- Beverages

- Europe Beer Adjuncts Market

Europe Beer Adjuncts Market Size, Share, and Growth Forecast 2026 - 2033

Europe Beer Adjuncts Market by Beer Adjunct Type (Unmalted Grain: Unmalted Corn, Unmalted Rice, Others; Sugar; Cassava; Potatoes; Others), Form (Dry, Liquid), Country-Level Analysis, 2026 - 2033

Europe Beer Adjuncts Market Size and Trend Analysis

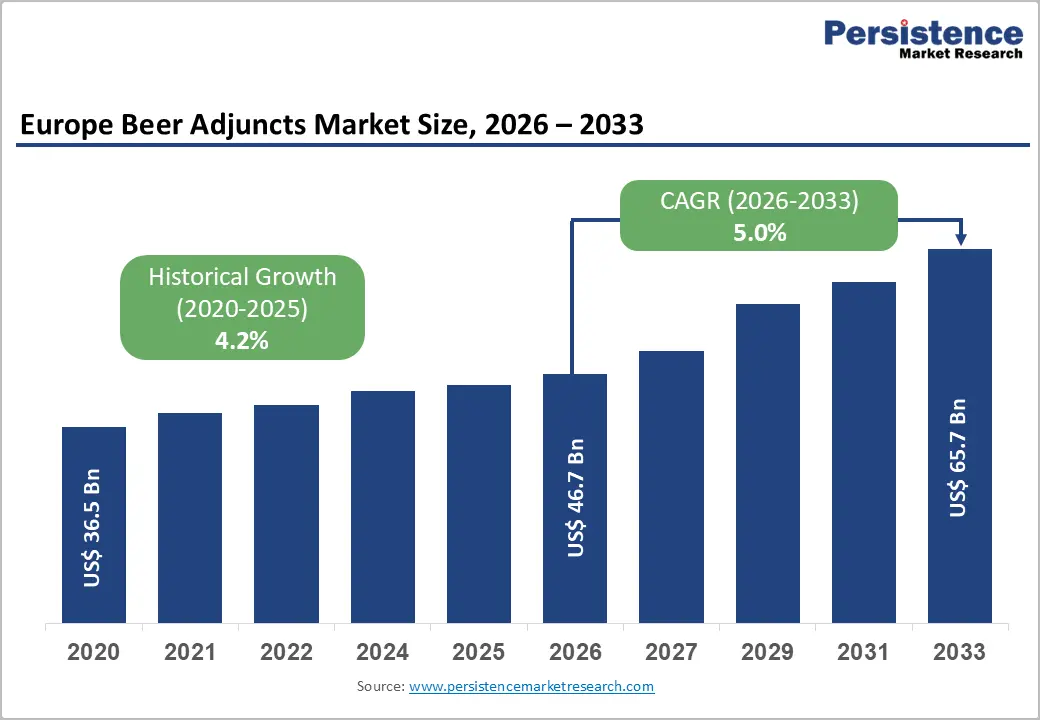

Europe beer adjuncts market size is expected to be valued at US$ 46.7 billion in 2026 and projected to reach US$ 65.7 billion by 2033, growing at a CAGR of 5.0% between 2026 and 2033.

The beer adjuncts market is on a steady upward trajectory in Europe, mainly driven by the brewing industry's need to optimize production costs, improve fermentation efficiency, and develop diversified flavor profiles that resonate with evolving consumer preferences. Adjuncts, including unmalted grains, sugars, cassava, and potatoes, allow brewers to partially or fully substitute malted barley, reducing raw material costs while adjusting the sensory attributes of beer.

According to the Brewers Association and Barth-Haas Group, beer production volumes have remained robust despite macroeconomic headwinds, and the craft brewing movement's experimentation with non-traditional adjuncts is opening new ingredient segments. Regulatory harmonization across the European Union and expanding industrial brewing capacity in the Asia Pacific are further sustaining demand momentum through the forecast period.

Key Industry Highlights:

- Leading Region: The United Kingdom leads the European beer adjuncts market with approximately 45% of regional market share in 2025, underpinned by large-scale industrial brewing, historical sugar adjunct usage in traditional ale production, and over 2,000 independent craft breweries according to SIBA.

- Fast-Growing Market: France is the fastest growing European beer adjuncts market over 2026–2033, powered by extraordinary craft brewery expansion exceeding 2,500 breweries in 2023 per Brasseurs de France driving demand for diverse and specialty adjunct ingredients.

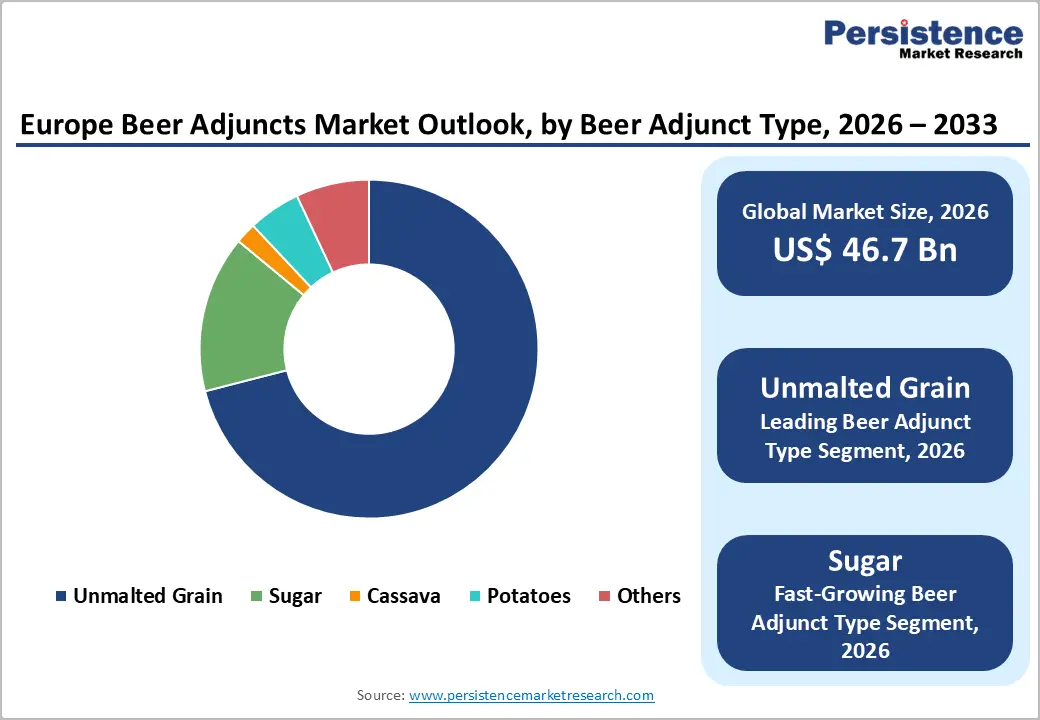

- Dominant Beer Adjunct Type: Unmalted grain is the leading beer adjunct type with approximately 71% market share in 2025, driven by its entrenched use in high-volume industrial lager production across North America, Asia Pacific, and Europe as a cost-efficient malted barley substitute.

- Fast-Growing Beer Adjunct Type: Sugar adjuncts represent the fastest growing type over 2026–2033, propelled by the surge in no-alcohol and low-alcohol beer production, which grew over 9% in Europe per IWSR Drinks Market Analysis, requiring precise sugar-based fermentation management.

- Opportunity: Premiumization of locally sourced, organic, and specialty adjunct ingredients supported by Europe's growing craft brewing culture and consumer demand for traceable, sustainable brewing inputs offers adjunct suppliers compelling margin enhancement and exclusive brewery partnership opportunities through 2033.

Market Dynamics

Drivers - Cost Optimization Imperatives Driving Widespread Adjunct Adoption Among Brewers

Cost management remains one of the most powerful and persistent structural drivers underpinning adjunct adoption in the brewing industry. Malted barley the traditional foundation of beer production is subject to significant agricultural price volatility driven by climate events, geopolitical disruptions to grain trade, and energy-intensive malting processes. According to the International Grains Council (IGC), barley prices across European markets experienced notable price spikes exceeding 20–25% during 2021–2022 amid supply chain disruptions.

Unmalted grains such as corn and rice, as well as sugars and cassava, offer brewers viable cost-effective substitution options. Large commercial brewers including Anheuser-Busch InBev and Heineken N.V. extensively utilize adjuncts to maintain competitive retail pricing while preserving product quality and fermentation consistency, making cost optimization a durable, long-term demand driver for the beer adjuncts market globally.

Restraints - Regulatory Restrictions on Adjunct Usage in Traditional Beer Markets

Longstanding brewing tradition laws remain a significant barrier to beer adjunct adoption in several key European markets. Germany's Reinheitsgebot (Purity Law of 1516), still observed by many German brewers as a quality and authenticity marker, restricts the use of adjuncts other than water, malt, hops, and yeast in beer production.

While the law is not enforced for imported beers, domestic German brewers adhering to this tradition represent a substantial market segment where adjunct adoption is inherently constrained. Similar traditional brewing standards in Belgium, Czech Republic, and parts of Austria further limit the addressable market for adjuncts in premium and traditional beer segments across Europe.

Opportunities - Rising Demand for Sugar Adjuncts in Low-Alcohol and No-Alcohol Beer Brewing

The rapid growth of the no-alcohol and low-alcohol beer (NoLo) category presents a compelling opportunity for sugar-based adjunct suppliers. Producing technically precise NoLo beer requires careful fermentation management, and specialized sugar adjuncts play a critical role in achieving consistent residual sweetness, mouthfeel, and flavor balance in the absence of full alcohol content.

According to IWSR Drinks Market Analysis, no-alcohol and low-alcohol beer volumes in Europe grew by over 9% in 2023, making it the fastest growing segment of the broader beer category. With consumers across Germany, Spain, and the U.K. increasingly embracing moderation-oriented drinking occasions, brewers are scaling NoLo production, creating sustained incremental demand for sugar adjuncts and specialty fermentable carbohydrate ingredients through the 2026–2033 forecast period.

Category-wise Analysis

Beer Adjunct Type Insights

Unmalted grain is the dominant beer adjunct type globally, accounting for approximately 71% of total market share in 2025. The segment's commanding position reflects unmalted grains' well-established role in industrial brewing as cost-efficient, technically reliable partial substitutes for malted barley. Unmalted corn and unmalted rice are particularly widely used by large commercial brewers across North America, Asia Pacific, and Latin America, where consumer preference for lighter-bodied, low-bitterness lager styles aligns with the sensory profile that these adjuncts impart.

According to the Barth-Haas Group's Annual Hops Report, the majority of beer production by volume is lager style, underpinning consistent base-level demand for unmalted grain adjuncts. Sugar is identified as the fastest growing adjunct type segment, driven by its critical role in no-alcohol and low-alcohol beer formulation and craft beer flavor innovation.

Form Analysis

Dry form beer adjuncts hold the leading position in the beer adjuncts market by form, accounting for approximately 64% of total market share in 2025. Dry adjuncts including dry milled unmalted grains, granulated sugars, and dehydrated specialty ingredients offer superior shelf life, easier transportation logistics, and more flexible incorporation into diverse brewing processes compared to liquid alternatives. These handling advantages are particularly valued by large-scale industrial brewers managing complex supply chains and by smaller craft brewers with limited cold storage infrastructure.

The American Society of Brewing Chemists (ASBC) technical guidelines widely reference dry grain adjunct incorporation in mashing processes, reflecting the format's technical entrenchment. Liquid adjuncts, including liquid sugar syrups and liquid unmalted grain extracts, represent the fastest growing form segment, driven by their precision dosing benefits in automated brewing systems.

Country-Level Insights

UK Beer Adjuncts Market Trends and Insights

United Kingdom is dominant due to its high innovation-driven brewing ecosystem and strong adjunct usage in diverse beer styles. The country has a large and dynamic craft beer industry, with over 1,900 breweries operating in 2021, reflecting a highly fragmented and innovation-led market. Unlike Germany, U.K. brewers are not restricted by purity laws, allowing extensive use of adjuncts such as sugar, fruits, and alternative grains to create flavored and specialty beers.

Additionally, beer remains a major beverage category within U.K. manufacturing, contributing significantly to beverage industry sales. This combination of high product experimentation, strong consumer acceptance of craft beers, and flexible regulations drives higher adjunct consumption, making the U.K. the leading market in Europe.

Germany Beer Adjuncts Market Trends and Insights

Germany is a critical region in the beer adjuncts market due to its sheer scale of beer production and strong global influence in brewing. It is the largest beer producer in Europe, accounting for about 7.2 billion litres or over 22% of total EU production in 2023 . This massive production base ensures consistent demand for brewing inputs, including adjuncts in certain segments like non-alcoholic and export-oriented beers.

However, the traditional Reinheitsgebot (beer purity law) restricts the use of adjuncts in many domestic beers, limiting penetration compared to other countries. Despite this, Germany’s leadership in production volume and growing innovation in categories such as non-alcoholic beer sustains its importance. Thus, Germany acts as a volume-driven but structurally constrained market within the European adjunct landscape.

France Beer Adjuncts Market Trends and Insights

France is the fastest-growing market for beer adjuncts in Europe due to its rapid expansion in craft brewing and changing consumption patterns. The country has seen strong growth in beer production and consumption, ranking among notable EU producers with around 2.1 billion litres of beer output, indicating a sizable and expanding base. Additionally, France is identified as a major beer importer within the EU, highlighting rising domestic demand and evolving consumer preferences toward diverse beer styles.

The shift toward premium, flavored, and experimental beers is encouraging brewers to increasingly adopt adjuncts. Combined with a growing microbrewery ecosystem and innovation-led consumption, France is witnessing accelerated adjunct adoption, positioning it as the fastest-growing country in the European beer adjuncts market.

Competitive Landscape

Europe beer adjuncts market is moderately consolidated at the end-user (brewer) level, dominated by multinational brewing conglomerates including Anheuser-Busch InBev, Heineken N.V., Carlsberg Group, and Molson Coors Beverage Company, which collectively command the majority of adjunct procurement volumes. At the ingredient supply level, the market is more fragmented, with agricultural commodity traders, specialty ingredient suppliers, and regional processors serving diverse brewer tiers.

Key competitive differentiators among adjunct suppliers include consistent ingredient quality, traceability, supply chain reliability, organic and non-GMO certification, and tailored technical support. Direct farm-to-brewery supply models and proprietary specialty adjunct formulations are emerging as differentiation strategies among premium-oriented suppliers.

Key Developments:

- April, 2026: Constellation Brands, Inc. evaluated a turnaround strategy for its beer segment as the broader alcohol industry showed signs of stabilization. The company assessed operational improvements, portfolio optimization, and targeted marketing initiatives to strengthen beer sales performance.

- December, 2025: Diageo plc agreed to sell its shareholding in East African Breweries plc (EABL) to Asahi Group Holdings, Ltd. The transaction marked Diageo’s strategic move to streamline its portfolio and focus on core markets and premium spirits. Meanwhile, Asahi expanded its footprint in the African beer market by acquiring the stake, strengthening its international presence. The deal was expected to support Asahi’s long-term growth strategy and enhance its position in emerging markets, particularly in East Africa’s evolving alcoholic beverages sector.

Europe Beer Adjuncts Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 36.1 Billion |

|

Projected Market Value (2026) |

US$ 46.7 Billion |

|

Projected Market Value (2033) |

US$ 65.7 Billion |

|

CAGR (2026-2033) |

5.0% |

|

Leading Country |

UK, 26% share |

|

Dominant Product |

Unmalted Grain, 71% share |

|

Top-ranking Form |

Dry, 56% share |

|

Incremental Opportunity |

US$ 14.3 billion |

Companies Covered in Europe Beer Adjuncts Market

- Heineken N.V.

- Asahi Group Holdings, Ltd.

- Constellation Brands, Inc.

- The Molson Coors Beverage Company

- Bitburger Brewery

- Anheuser Busch InBev

- Carlsberg Group

- BrewDog

- Diageo Plc.

- Kirin Holdings Company, Limited

- Tsingtao Brewery Co., Ltd.

- Others

Frequently Asked Questions

Europe beer adjuncts market is expected to be valued at US$ 46.7 billion in 2026, growing at a CAGR of 5.0% to reach US$ 65.7 billion by 2033.

Cost reduction, flavor diversification, rising beer consumption, craft brewing growth, improved fermentation efficiency, product innovation demand

The United Kingdom leads the European beer adjuncts market with approximately 45% of regional market share in 2025.

Craft beer expansion, low-calorie formulations, emerging markets growth, novel ingredients adoption, premiumization, sustainable sourcing innovations.

Heineken N.V., Asahi Group Holdings, Ltd., Constellation Brands, Inc., The Molson Coors Beverage Company, Bitburger Brewery, Anheuser Busch InBev.