- Processed Food

- Fermented Foods Market

Fermented Foods Market Size, Share, and Growth Forecast, 2026 - 2033

Fermented Foods Market by Food Type (Dairy-Based, Vegetable-Based, Soy-Based, Grain-Based, Beverage-Based), Microorganism (Bacteria, Yeasts, Molds, Mixed Cultures), Functional Benefit (Probiotic & Gut Health, Nutritional Enhancement, Extended Shelf Life/Preservation), and Regional Analysis for 2026 - 2033

Fermented Foods Market Share and Trends Analysis

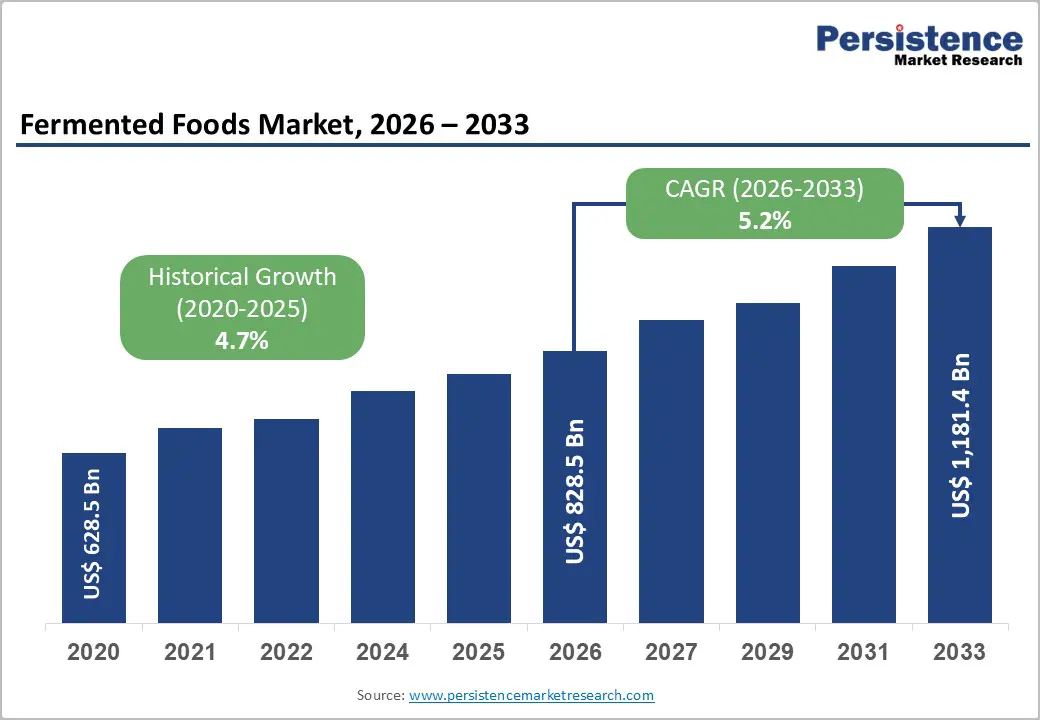

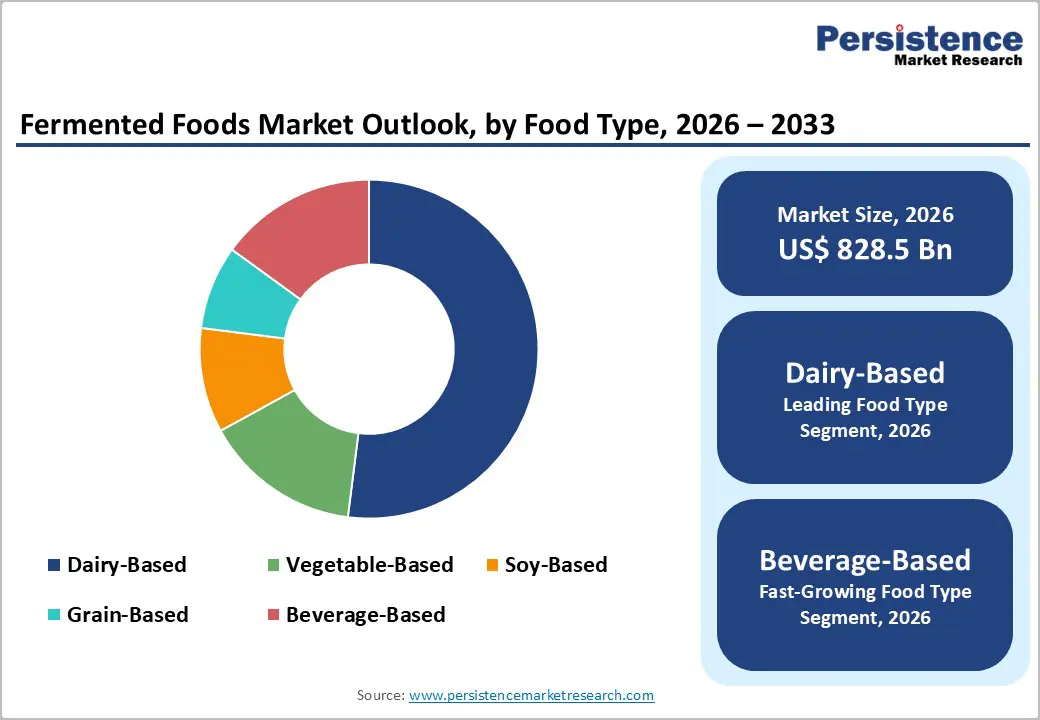

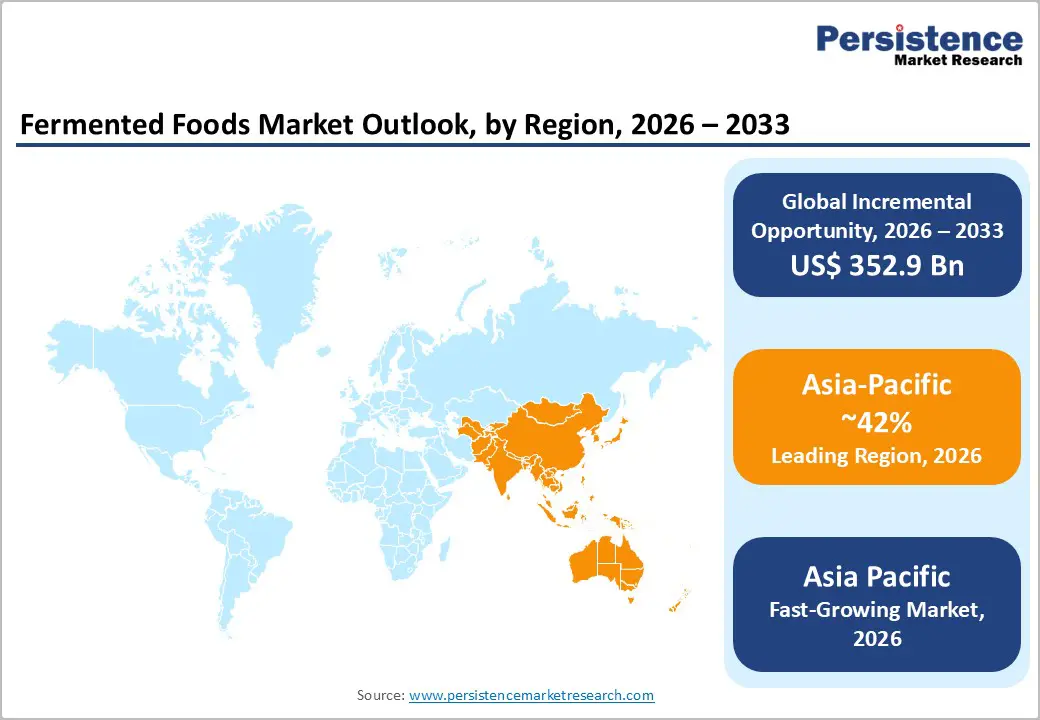

The global fermented foods market size is likely to be valued at US$ 828.5 billion in 2026, and is projected to reach US$ 1,181.4 billion by 2033, growing at a CAGR of 5.2% during the forecast period 2026−2033. Market expansion is driven by rising global health consciousness, increased demand for products with probiotic benefits, and expanding retail and e-commerce distribution channels.

Consumers across developed and emerging regions are increasingly prioritizing digestive health and natural food offerings, amplifying intake of fermented dairy, vegetable, soy, grain, and beverage-based foods. Urbanization and cultural preferences further bolster adoption, while manufacturers emphasize functional ingredients and advanced fermentation technologies to improve shelf life and nutritional profiles. Key macro drivers include demographic shifts toward aging populations with higher health needs and regulatory support for food safety standards.

Key Industry Highlights

- Dominant Region: Asia Pacific is predicted to hold about 40% market share in 2026, driven by strong cultural consumption habits and widespread awareness of digestive health.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, fueled by a rising demand for functional and plant-based fermented products.

- Leading Food Type: The dairy-based segment is likely to lead with about 52% market share in 2026 due to strong consumer familiarity, daily consumption habits, and a well-established retail presence.

- Fastest-growing Food Type: Beverage-based foods are slated to grow the fastest through 2033, fueled by flavor diversification and expanding availability of ready-to-drink probiotic beverages.

- Key Drivers: Improving health consciousness, strong demand for probiotics, growing interest in functional and plant-based foods, and expanding retail and e-commerce channels fuel market growth.

- November 2025: Netherlands became the first European Union (EU) nation to permit pre-market tastings of precision- and biomass-fermented novel foods under a new Code of Practice, allowing startups to gather consumer feedback before full EU authorization.

| Key Insights | Details |

|---|---|

|

Fermented Foods Market Size (2026E) |

US$ 828.5 Bn |

|

Market Value Forecast (2033F) |

US$ 1,181.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Awareness of Health Benefits and Probiotics

Increasing awareness of health benefits of fermented foods and probiotics drives growth as consumers seek products that actively support wellness. Fermented foods naturally contain live microorganisms that enhance gut health, improve digestion, and contribute to immune system regulation. Growing knowledge of these functional properties encourages more individuals to incorporate these foods into daily diets as preventive health measures. The shift toward preventive healthcare and self-managed nutrition created demand for items that offer measurable health outcomes, positioning fermented foods as a preferred choice.

Consumer confidence in the functional benefits of probiotics shapes purchasing decisions, influencing retailers and manufacturers to focus on product innovation. Companies are investing in research and development to optimize strains, improve flavor profiles, and extend shelf life while maintaining microbial viability. Educational campaigns, social media influence, and health-focused marketing further reinforce understanding of the link between probiotics and overall wellness. Urbanization and evolving lifestyle patterns amplify consumption as convenience-driven formats, such as ready-to-eat beverages and snackable fermented foods, become more accessible.

Regulatory Hurdles and Compliance Costs

Regulatory hurdles and compliance costs act as key restraints as these factors directly impact production efficiency and operational scalability. Fermented foods involve live microorganisms, which require strict adherence to food safety standards, labeling regulations, and quality control protocols. Manufacturers must invest in specialized equipment, testing, and monitoring systems to meet regulatory requirements. Such obligations increase capital expenditure and operational complexity, particularly for small and medium-sized enterprises seeking market entry. Variations in regional regulations create additional challenges, requiring companies to navigate diverse standards for microbial content, shelf life, and ingredient approval, which can delay product launches and limit geographic expansion.

Compliance costs also affect pricing strategies and profit margins. Firms allocate significant resources toward documentation, certification, and periodic audits to demonstrate adherence to safety and quality norms. Any failure to comply can result in product recalls, fines, or reputational damage, impacting stakeholder confidence and market credibility. The burden of regulatory oversight may discourage innovation, as companies weigh the risk and cost of launching new fermented variants against potential returns. Strict labeling and health claim restrictions limit marketing flexibility, reducing the ability to communicate functional benefits effectively to consumers.

Plant-Based and Innovative Product Convergence

Plant-based and innovative product convergence represents a significant opportunity as consumer demand shifts toward sustainable, health-focused alternatives. Rising awareness of plant-based nutrition, combined with interest in functional foods, creates a fertile environment for novel fermented offerings. Companies can develop dairy-free yogurts, kombuchas, and protein-rich fermented snacks that cater to vegan, lactose-intolerant, and environmentally conscious consumers. Innovation in ingredients, flavors, and textures enables differentiation in a crowded market, allowing brands to attract diverse consumer segments and expand customer loyalty.

Integration of plant-based approaches with innovative processing also drives operational efficiency and portfolio expansion. Startups and established players can leverage technology to optimize fermentation cycles, reduce production costs, and maintain microbial integrity while experimenting with new plant substrates such as legumes, cereals, and botanical extracts. The convergence supports sustainable sourcing initiatives, aligning with corporate social responsibility goals and attracting environmentally conscious investors. Consumer engagement through novel formats, ready-to-eat options, and functional benefits strengthens market penetration and brand positioning.

Category-wise Analysis

Food Type Insights

The dairy-based segment is poised to lead with a forecasted 52% of the fermented foods market revenue share in 2026, owing to strong consumer familiarity, daily consumption patterns, and a well-established retail presence. Yogurt, kefir, cheese, and related fermented dairy products benefit from established brand reputations, broad availability, and deep integration into both traditional and modern diets across the globe. Their appeal is reinforced by functional benefits such as probiotics, improved digestion, and enhanced nutrient absorption, which have strengthened consumer preference and loyalty over time.

The beverage-based segment is expected to be the fastest-growing category between 2026 and 2033, driven by ongoing innovation, flavor diversification, and rising health-conscious consumption among younger demographics. Ready-to-drink options such as kombucha, kefir drinks, and functional probiotic beverages are meeting the growing demand for digestive health support and functional nutrition. Expanding retail availability, strategic marketing efforts, and increased awareness of wellness benefits are further accelerating adoption, making this segment a key driver in the fermented foods market growth trajectory.

Microorganism Insights

The bacteria model is projected to hold a leading market share of 48% in 2026, as it plays a critical role in producing yogurt, sauerkraut, kimchi, and a wide range of traditional fermented foods. Bacterial fermentation ensures consistent taste, texture, and product stability, making it highly suitable for large-scale commercial production. The segment benefits from strong consumer preference driven by probiotic benefits and digestive health support, which encourage steady adoption across age groups and regions. Ongoing investment in strain optimization, fortified formulations, and functional variants further improves product quality and nutritional value.

The mixed cultures model is expected to experience the fastest growth from 2026 to 2033, since it enables the creation of complex flavors, enhanced nutritional profiles, and diverse functional benefits. By combining bacteria, yeasts, and sometimes molds, manufacturers can innovate in taste, aroma, and product variety, appealing to consumers interested in artisanal, plant-based, or premium fermented foods. Expansion of research and development efforts is supporting the optimization of fermentation processes, the development of novel product formats, and the enhancement of microbial stability, further driving segment growth.

Functional Benefit Insights

The probiotic and gut health segment is expected to maintain a dominant position, accounting for an estimated 45% of the market share in 2026, as consumers increasingly prioritize digestive wellness and long-term health maintenance. Fermented foods containing live cultures are valued for their ability to enhance microbiome balance, improve nutrient absorption, and support immune system function, which strongly influences purchasing decisions across age groups and regions.

The nutritional enhancement segment is projected to be the fastest-growing segment from 2026 to 2033, driven by rising demand for multifunctional foods fortified with vitamins, minerals, and bioactive compounds that support immunity, energy, and overall well-being. Fermented foods with enhanced nutrient profiles are meeting the needs of health-conscious consumers who seek preventive nutrition and convenient dietary solutions, further accelerating segment growth.

Regional Insights

North America Fermented Foods Market Trends

North America holds a significant position in the fermented foods market due to high consumer awareness of health, wellness, and digestive benefits. Interest in probiotics and functional nutrition drives steady demand across various age groups. Well-established retail infrastructure, including supermarkets, specialty stores, and online platforms, ensures wide accessibility to a diverse range of fermented products. Urban consumers show preference for convenient, ready-to-eat options such as yogurt, kefir, and fermented beverages. Continuous investment in product innovation, fortified formulations, and flavor diversification strengthens market presence and encourages broader adoption.

Market growth in North America is driven by rising interest in plant-based and functional fermented foods. Health-conscious younger demographics are increasingly seeking products that support gut health, immunity, and overall wellness. Expansion of e-commerce channels and digital marketing enhances consumer awareness and accessibility. Research and development in fermentation technologies, probiotic strain optimization, and new product formats support innovation, while changing consumption patterns favor convenient and nutrient-rich offerings, accelerating adoption and market development.

Europe Fermented Foods Market Trends

Europe demonstrates strong demand for fermented foods due to widespread consumer focus on health, wellness, and functional nutrition. Traditional diets that incorporate products such as yogurt, sauerkraut, kefir, and cheese support consistent consumption across countries. Awareness of digestive health and probiotic benefits drives purchasing behavior, particularly among urban populations. Well-developed retail channels, including supermarkets, specialty stores, and online platforms, provide broad accessibility and product variety. Continuous innovation in flavors, fortified formulations, and convenient packaging enhances appeal and encourages adoption across diverse demographic groups.

Growth in Europe is supported by interest in plant-based and functional fermented products that provide nutritional and immunity benefits. Health-conscious consumers increasingly seek options that combine convenience with preventive nutrition. E-commerce expansion and targeted marketing campaigns help educate consumers and increase availability of innovative products. Investment in fermentation technology, research on microbial strains, and collaboration between local and international brands strengthen product differentiation, encouraging experimentation and expansion across the market.

Asia Pacific Fermented Foods Market Trends

By 2026, Asia Pacific is expected to lead with an estimated 40% of the fermented foods market share, propelled by deep-rooted cultural consumption patterns, widespread adoption of traditional fermented products, and high awareness of digestive health and functional nutrition. The prevalence of kimchi, miso, tempeh, natto, and regional yogurts, combined with rising disposable incomes and expanding modern retail networks, reinforces market dominance. Aging populations seeking preventive health benefits, government initiatives supporting nutritional awareness, and diverse agricultural bases ensuring raw material availability further strengthen market performance.

Asia Pacific is also poised to be the fastest-growing market for fermented foods during the 2026-2033 forecast period, driven by rapid urbanization, evolving lifestyle habits, and growing interest in functional and fortified fermented products. Increasing demand for plant-based beverages like kombucha and fortified kefir, along with e-commerce expansion and digital marketing campaigns, accelerates adoption. Investment in advanced fermentation technologies, research on probiotic efficacy, and partnerships between local and international brands support innovation and efficient supply chains, contributing to rapid market development.

Competitive Landscape

The global fermented foods market structure exhibits moderate fragmentation, with key players such as Nestlé, Danone, PepsiCo, General Mills, and Kerry Group holding a significant market presence. Fragmentation remains among smaller producers and local innovators, creating a competitive landscape that contrasts with the strong positioning of established multinational brands. This dual-layer structure reflects varying barriers to entry across product types, with larger companies leveraging brand recognition, comprehensive product portfolios, and extensive distribution networks, while smaller firms focus on niche offerings, unique flavors, and specialized functional benefits to capture growth opportunities.

Strategic positioning favors innovation-driven companies that invest in product development, functional ingredients, and advanced fermentation techniques. These companies differentiate themselves by offering fortified dairy products, probiotic beverages, and plant-based fermented options that meet evolving consumer preferences. Emphasis on flavor innovation, nutritional enhancement, and convenient packaging supports market expansion. Continuous research in microbial cultures, fermentation efficiency, and product safety strengthens operational effectiveness and enables manufacturers to deliver high-quality, health-oriented solutions that cater to both traditional and modern consumption trends.

Key Industry Developments

- In November 2025, a new Canadian network launched the Canadian Fermented Foods Initiative to share accessible research, recipes, and science-based resources highlighting health benefits of fermented foods and foster collaboration among consumers, researchers, health professionals, and industry experts.

- In October 2025, the Aliko Dangote Foundation, in partnership with the Sight and Life Foundation, launched a nationwide initiative in Nigeria to promote production and consumption of fermented foods to combat malnutrition and improve food and nutrition security by leveraging traditional fermentation practices with modern science.

- In September 2025, the UK Food Standards Agency and Food Standards Scotland launched a precision fermentation innovation research program to enhance regulatory expertise, introduce a business support service, and help companies navigate market authorization for precision-fermented products.

Companies Covered in Fermented Foods Market

- Nestlé

- Danone

- PepsiCo

- General Mills

- Kerry Group

- Chr. Hansen

- Cargill

- Angel Yeast

- Ajinomoto

- Lallemand

- Meiji Holdings

- Conagra Brands

- Mars

- Mondelez International

Frequently Asked Questions

The global fermented foods market is projected to reach US$ 828.5 billion in 2026.

The market is driven by rising health consciousness, increasing demand for probiotics and gut-friendly products, and growing consumer preference for natural and functional foods.

The market is poised to witness a CAGR of 5.2% from 2026 to 2033.

Key market opportunities include the development of plant-based and functional fermented products, adoption of advanced fermentation technologies, and expansion into e-commerce and health-focused consumer segments.

Some of the key market players include Nestlé, Danone, PepsiCo, General Mills, Kerry Group, and Chr. Hansen.