- Food Ingredients & Additives

- Food Holding Equipment Market

Food Holding Equipment Market Size, Share, and Growth Forecast, 2026 – 2033

Food Holding Equipment Market by Product Type (Holding Cabinets, Proofing Cabinets, Refrigerators & Chillers), Temperature Range (Hot Holding, Cold Holding, Dry Holding), End-User (Full-Service Restaurants, Quick Service Restaurants (QSRs), Hotels, Railways, Airports, Hospitals, Schools), and Regional Analysis for 2026-2033

Food Holding Equipment Market Share and Trends Analysis

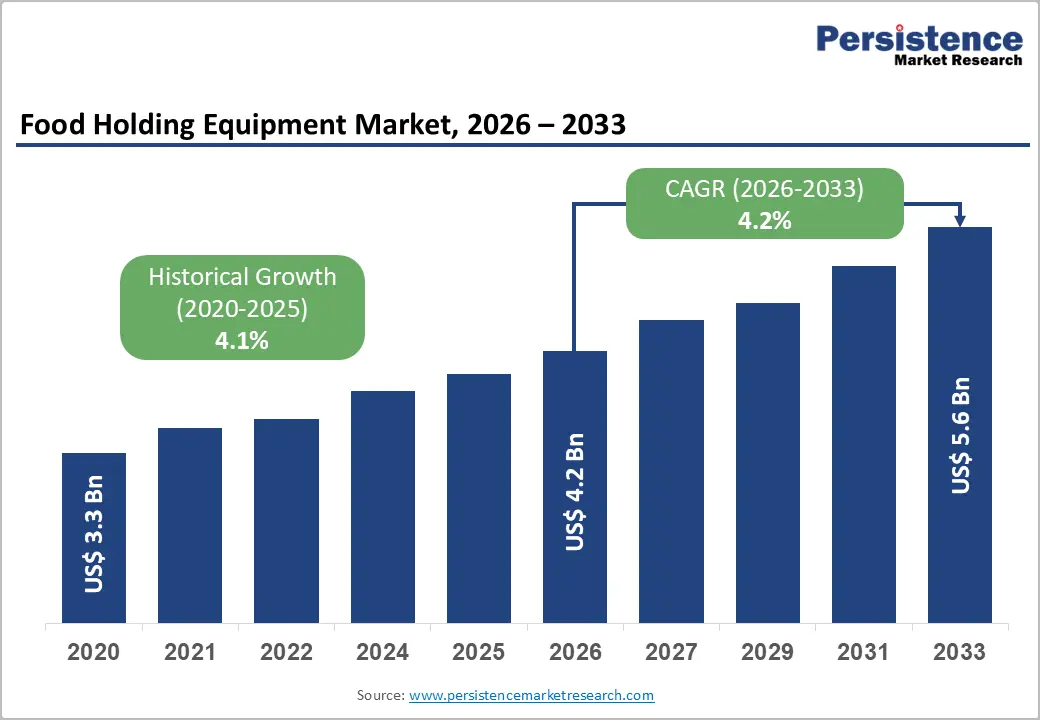

The global food holding equipment market size is likely to be valued at US$ 4.2 billion in 2026, and is projected to reach US$ 5.6 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033. Growth is driven by increasing demand for efficient food service operations and optimized temperature control solutions. Demographic shifts toward urbanization and rising disposable income elevate food consumption outside the home, expanding institutional and commercial food service demand. Integration of energy-efficient technology and automation in food holding equipment enhances operational efficiency and reduces operational costs.

Expansion of digital ordering systems and cloud-connected kitchens creates opportunities for equipment with remote monitoring and predictive maintenance capabilities. Healthcare institutions and educational facilities seek reliable food preservation methods to comply with health regulations, boosting adoption. Infrastructure investment in hotels, airports, and quick-service outlets increases the installation of modern holding cabinets and temperature-controlled equipment.

Key Industry Highlights

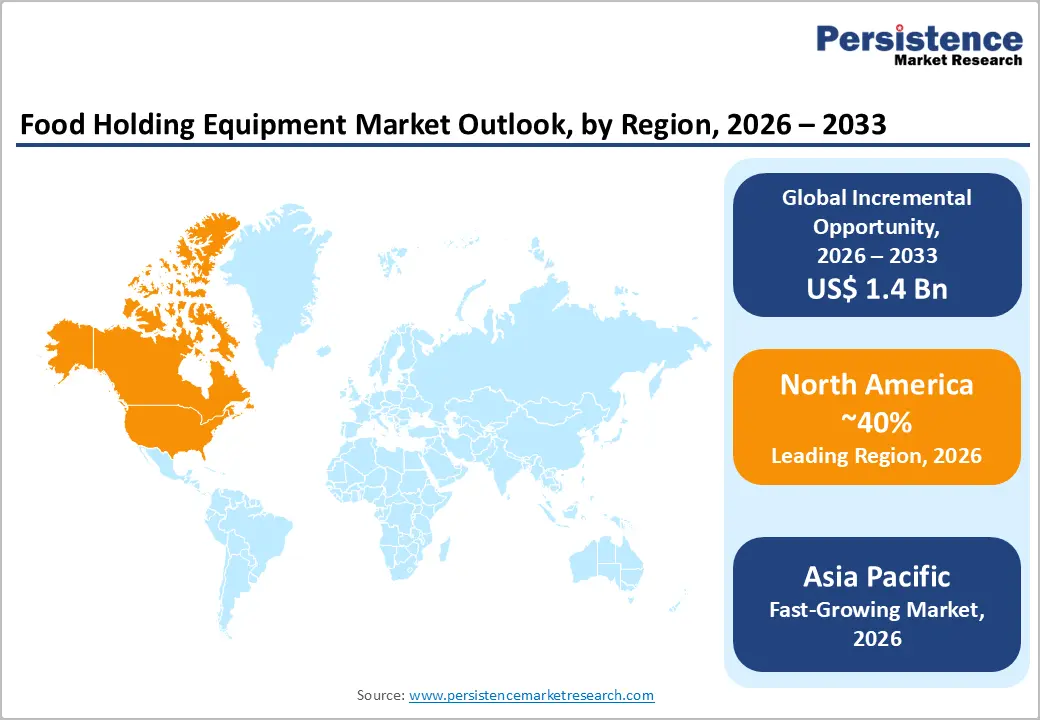

- Dominant Region: North America is predicted to hold a 40% market share in 2026, driven by large-scale commercial and institutional food service operations.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, fueled by rapid expansion of commercial food service and organized retail.

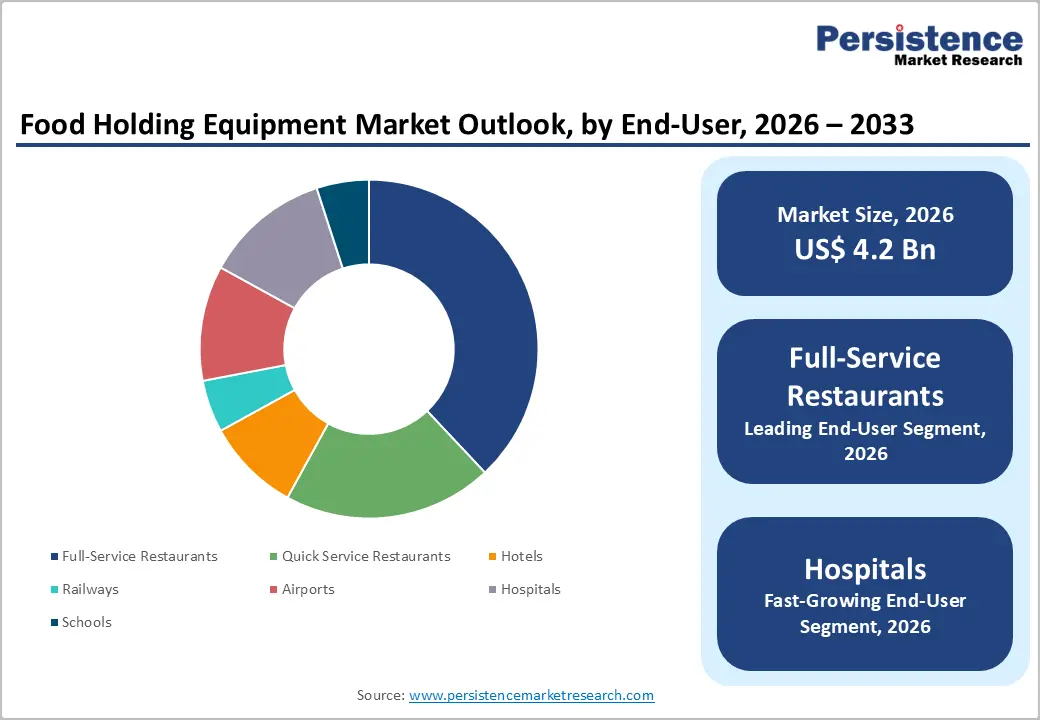

- Leading End-User: Full-service restaurants are likely to lead with about 38% market share in 2026 due to their complex menu structures and extended service durations.

- Fastest-growing End-User: Hospitals are slated to grow the fastest through 2033, driven by stringent food safety protocols and expanding patient care infrastructure.

- July 2025: Hoshizaki introduced the Valiance series of cost-conscious foodservice refrigeration equipment at the 2025 NRA Show, including reach-in refrigerators/freezers and undercounter units designed for reliability and accessibility.

| Key Insights | Details |

|---|---|

| Food Holding Equipment Market Size (2026E) | US$ 4.2 Bn |

| Market Value Forecast (2033F) | US$ 5.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Convenient Food Services

The rapid expansion of convenient food services such as quick service restaurants (QSRs), fast casual outlets and digital delivery platforms has reshaped operational priorities across commercial kitchens and stands as a primary force driving adoption of food holding equipment. Urban consumption patterns increasingly emphasize speed, reliability and minimal wait times, prompting operators to shift toward advanced preparation and continuous service models. In this operating context, food holding solutions such as heated cabinets, temperature controlled displays and chilled holding units enable prepared items to be kept service ready without compromising quality standards. These systems support faster order fulfillment, smoother peak period management and consistent output across extended operating hours, aligning kitchen performance with convenience-focused consumer expectations.

Operational efficiency and scalability remain central to competitive positioning within convenience-driven foodservice formats. High-order velocity combined with labor optimization goals places pressure on kitchens to stabilize production flow while maintaining food safety compliance. Food holding equipment enables structured batching, reduces dependency on real-time cooking and improves utilization of kitchen staff during demand surges. This capability supports waste reduction, consistency in portioning and uniform presentation across service channels. For operators managing multiple outlets or high throughput locations, standardized holding infrastructure strengthens process control and service uniformity.

Regulatory Complexity and Standardization Gaps

Regulatory fragmentation across markets creates structural friction for manufacturers and buyers by imposing multiple, misaligned compliance frameworks governing temperature control, material safety, energy efficiency, and food-contact hygiene. Divergent certification processes force companies to customize designs, documentation, and testing protocols for each jurisdiction, thereby inflating development timelines and costs. Product approvals experience delays as authorities apply varied interpretations of safety thresholds and performance benchmarks. This environment discourages rapid innovation cycles, limits scalability of standardized product lines, and constrains cross-border commercialization. Small and mid-sized producers face disproportionate pressure, as compliance investment absorbs capital otherwise allocated to product enhancement or channel expansion. Procurement teams within food service chains encounter complexity when equipment cleared in one market is not accepted elsewhere, disrupting uniform operational deployment across multi-location networks.

Standardization gaps further weaken purchasing confidence and operational consistency across end-user segments. The lack of universally accepted performance metrics for heat retention, recovery time, and energy consumption complicates product comparisons and return-on-investment evaluations. Buyers struggle to benchmark lifecycle costs, leading to extended decision cycles and conservative purchasing behavior. Service providers face challenges in maintenance and replacement planning when component specifications vary widely across brands and approval systems. Training protocols for kitchen staff become fragmented, increasing operational risk and reducing efficiency. Institutional buyers, such as hospitals and educational facilities, adopt risk-averse procurement strategies that favor legacy systems over newer solutions that lack clear alignment with established standards.

Expansion across Institutional and Public Infrastructure Projects

Rising investment in institutional and public infrastructure projects drives significant demand for food holding equipment, as large-scale facilities require robust and efficient solutions for meal storage, transport, and service. Educational institutions, healthcare facilities, and government-run cafeterias increasingly adopt modern equipment to maintain food quality, ensure hygiene standards, and streamline operational workflows. Equipment designed for high-volume usage reduces waste, improves temperature control, and enhances service efficiency, aligning with institutional priorities of cost optimization and consistent performance. Procurement policies in public infrastructure projects often favor standardized, durable, and energy-efficient solutions, which encourages suppliers to innovate and supply tailored products that meet these stringent operational and regulatory requirements.

Operational scalability and efficiency considerations within public projects create opportunities for the adoption of advanced food holding solutions. Catering and meal distribution services in large institutions benefit from modular and automated systems that minimize manual handling and maintain food safety compliance. Integration of digital temperature monitoring, automated carts, and insulated storage units allows institutions to optimize service timelines and reduce maintenance challenges. Projects with multiple touchpoints, such as airports, universities, and hospitals, require equipment that supports coordinated food delivery at scale, generating sustained demand for specialized solutions.

Category-wise Analysis

Product Type Insights

Holding cabinets are likely to be the leading segment, with an approximate 45% revenue share in 2026, due to their broad applicability across commercial and institutional foodservice environments. These cabinets maintain consistent temperatures during peak service periods, ensuring food quality, safety, and compliance with hygiene standards. Full-service restaurants, hotels, hospitals, and transportation hubs rely on these systems to efficiently manage high-volume meal preparation and staged serving models. Design flexibility, including mobile units, multi-compartment layouts, and adjustable shelving, enhances adoption across varied kitchen configurations. Provider preference is influenced by operational reliability, user-friendly controls, and seamless integration with existing workflows.

Proofing cabinets are expected to witness the fastest growth between 2026 and 2033, as bakery-focused operations and quick-service formats expand standardized food preparation models. The increasing emphasis on consistent dough fermentation, product uniformity, and quality control is driving adoption in commercial bakeries, in-store bakery sections, and food service chains that prioritize menu consistency. Equipment advancements enable precise temperature and humidity regulation, improving repeatability and reducing reliance on manual monitoring. Integration with automated baking lines and centralized kitchens accelerates provider adoption. Compact, modular designs support scalability, making proofing cabinets accessible to mid-scale operations while optimizing workflow efficiency and process reliability.

Temperature Range Insights

Hot holding is poised to lead, with an estimated 50% revenue share in 2026, owing to its widespread application in prepared meal services and time-sensitive food delivery environments. Consumer expectations for the immediate availability of warm meals across restaurants, institutional cafeterias, and transport catering services reinforce reliance on hot-holding solutions, ensuring consistent quality and service speed. A cultural preference for freshly prepared hot food enhances customer satisfaction and operational credibility. Retail penetration across quick-service outlets, buffet-style operations, and large-scale catering setups supports sustained demand. Preventive food safety practices emphasizing accurate temperature control further encourage adoption across highly regulated food service environments.

Cold holding is anticipated to be the fastest-growing segment between 2026 and 2033, driven by expanding chilled food offerings and the growth of ready-to-serve formats. Healthcare, educational institutions, and travel catering increasingly demand reliable solutions that maintain freshness, extend shelf life, and preserve nutritional value. The growth of digital commerce, meal kit delivery, and pre-prepared meal distribution increases reliance on cold-holding equipment. Advancements in energy-efficient refrigeration, uniform temperature distribution, and modular design improve operational efficiency and handling. Market adoption is further supported by emphasis on compliance with food safety regulations and scalable storage solutions for high-volume operations.

End-User Insights

Full-service restaurants are positioned as the dominant segment, with a 38% market share in 2026, supported by complex menu structures and extended service durations. These establishments require dependable holding solutions to manage a variety of dishes without compromising quality or presentation, particularly for multi-course meals and time-sensitive service. Decision-making around equipment procurement is influenced by clinical credibility of food safety compliance, provider referrals, and inspection outcomes, ensuring operational reliability. Investment in kitchen modernization, workflow optimization, and digitalization enhances equipment adoption, supporting both labor efficiency and energy management.

Hospitals are expected to emerge as the fastest-growing segment between 2026 and 2033, driven by stringent food safety protocols and expanding patient care infrastructure. Healthcare facilities emphasize precise temperature control, compliance with hygiene protocols, and consistency in meal delivery across diverse patient populations. Centralized meal preparation models, automated distribution systems, and digital kitchen monitoring encourage the adoption of advanced food holding equipment. Access to institutional funding, efficiency-driven procurement policies, and long-term cost control considerations strengthen procurement capacity. Integration of insulated storage units, modular carts, and user-friendly interfaces allows hospitals to maintain service quality while supporting scalability in patient meal operations.

Regional Insights

North America Food Holding Equipment Market Trends

North America is expected to dominate with an estimated 40% of the food holding equipment market share in 2026, driven by the concentration of large-scale commercial and institutional food service operations. High consumer expectations for service speed, food quality, and safety sustain demand for advanced holding solutions in full-service restaurants, quick-service formats, and healthcare facilities. Widespread integration of digital kitchen management systems and automated meal-delivery workflows enhances operational efficiency, reinforcing reliance on technologically sophisticated cabinets, carts, and hot- and cold-holding units. Strict hygiene regulations and temperature compliance requirements increase the adoption of reliable equipment that minimizes food waste and supports process consistency. Strategic investment in kitchen modernization, along with the availability of institutional funding, strengthens penetration and replacement cycles.

Operational complexity across high-volume catering and centralized meal preparation models drives continued demand for high-performance holding solutions. Multi-site chains benefit from modular, scalable equipment that maintains consistent temperature, humidity, and product integrity across service points. Innovations in energy-efficient insulation, humidity control, and digital monitoring reduce operational costs while ensuring food safety compliance, influencing procurement decisions. Supplier partnerships with institutional operators facilitate customized solutions aligned with workflow requirements. Expansion of corporate catering, healthcare services, and hospitality operations increases reliance on versatile equipment that balances capacity, flexibility, and durability, reinforcing long-term market dominance.

Europe Food Holding Equipment Market Trends

Europe is predicted to hold a significant position in the market for food holding equipment through 2033, supported by well-established commercial food service networks, mature institutional catering systems, and high regulatory standards for food safety and hygiene. Strong consumer demand for quality, consistency, and compliance drives adoption of advanced holding solutions across full-service restaurants, healthcare facilities, and educational institutions. Technological integration, including digital temperature monitoring, automated meal transport systems, and energy-efficient storage units, enhances operational reliability and reduces labor requirements. Investment in kitchen modernization and refurbishment programs by large hospitality chains and institutional operators ensures steady replacement demand and supports adoption of modular, versatile equipment. Emphasis on sustainability and energy management encourages the selection of solutions that balance operational efficiency with environmental compliance, strengthening long-term market stability.

High-volume catering operations and multi-site food production facilities require cabinets, carts, and hot/cold holding systems that maintain precise temperature, humidity, and product integrity across multiple service points. Growth of airline catering, centralized meal preparation, and pre-prepared meal distribution increases reliance on reliable equipment capable of reducing food waste and ensuring service consistency. Continuous innovation in insulation performance, digital controls, and modular configurations supports workflow optimization and scalability. Collaborative initiatives between suppliers and operators facilitate the development of customized solutions tailored to operational requirements.

Asia Pacific Food Holding Equipment Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for food holding equipment between 2026 and 2033, stimulated by rapid expansion of commercial food service networks, institutional catering, and organized retail chains. Rising urbanization, increasing disposable income, and evolving consumer preferences for ready-to-serve and time-sensitive meals drive demand for advanced hot and cold holding solutions. Centralized kitchen models and multi-outlet operations require scalable, modular equipment capable of maintaining consistent temperature, quality, and hygiene standards across distributed service points. Adoption of digital monitoring, automated meal distribution, and energy-efficient storage systems enhances operational efficiency and reduces labor dependency. Investment in professional kitchen infrastructure by emerging hospitality chains, corporate cafeterias, and healthcare facilities reinforces demand for durable, versatile holding equipment.

Operational sophistication and food safety compliance are key factors driving market growth. The expansion of international quick-service chains and standardized menu concepts increases reliance on equipment that enables high-volume, consistent meal delivery. The growth of pre-prepared meal distribution, airline catering, and institutional services is driving demand for precision-controlled cabinets and carts that minimize spoilage and improve service reliability. Innovations in insulation, humidity control, and modular design optimize capacity and workflow flexibility for multi-location operations. Access to infrastructure development support, modernization incentives, and increasing awareness of hygiene standards further encourage adoption.

Competitive Landscape

The global food holding equipment market structure is moderately fragmented, characterized by the presence of several established manufacturers alongside a broad base of specialist suppliers. Key players such as Alto-Shaam, Inc., Duke Manufacturing, Hatco Corporation, Cambro, and InterMetro Industries Corporation hold significant market positions through strong product portfolios, extensive distribution networks, and technological innovation. These companies leverage expertise in temperature control, insulation efficiency, and modular design to provide high-performance solutions across commercial and institutional food service operations. Mid-tier firms and regional suppliers contribute a substantial combined share, ensuring product diversity across price segments, operational scales, and application requirements. Adoption by institutional buyers is guided by equipment reliability, compliance with food safety standards, and compatibility with automated workflows, allowing leading manufacturers to differentiate through design, durability, and energy efficiency.

Competition in the sector is increasingly driven by automation, digital integration, and sustainability. Suppliers focus on developing equipment that supports centralized kitchen models, multi-site catering, and high-volume food distribution while minimizing energy consumption and operational downtime. Modular configurations, mobility features, and user-friendly controls enhance flexibility, enabling buyers to optimize workflows and reduce labor requirements. Compliance with hygiene regulations, temperature accuracy, and reliability are critical decision factors that reinforce supplier positioning. Strategic partnerships, localized service networks, and customization options further strengthen competitive advantage.

Key Industry Developments

- In September 2025, Alto-Shaam celebrated its 70th anniversary at HOST Milano 2025, showcasing ventless multi-cook ovens plus Halo Heat® holding solutions. Live demos highlighted stackable, water-free designs for space efficiency and premium hot holding (Cook & Hold, Smoker Ovens, and merchandisers), emphasizing sustainability and operational flexibility.

- In July 2025, Elanpro opened its first Experience Centre in Bengaluru, showcasing stainless steel refrigeration, bakery solutions, beverage dispensers, softy/slush machines, cold rooms, ice machines, and AI vending for HoReCa, QSRs, ice cream/dairy, retail, and healthcare. Targeting Bengaluru's booming F&B ecosystem, it projects INR 8 crore revenue in 12 months as a hands-on demo/learning hub with specialists.

- In April 2025, Hatco launched the Flav-R 2-Go Built-In Outdoor Locker System with dual-sided access in 7/11-cubby configurations for contactless pickup in high-volume foodservice.

Designed for QSRs, colleges, and ghost kitchens, the system features ambient/heated holding, outdoor-rated touchscreen with anti-glare, insulated SS doors, LED indicators, and connectivity options.

Companies Covered in Food Holding Equipment Market

- Alto-Shaam, Inc.

- Duke Manufacturing

- Hatco Corporation

- Cambro

- InterMetro Industries Corporation

- Cres Cor

- Shandong Huangda Trading Co., Ltd.

- Henny Penny

Frequently Asked Questions

The global food holding equipment market is projected to reach US$ 4.2 billion in 2026.

Rising demand for high-quality, safe, and efficient food service operations is driving the market.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Expansion across institutional and public infrastructure projects, rising demand for ready-to-serve meals, and adoption of advanced hot and cold holding solutions are key opportunities for the market.

Some of the key market players include Alto-Shaam, Inc., Duke Manufacturing, Hatco Corporation, Cambro, and InterMetro Industries Corporation.