- Executive Summary

- Global Ethyl Acetoacetate Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026-2033, US$ Mn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Value Chain Analysis

- Macro-Economic Factors

- Global GDP Outlook

- Global Pharmaceutical Industry Overview

- Global Fertilizer Industry Overview

- Forecast Factors – Relevance and Impact

- COVID-19 Impact Assessment

- PESTLE Analysis

- Porter's Five Forces Analysis

- Geopolitical Tensions: Market Impact

- Regulatory and Technology Landscape

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Trends

- Price Trend Analysis, 2020 – 2033

- Region-wise Price Analysis

- Price by Segments

- Price Impact Factors

- Global Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Global Ethyl Acetoacetate Market Outlook: Product Type

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Product Type, 2020-2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- Market Attractiveness Analysis: Product Type

- Global Ethyl Acetoacetate Market Outlook: Application

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Application, 2020-2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- Market Attractiveness Analysis: Application

- Global Ethyl Acetoacetate Market Outlook: End-use Industry

- Introduction/Key Findings

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by End-use Industry, 2020-2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- Market Attractiveness Analysis: End-use Industry

- Global Ethyl Acetoacetate Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Mn) and Volume (Tons) Analysis by Region, 2020-2025

- Current Market Size (US$ Mn) and Volume (Tons) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- North America Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- North America Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- Europe Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Europe Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- Europe Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- Europe Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- East Asia Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- East Asia Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- East Asia Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- East Asia Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- South Asia & Oceania Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- South Asia & Oceania Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- South Asia & Oceania Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- South Asia & Oceania Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- Latin America Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Latin America Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- Latin America Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- Latin America Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- Middle East & Africa Ethyl Acetoacetate Market Outlook: Historical (2020 – 2025) and Forecast (2026 – 2033)

- Key Highlights

- Pricing Analysis

- Middle East & Africa Market Size (US$ Mn) and Volume (Tons) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Mn) and Volume (Tons) Forecast, by Product Type, 2026-2033

- Industrial

- Pharmaceutical

- Food

- Middle East & Africa Market Size (US$ Mn) and Volume (Tons) Forecast, by Application, 2026-2033

- Pharmaceutical

- Agrochemicals

- Dyes & Pigments

- Flavors & Fragrance

- Other

- Middle East & Africa Market Size (US$ Mn) and Volume (Tons) Forecast, by End-use Industry, 2026-2033

- Pharmaceutical

- Chemical

- Food & Beverage

- Cosmetics

- Agrochemical

- Other

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Eastman Chemical Company

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- Lonza Group AG

- Daicel Corporation

- Wacker Chemie AG

- Mitsubishi Chemical Corporation

- Hubei Jusheng Technology Co., Ltd.

- Zhejiang Realsun Chemical Co., Ltd.

- Laxmi Organic Industries Ltd.

- Henan Tianfu Chemical Co., Ltd.

- Jubilant Life Sciences Limited

- Eastman Chemical Company

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Specialty & Fine Chemicals

- Ethyl Acetoacetate Market

Ethyl Acetoacetate Market Size, Share, and Growth Forecast 2026 - 2033

Ethyl Acetoacetate Market by Product Type (Industrial Grade, Pharmaceutical Grade, Food Grade), Application (Pharmaceutical, Agrochemicals, Dyes & Pigments, Flavors & Fragrance, Other), End-use Industry (Pharmaceutical, Chemical, Food & Beverage, Cosmetics, Agrochemicals, Other), and Regional Analysis for 2026-2033

Ethyl Acetoacetate Market Size and Trend Analysis

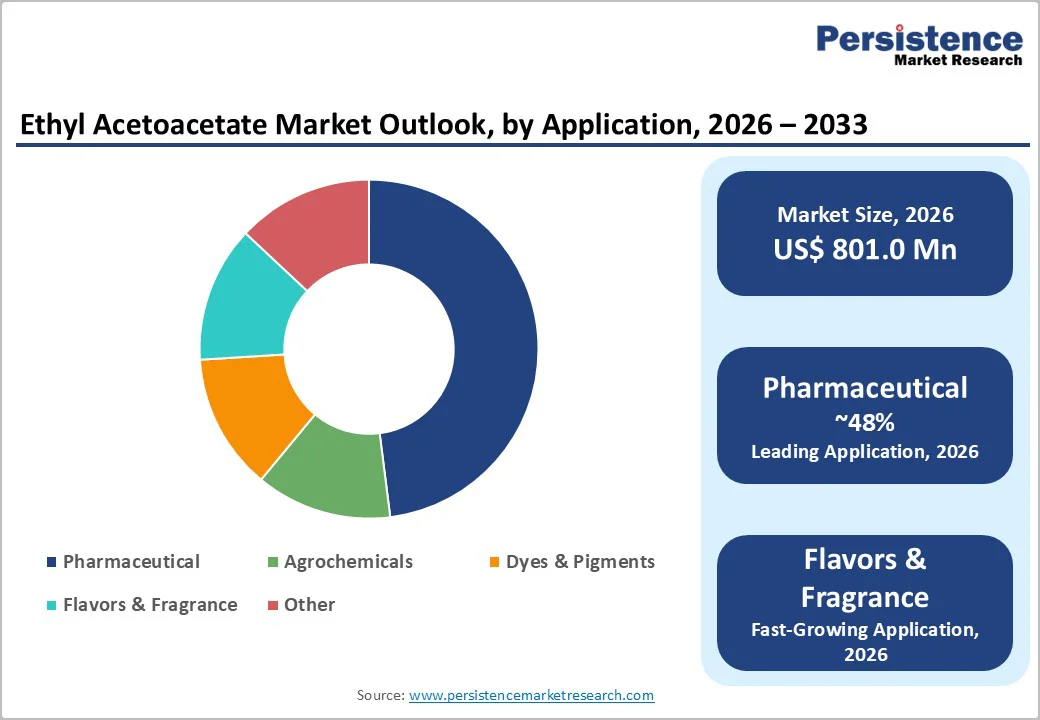

The global ethyl acetoacetate market size is supposed to be valued at US$ 801.0 Mn in 2026 and is projected to reach US$ 1,244.7 Mn by 2033, growing at a CAGR of 6.5% between 2026 and 2033.

The market’s growth is fueled by the rapid expansion of the pharmaceutical industry, driven by aging populations and the increasing prevalence of chronic diseases. This trend necessitates the ongoing development of innovative therapeutic molecules, which rely heavily on high-quality chemical intermediates. At the same time, the global agrochemical sector is driving significant demand for ethyl acetoacetate, a key raw material in pesticide and fungicide production. Furthermore, the chemical manufacturing industry’s shift toward sustainability and bio-based production methods is opening new opportunities. CropEnergies AG’s investment of US$130–140 million in a renewable ethyl acetate facility in Europe underscores the industry-wide transition toward environmentally responsible production practices.

Key Market Highlights

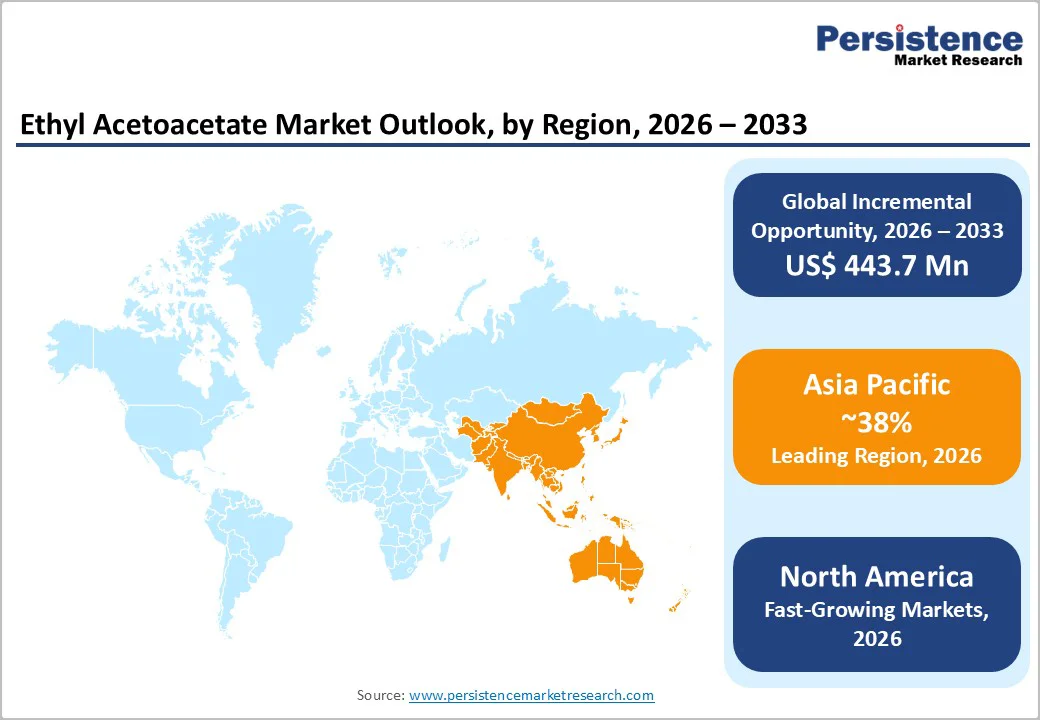

- Regional Leader: Asia Pacific dominates the global ethyl acetoacetate market with approximately 38% market share, driven by exceptional pharmaceutical manufacturing expansion and agrochemical sector growth.

- FastestGrowing Region: North America emerges as the fastest growing region, driven by the region’s sophisticated pharmaceutical manufacturing ecosystem and advanced chemical processing capabilities.

- Leading Segment: The pharmaceutical application segment, representing approximately 48% of total ethyl acetoacetate consumption, is driven by continuous drug development activities, expanding generic drug production, and emerging market pharmaceutical manufacturing growth.

- Fastest Growing Segment: Flavors and fragrances segments, supported by premium food and beverage market expansion, represent faster-growing application vectors with projected 7.0% CAGR growth trajectories during the forecast period.

- Key Market Opportunity: The bio-based ethyl acetoacetate segment represents a distinct high-growth market vector driven by regulatory imperatives, corporate sustainability commitments, and premium pricing opportunities.

| Key Insights | Details |

|---|---|

|

Ethyl Acetoacetate Market Size (2026E) |

US$ 801.0 Mn |

|

Market Value Forecast (2033F) |

US$ 1,244.7 Mn |

|

Projected Growth CAGR (2026-2033) |

6.5% |

|

Historical Market Growth (2020-2025) |

4.1% |

Market Dynamics

Market Growth Drivers

Expanding Pharmaceutical Synthesis and Active Pharmaceutical Ingredient Production

The pharmaceutical industry’s ongoing drive for innovative therapeutics and affordable generic drugs is the primary growth driver of the ethyl acetoacetate market. Ethyl acetoacetate serves as a critical building block in pharmaceutical synthesis, enabling efficient production of various active pharmaceutical ingredients through its facile acylation and alkylation reactions. The compound's role in synthesizing complex heterocyclic molecules commonly found in modern pharmaceutical formulations has made it indispensable for the efficient development of drugs, particularly for anti-inflammatory and analgesic medications.

The global pharmaceutical market is experiencing significant expansion, with North America accounting for 42% of the worldwide market share, reflecting strong demand for high-purity intermediates supporting advanced drug development. Meanwhile, the Asia-Pacific is expected to grow at a 3.7% CAGR, with India’s market creating substantial opportunities for API synthesis and generic drug manufacturing. India's significant presence in generic drug production and API synthesis, combined with China's expanding pharmaceutical manufacturing capabilities, drives substantial demand for specialized chemical intermediates that meet stringent 99.5% minimum purity standards.

Surge in Agrochemical Production Driven by Food Security Imperatives

The global agrochemical market is expanding rapidly, driven by rising demand for agricultural productivity and population growth. Ethyl acetoacetate is a critical raw material in agrochemical synthesis, particularly for the production of herbicides, fungicides, insecticides, and crop protection agents essential for yield optimization. Ethyl acetoacetate's ability to undergo cyclization reactions enables the construction of complex heterocyclic compounds essential for modern agrochemical formulations that enhance crop yields and protect against pests and diseases.

The pesticide and agricultural chemicals segment is reflecting strong growth momentum. China’s dominance in agrochemical manufacturing, with approximately 64% of global ethyl acetate production capacity and sophisticated supply chain infrastructure, facilitates robust availability of ethyl acetoacetate for downstream agrochemical manufacturers across the Asia-Pacific, Latin America, and emerging market regions. The development of integrated pest management solutions and bio-based agrochemical intermediates further expands application opportunities, as manufacturers seek versatile building blocks that support sustainable agriculture while meeting efficacy standards required for effective crop protection.

Market Restraints

Regulatory Compliance Complexity and Environmental Constraints

Increasingly stringent regulatory frameworks governing chemical manufacturing, particularly the EU REACH regulation and FDA quality standards, impose substantial compliance costs and technical requirements on ethyl acetoacetate producers. The European Union’s comprehensive regulatory architecture, including REACH Regulation (EC) No 1907/2006 and emerging restrictions on volatile organic compounds and per- and polyfluoroalkyl substances (PFAS), necessitates continuous investment in quality assurance, safety documentation, and sustainability certifications. Manufacturers must maintain rigorous environmental monitoring and possess

International Sustainability and Carbon Certification PLUS (ISCC+) credentials for bio-based products create barriers to entry for smaller producers and increase operational costs. Volatile raw material costs for acetic acid and ethanol, coupled with fluctuating petroleum prices and geopolitical supply chain disruptions, directly impact production economics, constraining profit margins for mid-tier manufacturers and limiting market accessibility for cost-sensitive downstream customers.

Supply Chain Concentration and Geopolitical Risk Exposure

The pronounced concentration of ethyl acetoacetate production capacity in China, representing approximately 64% of global capacity, creates substantial supply chain vulnerability and geopolitical risk exposure for global manufacturers. China’s production capacity of 3.8 Mn tons annually establishes overwhelming market dominance, potentially exacerbating price volatility and supply constraints during periods of elevated geopolitical tension or trade restrictions.

The historical precedent of antidumping duties imposed by South Korea and other nations against Chinese and Indian producers demonstrates protectionist tendencies that could fragment global markets and elevate import tariffs. Additionally, the capital-intensive nature of ethyl acetoacetate manufacturing facilities and the limited number of established producers create significant barriers to entry, preventing rapid capacity expansion to meet surging demand and potentially constraining market growth during cyclical demand upturns.

Market Opportunities

Bio-Based and Sustainable Production Methodologies Creating Premium Market Segments

The global shift toward carbon neutrality and circular economy principles is driving strong demand for renewable ethyl acetoacetate derived from sustainable feedstocks. The bio-based ethyl acetate market, projected to grow at 8.13% CAGR from US$254.21 million in 2024 to significant valuations by 2032, represents a high-margin growth segment. CropEnergies AG’s investment of US$130–140 million in a 50,000 tons/year green ethyl acetate facility in Germany, scheduled for commissioning by the end of 2025, underscores industry commitment to sustainable alternatives.

Similarly, Viridis Chemical LLC, the sole North American producer of 100% bio-based ethyl acetate with ISCC PLUS certification, serves pharmaceutical, food, and specialty chemical sectors, prioritizing sustainability. Regulatory initiatives such as the EU’s Eco-design for Sustainable Products Regulation (effective July 2024) and corporate ESG commitments are accelerating adoption across coatings, adhesives, pharmaceuticals, and food industries.

Specialty Application Development in Flavors, Fragrances, and Cosmetics Sectors

Emerging applications of ethyl acetoacetate in the rapidly growing flavors and fragrances sector present significant growth opportunities, supported by global food and beverage market expansion and rising consumer preference for natural aromatic compounds. Ethyl acetoacetate serves as a key solvent and extraction agent in flavor and fragrance formulations, enabling carrier functionality and sensory enhancement for premium products. The industry, integral to India’s rising pharmaceutical and consumer goods market, consumes substantial volumes for natural flavor extraction and the distribution of aromatic compounds.

Furthermore, its use in cosmetics, such as nail polish, mascara, and personal care products, leverages its low toxicity and rapid evaporation. The specialty pigments and dyes segment further drives demand by serving as a precursor in the synthesis of synthetic dyes and pigments.

Category-wise Insights

Product Type Analysis

Pharmaceutical-grade ethyl acetoacetate holds the leading position in the market, accounting for about 52% of the total share, driven by stringent purity standards and consistent demand from established pharmaceutical manufacturers. These products comply with USP, EP, and JP pharmacopoeia standards, requiring purity levels above 99.5% and rigorous impurity control to ensure drug safety and efficacy.

The industrial-grade segment is applied in serving chemical synthesis, coatings, and adhesive applications where slightly relaxed purity requirements enable cost-effective solutions. Food-grade ethyl acetoacetate, designated as E1504 under European regulations, commands premium pricing due to ultra-high purity exceeding 99.7%, meeting FCC, EFSA, and FDA CFR 21 standards. Pharmaceutical-grade dominance reflects uncompromising quality requirements and established regulatory pathways supporting compliant manufacturers.

Application Analysis

The pharmaceutical application segment leads the ethyl acetoacetate market, accounting for approximately 48% of the total share, driven by its critical role in active pharmaceutical ingredient synthesis and drug formulation. Its versatility in constructing complex molecules, particularly cephalosporin antibiotics, the largest single-product category, combined with rising global pharmaceutical R&D investments and emerging market drug development, ensures sustained demand.

The agrochemical segment holds around 28% share, supported by pesticide and fungicide production and projected 5.1% CAGR growth through 2034. Applications in dyes and pigments account for 14% of the market, driven by the textile industry's recovery and specialty coatings. Flavors and fragrances account for about 10%, driven by diversification in premium food, beverage, and cosmetics. This distribution underscores ethyl acetoacetate’s exceptional adaptability across diverse industries and its indispensable role in optimizing product formulations.

End-use Industry Analysis

The pharmaceutical industry accounts for approximately 45% of total market demand, spanning active pharmaceutical ingredient synthesis, contract manufacturing operations, and pharmaceutical research institutions that require consistent supplies of high-purity intermediates. The segment's leadership is reinforced by pharmaceutical industry consolidation in the Asia-Pacific regions, particularly China and India, where expanding API manufacturing capabilities and generic drug production create substantial intermediate demand. Jubilant Life Sciences Limited, through its CRDMO business, encompassing drug discovery services and API manufacturing, exemplifies the integrated pharmaceutical value chain that drives ethyl acetoacetate consumption.

The chemical manufacturing sector represents approximately 32% of consumption, encompassing fine chemical producers, specialty chemical manufacturers, and chemical distributors serving diverse downstream industries. The agrochemical sector’s indirect participation through chemical intermediate procurement underscores the market’s complex value chain architecture and the intermediate’s indispensable role across multiple industrial ecosystems.

Regional Insights

North America Ethyl Acetoacetate Trends

North America accounts for nearly 28% of the global ethyl acetoacetate market, supported by its advanced pharmaceutical manufacturing ecosystem and sophisticated chemical processing capabilities. The United States, representing 35% of the global pharmaceutical market and valued at US$635.31 billion in 2025, drives substantial demand for high-purity chemical intermediates essential for drug development and generic production.

Eastman Chemical Company, a leading regional producer, exemplifies innovation through proprietary synthesis technologies and its 2025 partnership with LanzaTech to scale circular ethyl acetate production using captured carbon. Robust regulatory frameworks established by the FDA and EPA, combined with strong quality assurance systems and intellectual property protections, provide competitive advantages. Additionally, onshoring initiatives, government incentives, and mature coatings and adhesives industries further enhance regional consumption and strengthen supply chain resilience.

Europe Ethyl Acetoacetate Trends

Europe holds approximately 26% of the global ethyl acetoacetate market, supported by stringent regulatory frameworks, advanced pharmaceutical manufacturing, and a strong shift toward bio-based production. The regional pharmaceutical market, valued at US$234 billion in 2024, demands premium-quality intermediates that meet rigorous compliance standards. Key manufacturing hubs include Germany, the United Kingdom, France, and Spain, where established contract manufacturers and fine chemical producers drive consistent procurement.

The EU’s regulatory environment, covering REACH Regulation (EC) No 1907/2006, Eco-design for Sustainable Products Regulation (ESPR), and restrictions on volatile organic compounds, creates significant opportunities for sustainable producers. Investments such as CropEnergies AG’s renewable ethyl acetate facility, scheduled for late 2025, highlight institutional commitment to green manufacturing. Additionally, Europe’s advanced coatings industry, supporting automotive and construction sectors, sustains robust demand for ethyl acetoacetate as a specialty solvent.

Asia Pacific Ethyl Acetoacetate Trends

Asia Pacific leads the global ethyl acetoacetate market, with approximately 38% share, driven by robust growth in pharmaceutical manufacturing, expanding agrochemical demand, and China’s dominant production capacity. China, the world’s largest producer, with 3.8 million tons annually (64% of global supply), benefits from an integrated chemical infrastructure that offers cost-efficient access to acetic acid and ethanol feedstocks.

India’s pharmaceutical sector, a cornerstone of the global generic drug supply chain, combines cost competitiveness with advanced manufacturing capabilities, creating significant demand for pharmaceutical-grade intermediates. Japan, South Korea, Malaysia, and Thailand contribute additional demand through fine chemical production and industrial expansion, reinforcing the region’s sustained growth trajectory.

Competitive Landscape

The ethyl acetoacetate market reflects moderate consolidation, with global production concentrated among a few established manufacturers and significant fragmentation among regional players serving niche and local markets. The competitive landscape is structured in two tiers: multinational chemical companies with integrated facilities, advanced R&D capabilities, and strong customer networks compete alongside specialized fine chemical producers targeting premium applications. Leading firms such as Eastman Chemical Company, Lonza Group AG, Daicel Corporation, and Wacker Chemie AG leverage vertical integration, proprietary technologies, and extensive distribution networks to maintain market leadership. Chinese manufacturers, including Wanglong Tech Co. Ltd., Nantong Acetic Acid Chemical Co. Ltd., and Anhui Tiancheng New Materials Co. Ltd., focus on cost efficiency and scale. Strategic priorities increasingly include bio-based production, sustainability certifications, process innovation, and supply chain transparency, supported by active mergers and acquisitions for vertical integration and geographic expansion.

Key Market Developments

August 2025: Eastman Chemical Company partnered with LanzaTech to scale circular ethyl acetate production utilizing captured carbon, demonstrating technological innovation in sustainable manufacturing while expanding North American production capacity and addressing environmental compliance objectives critical to pharmaceutical and specialty chemical customers.

November 2024: Jubilant Biosys Limited expanded its footprint in Europe through a strategic partnership, establishing a center of excellence for biologics and antibody-drug conjugates at the Saint Julien facility. This partnership enhances drug discovery services by combining 1,200 scientists from Indian centers of excellence in chemistry and CDMO capabilities.

March 2024: Jubilant Ingrevia commissioned a new facility to produce high-value esters, adding approximately 2,000 TPA of capacity and strengthening its diketene and derivatives platform, marking a strategic evolution toward accelerated growth and higher margins with the introduction of several downstream derivatives.

Top Companies in Ethyl Acetoacetate Market

Eastman Chemical Company (Kingsport, Tennessee, U.S.) represents the global market’s largest integrated chemical manufacturer, operating advanced ethyl acetoacetate production facilities with proprietary synthesis technologies and a demonstrated commitment to sustainable manufacturing innovations. The company commands substantial market share through extensive pharmaceutical and specialty chemical customer relationships, advanced research capabilities, and strategic investments in circular and bio-based production methodologies addressing evolving regulatory and sustainability requirements.

Lonza Group AG (Basel, Switzerland) operates as a leading specialty chemical and pharmaceutical ingredients manufacturer with established capabilities in ethyl acetoacetate production and a comprehensive customer support infrastructure serving pharmaceutical, agrochemical, and specialty chemical sectors. The company’s commitment to quality excellence, regulatory compliance, and sustainable manufacturing practices positions it as a trusted supplier for demanding pharmaceutical applications requiring rigorous purity specifications and documentation.

Daicel Corporation (Osaka, Japan) maintains prominent market positioning through integrated fine chemical production capabilities, established Japanese and Asia-Pacific market presence, and strategic focus on pharmaceutical and specialty chemical intermediates. The company’s manufacturing facilities, distributed across multiple global locations, provide regional supply security and comprehensive technical support serving diverse customer requirements across pharmaceutical synthesis, agrochemical applications, and specialty chemical formulations.

Companies Covered in Ethyl Acetoacetate Market

- Eastman Chemical Company

- Lonza Group AG

- Daicel Corporation

- Wacker Chemie AG

- Mitsubishi Chemical Corporation

- Hubei Jusheng Technology Co., Ltd.

- Zhejiang Realsun Chemical Co., Ltd.

- Laxmi Organic Industries Ltd.

- Henan Tianfu Chemical Co., Ltd.

- Jubilant Life Sciences Limited

Frequently Asked Questions

The global ethyl acetoacetate market is projected to reach US$ 1,244.7 Mn by 2033, expanding from US$ 801.0 Mn in 2026 at a 6.5% CAGR during the forecast period.The global ethyl acetoacetate market is projected to reach US$ 1,244.7 Mn by 2033, expanding from US$ 801.0 Mn in 2026 at a 6.5% CAGR during the forecast period.

The ethyl acetoacetate market is driven by exceptional pharmaceutical industry expansion, requiring continuous supplies of high-quality chemical intermediates.

The pharmaceutical application segment represents the dominant market category with approximately 48% market share, driven by continuous requirements for chemical intermediates in active pharmaceutical ingredient synthesis, particularly for cephalosporin antibiotic production.

North America emerges as the fastest-growing region, driven by the region’s sophisticated pharmaceutical manufacturing ecosystem and advanced chemical processing capabilities.

Bio-based and sustainable production methodologies represent the most significant emerging opportunity, with the bio-based ethyl acetoacetate market expanding at 8.13% CAGR and CropEnergies AG, Viridis Chemical LLC, and emerging producers investing substantially in renewable production facilities.

Eastman Chemical Company, Lonza Group AG, Daicel Corporation, and Wacker Chemie AG represent the established multinational manufacturers commanding substantial global market share.