- Specialty & Fine Chemicals

- Ethyl Carbamate Market

Ethyl Carbamate Market Size, Share, and Growth Forecast, 2026 – 2033

Ethyl Carbamate Market by Product Form (Liquid, Powder), Application (Food & Beverage, Pharmaceuticals, Cosmetics, Industrial Chemicals, Others), End-User (Food Industry, Pharmaceutical Industry, Cosmetic Industry, Chemical Industry, Others), and Regional Analysis for 2026-2033

Ethyl Carbamate Market Share and Trends Analysis

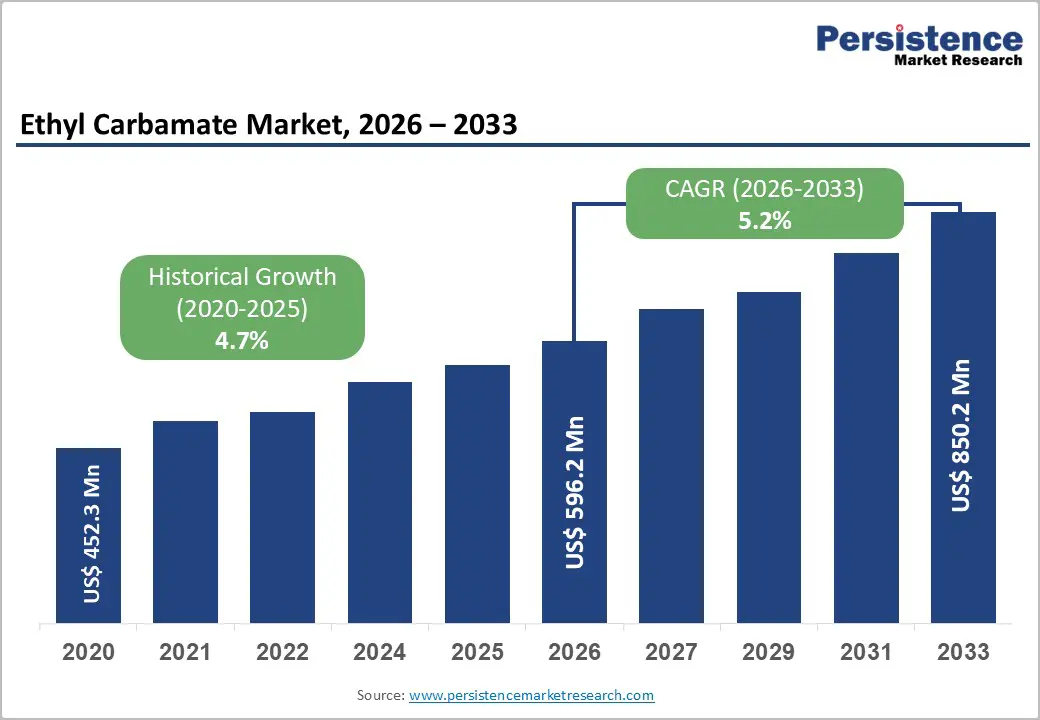

The global ethyl carbamate market size is likely to be valued at US$ 596.2 million in 2026, and is projected to reach US$ 850.2 million by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033. Sustained regulatory oversight combined with expanding industrial and pharmaceutical utilization positions the ethyl carbamate market on a stable growth trajectory during the forecast period. Increased global focus on chemical safety compliance has accelerated demand for controlled-grade ethyl carbamate in laboratory calibration, pharmaceutical synthesis, and regulated food testing environments. Heightened clinical and toxicological awareness among regulatory authorities has reinforced structured monitoring frameworks, prompting consistent procurement by institutional users.

Advancements in analytical chemistry and quality assurance technologies have strengthened controlled production and detection capabilities.High-precision chromatography, improved impurity profiling, and digital compliance documentation have enhanced traceability across pharmaceutical and food safety applications. Healthcare infrastructure modernization has indirectly supported market expansion through rising demand for validated reference compounds. National food safety agencies, pharmaceutical regulators, and public health laboratories have increased reliance on certified chemical standards to support surveillance and compliance enforcement. Standardization of treatment protocols and clinical research workflows continue to require consistent chemical benchmarking materials.

Key Industry Highlights

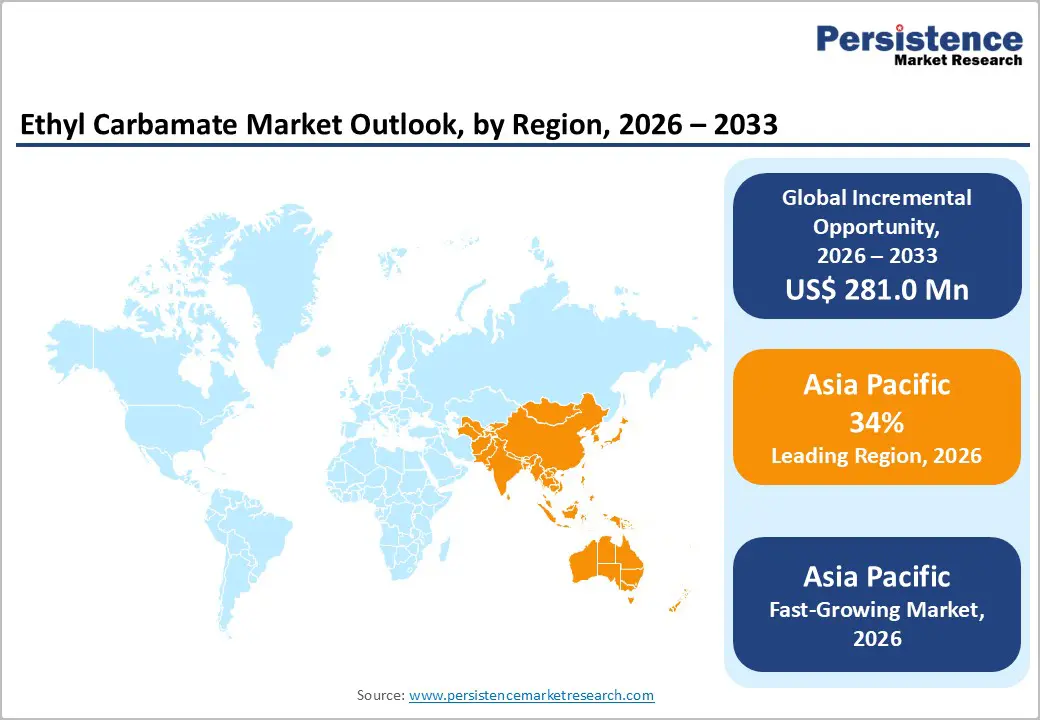

- Dominant Region: Asia Pacific is expected to hold an estimated 34% market share in 2026, supported by high production of fermented foods and beverages and pharmaceutical manufacturing growth.

- Fastest-growing Market: Asia Pacific is also projected to be the fastest-growing market through 2033, driven by laboratory automation and rising compliance with global trade standards.

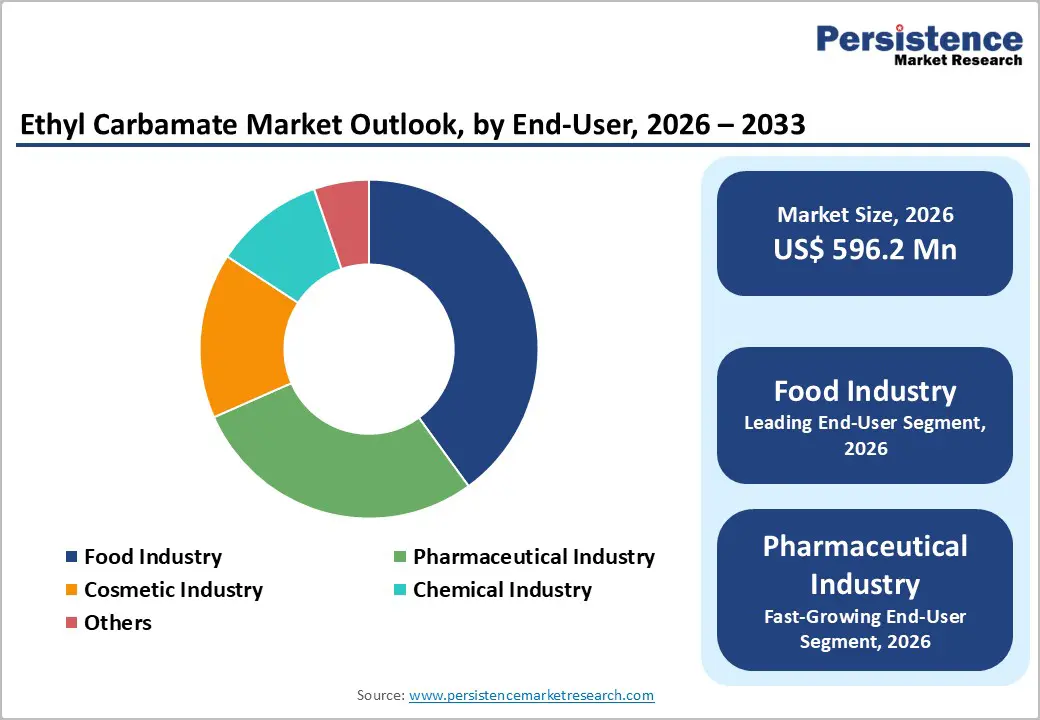

- Leading End-User: The food industry is expected to hold roughly 38% revenue share in 2026, fueled by mandatory compliance testing, export certification, and standardized verification.

- Fastest-growing End-User: The pharmaceutical industry is projected as the fastest-growing segment between 2026 and 2033, driven by laboratory digitalization and technology-enabled quality control.

| Global Market Attributes | Key Insights |

|---|---|

| Ethyl Carbamate Market Size (2026E) | US$ 596.2 Mn |

| Market Value Forecast (2033F) | US$ 850.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory-Driven Demand for Certified Reference and Compliance Materials

Regulatory enforcement across food, beverage, and pharmaceutical quality systems has repositioned certified reference and compliance materials as mandatory infrastructure rather than supportive tools. Laboratories and manufacturers operate under compulsory validation regimes that require defensible calibration for trace contaminants with high toxicological sensitivity. Ethyl carbamate occupies a critical compliance position due to strict monitoring expectations and low tolerance levels in fermented and distilled products. Inspection frameworks increasingly examine the certification scope, traceability, and uncertainty documentation of analytical inputs alongside test outcomes. This shift places material credibility at the center of regulatory acceptance, transforming certified references into commercial safeguards that protect operating approvals, export continuity, and contractual eligibility. Procurement decisions therefore reflect governance and risk priorities, where certified materials reduce exposure during audits and reinforce confidence in reported results.

Harmonization of analytical expectations across jurisdictions reinforced recurring demand for compliance-grade materials embedded into routine testing cycles. Accreditation bodies and border authorities emphasize method consistency and inter-laboratory comparability, which elevates reliance on validated references with stable performance characteristics. Testing programs evolve from periodic verification toward continuous monitoring, increasing consumption frequency of certified inputs. Organizations integrate these materials into standard operating procedures, proficiency testing, and digital laboratory management systems to sustain compliance readiness. Regulatory clarity and enforcement depth therefore convert certified reference materials into predictable operating necessities. Demand strength emerges from mandated testing intensity and documentation rigor rather than discretionary quality initiatives, anchoring long-term commercial relevance through compliance-driven analytical discipline.

Stringent Health Risk Classification and Regulatory Restrictions

Heightened regulatory scrutiny emerged after global health authorities categorized ethyl carbamate under high-risk chemical profiles, reshaping acceptance across regulated industries. This classification triggered stricter internal governance among manufacturers, distributors, and end users, where compliance assurance became a prerequisite for commercial engagement. Risk classification influenced corporate policies, procurement audits, and product stewardship frameworks, reducing tolerance for substances associated with long-term health exposure. Testing frequency, validation protocols, and traceability requirements expanded, elevating operational complexity and cost intensity. Decision-makers increasingly prioritized reputational protection and regulatory alignment, leading to conservative portfolio rationalization. Innovation pipelines faced limitations as research investment shifted toward safer substitutes rather than optimization of regulated compounds. These dynamics reduced commercial attractiveness, especially in consumer-facing segments subject to public health oversight.

Regulatory restrictions reinforced this restraint through enforceable exposure limits, monitoring obligations, and conditional approvals that constrained operational flexibility. Cross-border trade encountered friction as compliance standards varied by jurisdiction, increasing administrative burden and limiting scalability. Licensing timelines extended due to mandatory toxicological assessments and periodic reassessments, delaying market entry and discouraging capacity investments. Contractual relationships evolved to include stricter indemnity clauses and compliance warranties, transferring regulatory risk across the value chain. Financial institutions integrated chemical risk screening into funding criteria, tightening access to capital for projects involving restricted substances. End-user industries adopted precaution-driven sourcing strategies, favoring alternatives with lower regulatory exposure to ensure continuity and stakeholder confidence.

Growth of Accredited Testing Laboratories in Emerging Economies

Expansion of certified analytical infrastructure across developing regions reshapes compliance dynamics for regulated food and beverage compounds. Wider availability of internationally recognized laboratories reduces dependency on overseas testing, shortens turnaround cycles, and improves consistency in detection thresholds. This structural shift elevates routine screening from a compliance formality to a continuous quality-control function embedded within production workflows. Producers of alcoholic beverages, fermented foods, and flavoring inputs operate under closer analytical visibility, prompting higher testing frequency and broader parameter coverage. Improved laboratory density strengthens alignment with global food safety frameworks, enabling exporters to meet stringent import specifications with greater confidence. Increased domestic testing capability supports faster regulatory audits and smoother certification processes, reinforcing trust across supply chains and trade partners while lowering operational friction tied to cross-border verification.

Commercial implications extend beyond compliance into demand creation for reference standards, calibration materials, and validated analytical methods. Accredited facilities act as market enablers by translating regulatory thresholds into measurable operational requirements, which stimulates procurement of high-purity compounds used for method validation and proficiency testing. Emerging economies experience accelerated regulatory maturity as laboratory accreditation under ISO 17025 becomes a prerequisite for cross-border trade participation. This environment favors suppliers capable of supporting laboratories with consistent quality, documentation, and traceability aligned with international norms. As laboratory networks expand, data generation increases, driving deeper regulatory scrutiny and more frequent method updates, which reinforces sustained testing demand.

Category-wise Analysis

Product Type Insights

Liquid is poised to lead with a forecasted 58% of the ethyl carbamate market revenue share in 2026, owing to superior handling precision, uniform concentration control, and compatibility with analytical instrumentation. Liquid ethyl carbamate supports streamlined laboratory workflows through ready-to-use formats that minimize weighing errors and preparation time. Consistent concentration profiles enable accurate dilution series, calibration curves, and method validation aligned with regulatory protocols. Pharmaceutical and food safety laboratories prioritize liquid formulations due to reduced preparation variability and improved reproducibility across repeated analyses. Availability in standardized packaging with certified concentration ranges strengthens confidence during audits and inter-laboratory comparisons. Progress in sealed containment systems, tamper-evident closures, and contamination prevention mechanisms improves operational safety, reinforcing preference among compliance-focused users and high-throughput testing environments.

Powder is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for extended shelf life, flexible formulation, and cost-efficient transportation. Powder form enables long-term storage without degradation risk under controlled conditions, supporting strategic inventory management. Bulk procurement aligns with research institutions and industrial laboratories that conduct in-house formulation and custom dilution protocols. Lower shipping weight and reduced packaging volume improve logistics efficiency across geographically dispersed facilities. Advancements in packaging technology, moisture barriers, and anti-static handling solutions improve stability and user safety. Rising research intensity and decentralization of laboratory infrastructure expand demand for adaptable product formats, supporting accelerated adoption across emerging testing and research ecosystems.

Application Insights

Food and beverage are likely to be the leading segment with a projected 42% ethyl carbamate market share in 2026, due to regulatory surveillance requirements and standardized testing protocols. National food safety authorities mandate ethyl carbamate monitoring within alcoholic beverages and fermented products to align with public health risk thresholds. Routine surveillance programs translate regulatory intent into recurring analytical demand across production batches. Consumer trust considerations influence brand reputation, prompting manufacturers to integrate systematic testing into quality frameworks. International trade compliance requirements for exports into regulated markets reinforce consistency in testing practices. Expansion of quality assurance outsourcing and accredited laboratories strengthens procurement continuity, improves turnaround efficiency, and embeds analytical verification as a core operational function within food and beverage supply chains.

Pharmaceuticals expected to witness the fastest growth between 2026 and 2033, powered by expanding drug development pipelines and heightened regulatory scrutiny. Pharmaceutical manufacturing emphasizes impurity profiling and toxicological assessment throughout development and production stages to align with global regulatory submissions. Analytical rigor supports risk mitigation during formulation, stability testing, and process scale-up. Growing focus on patient safety elevates demand for precise contaminant monitoring across active pharmaceutical ingredients and finished dosage forms. Regulatory agencies require detailed analytical documentation, driving repeat testing and method validation. Expansion of contract research and manufacturing organizations increases decentralized testing activity, reinforcing sustained demand across pharmaceutical development and commercial manufacturing environments.

End-User Insights

The food industry is slated to hold a dominant position, with an anticipated 38% of market share in 2026, driven by mandatory compliance testing and export certification requirements. Regulatory enforcement frameworks across alcoholic beverages, fermented foods, and processed products institutionalize routine analytical verification within production cycles. Export-oriented manufacturers align internal quality systems with destination-country safety thresholds, reinforcing repeat testing activity. Standardized documentation, batch-level traceability, and audit readiness elevate demand consistency across large and mid-sized processors. Growth in accredited third-party laboratories supports scalable testing access, reducing operational bottlenecks. Integration of testing outcomes into supplier qualification programs further embeds analytical verification into procurement and sourcing decisions, sustaining long-term demand stability.

The pharmaceutical industry is forecasted to be the fastest-growing end-user between 2026 and 2033, boosted by laboratory digitalization, contract research expansion, and cost-efficient outsourcing models. Digital laboratory information management systems enable higher testing throughput, data integrity, and regulatory transparency across development stages. Contract research organizations and contract manufacturing organizations expand analytical service capacity, supporting flexible sourcing strategies for pharmaceutical developers. Centralized quality control frameworks standardize impurity assessment across global production networks. Technology-enabled service delivery shortens validation cycles and improves compliance alignment, amplifying procurement volumes as pharmaceutical pipelines diversify and regulatory expectations intensify across markets.

Regional Insights

North America Ethyl Carbamate Market Trends

North America maintains a strong position in ethyl carbamate utilization, driven by stringent regulatory frameworks, high production volume of alcoholic beverages, and advanced laboratory infrastructure in countries such as the United States and Canada. Federal and state-level agencies enforce contaminant monitoring across distilled spirits, wine, and fermented products, converting regulatory oversight into continuous analytical demand. The United States operates under well-established voluntary and mandatory testing programs that align with international safety standards, supporting both domestic production and export compliance. Canada emphasizes harmonized testing protocols across provinces, reinforcing consistency in detection methods and validation procedures. High concentration of ISO-accredited laboratories and widespread adoption of high-throughput analytical instrumentation ensures rapid batch verification, minimizes non-compliance risk, and embeds routine testing into standard production operations.

Growth dynamics focus on adoption of advanced technologies, data integration, and expanded contract testing services. Pharmaceutical and biotech manufacturing hubs in the United States and Canada increasingly require ethyl carbamate monitoring during impurity profiling, stability testing, and formulation validation. Expansion of contract research organizations and third-party laboratories supports flexible analytical capacity for small- and mid-sized manufacturers. Investment in laboratory automation, digital data management, and high-sensitivity chromatography enhances testing efficiency, traceability, and audit readiness. Rising consumer awareness and stricter import-export scrutiny reinforce frequent method updates, recalibration, and validation demand.

Europe Ethyl Carbamate Market Trends

Europe demonstrates a mature and compliance-intensive landscape for ethyl carbamate uptake, anchored by stringent food safety enforcement and advanced analytical infrastructure across countries such as Germany, France, Italy, Spain, and the United Kingdom. Wine-producing economies including France, Italy, and Spain operate under mandatory contaminant thresholds enforced through routine batch-level surveillance, converting regulatory oversight into stable analytical demand. Germany and the United Kingdom contribute through strong laboratory networks and pharmaceutical-grade testing capacity aligned with European Union (EU) food safety and chemical regulations. High export penetration into premium beverage markets sustains strict adherence to contaminant limits, reinforcing repeat testing cycles. Dense concentration of ISO 17025–accredited laboratories ensures analytical consistency, rapid turnaround, and cross-border recognition of test results, embedding testing activity into standard commercial operations rather than episodic compliance events.

Growth dynamics across Europe reflect sophistication-driven expansion rather than volume-led acceleration. Pharmaceutical manufacturing hubs in Germany, Switzerland, Belgium, and Ireland intensify impurity profiling requirements across active pharmaceutical ingredients and excipients. Regulatory alignment under centralized approval pathways elevates demand for validated analytical methods and reference materials. Contract research organizations expand specialized testing services to support smaller manufacturers navigating complex regulatory submissions. Investment flows prioritize high-sensitivity chromatography, laboratory automation, and digital quality systems to improve traceability and audit readiness. Environmental and consumer protection policies elevate scrutiny across fermentation-derived inputs used in food and pharmaceutical formulations. Periodic regulatory updates translate into revised testing protocols, sustaining recalibration and method validation activity.

Asia Pacific Ethyl Carbamate Market Trends

Asia Pacific is expected to dominate with an estimated 34% of the ethyl carbamate market share in 2026, reflecting high concentration of fermented food and alcoholic beverage production, expanding pharmaceutical manufacturing activity, and tightening contaminant monitoring frameworks across major economies. Large-scale production of spirits, rice wine, and fermentation-based ingredients generates continuous analytical testing requirements tied to food safety thresholds. Export-oriented manufacturers integrate routine screening into quality control systems to meet international compliance expectations. Expansion of accredited laboratories and contract testing facilities improves domestic analytical capacity, shortens turnaround timelines, and supports consistent procurement cycles. Regulatory modernization initiatives and stronger enforcement mechanisms institutionalize testing frequency, reinforcing structural demand leadership driven by scale and compliance intensity.

Asia Pacific is forecasted to be the fastest-growing regional market for ethyl carbamate between 2026 and 2033, stimulated by acceleration in pharmaceutical development, growth of contract research services, and rising adoption of standardized analytical protocols. Active pharmaceutical ingredient production and formulation activities increasingly emphasize impurity profiling across development and commercial stages. Expansion of third-party laboratories and laboratory automation enhances testing throughput while lowering per-sample cost, encouraging broader adoption among mid-sized manufacturers. Alignment with global trade standards and increasing export participation elevate testing rigor, sustaining elevated growth momentum and reinforcing long-term leadership through compliance-driven expansion.

Competitive Landscape

The global ethyl carbamate market structure reflects moderate concentration, with leading multinational chemical suppliers controlling approximately 60% of overall activity. Key players such as Merck KGaA, Thermo Fisher Scientific Inc., Spectrum Chemical, LGC Limited, and Tokyo Chemical Industry (India) Pvt. Ltd. leverage established regulatory certifications, global distribution networks, and long-term institutional contracts to maintain consistent revenue streams. These companies benefit from brand recognition, technical expertise, and the ability to supply standardized high-purity compounds that meet stringent laboratory and industrial requirements. Their broad geographic reach allows servicing of both mature and emerging markets, supporting recurring procurement across food, pharmaceutical, and research applications.

Smaller participants focus on niche research applications and regional laboratory segments where demand patterns are specialized or limited in scale. These companies compete on agility, tailored service offerings, and customized product solutions, often supplying specialized reagents or smaller volume requirements that large-scale suppliers may not prioritize. Growth opportunities for smaller players include supporting contract research organizations, academic laboratories, and emerging pharmaceutical hubs that require flexible sourcing options. Despite the presence of dominant multinational suppliers, moderate market concentration allows for innovation and specialized offerings, ensuring that smaller participants maintain relevance within targeted segments.

Key Industry Developments

- In September 2025, the University of Agronomic Sciences and Veterinary Medicine of Bucharest conducted a review on ethyl carbamate in fermented beverages and foods. It found that compound levels were highest in stone fruit distillates, fortified wines, and soy sauce. However, they were lower in breads and yogurt, and formations via urea/ethanol reactions during fermentation/storage processes.

- In September 2025, Dalian Institute of Chemical Physics, Chinese Academy of Sciences led a study on rapid ethyl carbamate detection in Chinese liquor. They developed FastGC-PICI-TOFMS method achieving 1.6-3.7% precision without sample pre-treatment. The method was successfully tested across four liquor types, enabling high-throughput quality control for the carcinogen.

- In February 2025, Canadian authorities announced proposals to reclassify ethyl carbamate limits for alcoholic beverages into enforceable food contaminant regulations, aiming to modernize classifications and strengthen safety enforcement under federal food law.

Companies Covered in Ethyl Carbamate Market

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Spectrum Chemical

- LGC Limited

- Tokyo Chemical Industry (India) Pvt. Ltd.

- Santa Cruz Biotechnology Inc.

- Cayman Chemical

Frequently Asked Questions

The global ethyl carbamate market is projected to reach US$ 596.2 million in 2026.

Rising regulatory compliance requirements, growing alcoholic beverage and fermented food production, and increasing pharmaceutical testing demand are driving the market.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

A key market opportunity is the expansion of accredited testing laboratories supporting pharmaceutical, food safety, and research applications.

Some of the key market players include Merck KGaA, Thermo Fisher Scientific Inc., Spectrum Chemical, LGC Limited, and Tokyo Chemical Industry (India) Pvt. Ltd.