- Electric Mobility

- Europe Electric Kick Scooter Market

Europe Electric Kick Scooter Market Size, Share, Trends, Growth, Regional Forecasts 2026 - 2033

Europe Electric Kick Scooter Market by Product Type (Two-Wheeled, Three-Wheeled), Battery Type (Lithium-ion Battery, Lead-acid Battery), Range (Less than 25 km, 25-50 km, Above 50 km), Application (Personal Use, Shared Mobility / Rental Services), and Regional Analysis for 2026 - 2033

Europe Electric Kick Scooter Market Share and Trends Analysis

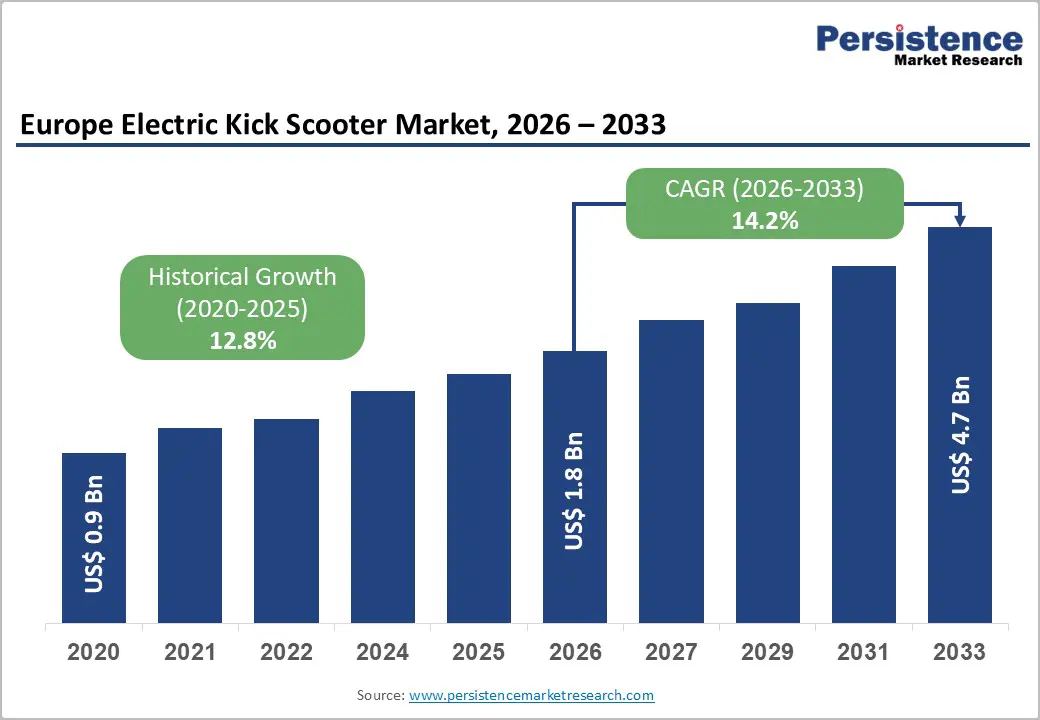

The Europe electric kick scooter market size is projected at US$1.8 Bn in 2026 and is projected to reach US$4.7 Bn by 2033, growing at a CAGR of 14.2% between 2026 and 2033.

Rising urbanization, congestion, and municipal climate goals are driving accelerated adoption of electric micromobility across European cities, including electric kick scooters. EU and national-level decarbonization frameworks promote low-emission transport and encourage operators and OEMs to invest in shared and personal e-scooters. Battery cost declines and enhanced lithium-ion energy densities further improve ownership economics and fleet profitability in both mature and emerging European markets.

Key Industry Highlights:

- Europe electric kick scooter market is poised for robust growth, expanding from US$1.84 Bn in 2026 to US$4.65 Bn by 2033, registering a CAGR of 14.2%, supported by rising urban mobility demand and regulatory support for micro-mobility solutions.

- Two-wheeled scooters dominate the market with ~90.3% share, reflecting their widespread adoption in urban commuting, while three-wheeled models are witnessing accelerated uptake, growing at approximately 16.1% CAGR due to increasing demand for enhanced stability and accessibility.

- Lithium-ion battery-powered scooters lead with ~71.8% share and are projected to grow at 15.8% CAGR, significantly outperforming lead-acid variants owing to superior energy efficiency, longer lifecycle, and declining battery costs.

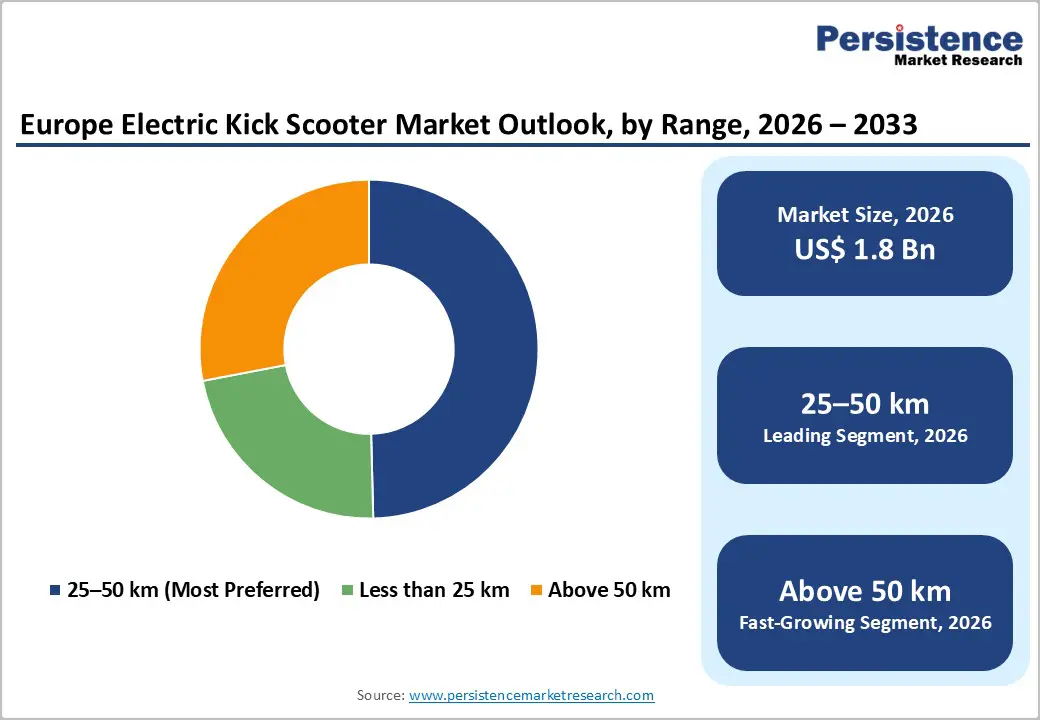

- The 25-50 km range segment accounts for ~49.6% of total demand, positioning it as the optimal balance between cost and performance, whereas >50 km range scooters are emerging as the fastest-growing segment, driven by premiumization and extended-use applications.

- Personal-use applications contribute ~64.3% of total revenue, underpinned by increasing consumer preference for convenient last-mile connectivity, while shared mobility and rental services are expanding at 16.3% CAGR, supported by fleet deployments across major European cities.

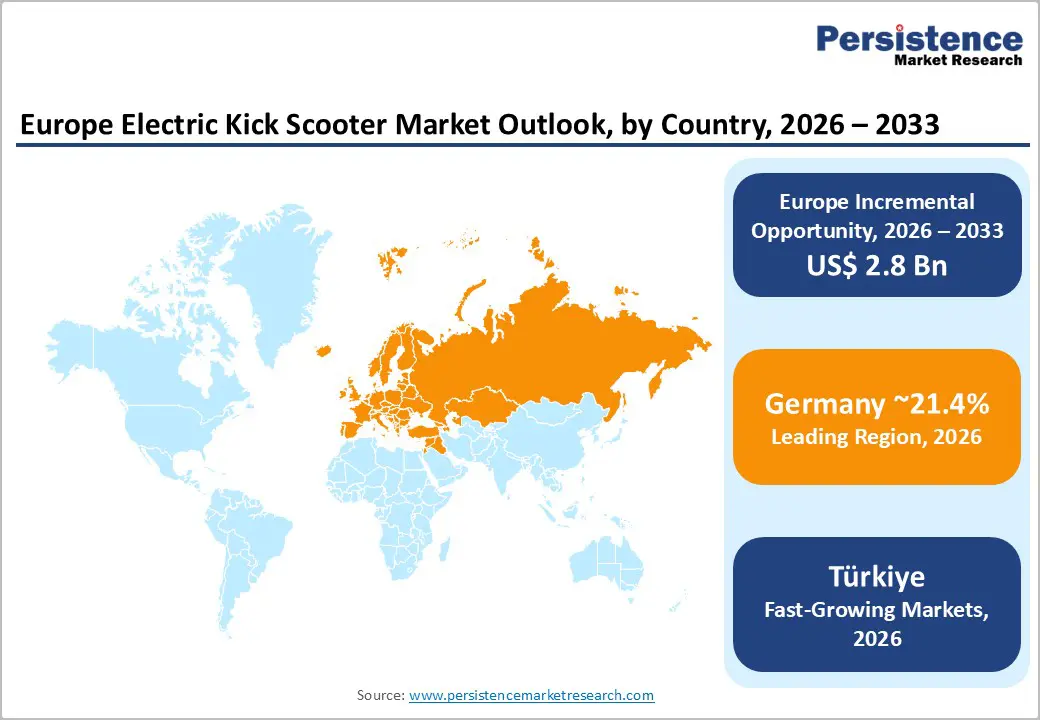

- Germany and France collectively account for over 36% of regional revenue, establishing them as key demand centers, while high-growth markets such as France 14.1% CAGR and Türkiye 15.8% CAGR are driving incremental expansion.

- The competitive landscape is undergoing strategic consolidation and technological advancement, highlighted by developments such as the Tier-Dott integration and increasing focus on high-performance lithium-ion scooters, reshaping both market competition and product innovation.

| Key Insights | Details |

|---|---|

| Europe Electric Kick Scooter Market Size (2026E) | US$ 1.8 billion |

| Market Value Forecast (2033F) | US$ 4.7 billion |

| Projected Growth CAGR (2026 - 2033) | 14.2% |

| Historical Market Growth (2020 - 2025) | 12.8% |

Market Dynamics Analysis

Drivers - Urbanization, congestion, and sustainable mobility policies

Rapid urbanization and congestion are pushing European cities to adopt low-emission micromobility solutions as part of broader climate and transport strategies. The EU targets at least a 55% reduction in greenhouse gas emissions by 2030 versus 1990 levels, prompting local authorities to prioritize cycling lanes, low-emission zones, and multimodal hubs. Electric kick scooters provide flexible, low-footprint last-mile connectivity aligned with these policies. Germany, France, the Netherlands, and the Nordics are leading adopters, with Europe’s broader electric scooter segment expected to grow at around 12-15% CAGR through 2030, providing a strong macro tailwind for kick scooters.

Growth of shared micromobility ecosystems

Shared electric kick scooters have become an integral part of urban mobility ecosystems in many European cities, offering pay-per-ride access without ownership barriers. Operators deploy tens of thousands of units, particularly in Germany, France, Spain, and the Benelux region, to complement public transit and reduce reliance on private cars. Europe’s electric scooter/sharing market has been growing at double-digit rates, supported by municipal tenders and concessions. While regulatory scrutiny has increased, consolidation and more disciplined deployment strategies are improving fleet utilization and financial sustainability, supporting continued demand for robust, longer-range kick scooters.

Restraints - Regulatory fragmentation and operating restrictions

Regulation of electric kick scooters remains fragmented across Europe, with differing rules on speed limits, helmet use, sidewalk riding, parking, and shared fleet caps. Paris’s 2023 decision to remove shared e-scooters underscores the risk that local political pressure and safety concerns can sharply reduce fleet sizes or eliminate markets. Some countries have introduced stricter requirements, including mandatory insurance and registration, adding compliance costs and uncertainty. This regulatory variability complicates cross-country fleet strategies and can slow deployment, especially in cities where public acceptance is contested.

Safety, infrastructure gaps, and public perception

Accident reports and concerns around unsafe riding, sidewalk clutter, and inadequate cycling infrastructure pose challenges to sustained growth. In the absence of dedicated lanes and parking zones, conflicts with pedestrians can intensify, prompting calls for bans or stricter controls. These issues translate into risk premiums for insurers and additional training or infrastructure investments for operators and municipalities. If not addressed, they can limit adoption among risk-averse users and restrict operating permits, particularly in historic city centers and heavily pedestrianized districts.

Opportunities - Growth of high-range (>50 km) premium and commuter segments

As commuting distances and expectations for reliability increase, demand for higher-range (above 50 km) electric kick scooters is rising among daily commuters and prosumers. Premium models with improved suspension, larger batteries, and robust frames support longer trips, potentially replacing portions of car use in urban and suburban corridors. Assuming high-range scooters expand from a niche base to 20-25% of Europe’s market by 2033, they could represent US$0.9-1.1 Bn in annual revenues, benefiting manufacturers offering differentiated performance and safety features.

Localization and manufacturing opportunities in emerging European markets

Emerging manufacturing hubs in Eastern Europe and Türkiye offer cost-competitive assembly bases for electric kick scooters targeting both local and Western European demand. Nearshoring trends, driven by supply chain resilience concerns, support investments in regional production of frames, batteries, and electronics. Türkiye, in particular, is projected to grow its e-mobility sector at high double-digit rates, providing opportunities for OEM partnerships and private-label manufacturing. This could create a sizeable supply-side opportunity, potentially adding several hundred million dollars in export-oriented production value by the early 2030s.

Category-wise Analysis

Product Type Insights

Two-wheeled electric kick scooters are the leading product type, accounting for approximately 90.3% of the Europe market, reflecting their familiarity, maneuverability, and broad suitability for adults and older youths across commuting and leisure use cases. They dominate both personal ownership and shared fleets due to standardized designs, lower per-unit manufacturing costs, and an established supply chain. Their compact footprint and compatibility with existing bike lanes make them the default choice in most cities, supporting scale and network effects across Europe.

Three-wheeled electric kick scooters represent the fastest-growing product type, with an estimated 16.1% CAGR over 2026-2033 as demand grows among older users, families, and safety-conscious riders. Enhanced stability and load-carrying capability support adoption in niche personal mobility and light cargo segments, while municipalities exploring inclusive micromobility pilots may increasingly test three-wheeled formats.

Battery Type Insights

Lithium-ion battery-powered electric kick scooters hold the leading position with around 71.8% share of the Europe market, supported by their superior energy density, lighter weight, and longer cycle life compared with lead-acid alternatives. Market data show lithium-ion as both the largest and fastest-growing battery segment across Europe’s wider electric scooter category, underpinning most modern models. Their faster charging capability and compatibility with swappable pack concepts also reinforce their dominance in shared fleets and higher-range consumer scooters.

Lithium-ion battery scooters are also the fastest-growing battery segment, expanding at roughly 15.8% CAGR during 2026-2033 as OEMs phase out lead-acid technologies. Declining pack prices and robust EU focus on battery sustainability and recycling support widespread adoption, while improved safety management systems address earlier concerns about thermal events.

Range Insights

The 25-50 km range category is the leading segment, representing about 49.6% of Europe’s electric kick scooter market, as it aligns well with typical urban daily travel distances and provides a practical balance between weight, cost, and performance. Many commuters need only 10-20 km per day, but appreciate buffer capacity for errands or multi-stop trips, making 25-50 km a sweet spot. Shared fleet operators also favor this range class to optimize battery leasing costs, recharging logistics, and vehicle utilization within dense service areas.

The Above 50 km range class is the fastest-growing subsegment, registering an estimated 15.6% CAGR as more users seek car-substitute options and longer-distance commuting solutions. Improvements in lithium-ion chemistry and vehicle design support extended ranges without prohibitive weight increases, enabling premium price points while expanding the addressable commuter base beyond inner-city cores.

Application Insights

Personal use dominates the Europe electric kick scooter market with a share of approximately 64.3%, reflecting strong consumer uptake for commuting, leisure, and first/last-mile journeys. Online retail channels, declining prices, and rising environmental awareness encourage households to purchase their own devices rather than rely solely on shared fleets. Personal ownership is especially prominent in suburban areas and smaller cities where shared services are less prevalent, supporting stable baseline demand across the region.

Shared mobility / rental services form the fastest-growing application, with an estimated 16.3% CAGR through 2033 as operators optimize fleets and expand into regulatory-supportive cities. Consolidation, such as major e-scooter operator mergers, and improved fleet management solutions are enhancing per-vehicle economics, which in turn drives periodic fleet refresh cycles and sustained demand for durable, connected kick scooters.

Regional Market Insights

Germany Electric Kick Scooter Market Trends

Germany holds a dominant ~21.4% share of the Europe electric kick scooter market, benefiting from a large urban population, strong purchasing power, and robust micromobility ecosystems. The country has tens of thousands of shared e-scooters in operation and active private ownership in major cities, supported by extensive cycling infrastructure and climate-oriented transport policies. Regulatory frameworks increasingly align e-scooter rules with bicycle regulations, providing clearer conditions for operators while emphasizing safety and liability standards.

Germany is expected to maintain its leadership position, with growth supported by continued smart city initiatives, public transport integration, and corporate mobility programs. Demand for higher-range and connected scooters is likely to rise, particularly among commuters in large metro areas, driving steady fleet replacement and premium segment expansion.

France Electric Kick Scooter Market Trends

France accounts for roughly 15.1% of Europe’s electric kick scooter market and is projected to grow at around 14.1% CAGR, driven by active urban mobility policies and widespread consumer adoption. While Paris removed shared e-scooters in 2023, other French cities continue to support regulated micromobility schemes, and personal ownership remains strong. National initiatives to reduce transport emissions and improve air quality underpin demand, alongside tourism-driven usage in coastal and heritage destinations.

Regulatory harmonization and clearer national guidelines on speed, parking, and insurance are fostering a more predictable operating environment outside Paris. This supports sustained investment by both domestic and international manufacturers and operators, particularly in mid-range scooters designed for daily commuting and multimodal integration.

Türkiye Electric Kick Scooter Market Trends

Türkiye is among the fastest-growing markets in Europe’s electric kick scooter segment, with an estimated 15.8% CAGR as urbanization, rising incomes, and congestion spur demand for affordable micromobility. Local assemblers and regional brands are scaling production to serve both domestic and export markets, leveraging cost advantages and a strong manufacturing base. Major cities such as Istanbul and Ankara are experimenting with shared micromobility schemes, integrating scooters with public transport corridors and digital payment systems.

Türkiye’s growth trajectory is further supported by government's interest in e-mobility industrialization and export opportunities to EU neighbors. Investments in local battery and components manufacturing could enhance the competitiveness of Turkish-produced kick scooters, while ongoing urban transport modernization creates sustained demand for both personal and shared vehicles.

Competitive Landscape

Leading players pursue innovation-focused strategies combining high-efficiency lithium-ion batteries, connected telematics, and modular designs to balance performance and cost. They differentiate through robust frames for shared fleets, premium comfort and range for personal users, and flexible financing or leasing models. Emerging business models emphasize fleet analytics, dynamic pricing, and partnerships with cities and public transport agencies to embed e-scooters into integrated mobility ecosystems.

Strategic Developments

- In January 2024, Tier Mobility and Dott advanced a merger process aimed at creating a leading European shared e-scooter operator, consolidating fleets and improving cost efficiency across several EU markets.

- In October 2024, Tier brand transition to Dott began, with all vehicles to be migrated to the Dott platform by spring 2025, streamlining operations and strengthening network coverage.

Companies Covered in Europe Electric Kick Scooter Market

- Dott

- Tier Mobility

- Lime

- Voi Technology

- Bolt

- NIU Technologies

- Segway-Ninebot

- Xiaomi

- Decathlon (Oxelo / in-house brands)

- Micro Mobility Systems AG

- Okai

- Yadea Group

- Kaabo

Frequently Asked Questions

The Europe Electric Kick Scooter Market is estimated at about US$1.8 Bn in 2026, projected to reach roughly US$4.7 Bn by 2033.

Market growth is driven by urban congestion, climate-focused mobility policies, and advances in lithium-ion and connected scooter technologies.

The Europe Electric Kick Scooter Market is expected to grow at around 14.2% CAGR between 2026 and 2033.

Key opportunities lie in shared mobility expansion, high-range premium commuter scooters, and localized manufacturing in emerging hubs such as Türkiye and Eastern Europe.

Major players include Dott, Tier Mobility, Lime, Voi Technology, Bolt, Segway-Ninebot, NIU, Xiaomi, Decathlon, Micro Mobility Systems, Okai, and Yadea.