- Specialty & Fine Chemicals

- Dimethylolpropionic Acid (DMPA) Market

Dimethylolpropionic Acid (DMPA) Market Size, Share, and Growth Forecast 2025 - 2032

Diemthylolpropionic Acid (DMPA) Market by Product Type (Polyurethane Dispersions, Resins, Powder Coatings), Grade (Technical Grade, High-Purity Grade, Ultra-High Purity Grade), Application (Coatings, Adhesives & Sealants, Textiles & Synthetic Fibers), Industry and Regional Analysis 2025 - 2032

Diemthylolpropionic Acid (DMPA) Market Share and Trends Analysis

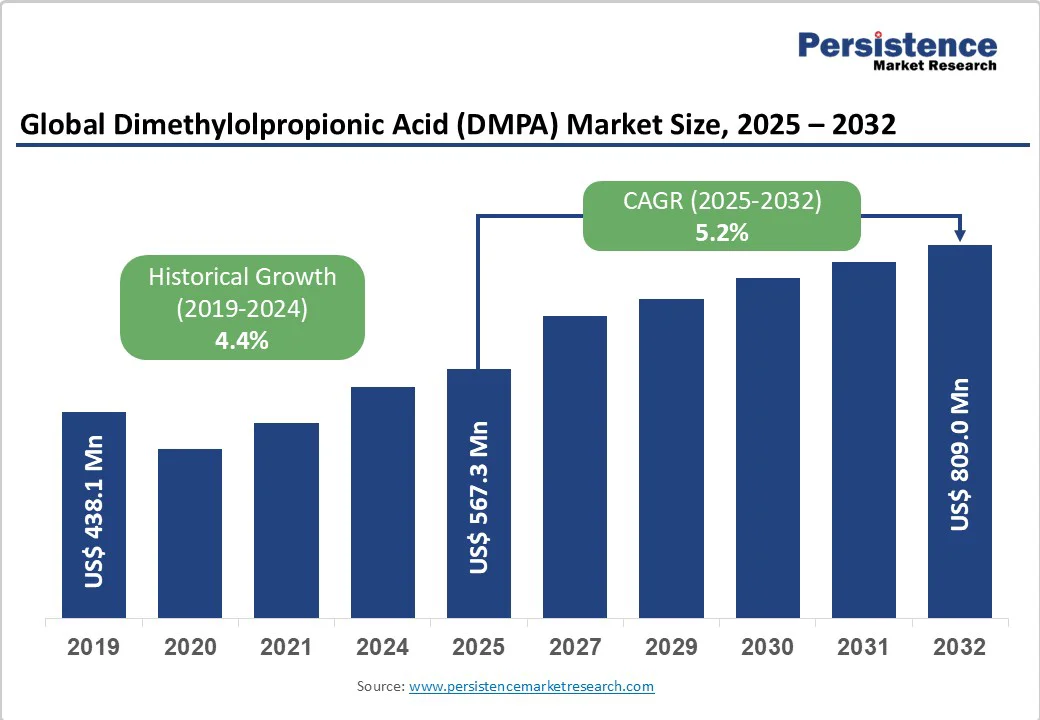

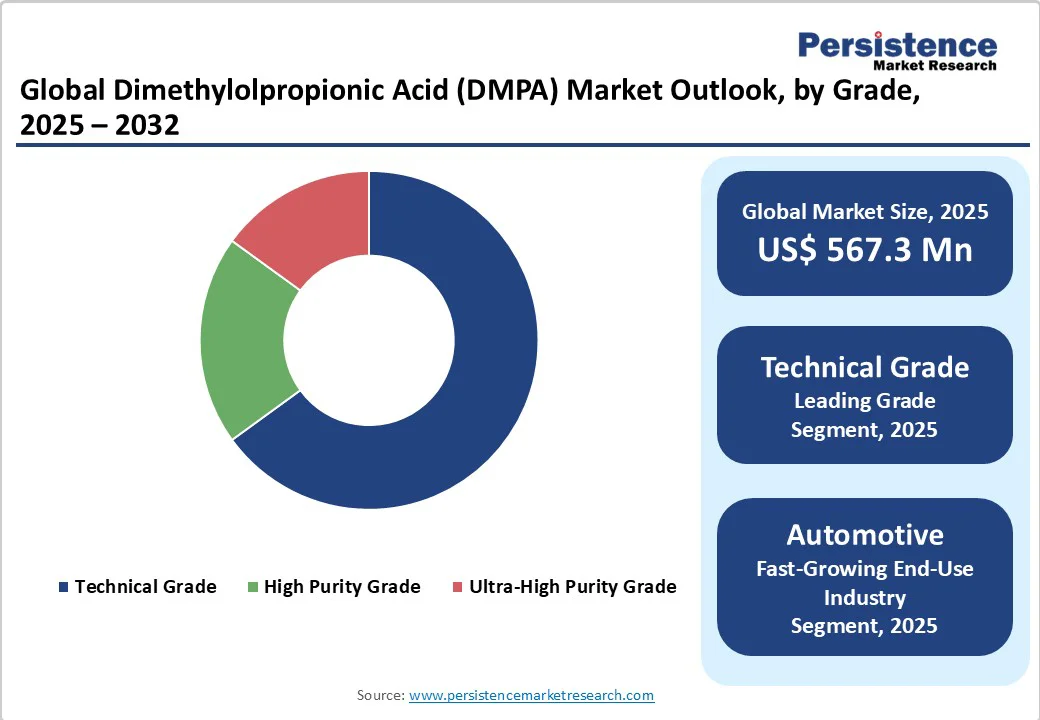

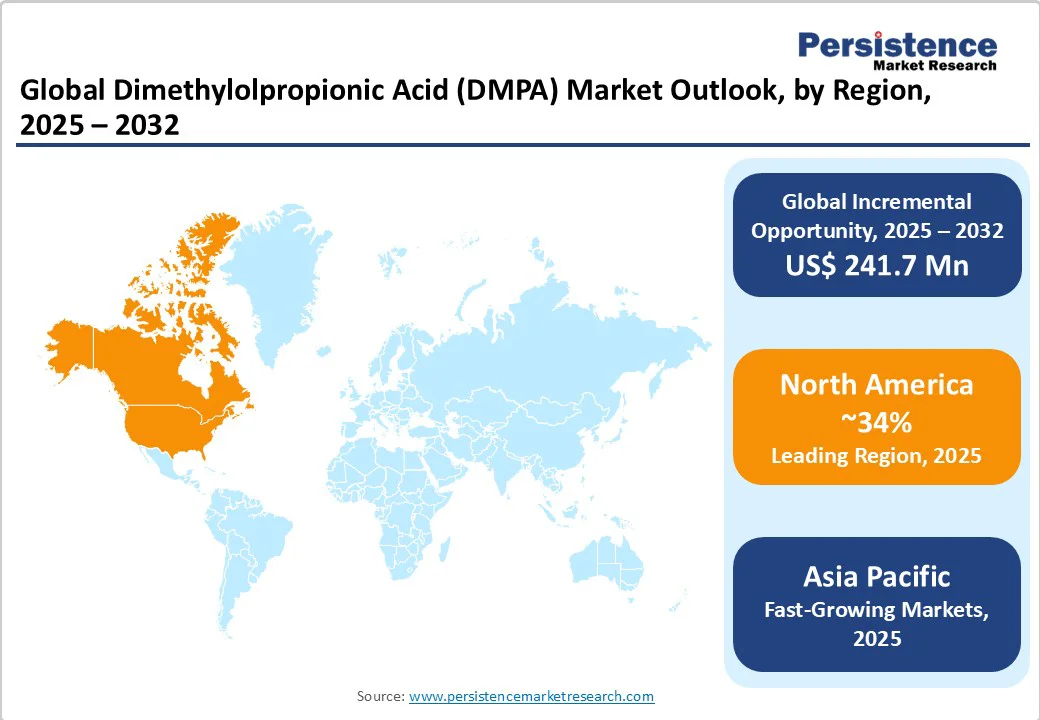

The global Dimethylolpropionic Acid (DMPA) market size is likely to be valued at US$567.3 billion in 2025 and is projected to reach US$809.0 billion by 2032, growing at a CAGR of 5.2% between 2025 and 2032. The increasing adoption of waterborne coatings, tighter regulations favoring eco-friendly chemistries, and rising demand across various sectors, including automotive, electronics, and construction, drive market growth.

Manufacturers are witnessing heightened interest in DMPA due to its integral role in low-VOC and high-performance polyurethane dispersions (PUDs). These trends are reinforced by shifting consumer preferences toward sustainable and non-toxic products, prompting industry players to innovate in product formulation and the integration of green technology.

Key Market Highlights

- North America leads the global DMPA market, attributed to its technological edge, regulatory innovation, and collaborative R&D ecosystem.

- Asia Pacific is the fastest growing region, thanks to rapid industrialization and favorable investment climates in manufacturing.

- Polyurethane Dispersions (PUDs) dominate the product landscape as the leading segment due to widespread adoption in automotive, furniture, and architectural coatings.

- The adhesives segment is expanding at the highest CAGR, reflecting increasing demand for low-VOC, high-performance assembly solutions.

- The development of new DMPA derivatives for high-tech applications such as electronics and specialty surface coatings represents a key future market opportunity.

| Key Insights | Details |

|---|---|

|

Dimethylolpropionic Acid (DMPA) Size (2025E) |

US$567.3 billion |

|

Market Value Forecast (2032F) |

US$809.0 billion |

|

Projected Growth CAGR (2025-2032) |

5.2% |

|

Historical Market Growth (2019-2024) |

4.4% |

Market Dynamics

Driver - Increasing Demand for Eco-Friendly Coatings

The demand for eco-friendly waterborne coatings is a principal driver of the Dimethylolpropionic Acid market. Regulatory mandates such as those imposed by the US EPA and the European Chemicals Agency (ECHA) are tightening volatile organic compound (VOC) emission thresholds, catalyzing a transition to water-based systems that require DMPA as a critical monomer. As industries prioritize green chemistry, DMPA-based coatings which deliver low toxicity, high performance, and robust adhesion—are expanding in automotive, electronics, and industrial finishes. This sustainable shift is further encouraged by consumers who increasingly seek products with reduced environmental impact.

Growth in Automotive Sector Adoption

Automotive manufacturers worldwide are incorporating polyurethane dispersions (PUDs), a primary application of DMPA, in OEM and aftermarket coatings. Vehicle lightweighting and environmental standards push automakers to adopt waterborne and powder coatings for resistance and durability in challenging environments. This application leverages DMPA’s chemical structure to provide elasticity, adhesion, and enhanced weatherability, resulting in superior topcoats and primers. According to industry sources and regulatory guidance, PUD-based coatings now represent over 30% share in modern automotive finishing.

Restraint - Feedstock Price Volatility

Market participants face challenges from fluctuating prices of raw materials, such as formaldehyde and propionaldehyde, which are fundamental feedstocks for DMPA synthesis. Global supply disruptions or shifts in petrochemical markets can impact margin stability and planning for DMPA producers, particularly in regions that rely heavily on oil and gas imports or those without domestic upstream integration. Such price swings hinder cost predictability for downstream manufacturers, offsetting gains from higher demand.

Regulatory Complexity for Cross-Border Trade

Increasingly complex health and environmental regulations differing across the US, Europe, and Asia Pacific add to compliance costs and prolong approval processes for new DMPA-based systems. The need to meet REACH, TSCA, and respective national standards raises the barrier for market entry, with additional documentation, labeling, and lifecycle monitoring typically required. For new market entrants and smaller suppliers, this elevates risk and operational cost, limiting ecosystem dynamism.

Opportunity - Innovation in Electronics and High-Tech Coating Applications

DMPA’s role in formulating coatings for electronics, such as printed circuit boards and protective encapsulants, opens fresh avenues for growth. The electronics industry’s strict performance and environmental standards require polymers with optimal chemical resistance and low toxicity attributes, which are inherent to DMPA-based dispersions. Companies investing in R&D to tailor DMPA solutions for high-frequency electronics, miniaturization, and wearable technology applications are set to capture long-term demand.

Expansion in Asia Pacific Industrial Production

Rapid industrialization in China, India, and Southeast Asia continues to propel consumption of DMPA in coatings, adhesives, and textiles. Robust construction activity, increased foreign direct investment in manufacturing, and favorable policies (such as “Make in India” and the “China Manufacturing 2025” initiative) amplify DMPA uptake. Local regulatory incentives for sustainable manufacturing further stimulate innovation and localization of DMPA-based chemistries.

Category-wise Insights

Product Type Analysis

Polyurethane Dispersions (PUDs) account for approximately 33% of the global Dimethylolpropionic Acid (DMPA) market, making them the leading product type segment. DMPA plays a vital role as a chain extender and internal emulsifier in PUD synthesis, contributing to improved mechanical strength, abrasion resistance, and environmental compatibility. The growing shift toward eco-friendly, waterborne coatings in industries such as automotive, furniture, and industrial manufacturing has significantly boosted demand for PUDs. Their superior performance offering low Volatile Organic Compound (VOC) content, flexibility, and excellent adhesion, has made them a preferred alternative to conventional solvent-based systems.

Furthermore, stringent emission norms by agencies such as the U.S. Environmental Protection Agency (EPA) and European Chemicals Agency (ECHA) are compelling manufacturers to adopt DMPA-based PUDs, thereby strengthening their market leadership.

Technical Grade

The technical grade segment dominates the Dimethylolpropionic Acid (DMPA) market, capturing more than 65% of total demand. This grade is widely preferred across industries for manufacturing coatings, adhesives, and sealants due to its optimal balance between purity, cost-efficiency, and performance consistency.

Technical-grade DMPA is extensively used in polyurethane dispersions, waterborne resins, and powder coatings, where it acts as a crosslinking and dispersing agent to enhance film-forming properties. Its widespread adoption is further supported by its ability to deliver reliable results in bulk industrial formulations without requiring the ultra-high purity associated with reagent grades. As demand for large-scale waterborne polymer systems continues to grow globally, particularly in the Asia Pacific and North America, the technical-grade DMPA segment is expected to maintain its dominant position in industrial production environments.

Application Analysis

The coatings are the largest application segment for Dimethylolpropionic Acid (DMPA), accounting for nearly 47% of global consumption. DMPA is a key intermediate in formulating polyurethane coatings, enhancing their durability, gloss retention, and resistance to water, chemicals, and abrasion. Its hydrophilic nature allows for stable waterborne coatings, replacing solvent-based alternatives that emit high VOCs.

The transition toward sustainable coatings across industries such as automotive, electronics, construction, and wood finishing is a primary growth driver. DMPA-based coatings offer protective performance and enable manufacturers to meet environmental and regulatory standards. The rising adoption of powder and waterborne systems, driven by increasing environmental regulations and consumer preference for sustainable finishes, ensures steady growth of this segment in the global DMPA market.

Industry Analysis

The automotive industry holds a leading position in the global Dimethylolpropionic Acid (DMPA) market, representing over 29% of total end-use demand. DMPA’s role in developing polyurethane-based coatings and adhesives makes it critical for automotive applications, where surface protection, corrosion resistance, and aesthetic enhancement are essential. The shift toward eco-friendly, low-emission coatings has augmented the integration of DMPA in waterborne polyurethane dispersions used for vehicle exteriors, interiors, and component coatings.

Automakers are increasingly adopting these systems to comply with stringent emission regulations and to improve fuel efficiency through lightweight coating solutions. Moreover, the expansion of electric vehicle (EV) production is amplifying the demand for high-performance, sustainable materials further driving DMPA utilization in specialized automotive coatings and adhesive formulations.

Regional Insights

North America Dimethylolpropionic Acid (DMPA) Trends

The U.S. leads in DMPA consumption on account of sophisticated manufacturing, advanced technology infrastructure, and substantial R&D capabilities. Regulatory actions by the US EPA around VOC reduction and chemical safety accelerate industry conversion to waterborne and powder systems. Growth trends are reinforced by the region’s innovation ecosystem, including collaborations among manufacturers, research institutions, and regulatory bodies for sustainable coating development. Canadian and Mexican markets are growing steadily, with policy alignment favoring green chemistry and advanced industrial design.

Europe Dimethylolpropionic Acid (DMPA) Trends

Germany, France, and the United Kingdom are driving European market growth with stringent regulatory harmonization under REACH and a commitment to circular economy principles. European manufacturers leverage DMPA to formulate high-performance water-based resins for construction and automotive applications. Governmental green initiatives and public-private innovation hubs underpin steady technology adoption, while regulatory synchronization across the EU enables smoother cross-border movement of advanced chemicals.

Asia Pacific Dimethylolpropionic Acid (DMPA) Trends

Asia Pacific emerges as the fastest growing regional market led by China, India, Japan, and the ASEAN bloc due to robust industrial expansion and competitive manufacturing costs. Strategic investments in electronics, automotive, and textile manufacturing propel regional DMPA demand, especially as governments incentivize eco-friendly production. Rapid urbanization and infrastructure spending create favorable markets for DMPA-enabled coatings, adhesives, and high-performance resins.

Competitive Landscape

The global DMPA market exhibits moderate concentration, with leadership by diversified chemical multinationals and a growing presence of regional manufacturers. Competitive strategies focus on vertical integration, portfolio diversification, and regional localization of production. Leading players are emphasizing R&D, process innovations, and sustainability-driven differentiation—key differentiators include emission-reducing synthesis processes, proprietary coating technologies, and partnerships with downstream end-users.

Key Market Developments

- April 2025: BASF expands its North American production capacity for DMPA, enhancing local supply security amid rising demand for eco-friendly automotive and industrial coatings.

- February 2025: Arkema SA introduces a new grade of high-purity DMPA designed for electronics applications, supporting miniaturized device encapsulation and environmental safety compliance.

- October 2024: Wacker Chemie AG develops a new series of waterborne resins utilizing DMPA, targeting the European architectural coatings segment and aligning with VOC reduction mandates.

Companies Covered in Dimethylolpropionic Acid (DMPA) Market

- Geo Specialty Chemicals, Inc.

- Perstorp Specialty Chemicals AB

- Henan Fianfu Chemical Ltd.

- Jiangxi Nancheng Hongdu Chemical Technology Development Co., Ltd.

- Shenzhen Vtolo Chemicals Co. Ltd.

- Lemman Laboratories International Co., Ltd.

- Biosynth Carbosynth

- Yigyooly Enterprise Limited

- Jiangxi Selon Industrial Co., Ltd.

- Wacker Chemie AG

- BASF

- Lanxess

- Dow Chemical Company

- Celanese Corporation

- Arkema SA

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Ineos Group

Frequently Asked Questions

The global market is valued at US$ 567.3 billion in 2025 and projected to reach US$ 809.0 billion by 2032, at a CAGR of 5.2%.

Regulatory pressure for lower VOC emissions and the shift to eco-friendly waterborne coatings are major demand drivers worldwide.

Polyurethane Dispersions (PUDs) hold the largest share owing to their performance and regulatory fit in coatings and adhesives.

North America leads the market, supported by high technological adoption and regulatory focus on green chemistry.

The development of DMPA-based materials for electronics and high-performance coatings is a major growth opportunity.

Major companies include BASF, Wacker Chemie AG, and Dow Chemical Company.