- Food Ingredients & Additives

- Europe Natural Food Colors Market

Europe Natural Food Colors Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Europe Natural Food Colors Market By Ingredient Type (Carotenoids, Spirulina, Paprika, Anthocyanins, Others), Application (Bakery & Confectionery, Dairy & Frozen Food, Others), Source, by Nature, and Country Analysis for 2025 - 2032

Europe Natural Food Colors Market Size and Trends Analysis

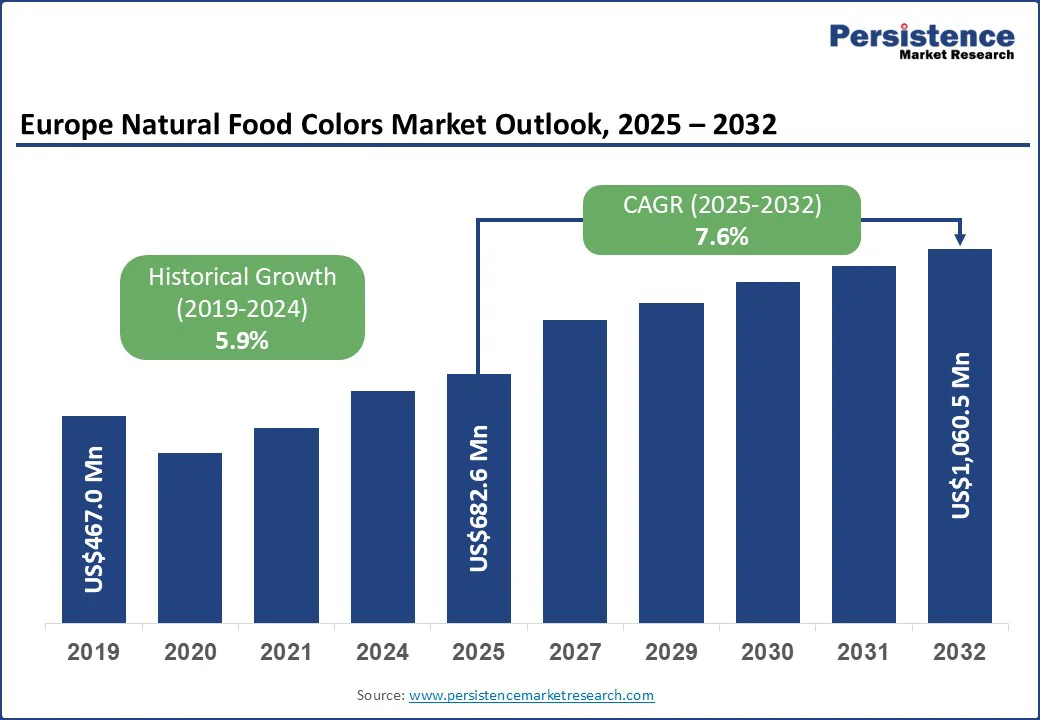

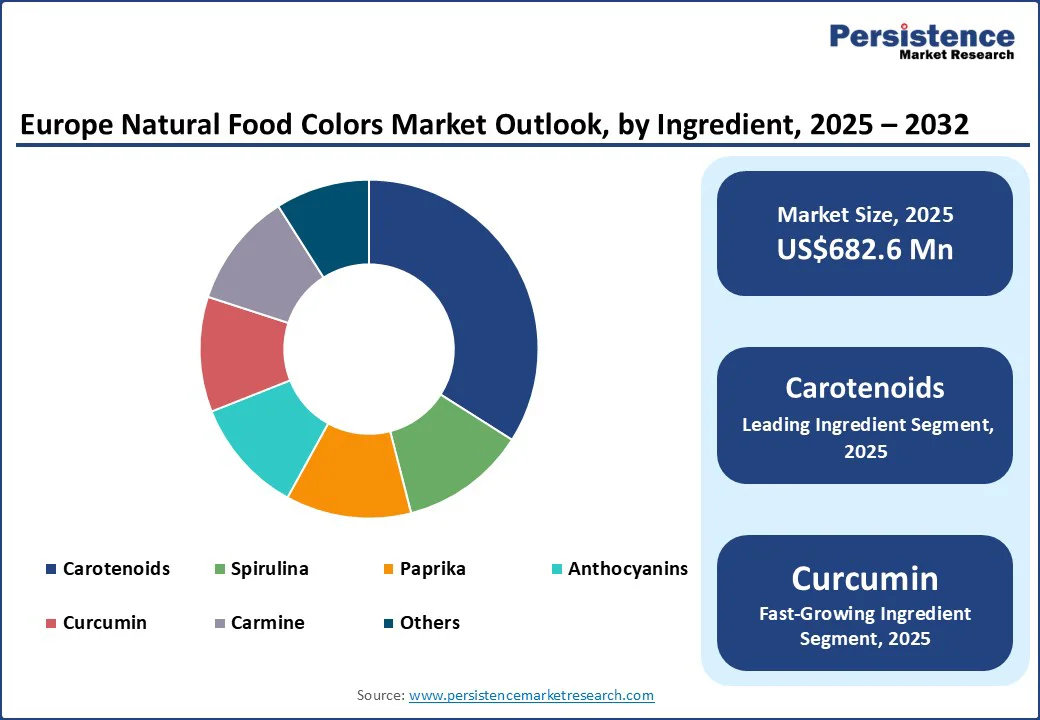

Europe natural food colors market size is likely to be valued at US$682.6 Mn in 2025 and is expected to reach US$1,060.5 Mn by 2032, growing at a CAGR of 7.6% during the forecast period from 2025 to 2032, driven by a robust food and beverage industry spanning dairy, bakery, confectionery, snacks, and beverages.

Key Industry Highlights

- Leading Country: Germany holds a dominant position with the largest import and usage of plant-based natural food colors, supported by its strong food and beverage sector, robust organic market, and advanced supply chain networks.

- Fastest-Growing Ingredient Segment: Carotenoids lead the natural food colors market, due to their stability, wide availability, health benefits, and versatile applications across beverages, dairy, bakery, and confectionery.

- Fastest-Growing Application Segment: Beverages are the largest and fastest-growing application segment, driven by clean-label trends, functional drinks, and consumer demand for vibrant, stable, and health-oriented colors.

- Market Drivers: Rising consumer preference for natural, clean-label ingredients and regulatory pressure following the EU ban on titanium dioxide (E171) are driving adoption across Europe.

- Key Players: Leading companies include Symrise, Döhler, ADM, and Brenntag, leveraging integrated sourcing, R&D, and product development to strengthen market presence.

| Key Insights | Details |

|---|---|

|

Natural Food Colors Market Size (2025E) |

US$682.6 Mn |

|

Market Value Forecast (2032F) |

US$1,060.5 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.9% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Clean-Label Natural Colors in Europe

European consumers are increasingly choosing foods made with natural and healthier ingredients, creating strong pressure on manufacturers to replace synthetic colors with plant-based options. This change is reinforced by strict EU food safety regulations, which push companies to adopt safer and more transparent alternatives. A major boost came after the EU banned titanium dioxide (E 171), encouraging the food industry to reformulate using natural choices.

Popular solutions now include fruit and starch-based colors such as Exberry’s Shade White and ADM’s PearlEdge, which provide reliable performance in terms of stability, safety, and taste neutrality. As a result, the demand for vegetable-based colorants continues to rise, supported by growing imports from both inside and outside Europe. Key markets such as Germany, Spain, Italy, France, the U.K., and Denmark are at the forefront, owing to their large-scale food industries and increasing consumer interest in organic, clean-label products that align with sustainability and health-conscious trends.

Technical and Regulatory Challenges Restrain Market Expansion in Europe

Although demand for natural food colors is increasing, several hurdles slow down wider adoption. Natural pigments often suffer from low stability under heat or light, inconsistent coloration, and reactivity with certain food ingredients, making them technically challenging to use.

European regulations also restrict which extracts are permitted, requiring safety checks and approval under EU Regulation EC 1333/2008. This makes it difficult for new or exotic ingredients to enter the market. At the same time, consumers demand transparency and traceable sourcing, which requires strong documentation and supply chain control. These technical, regulatory, and credibility challenges create barriers, especially for smaller suppliers, limiting innovation and overall market growth.

Opportunities for Stable, Sustainable, and Compliant Natural Colors in the European Market

Europe presents a strong opportunity for suppliers who can provide natural colors that are safe, stable, and sustainable, and meet EU regulations. The move away from synthetic additives, particularly after the ban on titanium dioxide, has created a clear need for high-performing white and other color alternatives. Food and beverage companies are actively seeking ingredients that are intense, heat- and light-stable, neutral in taste, and supported with proper documentation.

Alongside performance, there is growing interest in transparency and ethical sourcing, with organic certification and clear origin stories appealing strongly to European buyers. Suppliers from developing regions who can provide durable, traceable, and regulation-compliant natural colorants, backed by quality assurance, are well-positioned to gain market share. Active participation in key markets such as Germany, France, Spain, Italy, the U.K., and Denmark, where importers and formulators play a central role, will further expand access. Overall, these opportunities allow capable suppliers to strengthen their presence in Europe’s fast-growing natural food color sector.

Category-wise Analysis

Ingredient Insights

Carotenoids hold the leading position in the Europe natural food colors market, due to their wide availability, proven safety, and diverse applications. Derived from natural sources such as carrots, tomatoes, paprika, and marigolds, these pigments provide vibrant yellow, orange, and red hues that are widely preferred in food and beverages. Their strong antioxidant properties also enhance their appeal, as consumers increasingly look for ingredients that offer both functional and aesthetic benefits.

Carotenoids are highly stable compared to some other natural pigments, making them suitable for use in processed foods, dairy, confectionery, and beverages where color consistency is important. Moreover, their association with health benefits, including eye health and immune support, adds further value for health-conscious European consumers. With the ongoing transition from synthetic to natural colorants, carotenoids continue to dominate, supported by robust demand across mainstream food categories and strong alignment with clean-label and wellness-driven product trends.

Application Insights

The beverages segment leads the European natural food colors market as drinks demand vibrant, appealing, and stable shades to attract consumers. From juices, soft drinks, and energy beverages to flavored waters and non- alcoholic drinks, natural colors play a vital role in enhancing visual appeal and aligning with health-focused preferences. European consumers are particularly attentive to clean-label claims, pushing brands to replace synthetic dyes with fruit, vegetable, and plant-based alternatives. Natural pigments such as carotenoids, anthocyanins, and spirulina are widely used to create bright and consistent colors in beverages. The growing popularity of functional and organic drinks further strengthens demand, making beverages the most dominant application area for natural food colors in Europe.

Country Insights

Germany Natural Food Colors Market Trends

Germany stands out as Europe’s largest importer and one of the leading users of plant-based natural food colors, supported by its strong food and beverage industry. Imports grew in value between 2019 and 2024, even though volumes dipped slightly, highlighting rising demand for higher-quality, premium pigments. With nearly half of its imports sourced from non-EU countries, Germany remains highly connected to global supply chains, particularly China and India.

The strong organic food market further drives demand, as consumers seek safe, traceable, and clean-label ingredients. Meat, dairy, and bakery remain the largest application areas, pushing innovation in color formulations. Leading players like Symrise, Döhler, and ADM play a vital role in shaping the market through integrated sourcing, technological expertise, and product development. Overall, Germany’s market is expected to grow steadily, driven by health, safety, and sustainability trends.

Competitive Landscape

The Europe natural food colors market is highly competitive, with leading players focusing on innovation, sustainability, and regulatory compliance. Key companies include Givaudan (DDW), ADM, Sensient Technologies, Döhler, Symrise, and Chr. Hansen, all offering extensive pigment portfolios. Competition is driven by rising demand for clean-label, stable, and organic-certified solutions. Strategic partnerships, R&D investments, and global sourcing networks strengthen their market presence while meeting evolving consumer preferences across diverse food and beverage applications.

Key Industry Developments

- In June 2025, Sensient Flavors & Extracts launched BioSymphony™, a groundbreaking portfolio of natural flavors made from nature’s finest ingredients. Designed to deliver authentic, high-impact taste experiences, BioSymphony addresses the evolving demands of today’s food and beverage manufacturers.

- In April 2023, Sensient® Colors launched a new natural green shade designed to highlight wellness and naturalness, particularly appealing in pet food and treat formulations.

- In March 2023, Oterra®, a global leader in natural coloring solutions, announced the launch of its new range of organic coloring foodstuffs.

Companies Covered in Europe Natural Food Colors Market

- Oterra (Chr. Hansen Natural Colors)

- Sensient Technologies Corporation

- Archer Daniels Midland

- Naturex S.A.

- Döhler GmbH

- Symrise AG

- McCormick & Company

- Kalsec Inc.

- Kerry Group

- Sethness Roquette

- DDW The Color House Corporation

Frequently Asked Questions

The Europe natural food colors market is projected to be valued at US$682.6 Mn in 2025.

Europe’s natural food colors market is driven by clean-label demand, regulatory restrictions on synthetics, health consciousness, and sustainable sourcing preferences.

The Europe natural food colors market is poised to witness a CAGR of 7.6% between 2025 and 2032.

Key opportunities lie in blue spirulina innovations, organic-certified colors, and fermentation-based sustainable pigment production.

Major players in Europe natural food colors market are Oterra (Chr. Hansen Natural Colors), Sensient Technologies Corporation, Archer Daniels Midland, Naturex S.A., and Döhler GmbH.