- Food Ingredients & Additives

- Walnut Ingredients Market

Walnut Ingredients Market Size, Share, and Growth Forecast, 2025 - 2032

Walnut Ingredients Market By Product Type (Kernels, Flour, Oil, Powder, Others), Distribution Channel (Supermarkets, Specialty Stores, Online, Others), End-use (Household, Food & Beverages, Personal Care & Cosmetics, Nutraceuticals & Pharmaceuticals, Others), and Regional Analysis for 2025 - 2032

Walnut Ingredients Market Share and Trends Analysis

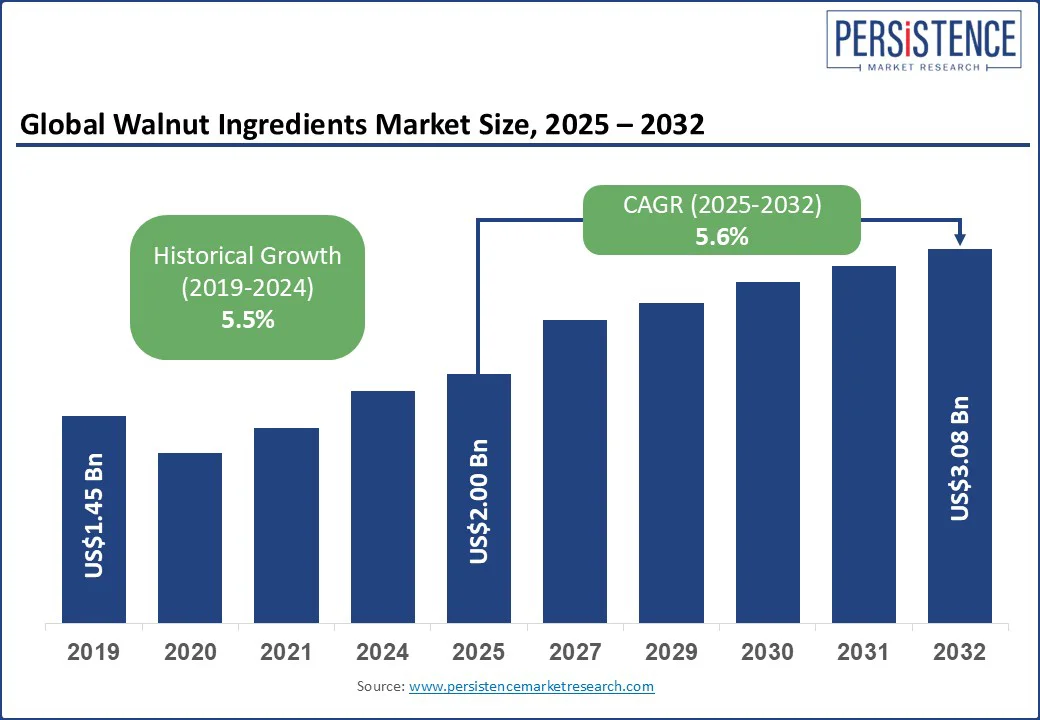

The global walnut ingredients market size is likely to value at US$ 2.00 Bn in 2025 and reach US$ 3.08 Bn by 2032, growing at a CAGR 5.6% during the forecast period from 2025 to 2032.

The demand for premium, versatile nutrition options that combine functionality and sustainability is expected to set a better precedence for future growth. Walnut ingredients, such as kernels and oil derivatives, are prized for their dense nutrition, especially plant-based omega-3 alpha-linolenic acid (ALA), functional fats, and clean-label appeal in food, nutraceutical, and personal-care applications.

These ingredients fit neatly into premiumization and sustainability narratives, from barista-ready walnut milks to microplastic-free exfoliants and upcycled high-protein flours, extending their applicability beyond the food and confectionery industries.

Surge in global demand for plant-based nutrition aligns well with the omega-3 ALA content in walnuts and their heart-health benefits, fueling innovation across food, beverages, dairy alternatives, and dietary supplements. Regulatory reforms in the personal care sector, including the EU's ban on microplastics, are also driving the adoption of walnut shell powder as a natural, eco-friendly exfoliant.

Key Industry Highlights

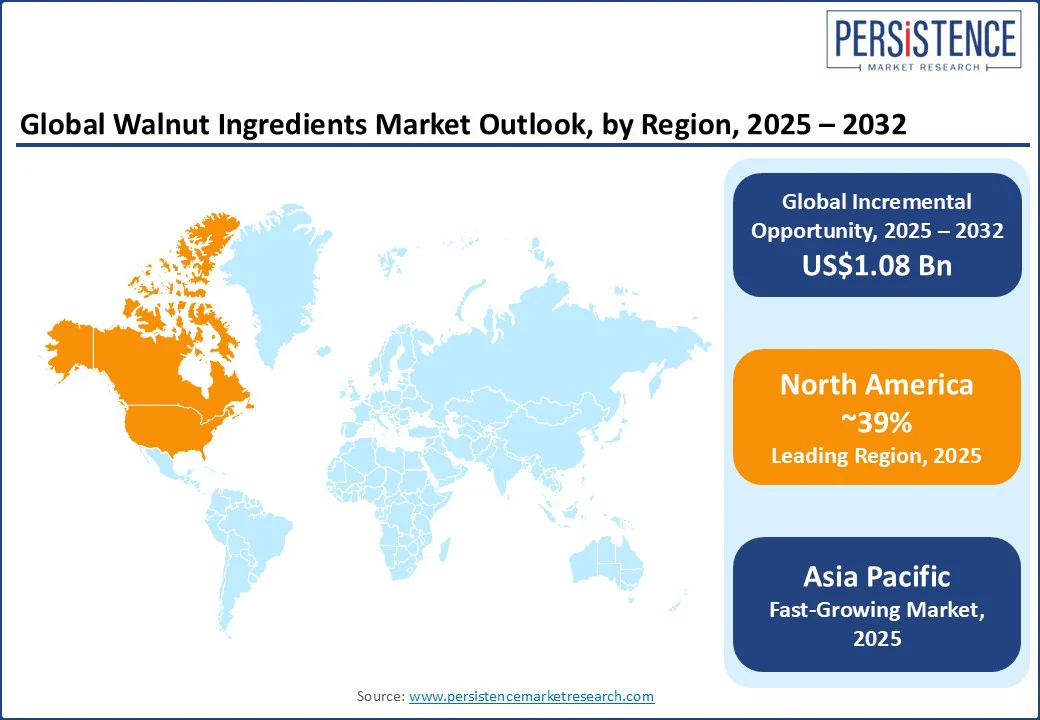

- Leading Region: North America is expected to dominate with a 39.0% share in 2025, supported by a mature food processing industry, high consumer nutrition awareness, and USDA-backed export initiatives.

- Fastest-growing Region: Asia Pacific is projected to be the fastest-growing regional market at an estimated highest CAGR from 2025 to 2032, due to prolific e-commerce expansion and tariff reductions boosting walnut imports, especially in China, India, Japan, and South Korea.

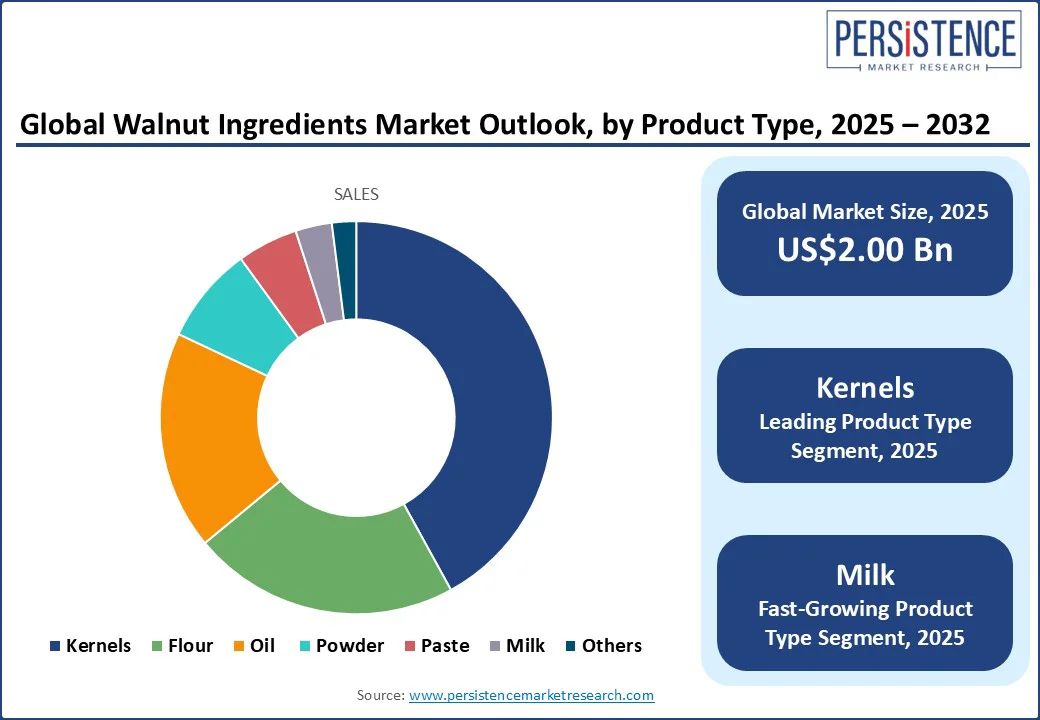

- Dominant Product Type Segment: Kernels are anticipated to lead in 2025 with an approximate share of 42%, as they are experiencing high adoption in clean-label snacking, bakery inclusions, and cereal fortification.

- Fastest-growing Product Type: Walnut milk is slated to register the highest CAGR during 2025-2032, owing to the surging demand for plant-based milk alternatives.

|

Global Market Attribute |

Key Insights |

|

Walnut Ingredients Market Size (2025E) |

US$ 2.00 Bn |

|

Market Value Forecast (2032F) |

US$ 3.08 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.5% |

Market Dynamics

Driver - Growing Awareness about Omega-3 to Bolster Market Prospects

The growth of the walnut ingredients market is accelerating due to widening consumer awareness of plant-based omega-3 fatty acids, specifically alpha-linolenic acid, and their role in cardiovascular health, cognitive function, and inflammation management.

With a one-ounce serving of walnuts delivering approximately 2.5 grams of ALA, the highest among tree nuts, food and beverage brands are leveraging this nutritional edge to command premium shelf space in functional snacks, fortified cereals, dairy alternatives, and ready-to-drink nut beverages.

For example, in 2024, U.S. retail sales of nut-based milks surged, with walnut milk stock keeping units (SKUs) expanding in chains such as Whole Foods and Sprouts. This unique positioning is further amplified by the clean-label trend, where claims of heart-healthy, plant-based, and non-GMO tags significantly boost consumer trust and repeat purchase rates.

For suppliers, this growing awareness is driving demand for walnut derivatives such as kernels, oil, flour, and high-protein press-cakes, spurring innovation, brand differentiation, and margin growth in both developed and emerging markets.

Restraint - Vulnerability to Climate Change and Supply Concentration to Dampen Market Outlook

Acute vulnerability to climate variability and geographic supply chokehold, which together create pronounced volatility in raw material availability and pricing, are acting as the foremost constraints on the market expansion. Over 70% of global walnut production is concentrated in a handful of regions, with China leading the pack, followed by the U.S., Iran, and Turkey, making the supply chain highly sensitive to extreme weather events, water scarcity, and pest pressures.

For instance, in 2024, the California Walnut Board and Commission reported that walnut growers are observing a 30% to 45% drop in yield, along with a smaller size of the nuts as a result of an intensely hot summer in the state.

This fragility is compounded by the long cultivation cycle of walnut trees, which take four to seven years to reach commercial yield, thereby limiting short-term supply elasticity and making it difficult for the market to respond to demand surges in plant-based beverages, functional snacks, or walnut oil-based personal care products.

Environmental instability in key producing regions is likely to translate into unpredictable input costs, shrunken margins for producers and suppliers, and heightened competition for certified, high-grade walnut ingredients.

Opportunity - Development of Upcycled Walnut Derivatives to Open High-Margin Pathways for Market Players

Companies in the walnut ingredients market can unlock a lucrative opportunity by transforming by-products such as press-cake, shells, and skins into sustainable, high-value ingredients for functional foods, nutraceuticals, and clean-label cosmetics. Press-cake, once treated largely as low-value animal feed, can be processed into defatted high-protein walnut flour with strong emulsification and water-binding properties, ideal for gluten-free bakery, plant-based meat binders, and ready-to-drink protein beverages.

Finely milled walnut shell powder can also replace synthetic microbeads in exfoliating scrubs and toothpaste formulations, a shift that has been accelerated by the EU’s 2023 directive on single-use plastics and similar bans in North America. Even polyphenol-rich walnut skins are being explored for antioxidant extracts in nutraceutical capsules and functional beverages.

As evolving consumer preferences and regulatory pressures converge on waste reduction and natural sourcing, upcycled walnut derivatives will allow producers to diversify portfolios, command premium pricing, and penetrate adjacent high-growth markets.

Category-wise Analysis

Product Type Insights

Kernels are anticipated to dominate in 2025 with an approximate market share of 42%, as they are perfectly placed at the intersection of clean-label snacking, bakery inclusions, and cereal fortification, monetizing familiar formats such as halves and pieces with minimal processing and broad retailer acceptance.

Their ubiquity is accentuated even more as food manufacturers lean on kernels for premiums, texture, and ALA omega-3 claims in snacks, granola, cookies, and confectionery. In practice, kernels mainly benefit from stable line integration, implying that they carry no reformulation risk, and wide country-of-origin sourcing that supports year-round procurement for private labels and brands. Even as value-added derivatives find market footing, bakery and cereal lines are likely to continue utilizing kernels for bite, visual appeal, and label simplicity.

Walnut milk is projected to be the fastest-growing product type, estimated to exhibit the highest CAGR through 2032. Its high growth pace is primarily attributable to the surging demand for plant-based milk alternatives and walnut milk’s distinct nutritional advantages over other milks made from soy, almond, or hazelnut.

Retailers and cafés are expanding their shelf spaces and menus, respectively, to incorporate walnut milk and other derivatives into their lineups, as sugar-free/organic claims soar across urban areas in several large economies. Meanwhile, formulators are capitalizing on protein fortification and emulsification synergies using walnut flour or powder to improve body and foam.

End-user Insights

The food & beverages segment is anticipated to lead with a market share of 48.2% in 2025, owing to the powerful nutritional profile of walnuts, from omega-3 fatty acids and antioxidants to protein and fiber. Consumers are increasingly seeking plant-based, clean-label, and functional foods that deliver tangible health benefits, especially for heart and brain health.

Food companies are converting walnuts into gluten-free flours, dairy-alternative oils, and vegan-friendly protein bases for snacks. At the same time, regulatory bodies such as the California Walnut Commission are actively funding health campaigns and expanding the global retail presence of walnut ingredients.

Backed by initiatives such as the U.S. Department of Agriculture’s (USDA) US$ 7 Mn export program, manufacturers are smartly leveraging walnuts’ adaptability to capture booming opportunities in snacks, confectionery, and plant-based dairy.

In contrast, the fastest-growing end-use segment through 2032 is personal care & cosmetics, as walnut-derived ingredients gain traction in the natural skincare and haircare space. Walnut oil, packed with antioxidants and anti-aging compounds, is prized for its silky texture, while finely milled walnut shells provide a biodegradable alternative to synthetic microbeads in exfoliants.

With the demand for botanical, clean-label, and cruelty-free beauty products rising, this niche has become a hotbed of innovation, blending wellness with sustainability. Moreover, the anti-inflammatory properties of walnut oil position it uniquely in the personal care space, setting it apart from purely edible applications.

Global cosmetics brands are integrating walnut-based actives into formulations, with R&D and advocacy from bodies such as the Personal Care Products Council further accelerating adoption.

Regional Insights

North America Walnut Ingredients Market Trends

North America is expected to command a 39.0% of the walnut ingredients market share in 2025, with the U.S. contributing nearly two-thirds of this regional demand. The market in the continent is primarily driven by a mature food processing industry, high consumer awareness of plant-based nutrition, and a strong adoption of functional ingredients rich in omega-3 fatty acids and antioxidants.

Regional manufacturers are incorporating different walnut formats, such as flour and oil, into health-oriented snacks, gluten-free baked goods, and dietary supplements. Furthermore, the personal care and cosmetics sector in the region is gradually expanding the usage of walnut derivatives, leveraging their anti-aging, moisturizing, and exfoliating benefits. The US$ 7 Mn funding by the USDA for promoting walnut exports from California has bolstered supply chains and amplified the global reach of walnut growers in the region.

Asia Pacific Walnut Ingredients Market Trends

Asia Pacific is expected to be the fastest-growing regional market between 2025 and 2032, fueled by increasing health awareness in the populous markets of China and India, rapid urbanization across the continent, and the proliferation of e-commerce operations that are boosting online sales of walnut-based snacks and other derivatives.

China’s extensive walnut production works as a strong force of uninterrupted growth for the regional market, while India’s 2023 tariff cuts on U.S. walnut imports have stimulated broader demand for high-quality imported walnut ingredients.

In Japan and South Korea, wellness and beauty trends are stimulating walnut integration in personal care, protein-enriched bakery goods, and nutraceuticals. With a growing middle class prioritizing plant-based diets and clean-label products, market players across Asia Pacific are innovating walnut applications for cognitive health, anti-inflammatory benefits, and premium natural foods.

Europe Walnut Ingredients Market Trends

Europe is projected to hold about 19.4% of the walnut ingredients market share, driven by a consumer base that values regulation-compliant practices, sustainability, organic sourcing, and transparent labeling. The demand for organic foods, fortified products, and botanically derived cosmetics is growing stronger in the region, particularly in Germany, France, and the U.K. Adhering to European Food Safety Authority (EFSA) standards builds consumer trust in clean-label walnut flour, oil, and protein used in bakery products, nutraceuticals, and natural cosmetics.

Imported Californian walnuts enjoy a competitive edge due to consistent quality that adheres to EU regulations. The region also leads in gluten-free innovation and plant-based alternatives, aligning with progressive health and ethical sourcing trends. Rising consumer focus on reducing carbon footprints and ensuring traceable supply chains reinforces the ongoing market growth for walnut ingredients in the region.

Competitive Landscape

The global walnut ingredients market is rapidly gaining momentum due to the interplay of various converging and diverging factors. Leading industry players such as Archer-Daniels-Midland (ADM), Olam Group, and Diamond Foods are leveraging vertical integration and consolidation to reduce costs and speed innovation across walnut oils, flours, and meals.

Other companies are simultaneously pursuing premiumization and functional differentiation in a bid to capitalize on the demand for nutrient-rich walnut products, such as omega-3-packed kernels and cold-pressed oils, targeting health-focused sectors including functional foods, dairy alternatives, and nutraceuticals.

Geopolitical tensions and trade conflicts are introducing instability into the supply chain and pricing of walnut ingredients. Moreover, evolving regulations and consumer preference for sustainable, clean-label cosmetics are opening new markets for walnut by-products such as shell powders and press cakes in natural personal care.

Key Industry Developments:

- In June 2025, the Walnut Research Station in Kupwara, Jammu and Kashmir, launched India's first walnut orchard tagged with QR codes. Scanning the code provided detailed information about each tree, including its variety, age, and nutritional content. This initiative has modernized horticulture, improved traceability, and enhanced orchard management, disease tracking, and quality control.

- In June 2025, a study at NUTRITION 2025 by the University of Illinois found that walnut consumption improved gut health, insulin response, and gut permeability in obese adults without diabetes or gastrointestinal disease. Walnuts increased beneficial gut bacteria such as Roseburia and reduced harmful bile acids.

- In April 2025, Elmhurst expanded its distribution in Whole Foods Market nationwide, introducing three new plant-based milks: Pistachio Barista Edition, Unsweetened Coconut Cashew Milk, and Maple Walnut Barista Edition. These products cater to the growing demand for simple, high-quality ingredients, offering barista-approved options that work well in coffee and beyond. The Maple Walnut Barista Edition combined walnut milk with maple syrup for a naturally sweet, refined sugar-free option.

Companies Covered in Walnut Ingredients Market

- Archer-Daniels-Midland Company (ADM)

- Olam Group Limited

- Mariani Packing Company, Inc.

- Hammons Products Company

- Poindexter Nut Company

- Diamond Foods, LLC

- Morada Nut Company

- Anderson International, Corp.

- La Morella Nuts

Frequently Asked Questions

The walnut ingredients market is projected to reach US$ 2.00 Bn in 2025.

Growing consumer awareness about plant-based omega-3 fatty acids and their role in cardiovascular health, cognitive function, and inflammation management is driving the market growth.

The walnut ingredients market is poised to witness a CAGR of 5.6% from 2025 to 2032.

Introduction of upcycled walnut derivatives and regulatory pressures to reduce waste and promote natural sourcing of ingredients are key market opportunities.

Archer-Daniels-Midland Company (ADM), Olam Group Limited, and Mariani Packing Company, Inc. are some key market players.