- Medical Devices

- ENT Devices Market

ENT Devices Market Size, Share, Trends, Growth, and Forecasts (2025 - 2032)

ENT Devices Market by product (surgical devices, hearing devices, nasal instruments, image-guided surgery systems, and CO₂ lasers), by Application (in otology and rhinology, laryngology, and sleep apnea), by End-Use (hospitals, ENT clinics, ambulatory surgical centers (ASCs), and homecare settings), and Regional Analysis for 2025 - 2032.

ENT Devices Market Size and Forecast Analysis

Market Overview

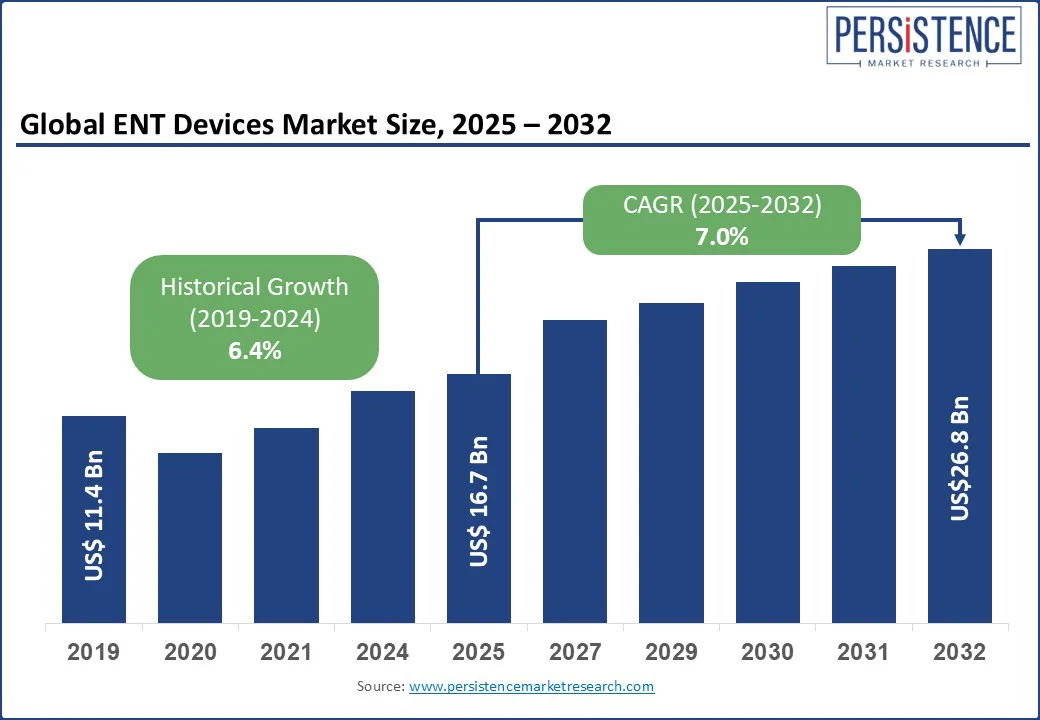

The global ENT devices market size is expected to reach US$ 16.7 billion in 2025. It is expected to reach US$ 26.8 billion by 2032, growing at a CAGR of 7.0% during the forecast period (2025 - 2032). This growth is driven by an increasing prevalence of ENT disorders, an aging global population, and rising demand for minimally invasive diagnostic and surgical procedures.

The global ENT (Ear, Nose, and Throat) devices encompass a wide range of products. This growth is also supported by advancements in diagnostic technologies, such as endoscopes and surgical navigation systems, and the rapid adoption of hearing aids enhanced by digital and AI-based features. Government initiatives to improve hearing healthcare and early diagnosis programs further boost market development, especially in emerging economies. North America dominates the global ENT devices market due to its advanced healthcare infrastructure and high awareness, followed by Europe, with strong adoption of advanced ENT treatment devices. The Asia Pacific region is the fastest-growing market, driven by increasing healthcare expenditure, large patient pools, and expanding access to ENT care in countries like China, India, and Japan.

Market Dynamics

Drivers

- Rising Prevalence of ENT Disorders:

The rising prevalence of ENT disorders is a major driver of growth in the ENT devices market. According to the World Health Organization (WHO), over 1.5 billion people globally experience some degree of hearing loss, while approximately 700 million suffer from chronic sinusitis. This increasing disease burden is fueling demand for advanced diagnostic and surgical ENT devices. For instance, the growing number of patients with chronic sinus issues has led to wider adoption of ENT devices for sinus treatment, such as balloon sinuplasty systems and nasal endoscopes. These innovations enhance precision and patient outcomes, particularly in minimally invasive ENT procedures.

- Aging Population:

The aging global population is significantly impacting the ENT devices market. By 2050, the number of people aged 65 and above is expected to reach 1.5 billion, leading to a sharp rise in age-related ENT conditions such as presbycusis, or age-related hearing loss. This demographic shift is contributing to a 12% annual increase in demand for hearing devices. For instance, elderly patients are increasingly opting for advanced hearing aids equipped with Bluetooth connectivity and noise-cancellation features to improve communication and quality of life. As life expectancy rises, the need for reliable ENT care tools tailored to older adults continues to grow.

Restraints

- Regulatory Hurdles:

Regulatory hurdles present a significant restraint in the ENT devices market, often delaying product development and commercialization. Agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) enforce stringent requirements for safety, efficacy, and clinical validation. For instance, the approval process for innovative ENT surgical devices such as image-guided surgical systems or next-gen cochlear implants can take 12 to 18 months due to extensive clinical trials and documentation. These delays increase time-to-market and development costs for manufacturers. Smaller companies, in particular, face challenges in navigating these complex regulatory landscapes, which can hinder innovation and limit global market penetration.

Opportunities

- Expansion in Emerging Markets:

The expansion of emerging markets presents a significant opportunity for growth in the ENT devices market. Rapidly developing healthcare infrastructure, rising healthcare spending, and increasing awareness of ENT disorders in regions such as Asia Pacific and Latin America are driving demand. For instance, India’s healthcare market is projected to, fueled by government initiatives such as Ayushman Bharat. This creates substantial demand for affordable and advanced ENT care tools, including hearing aids, endoscopic devices, and surgical instruments. Similarly, countries such as Brazil and Indonesia are investing in healthcare modernization, further supporting ENT market expansion.

- Advancements in Hearing Aid Technology:

Innovations such as AI-driven sound processing, Bluetooth connectivity, and real-time noise filtering are transforming traditional hearing aids into smart, personalized solutions. For instance, AI-enabled hearing aids can automatically adjust to different sound environments, improving user experience and speech clarity. This level of customization is increasingly appealing to tech-savvy consumers and the aging population. As a result, these digital innovations are expected to drive, positioning them as a key segment in personalized hearing care.

Category- wise Analysis

Product Type Insights

- Hearing devices dominate the ENT devices market, holding a 40% share in 2025. Their widespread adoption is driven by the high prevalence of hearing loss globally, particularly among the aging population. Technological advancements such as Bluetooth-enabled, AI-integrated, and rechargeable digital hearing aids have significantly improved user experience, driving greater acceptance.

- Image-guided surgery systems are projected to grow rapidly, fueled by the rising demand for minimally invasive ENT procedures. These systems enhance surgical precision in otology, rhinology, and skull base surgeries, reducing recovery times and improving patient outcomes. Integration of 3D imaging, navigation technologies, and real-time data during procedures is expanding their application across ENT specialties.

Application Insights

- Otology and rhinology applications are driven by the high incidence of hearing loss, sinusitis, and chronic ear infections globally. The aging population and increasing exposure to noise pollution further contribute to the demand for otologic interventions. Advancements in middle ear implants, cochlear implants, and balloon sinuplasty are enhancing treatment outcomes and supporting market growth.

- Sleep apnea applications are expected to grow steadily, propelled by rising awareness of sleep disorders and the health risks associated with untreated apnea. The demand for continuous positive airway pressure (CPAP) devices, oral appliances, and minimally invasive surgical tools is increasing. Technological innovations such as home-based sleep monitoring systems and AI-powered diagnostics are improving early detection and treatment compliance.

End-User Insights

- Hospitals hold the largest share, contributing a significant portion of the market revenue in 2025, due to their advanced infrastructure, skilled medical professionals, and high patient footfall for ENT procedures such as surgeries and diagnostics. The availability of specialized ENT departments and access to image-guided surgical systems further strengthen hospital dominance in the market.

- Homecare settings are projected to grow rapidly, driven by the increasing availability of compact and portable ENT devices, such as digital otoscopes and hearing aids. The rise of telehealth services and remote monitoring solutions has made at-home ENT care more accessible, especially for elderly patients and those in rural areas.

Regional Insights

North America ENT Devices Market Trends

North America holds the largest share of the global ENT devices market, at 38% in 2025, with the United States contributing significantly due to its advanced healthcare infrastructure and rapid adoption of cutting-edge ENT technologies. The U.S. ENT Devices Market growth is highlighted based on:

- High Disease Prevalence: Over 50 million Americans suffer from hearing loss or ENT-related disorders, driving substantial demand for hearing aids, diagnostic equipment, and surgical tools.

- Technological Innovation: U.S.-based companies account for 60% of global ENT device R&D spending, with firms like Cochlear Ltd. and Demant A/S introducing AI-powered hearing aids and smart diagnostic systems.

- Favorable Reimbursement Policies: Government programs such as Medicare and private insurance support ENT procedure coverage, contributing to ENT device adoption across clinical and home care settings.

Europe ENT Devices Market Trends

Europe holds a 32% share of the global ENT devices market, with Germany, France, and the U.K. leading regional growth in 2025. The market is driven by rising demand for advanced ENT solutions and strong government healthcare support across key nations:

- Germany: The country’s advanced medical device manufacturing capabilities and high healthcare expenditure drive the adoption of ENT surgical equipment, particularly in otology and rhinology.

- U.K.: The National Health Service (NHS) prioritizes improved ENT care delivery, while a 15% rise in sleep apnea diagnoses is increasing demand for diagnostic and minimally invasive ENT surgical tools.

- France: Market growth is fueled by robust government investment in minimally invasive ENT procedures and strong demand for image-guided surgery systems in public and private hospitals.

Asia Pacific ENT Devices Market Trends

Asia Pacific is the fastest-growing region in the global ENT devices market, led by expanding healthcare infrastructure, rising awareness, and large patient populations across key countries:

- India: Government programs like Ayushman Bharat, which cover over 500 million people, are significantly improving access to ENT care. The growing prevalence of hearing loss and ENT disorders is increasing demand for affordable diagnostic tools and surgical devices.

- China: Rapid urbanization, a rising aging population, and increased healthcare spending have driven a 20% surge in hearing device adoption since 2020. Leading companies are expanding their presence to meet the rising demand for ENT solutions.

- Government Initiatives: Across Southeast Asia, public health campaigns and national health missions are promoting ENT awareness, boosting the adoption of portable and cost-effective ENT diagnostic and therapeutic devices.

Competitive Landscape

The global ENT devices market is highly competitive, dominated by companies with robust product portfolios and expansive global distribution networks. Leading players such as Demant A/S and Sonova are heavily investing in R&D, allocating 6-8% of their annual revenue to develop AI-powered hearing aids and minimally invasive ENT technologies. Strategic acquisitions also play a key role in strengthening market presence. Cochlear Ltd., for instance, acquired an ENT diagnostics firm in 2023 to diversify its offerings. Additionally, companies like Olympus and Karl Storz are aggressively expanding in emerging markets such as China and India by enhancing their regional distribution infrastructure, enabling faster adoption in high-growth areas.

Key Developments

- Cochlear Ltd. (2024): Launched a next-generation cochlear implant with improved battery life and connectivity, capturing a 10% larger market share in otology and rhinology.

- Sonova (2023): Introduced AI-powered hearing aids with real-time sound optimization, boosting sales by 15% in North America and Europe.

- Olympus Corporation (2024): Developed a new image-guided surgery system for rhinology, enhancing surgical precision and reducing recovery times for chronic sinusitis treatment.

Companies Covered in ENT Devices Market

- Ambu A/S

- Cochlear Ltd.

- Demant A/S

- Sonova

- GN Store Nord A/S

- Karl Storz

- Olympus Corporation

- PENTAX Medical

- Richard Wolf GmbH

- Rion Co., Ltd.

- Others

Frequently Asked Questions

The ENT market is projected to reach US$ 16.7 billion in 2025.

Increasing prevalence of ENT disorders such as hearing loss and chronic sinusitis, an aging population, and advancements in ENT diagnostic and surgical devices are the key market drivers.

The ENT devices market is poised to witness a CAGR of 7.0% from 2025 to 2032.

Innovation in hearing devices, expansion in emerging markets such as the Asia Pacific, and growth in home care settings with portable ENT care tools are key opportunities.

Cochlear Ltd., Sonova, Demant A/S, Olympus Corporation, and Karl Storz are key players driving ENT device innovation in otology and rhinology.