- Specialty & Fine Chemicals

- High Density Polyethylene (HDPE) Bottles Market

High Density Polyethylene (HDPE) Bottles Market Size, Share, and Growth Forecast, 2025 - 2032

High Density Polyethylene (HDPE) Bottles Market by Product Type (Virgin HDPE, Others), Capacity (Up to 100 ml, 101-500 ml, Others), Application (Personal Care, Household Chemicals, Food & Beverages, Others), and Regional Analysis for 2025 - 2032

High Density Polyethylene (HDPE) Bottles Market Size and Trends Analysis

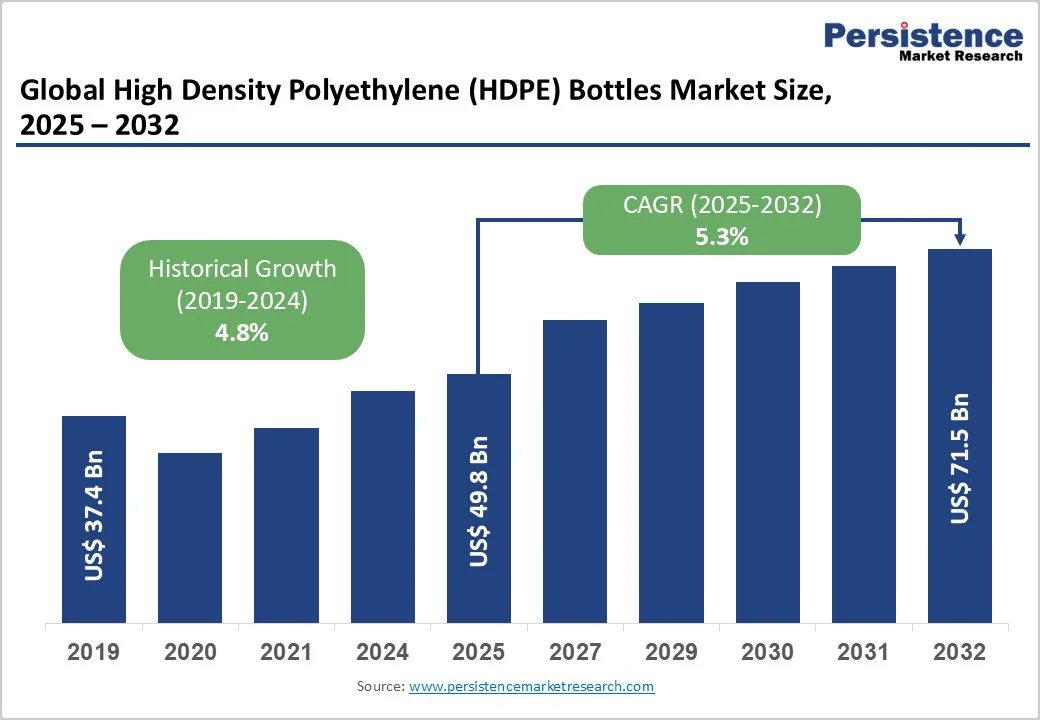

The global high density polyethylene (HDPE) bottles market size is likely to be valued at US$49.8 Billion in 2025 and is expected to reach US$71.5 Billion by 2032, growing at a CAGR of 5.3% during the forecast period from 2025 to 2032, driven by three interconnected macroeconomic and regulatory factors. Rising e-commerce adoption is fueling demand for secure, lightweight packaging solutions, while increasing food and beverage consumption in emerging economies further supports market expansion.

Regulations such as EPR and the EU Single-Use Plastics Directive drive recycled HDPE adoption, while advanced recycling and barrier-enhanced formulations help companies stay cost-efficient, sustainable, and competitively differentiated in mature markets.

Key Industry Highlights:

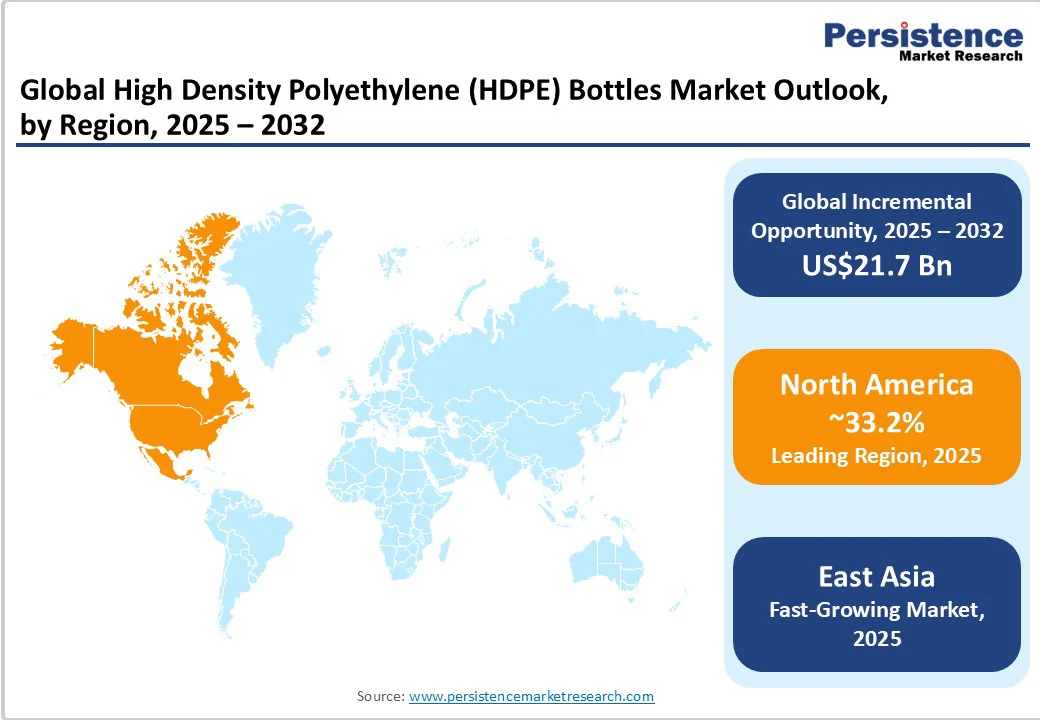

- Regional Leadership: North America dominates the global HDPE bottles market with a 33.2% share in 2025, supported by strong pharmaceutical, food, and personal care packaging demand and advanced e-commerce logistics networks.

- Fastest-Growing Region: East Asia stands as the fastest-growing region, driven by China’s capacity expansions and Japan-South Korea recycled content mandates accelerating rHDPE adoption.

- Material Dominance: Virgin HDPE leads with 72.0% share in 2025, driven by stringent food-grade purity requirements and long-standing certifications that limit rapid substitution by recycled grades.

- Fastest-growing Material Segment: Recycled HDPE (rHDPE) emerges as the fastest-growing category, propelled by EPR laws in the EU, Japan, India, and U.S. states mandating higher recycled content.

- Leading Capacity Segment: The 101-500 ml range holds 39.8% share in 2025, driven by large usage in household chemicals, personal care packaging, and standardized high-efficiency blow-molding production lines.

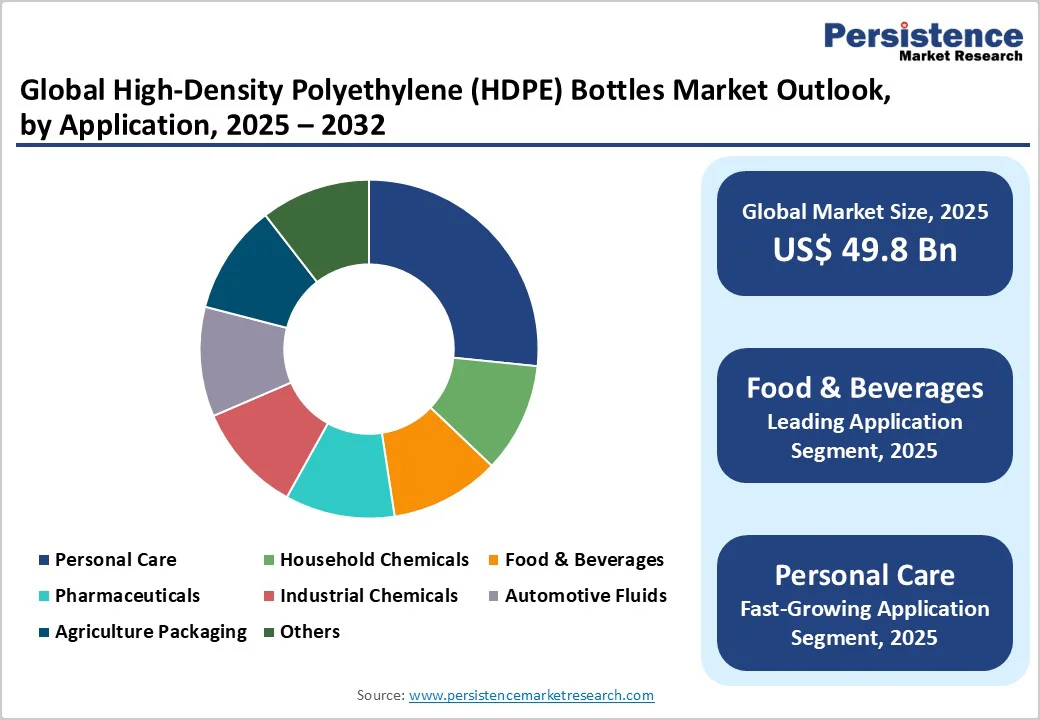

- Top Application Category: Food & Beverage remains the largest application segment with 28.1% share in 2025, anchored by HDPE’s moisture barrier strength and its dominance in dairy, oils, and juice packaging.

- Technology & Circularity Opportunity: Advanced mechanical and chemical recycling technologies enabling food-grade rHDPE present a major growth opportunity, unlocking a potential 22.3% share expansion as brands pursue 25-50% PCR targets by 2030.

| Key Insights | Details |

|---|---|

| High Density Polyethylene (HDPE) Bottles Market Size (2025E) | US$49.8 Bn |

| Market Value Forecast (2032F) | US$71.5 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Framework Mandating Recycled Content Integration

Global regulatory initiatives are significantly shaping demand in the high-density polyethylene (HDPE) bottles market. The EU’s Single-Use Plastics Directive, alongside Extended Producer Responsibility (EPR) frameworks in Canada and select U.S. states, requires manufacturers to integrate post-consumer recycled content, with targets often set at 25-50% by 2030.

These mandates create structural demand for recycled HDPE that is largely insulated from economic cycles. Similar measures are seen in Japan, where the Containers and Packaging Recycling Law stipulates a minimum recycled content of 10% in 2025, rising to 25% by 2030, fostering guaranteed procurement agreements between beverage fillers and recycled material suppliers.

Emerging markets such as India and China are also enforcing localized recycling mandates, prioritizing domestic material recovery. Consequently, manufacturers increasingly adopt dual-source supply chains to balance virgin and recycled feedstock while ensuring regulatory compliance and optimized capacity utilization.

E-Commerce Logistics Expansion and Protective Packaging Demand

The rise of e-commerce has significantly reshaped packaging demands across consumer goods and pharmaceuticals. In the EU, online retail grew from 14.2% of the total sales in 2020 to 17.1% by 2022, with continued expansion expected. This shift drives demand for packaging that withstands handling stress, temperature variations, and extended supply chain delays, capabilities well-matched by HDPE bottles.

HDPE offers superior impact resistance, moisture barriers, and thermal stability, minimizing damage-related returns and replacement costs. Growth is particularly pronounced in regions with advanced logistics infrastructure, where third-party logistics providers and brand owners collaborate on packaging optimization.

In urban China and India, e-commerce grocery fulfillment adds roughly 0.9% to regional HDPE bottle demand, while pharmaceutical adoption of temperature-stable, food-grade containers further accelerates market growth.

Barrier Analysis - Raw Material Cost Volatility and Margin Compression

Global HDPE bottle profitability is increasingly challenged by polyethylene feedstock price volatility, closely linked to crude oil and ethylene fluctuations. Six-month price swings of USD 60-80 per tonne create uncertainty for manufacturers with long-term contracts, disproportionately affecting mid-tier converters without upstream integration or hedging strategies.

Cost exposure includes both virgin and recycled HDPE, with recycled material margins under pressure when collection rates surpass demand, forcing absorption of excess inventory costs. In emerging markets, inadequate recycling infrastructure drives temporary premiums for food-grade recycled HDPE, sometimes 15-25% higher than virgin resin, reshaping competitive dynamics and favoring large, vertically integrated producers capable of managing supply chain and cost volatility.

Opportunity Analysis - Circular Economy Infrastructure Development and Localised Recycling Ecosystems

Emerging markets present significant opportunities for HDPE bottle manufacturers to develop localized recycling operations, supporting the transition to a circular economy. Governments in India, Southeast Asia, and Latin America are investing in mechanical and chemical recycling facilities, with India’s National Plastic Mission targeting over 5 million tonnes of collection annually by 2030.

Manufacturers establishing regional recycling partnerships and in-house reprocessing capabilities can command premium pricing and secure long-term contracts. Recycled HDPE represents the fastest-growing material segment. Vertical integration between bottle producers, waste management firms, and brand owners reduces virgin resin dependency while monetizing post-consumer HDPE.

Advanced Formulation Innovation and Food-Grade Recycled HDPE Development

Advances in HDPE formulation technology offer significant differentiation opportunities for manufacturers investing in R&D focused on barrier enhancement and contaminant tolerance in recycled streams.

Currently, recycled HDPE (rHDPE) faces adoption limits in food-contact applications due to contamination concerns and sensory property degradation, restricting its use to lower-value, non-food segments. Emerging mechanical sorting and chemical pre-treatment technologies enabling consistent food-grade rHDPE could unlock a 22.3% market share growth in the fastest-growing segment.

Innovations in advanced barrier coatings, including thin-film nanotechnology and active packaging, enhance shelf-life performance comparable to virgin HDPE while maintaining recycled content above 50%. Commercializing these formulations addresses regulatory compliance and sustainability commitments, creating premium market segments where patent-protected technologies and optimized processes generate value beyond commoditized offerings.

Category-wise Analysis

Product Type Insights

Virgin HDPE continues to dominate the market, holding a 72.0% share due to its established supply chain infrastructure, consistent material specifications, and proven performance across diverse applications. Structural advantages, including long-standing relationships with brand owners, manufacturing certifications, and regulatory approvals, create high switching costs that limit the adoption of alternative formulations.

Demand for virgin HDPE is particularly concentrated in food and beverage applications, where strict material purity and contamination sensitivity requirements restrict the use of recycled content, as current sorting and purification technologies are not yet widely available at scale.

Recycled HDPE (rHDPE), by contrast, represents the fastest-growing segment of the market, projected to capture 22.3% share in 2025 and significantly outpacing virgin HDPE growth.

This expansion is closely linked to regulatory pressures, including Extended Producer Responsibility frameworks and minimum recycled content mandates, which compel brand owners to integrate circular sourcing strategies into their supply chains. As a result, rHDPE offers both growth opportunities and a pathway for manufacturers to align with sustainability commitments while meeting emerging regulatory requirements.

Capacity Type Industry Insights

The 101-500 ml bottle capacity represents established market leadership with 39.8% market share, reflecting dominant positioning in household chemical applications, personal care formulations, and mid-scale food & beverage consumption patterns.

This capacity range demonstrates versatility across diverse application requirements while optimising manufacturing efficiency through standardized blow-molding processes and logistics cost management inherent to mid-scale container dimensions.

The 501-1,000 ml capacity demonstrates the fastest-growing market trajectory within the high density polyethylene (HDPE) bottles market, driven by shifting consumption patterns toward larger single-use formats in food and beverage categories, coupled with industrial packaging applications requiring mid-scale container solutions.

Application Industry Insights

Food & beverage applications hold the largest share of the global high-density polyethylene (HDPE) bottles market at 28.1%, highlighting HDPE’s superior suitability for beverage containerization. The material offers excellent moisture barrier properties, chemical inertness, and compliance with stringent food safety regulations across multiple jurisdictions.

HDPE is widely used in dairy packaging, including milk and yogurt beverages, as well as fruit juice containers and cooking oil formulations, where long-term shelf stability and consumer convenience drive preference over alternative materials. Its durability, lightweight nature, and cost-effectiveness reinforce its dominance in this critical application segment.

Personal care applications, meanwhile, represent the fastest-growing segment of the HDPE bottles market. Growth is propelled by rapid urbanization in emerging markets, increasing female workforce participation, and rising demand for personal care products.

Brand owners are also diversifying product formats across their portfolios, leveraging HDPE’s versatility and recyclability to introduce innovative packaging solutions that meet evolving consumer preferences, further accelerating adoption in this high-growth category.

Regional Insights

East Asia High Density Polyethylene (HDPE) Bottles Market Trends

East Asia represents the fastest-growing regional market for the high density polyethylene (HDPE) bottles market, with China and India collectively constituting substantial portions of global demand expansion.

Government official capacity expansion initiatives directly reflect manufacturing localisation priorities, where Sinopec expanded its Maoming Petrochemical complex HDPE production by 500,000 tonnes annually in 2024, addressing domestic consumption demands while reducing import dependency.

Key regional developments demonstrate concentrated momentum toward regulatory framework implementation aligned with European and North American sustainability standards, despite developmental stage differentiation. Japan's mandatory recycled content regulations, i.e., 10% in 2025, escalating to 25% by 2030, create definitive procurement obligations supporting recycled HDPE market development and collection infrastructure investment.

South Korea's 10% recycled content mandate, effective 2025, further reinforces regional regulatory convergence toward circular economy frameworks, generating structural demand for recycled material supply chains and processing infrastructure.

Europe High Density Polyethylene (HDPE) Bottles Market Trends

Europe represents the second-significant regional market, commanding approximately 20.2% of global market share in 2025, with regulatory environment intensity and circular economy framework implementation driving differentiated market dynamics relative to other developed regions.

The European packaging market achieved €214 Billion (US$248 Billion) in 2023 across all material categories, with HDPE maintaining established leadership in beverage, chemical, and household product containerization, supported by mature manufacturing infrastructure and established brand-owner relationships.

Regulatory environment impact demonstrates particular significance within Europe, where the Single-Use Plastics Directive and Extended Producer Responsibility frameworks establish binding constraints on virgin material consumption and recycled content requirements.

Germany leads European HDPE bottle manufacturing through an established industrial base, advanced manufacturing technologies, and vertical integration supporting competitive cost structures. The U.K. market demonstrates the fastest growth within the European region, driven by pharmaceutical packaging expansion and consumer goods market digitalisation, requiring enhanced e-commerce protective containerization.

North America High Density Polyethylene (HDPE) Bottles Market Trends

North America represents the largest regional market for the high density polyethylene (HDPE) bottles market, commanding approximately 33.2% of the global market share in 2025, reflecting mature consumer markets, established pharmaceutical infrastructure, and regulatory environments favoring plastic packaging innovation and circular economy implementation

The U.S. market specifically demonstrates sophisticated demand dynamics across the Food & Beverage, pharmaceutical, and personal care segments, supported by mature e-commerce logistics networks requiring protective containerization.

Key performance indicators within North America reflect dual market characteristics: established Food & Beverage consumption patterns supporting stable baseline demand, complemented by accelerating pharmaceutical and personal care segment expansion.

Manufacturing capacity utilisation demonstrates high efficiency levels across tier-one plastic converters, particularly following Amcor's October 2024 acquisition of Berry Global's rigid plastic division valued at US$8.4 Billion, creating integrated HDPE bottle and closure manufacturing ecosystems, enabling competitive cost structures and customer diversification.

Regulatory environment impact demonstrates particular significance within North America, where stringent FDA (Food and Drug Administration) and USP requirements drive compliance-based competitive differentiation.

Competitive Landscape

The global high density polyethylene (HDPE) bottles market is moderately consolidated, with leading players leveraging scale, recycling capabilities, and advanced molding technologies to strengthen their positions. Key companies, Amcor plc, Berry Global Group, ALPLA, Plastipak Holdings, and Gerresheimer AG, dominate across personal care, household, food, and industrial applications.

These firms focus on PCR integration, lightweighting, and design customization to meet sustainability regulations and brand requirements. Sonoco Products Company and Graham Packaging further intensify competition by expanding regional production and offering high-performance, specialty HDPE bottle solutions.

Key Industry Developments

- In January 2025, ALPLA expanded its South American HDPE recycling capacity by acquiring a majority stake in Brazilian recycler Clean Bottle, establishing a Paraná plant producing 15,000 tonnes of rHDPE annually to meet rising regional demand for recycled bottles.

- In June 2024, Berry Global Group launched the 250ml Domino HDPE bottle, made with up to 100% post-consumer recycled plastic. Fully recyclable, customizable with four-sided printing and embossing, it supports low MOQs, rapid delivery, and multiple closures for beauty, home, and personal care applications.

Companies Covered in High Density Polyethylene (HDPE) Bottles Market

- Amcor plc.

- Berry Global Group, Inc.

- ALPLA

- Gerresheimer AG

- Plastipak Holdings, Inc.

- Sonoco Products Company

- Berk Company LLC

- CL Smith

- RPC Group Plc

- Graham Packaging

- Nampac Limited

Frequently Asked Questions

The global high density polyethylene (HDPE) bottles market is projected to be valued at US$49.8 Billion in 2025.

The virgin HDPE segment is expected to hold around 72.0% market share by product type in 2025.

The high-density polyethylene (HDPE) bottles market is expected to witness a CAGR of 5.3% from 2025 to 2032.

The high-density polyethylene (HDPE) bottles market growth is primarily driven by global regulatory mandates requiring recycled content integration and the rising demand for protective packaging, fueled by expanding e-commerce and pharmaceutical logistics.

"Significant market opportunities exist in building circular economy infrastructure through localized recycling networks and in developing food-grade recycled HDPE formulations that comply with regulations and cater to premium packaging requirements.

The leading global players in the high density polyethylene (HDPE) bottles market include Amcor plc, Berry Global Group Inc., ALPLA, Gerresheimer AG, Plastipak Holdings Inc., Sonoco Products Company, Berk Company LLC, CL Smith, RPC Group Plc, Graham Packaging, and Nampac Limited.