a taste gap that prevents full adoption among those who prioritize flavor above all else.

Advanced formulation techniques, such as the use of condensed phosphates, are being patented to mitigate these undesired aftertastes and provide a rounder flavor profile.

Manufacturers must carefully balance these additives to avoid further complicating the ingredient list, which could conflict with clean label demands. Until the sensory experience perfectly mirrors the indulgence of real sugar, a portion of the population will remain hesitant to switch. This friction necessitates constant R&D investment to ensure that zero-sugar options provide a refreshing, clean finish without compromise.

Opportunity – Targeting health-conscious and weight-management consumers

Europe's expanding demographic of calorie-trackers presents a goldmine for established beverage giants and agile startups alike. As obesity rates rise and fitness culture becomes more mainstream, consumers are actively hunting for guilt-free hydration that supports weight-loss efficacy.

The integration of functional ingredients such as nootropics for mental focus or adaptogens like ashwagandha allows brands to transcend the diet soda label. This shift creates a multifaceted opportunity to market drinks that provide metabolic support while satisfying the craving for carbonation.

Small-batch startups are particularly well-positioned to exploit this by launching niche, hyper-targeted products like prebiotic-infused sparkling tonics that aid gut health. By focusing on satiety-driving fibers like inulin or metabolism-boosting green tea extracts, new players can build dedicated followings among the Gen Z and Millennial cohorts.

These consumers are often willing to pay a premium for transparency and functional benefits that simplify their weight-management journeys. Strategic partnerships with fitness influencers and gym chains further amplify this reach, turning a standard soft drink into a vital component of a wellness routine.

Category-wise Analysis

By Product Type, Soft Drinks dominate the Europe Sugar-Free Carbonated Drinks market

Soft Drinks hold approx. 46% market share as of 2025, firmly anchoring the Europe Sugar-Free Carbonated Drinks market through their universal appeal and decades of brand loyalty. Consumers frequently turn to sugar-free colas, orange sodas, and lemon-lime variants as their primary daily refreshment, bolstered by aggressive reformulation efforts from major players.

These products are often the first point of entry for people looking to reduce sugar without abandoning familiar flavors. The category remains resilient as legacy brands introduce limited-edition zero versions to keep the portfolio exciting and relevant.

Other segments like Carbonated Water, Energy Drinks, and Sports Drinks are rapidly evolving to capture specific functional needs beyond simple thirst quenching. Energy drinks are witnessing a surge in zero-sugar innovation to cater to gamers and office workers seeking mental alertness without a sugar crash.

Sports drinks are increasingly valued for electrolyte replenishment among the active population, while carbonated water gains ground as a pure, additive-free alternative to soda. Together, these subcategories complement the core soft drink market by offering a fizzy solution for every hour of the day.

By Sales Channel, online retail is expected to show lucrative growth during forecast period

Online retail is expected to grow at CAGR of 7.9% as digital platforms redefine how European households replenish their beverage stocks. The sheer convenience of bulk ordering and direct-to-door delivery removes the physical burden of transporting heavy cases of carbonated water or soda.

Digital natives are increasingly using subscription-based models to ensure a constant supply of their favorite sugar-free labels, bypassing traditional store visits entirely. This shift allows brands to showcase transparency by providing detailed digital ingredient lists and functional benefits that might be missed on a crowded physical shelf.

The broader retail landscape remains diverse, with Hypermarkets and Supermarkets continuing to provide the massive variety and promotional pricing that draws in family shoppers. Meanwhile, Convenience Stores and the HoReCa (Hotel, Restaurant, and Café) sector act as vital touchpoints for immediate, on-the-go consumption and social dining.

While physical stores maintain a stronghold for impulse buys, the analytical power of e-commerce allows for personalized marketing that drives higher frequency purchases. This digital expansion is particularly lucrative for emerging brands that can use social media to drive traffic directly to their own online storefronts.

Region-wise Insights

U.K. Sugar-Free Carbonated Drinks Market Trends

The British aisles are undergoing a radical transformation as the food as medicine ethos takes root among health-aware shoppers. There is a pronounced move away from artificial sweeteners, with many consumers now viewing them as a greater health foe than sugar itself.

This has triggered a latest trend of naturally sweetened beverages that use botanical extracts or fruit juices to achieve a less sweet, more sophisticated flavor profile. Additionally, the alcohol moderation movement is driving demand for alcohol-inspired flavors like sparkling elderflower or ginger blends that serve as elegant social replacements.

Premiumization is another key driver, with younger demographics gravitating toward artisanal, small-batch craft sodas that emphasize ethical sourcing. Many brands are now celebrating the absence of specific additives, using clean-label claims as a primary marketing tool to assuage concerns over ultra-processed foods. The market remains incredibly dynamic as companies like Carlsberg Britvic expand their portfolios with creative new zero-sugar flavors like Strawberries 'N' Cream. This relentless innovation ensures that the U.K. remains a global benchmark for sugar-free beverage evolution.

Germany Sugar-Free Carbonated Drinks Market Trends

Germans are increasingly harmonizing their desire for indulgence with a pragmatic better-for-you lifestyle, leading to a steady rise in diet and light beverage consumption. A fascinating local trend is the revitalization of nostalgic childhood flavors such as the culturally beloved Apfelschorle (apple juice with sparkling water) through modern, sugar-reduced formulations.

Consumers in Germany prioritize safe, natural ingredients and are particularly attracted to carbonated drinks that offer added functional benefits like energizing or hydrating properties. This focus on functionality is especially prevalent among Baby Boomers, who seek beverages that support sustainable hydration.

The market is also witnessing a shift toward sophisticated, less-sweet propositions that tap into the growing alcohol moderation movement. While fruit flavors appear in roughly 70% of new launches, there is an emerging interest in brown flavors like chocolate or vanilla, particularly in the iced coffee and tea subcategories.

Despite this interest in reduction, only a fraction of new German products currently highlight reduced sugar claims on their packaging, leaving a massive opening for brands to lead with clearer health messaging. This gap represents a significant opportunity for innovation in craveable, low-sugar formulations that avoid the common pitfalls of a bitter aftertaste.

Market Competitive Landscape

The European sugar-free carbonated drinks landscape is moderately consolidated, with massive global entities like PepsiCo, The Coca-Cola Company, and Red Bull leveraging their deep distribution networks. These industry leaders are currently fixated on clean-label transitions, aggressively swapping artificial sweeteners for natural alternatives like stevia to meet evolving regulatory and consumer standards.

Flavor innovation has become a frontline strategy, with brands launching limited-edition, disruptive tastes to maintain interest among younger demographics. Furthermore, there is a systemic push toward sustainability, with high-detail focus on recyclable aluminum cans and glass bottles to reduce environmental impact.

Beyond product formulation, companies are increasingly targeting the D2C market to build deeper emotional connections with their audience. This allow for personalized shopping experiences and the gathering of first-party data to refine future R&D cycles.

Government regulations including national sugar levies continue to force a rapid pace of reformulation, making agility a key competitive differentiator. By blending nostalgic appeal with modern, functional benefits, these top-tier players are successfully defending their market share against a rising wave of health-focused startups. This competition is ultimately accelerating the transition toward a more diverse and transparent beverage ecosystem across the continent.

Key Developments:

- In April 2025, Pepsi expands its zero-sugar portfolio, launching two new flavours while debuting the world’s first AI-designed Sweetest, signaling a shift toward tech-enabled flavour optimization without caloric trade-offs.

- In February 2025, CANS enters the UK market, positioning itself as an unsweetened, carbonated soft drink brand, directly targeting sugar-averse and ingredient-minimalist consumers seeking adult refreshment alternatives.

- In February 2025, Fanta UK rolls out three Zero Sugar flavours, reinforcing Coca-Cola’s aggressive defence strategy in the zero-sugar segment through flavour variety rather than reformulation alone.

Companies Covered in Europe Sugar-Free Carbonated Drinks Market

- The Coca Cola Company

- PepsiCo, Inc.

- Nestlé

- Danone

- Red Bull

- Nichols plc

- A.G. Barr p.l.c

- Lucozade

- Monster Energy Company

- SANPELLEGRINO

- Others

Frequently Asked Questions

The Europe Sugar-Free Carbonated Drinks market is projected to be valued at US$ 28.1 Bn in 2026.

Strong consumer shift toward reduced-sugar and no-sugar beverages drives the demand for Europe Sugar-Free Carbonated Drinks Market.

The Europe Sugar-Free Carbonated Drinks market is poised to witness a CAGR of 6.8% between 2026 and 2033

Targeting health-conscious and weight-management consumers is the key market opportunity

Major players in the Europe Sugar-Free Carbonated Drinks Market include The Coca Cola Company, PepsiCo, Inc., Nestlé, Red Bull, Monster Energy Company, SANPELLEGRINO, and others