- Specialty & Fine Chemicals

- Vinyl Acetate Ethylene (VAE) Copolymer Powder Market

Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Size, Share, and Growth Forecast, 2026 – 2033

Vinyl Acetate Ethylene (VAE) Copolymer Powder Market by Application (Adhesives, Paints & Coatings, Redispersible Polymer Powders, Textile Chemicals & Finishing, Paper & Packaging, Carpet Backing, Others), End-Use Industry (Construction & Building, Packaging & Paper, Textiles & Carpet, Consumer & Industrial Coatings, Automotive & Transportation, Others), and Regional Analysis for 2026–2033

Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Share and Trends Analysis

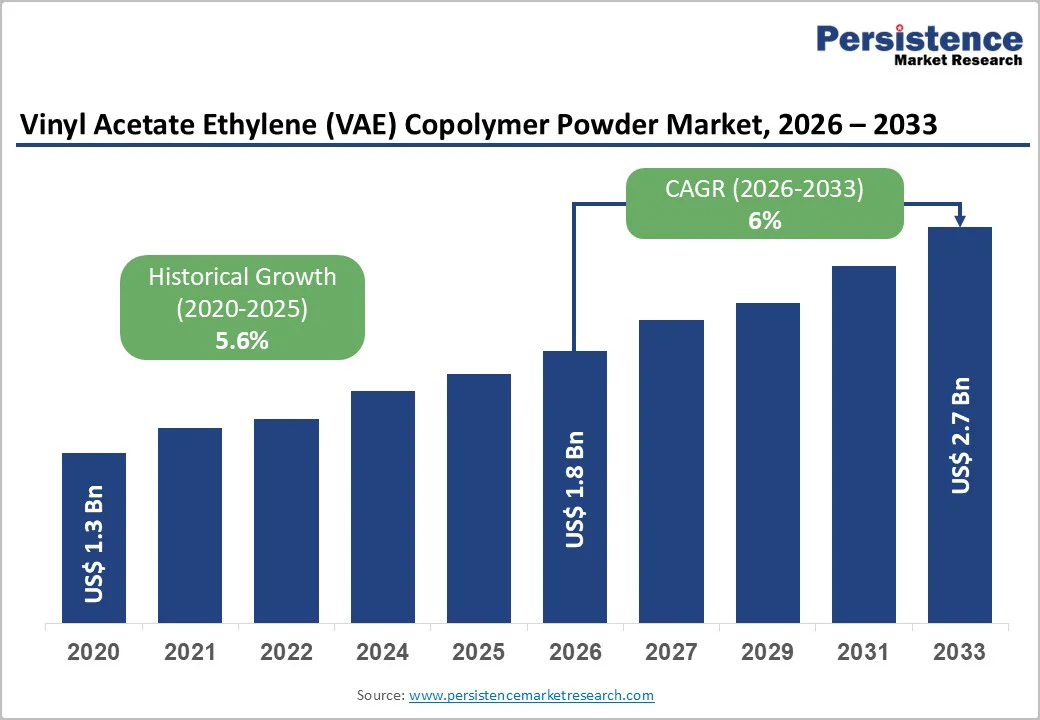

The global vinyl acetate ethylene (VAE) copolymer powder market size is likely to be valued at US$ 1.8 billion in 2026, and is projected to reach US$ 2.7 billion by 2033, growing at a CAGR of 6% during the forecast period 2026-2033. The growth trajectory of this market is primarily influenced by expanding construction output, increasing shift toward water-based adhesives in compliance with volatile organic compound (VOC) standards, and broader adoption of redispersible polymer powders in cementitious applications. Rising consumption in packaging, textiles, and industrial coatings further strengthens long-term stability.

Key Industry Highlights

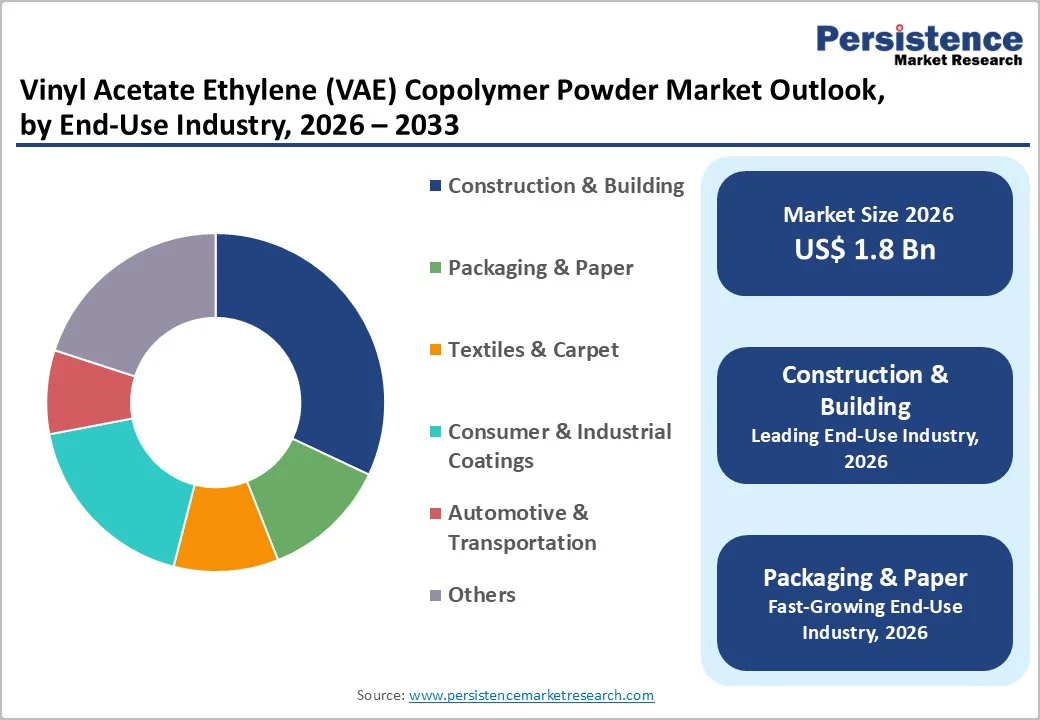

- Leading End-Use Industry: Construction & building is expected to lead with around 32% revenue share in 2026, driven by the dominant use of mortars and tile adhesives.

- Fastest-Growing End-Use Industry: Packaging & paper is projected to grow the fastest at roughly 6.4% CAGR between 2026 and 2033, supported by the rising demand for water-based packaging adhesives.

- Application Dominance: Adhesives are projected to dominate with an estimated 39% share in 2026, fueled by the rapid transition toward water-based adhesive systems.

- Fastest-Growing Application: Redispersible polymer powders (RDPs) are expected to grow the fastest at 7.2% CAGR through 2033, aided by escalating infrastructure spending in major economies.

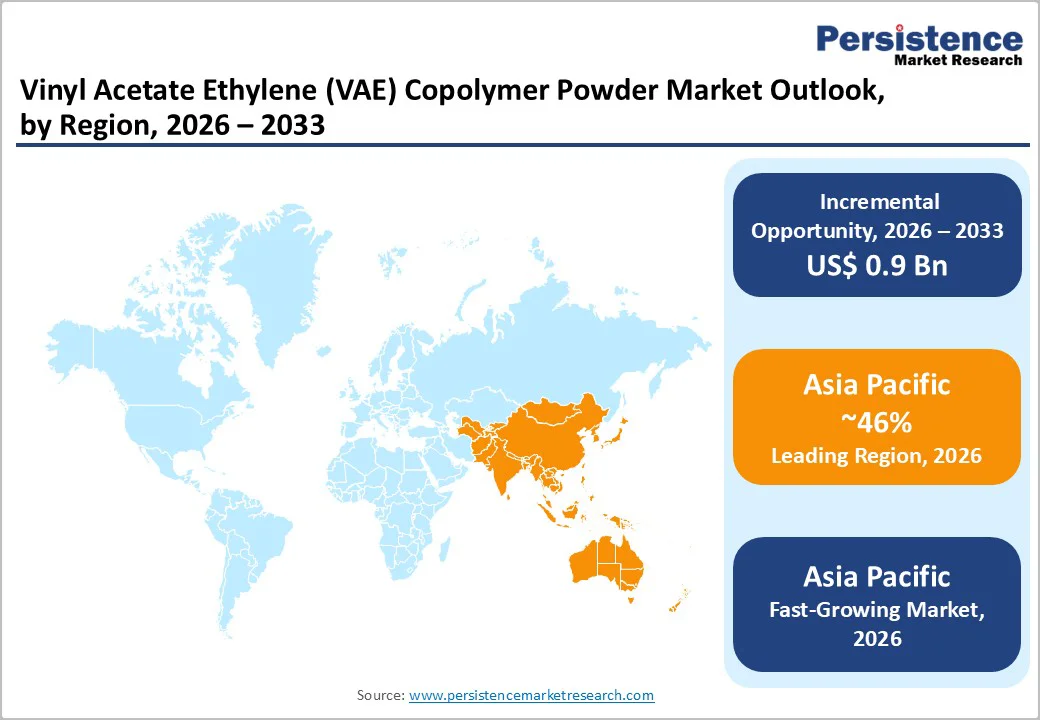

- Dominant Region: Asia Pacific is anticipated to command around 46% market share in 2026, driven by large-scale construction activities and textile sector expansion in China, India, and ASEAN.

| Report Attribute | Details |

|---|---|

|

Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Size (2026E) |

US$ 1.8 Bn |

|

Market Value Forecast (2033F) |

US$ 2.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6 % |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Demand for Low-Emission Construction & Packaging Adhesive Solutions

The expansion of construction projects around the globe, coupled with increasingly stringent environmental regulations, is driving widespread adoption of vinyl acetate ethylene copolymer powders in a variety of building materials. In emerging markets, where infrastructure development is accelerating, construction professionals are prioritizing binders that deliver improved adhesion strength, flexibility, and water resistance. VAE copolymer powders meet these performance needs while also supporting compliance with low VOC standards. Regulatory frameworks that promote environmentally friendly material formulations have encouraged manufacturers to move away from solvent-based chemistries, further boosting the use of VAE-based solutions. As a result, VAE copolymer powders are now recognized as critical additives for enhancing the durability and sustainability of modern cementitious systems.

The rapid growth of flexible packaging and paper-based alternatives is also increasing the demand for VAE formulations in coatings, lamination, and paper adhesives. Packaging producers favor VAE copolymer powders due to their excellent film-forming properties, compatibility with a wide range of substrates, and alignment with the shift toward recyclable and compostable packaging materials. The rise of e-commerce and evolving consumer preferences for sustainable packaging solutions are reinforcing the transition to water-based adhesive technologies.

Raw Material Instability and Competitive Pressure from Substitute Binders

Volatility in the prices of core inputs, including ethylene and vinyl acetate monomer (VAM), continues to disrupt planning for VAE copolymer powder producers. Energy price swings, unplanned outages, and logistics constraints can tighten supply and move costs quickly, which directly affects conversion economics and contract negotiations. When raw material costs rise sharply, buyers often slow procurement, adjust inventory strategies, or reformulate in the near term to protect budgets. This behavior creates uneven order patterns across construction, packaging, and textiles, and it forces suppliers to actively balance margin protection with service reliability.

VAE also competes with well-established binder technologies, including styrene butadiene rubber (SBR), polyurethane dispersions (PUD), and acrylic systems that already meet demanding performance specifications in many end uses. In applications that require high water resistance, chemical durability, or proven long-term performance, formulators may default to incumbent materials, especially when they perceive switching risk or qualification costs. Mature markets with entrenched acrylic-based recipes often offer limited incentives to change unless VAE delivers a clear cost or sustainability advantage at equivalent performance.

Growing Demand for Sustainable Construction, Textiles, and Packaging Solutions

Global mandates regarding sustainability and a rising preference for low-emission materials are significantly boosting the adoption of VAE-based polymers. Initiatives centered on green construction stimulate the use of low-VOC mortars, flexible tile adhesives, and lightweight renders, which strengthens the market for redispersible polymer powders. As procurement teams prioritize environmental, social, & governance (ESG) targets, builders are shifting toward clean-chemistry binders that support energy efficiency and low-carbon objectives. This transition establishes VAE products as critical components in next-generation building solutions that adhere to strict environmental compliance. Increasing capital allocation for infrastructure projects in both emerging and mature economies further amplifies this upward trajectory.

Parallel advancements in eco-friendly textiles and packaging reinforce this market potential as industries search for binders that offer improved softness, reduced toxicity, and compatibility with recyclable substrates. Textile manufacturers in Asia are expanding their application of VAE solutions for non-woven fabrics, carpet backings, and finishing processes. Industry events vividly illustrate this shift. For example, at CHINAPLAS 2025 in Shenzhen, BASF Societas Europaea (SE) highlighted its "#OurPlasticsJourney" campaign. This exhibition showcased technologies such as chemical and mechanical recycling, biomass-balanced materials, and low-carbon plastic innovations. These trends underscore a growing demand for VAE adhesives and coatings that facilitate strong bonding and cleaner end-of-life performance, creating a substantial opportunity for producers to serve environmentally aligned sectors.

Category-wise Analysis

Application Insights

Adhesives are expected to hold the leading position with approximately 38% of the VAE copolymer powder market revenue share in 2026, supported by broad usage in woodworking, packaging, and consumer goods, where the compound ensures flexibility and strong bonding. Their dominance is reinforced as industries steadily shift from solvent-based to water-based systems to meet low-VOC requirements. The segment benefits from consistent demand across paper converting and industrial adhesive lines, making it the most widely adopted application. VAE’s balanced performance and environmental compliance help maintain stable long-term penetration. As regulations tighten globally, adhesive manufacturers increasingly adopt VAE formulations. This keeps the segment structurally strong across both mature and emerging markets.

Redispersible polymer powders are likely to grow fastest with roughly 9.8% CAGR through 2033, supported by their expanding use in tile adhesives, self-leveling compounds, and high-strength mortars. In 2025, for example, Wacker expanded its RDP production capacity by 20,000 metric tons annually to meet rising demand across tiling, external thermal insulation composite systems (ETICS), and leveling applications, reflecting increasing market scale and commitment. Rapid urban development and construction activity in Asia further fuel adoption. RDPs enhance adhesion, flexibility, and crack resistance, making them essential for performance-driven formulations. Sustainability trends promoting low-emission mortars strengthen the competitive edge of VAE-based RDPs. Their integration across architectural, flooring, and repair applications underscores broad market relevance.

End-Use Industry Insights

The construction & building industry is projected to lead with an estimated 42% of the vinyl acetate ethylene copolymer powder market revenue share in 2026, driven by the heavy use of VAE in mortars, tile adhesives, EIFS, and concrete repair systems. Its dominance is reinforced by rising global infrastructure spending and the adoption of low-carbon building materials. The ability of VAE copolymer powder to enhance workability, bonding, and durability supports high consumption across new construction and renovation cycles. Growing emphasis on green materials further strengthens its relevance. The segment maintains a stable outlook due to continuous investment in residential and commercial development. This ensures construction remains the primary demand center for VAE products globally.

The textiles & carpet industry is expected to emerge as the fastest-growing, registering the highest CAGR of about 8.6% during the 2026–2033 forecast period, supported by expanding manufacturing capacity across India, Bangladesh, Vietnam, and Indonesia. VAE’s softness, clean chemistry profile, and strong film-forming behavior enhance adoption in non-wovens and carpet backing. Export-oriented factories increasingly prefer low-emission binders to meet global compliance expectations. Rising demand for performance textiles in furnishings and automotive interiors accelerates usage. The trend toward sustainable inputs encourages broader integration of VAE formulations.

Regional Insights

North America Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Trends

North America is expected to hold approximately 27% of the VAE copolymer powder market share in 2026, led by the U.S., where its demand spans construction chemicals, packaging adhesives, and non-woven materials. Regulatory focus on low-VOC systems accelerates the adoption of water-based VAE formulations, reinforcing their use in architectural and industrial applications. Established manufacturing infrastructure and high-quality standards support durable and environmentally compliant products. Renovation spending and infrastructure upgrades provide a stable demand base. Packaging converters increase VAE usage to meet sustainability expectations. Overall, North America maintains a consistent growth pattern supported by technology adoption and regulatory compliance.

Innovation in polymer emulsions and next-generation adhesives strengthens the position of North America in this market, while bio-based chemistry initiatives expand application scope. Distribution networks continue to grow to serve construction and packaging hubs efficiently. Demand in non-wovens for hygiene and filtration applications further contributes to incremental growth. Builders and converters prioritize performance and environmental compliance, supporting long-term market stability and ensuring North America remains a reliable contributor to global VAE consumption.

Europe Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Trends

Europe is likely to account for around 24% of the vinyl acetate ethylene copolymer powder market share in 2026, driven by Germany, France, the U.K., and Spain, where VAE demand in construction chemicals, sustainable packaging, and industrial coatings is robust. Stringent environmental and chemical compliance standards favor low-VOC VAE systems. Renovation and new construction activity reinforce usage in mortars, tile adhesives, and finishing materials. High-performance adhesives and recyclable packaging drive adoption across multiple sectors. Circular economy initiatives further encourage VAE integration in eco-friendly solutions. Europe’s mature market demonstrates steady expansion supported by regulatory alignment and sustainability focus.

Advanced manufacturing capabilities and investment in energy-efficient production bolster Europe’s competitive positioning. Industrial coatings and specialty adhesives increasingly incorporate VAE for enhanced flexibility and environmental performance. Export-oriented packaging and engineered materials demand reliable VAE formulations. Adoption trends are supported by member state regulations promoting low-emission construction and industrial products. Technology-driven innovation ensures continuous relevance across sectors. Europe maintains stable long-term growth prospects with a focus on performance and sustainability.

Asia Pacific Vinyl Acetate Ethylene (VAE) Copolymer Powder Market Trends

Asia Pacific is expected to command an estimated 46% of the market share in 2026 and is also likely to be the fastest-growing regional market for VAE copolymer powder, exhibiting a 2026-2033 CAGR of close to 9%. Market prospects here are brightened by surging pace of construction activity, expanding textile manufacturing, and rising packaging consumption in China, India, and ASEAN countries. China leads with high use of mortars, tile adhesives, and cementitious materials. India and Southeast Asia support growth through urbanization, infrastructure investment, and competitive manufacturing. The region’s cost advantages and raw material availability enhance production efficiency. E-commerce-driven packaging demand increases VAE adoption. Textile finishing and carpet backing expand with low-emission and flexible binder requirements.

Government initiatives promoting affordable housing and industrial modernization further stimulate VAE consumption. Capacity expansion by regional producers ensures reliable supply and supports exports. Growth in non-woven applications, specialty coatings, and eco-friendly packaging strengthens the market. Sustainability trends encourage wider VAE integration across construction, textiles, and packaging. Asia Pacific’s diversified demand base underpins consistent market momentum.

Competitive Landscape

The global vinyl acetate ethylene copolymer powder market structure is moderately consolidated. Key regional players, including Sinopec, Shaanxi Xutai Technology, Wanwei, and Dairen Chemical Corporation (Vinavil), are focusing on construction, adhesives, coatings, and packaging applications. Their localized production capabilities, cost advantages, and proximity to raw material sources enable rapid response to rising regional demand. Global leaders such as Wacker Chemie AG, Dow, Celanese, BASF, Synthomer, and Arkema also actively supply the APAC market, leveraging strong distribution networks and R&D investments to deliver high-performance VAE powders. The combined presence of multinational and regional companies intensifies competitive dynamics while ensuring wide availability and product innovation.

Emerging producers targeting the Asia Pacific market are capturing niche opportunities in redispersible polymer powders, non-woven textiles, and eco-friendly packaging binders. Flexible manufacturing setups allow rapid scaling to meet urbanization-driven construction, packaging, and textile demand. Investment in sustainable, low-VOC, and water-based formulations enhances market differentiation. Strategic partnerships, capacity expansions, and technology licensing strengthen regional competitiveness.

Key Industry Developments

- In April 2025, Wacker announced a price increase of up to 5% for dispersions and dispersible polymer powders effective May?1, 2025, reflecting rising raw material costs and potential downstream price pass-through in adhesives, construction chemicals, and coatings.

- In April 2025, BASF launched a chemical-recycling solution for polyamide (Ultramid® Ccycled®) in collaboration with a major supplier, highlighting industry shifts toward circular and low-impact materials, which may drive demand for eco-friendly VAE-based binders.

- In March 2025, Asian Paints announced plans for a new vinyl acetate monomer (VAM) and vinyl acetate emulsion (VAE) facility in Dahej, Gujarat, via Asian Paints (Polymers) Private Limited (APPPL), including Ethylene storage. The board approved a cost revision from INR 25.60 billion to INR 32.50 billion, funded by equity and debt to bolster manufacturing capabilities.

Companies Covered in Vinyl Acetate Ethylene (VAE) Copolymer Powder Market

- Wacker Chemie AG

- Dow Inc.

- Celanese Corporation

- BASF SE

- Synthomer plc

- Arkema SA

- Exxon Mobil Corporation

- Sinopec Corporation

- Shaanxi Xutai Technology Co., Ltd.

- Wanwei

- Dairen Chemical Corporation

- Gantrade Corporation

- Ashland Global

Frequently Asked Questions

The global vinyl acetate ethylene (VAE) copolymer powder market is projected to reach US$ 1.8 billion in 2026.

Rising construction activity, infrastructure spending in Asia Pacific, regulatory push toward low-VOC water-based adhesives, and increasing demand for sustainable and high-performance binders in textiles, coatings, and packaging are driving the market.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

Formulation of sustainable construction materials and low-VOC adhesives, growth in textile finishing and carpet backing, eco-friendly paper and packaging solutions, and expansion of production capacity in high-growth Asia Pacific markets present lucrative opportunities.

Wacker Chemie AG, Dow, Celanese Corporation, BASF SE, Synthomer plc, and Sinopec are some of the key players in the market.