- Sensors & Controls

- Electronic Sensor Market

Electronic Sensor Market Size, Share, and Growth Forecast 2025 - 2032

Electronic Sensor Market by Product Type (Pressure Sensor, Temperature Sensor, Motion Sensor, Light Sensor, Position and Proximity Sensors, Biosensors, Touch Sensor, Image Sensors, Acoustic Sensors, Others), by Sensor Technology (MEMS, CMOS/CCD, Photonics, Piezoelectric, Electrochemical, Magneto-resistive, Ultrasonic, Quantum Sensors, Others), by Application (Automotive & Transportation, Consumer Electronics, Industrial Automation, Healthcare & Medical Devices, Aerospace & Defense, Energy & Utilities, Building Automation, Environmental Monitoring, Others), by Regional Analysis, 2025 - 2032

Electronic Sensor Market Size and Trend Analysis

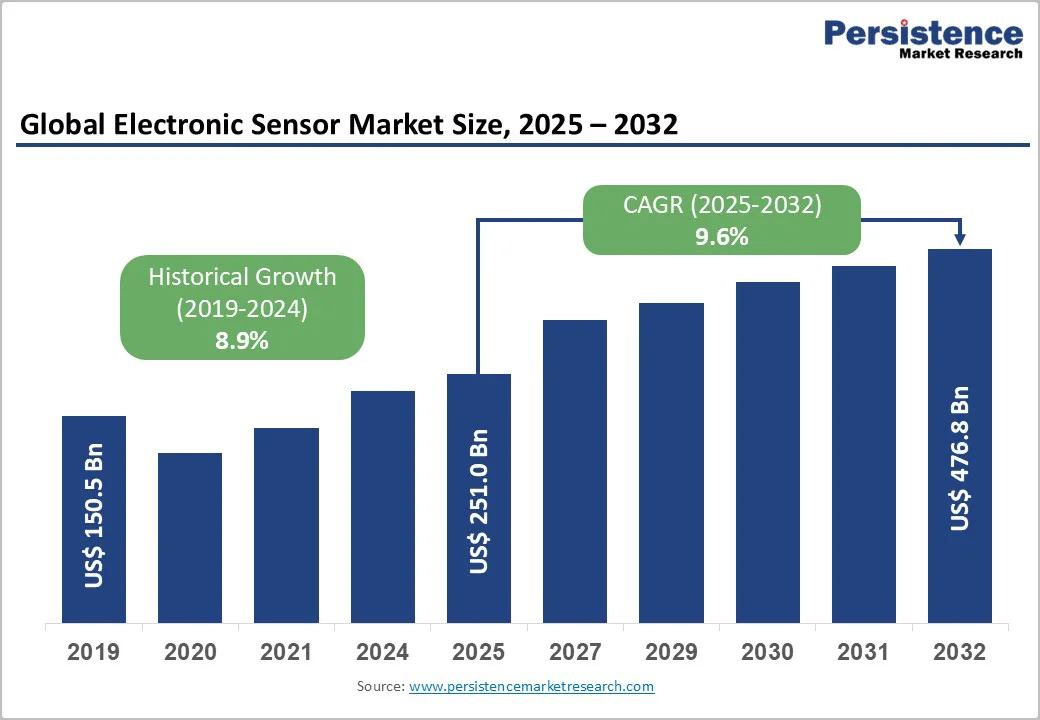

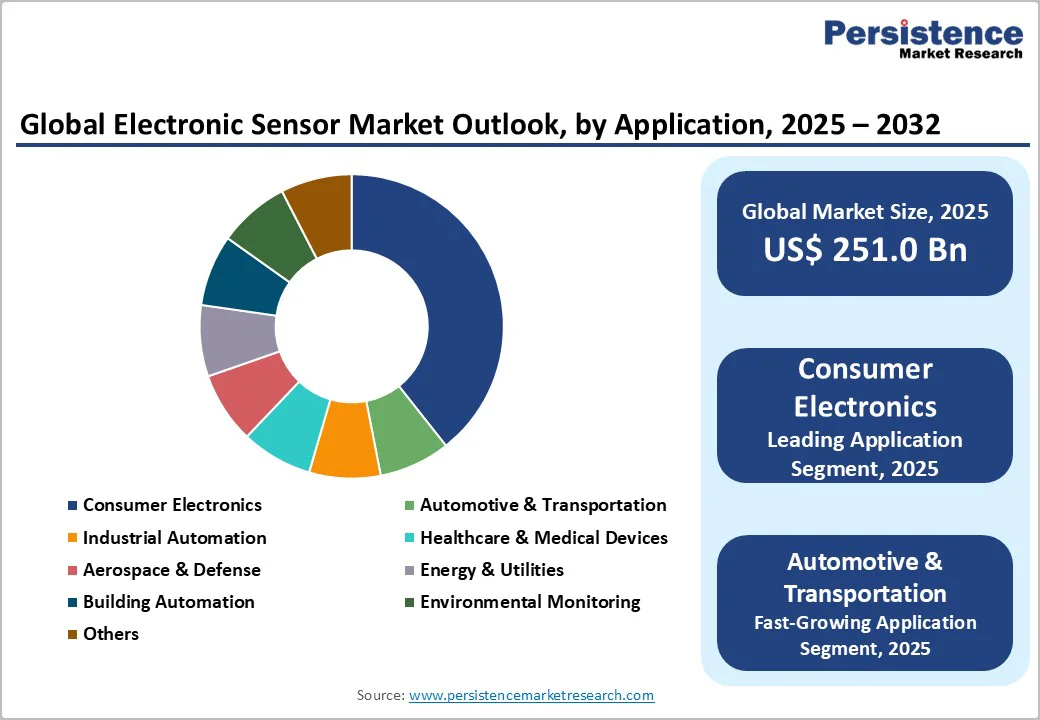

The global electronic sensor market size is linked to be valued at US$ 251.0 billion in 2025 and projected to reach US$ 476.8 billion by 2032, growing at a CAGR of 9.6% between 2025 and 2032.

The market expansion is fundamentally driven by accelerating adoption of Internet of Things (IoT) devices, autonomous vehicles, and Industry 4.0 manufacturing initiatives across global economies.

Rising demand for real-time data monitoring through sophisticated sensor technologies, coupled with government investments in smart city infrastructure and environmental monitoring systems, creates compelling drivers for sustained market growth.

Key Market Highlights

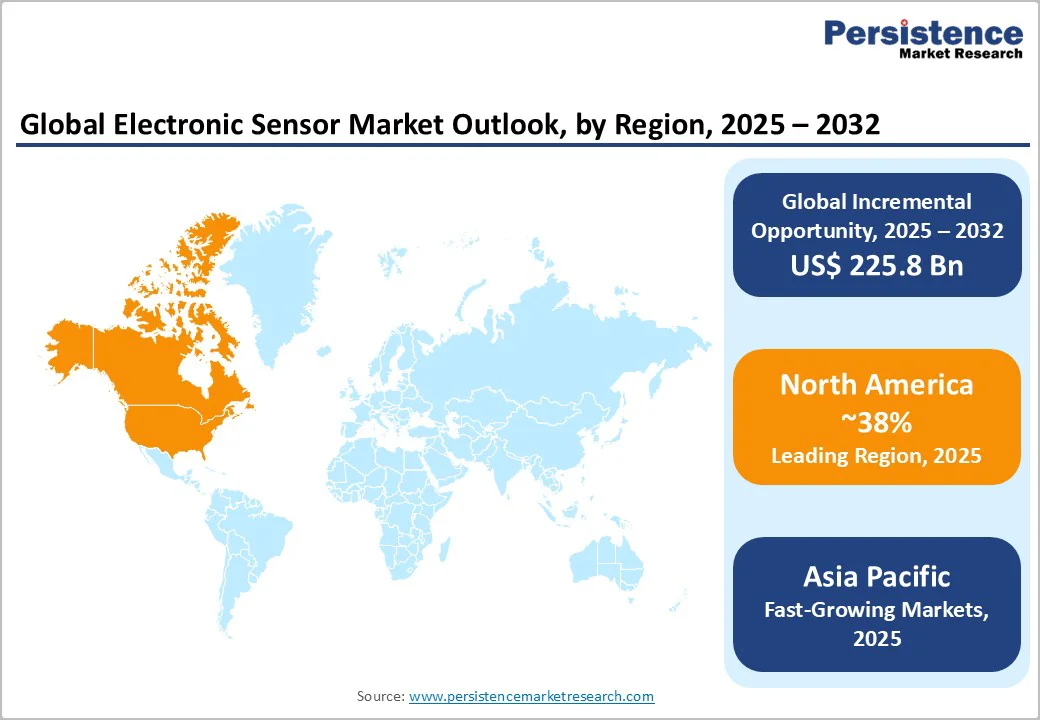

- Leading Region: North America lead the global electronic sensor market in 2025 with a 38% share, driven by automotive, aerospace, defense, strong regulations, and advanced innovation ecosystems

- Fastest Growing Region: Asia-Pacific is the fastest-growing regional market with a projected CAGR of over 12.8% through 2032, fueled by smartphone and consumer electronics production, EV adoption, Industry-4.0 initiatives, and emerging manufacturing hubs.

- Dominant Segment: Image sensors hold the largest segment with 20% market share in 2025, propelled by smartphone growth, ADAS integration, surveillance infrastructure, and autonomous vehicle perception requirements.

- Fastest Growing Segment: Pressure sensors are the fastest-growing segment with a projected CAGR of 11.4% through 2032, supported by automotive safety, industrial automation, healthcare wearables, and environmental monitoring applications.

- Key Market Opportunity: Automotive electrification and autonomous vehicle development offer the primary growth opportunity, driven by EV battery management sensor needs, ADAS mandates, autonomous perception systems, and regulatory safety requirements.

| Key Insights | Details |

|---|---|

| Electronic Sensors Market Size (2025E) | US$ 251.0 billion |

| Market Value Forecast (2032F) | US$ 476.8 billion |

| Projected Growth CAGR (2025 - 2032) | 9.6% |

| Historical Market Growth (2019 - 2024) | 8.9% |

Market Dynamics

Market Growth Drivers

Internet of Things Proliferation and Smart Device Ecosystem Expansion

The explosive growth of Internet of Things (IoT) applications across consumer, industrial, and healthcare domains represents the primary growth catalyst driving global electronic sensor demand. Global IoT sensor market was valued at approximately US$ 14.8 billion in 2022, with projections exceeding US$ 209.4 billion by 2033, representing remarkable CAGR of 27.3%.

Smart devices including smartphones with ambient light sensors and proximity detection, smartwatches incorporating biometric sensors, and connected home appliances incorporating environmental sensors represent baseline IoT applications generating consistent sensor demand.

Industrial IoT (IIoT) deployment across manufacturing facilities, supporting predictive maintenance and production optimization, accelerates demand for advanced pressure sensors, temperature sensors, and motion sensors enabling real-time monitoring.

Wearable electronics expansion incorporating biometric sensors for continuous health monitoring drives healthcare sensor adoption, with over 80% of United States hospitals implementing remote patient monitoring systems.

Government smart city initiatives across Asia-Pacific and Europe deploying sensor networks for traffic management, environmental monitoring, and energy efficiency optimization create substantial policy-driven sensor demand. Building automation systems increasingly incorporate environmental sensors for occupancy detection, temperature regulation, and air quality monitoring, supporting energy consumption reduction objectives.

Automotive Electrification and Advanced Driver Assistance Systems Integration

Automotive industry represents the largest single application segment for electronic sensors, with global automotive sensors market projected to reach US$ 89.6 billion by 2032, expanding at CAGR of 12.3% through forecast period.

Electric vehicle (EV) proliferation requires sophisticated battery management sensors, thermal sensors monitoring cooling systems, and regenerative braking sensors enabling energy recovery optimization. Advanced Driver Assistance Systems (ADAS) mandate comprehensive sensor suites including imaging sensors for lane detection and pedestrian recognition, ultrasonic sensors for parking assistance, and radar sensors for collision avoidance.

Autonomous vehicle development progression toward Level 4-5 autonomy requires 360-degree environmental awareness through multi-modal sensor fusion combining cameras, LiDAR, and radar, establishing extraordinarily demanding sensor specifications.

Government regulations establishing mandatory safety requirements increasingly mandate ADAS deployment in new vehicles, creating regulatory-driven sensor adoption. Electric and hybrid vehicles require specialized sensors for battery state monitoring, thermal management, and powertrain optimization, expanding total sensor requirements per vehicle beyond conventional platforms.

Market Restraints

High Cost of Advanced Sensor Technologies and Integration Complexity

Advanced sensors such as MEMS, CMOS image sensors, and photonic devices involve substantial R&D investments, creating high market entry barriers. Manufacturing requires sophisticated semiconductor fabrication, precision etching, and specialized packaging, demanding significant capital expenditure.

Integrating multiple sensor modalities into unified systems involves complex signal conditioning, analog-to-digital conversion, and data fusion, increasing implementation challenges. Industrial 4.0 deployments require upgrading infrastructure, training personnel, and embedding sensors into existing systems, further raising costs.

Miniaturization drives advanced packaging needs, escalating per-unit production costs, while supply chain disruptions constrain semiconductor availability. High-reliability applications, including automotive and aerospace, impose rigorous testing and certification requirements, extending development timelines and adding to overall manufacturing expenditure.

Sensor Data Privacy Concerns and Cybersecurity Vulnerabilities in Connected Systems

IoT and connected sensor systems collect vast amounts of personal and operational data, necessitating robust privacy protections and data governance. Wearable devices capturing biometric or health information raise privacy risks, while connected and autonomous vehicle sensors present critical safety vulnerabilities if compromised. Industrial sensor networks face potential cyberattacks targeting intellectual property and production systems.

Environmental monitoring and smart home sensors transmitting real-time data risk interception or manipulation, affecting consumer confidence. Regulatory frameworks like GDPR and emerging data protection laws impose strict compliance obligations, increasing operational complexity and costs. Security and privacy concerns can slow adoption, particularly in sensitive applications such as healthcare, automotive, and residential IoT environments.

Market Opportunities

Quantum Sensor Technology Development and Defense/Aerospace Applications

Quantum sensors represent frontier sensing technology utilizing quantum mechanical principles to achieve unprecedented sensitivity and accuracy, with significant applications in defense and aerospace domains.

Quantum-enhanced sensors including quantum accelerometers, quantum gyroscopes, and quantum magnetometers provide navigation capabilities operating independently of Global Positioning System (GPS) infrastructure, enabling secure operations in GPS-denied environments.

Defense applications for quantum sensors include electronic warfare systems, radar technology enhancement, and secure communication infrastructure supporting quantum key distribution (QKD) protocols.

Aerospace applications for quantum sensors include inertial navigation systems for aircraft and spacecraft operating without GPS dependency, representing critical capability for autonomous operations. Honeywell's Quantum Apertures project, funded through Defense Advanced Research Projects Agency (DARPA), develops programmable wideband Rydberg-based quantum sensors for military applications.

Advanced integrated photonics enabling miniaturization of laser sources and vacuum chambers accelerates quantum sensor transition from laboratory environments to field deployment, creating substantial market opportunity within aerospace and defense sectors.

Environmental Monitoring and Air Quality Sensing Applications Expansion

Environmental monitoring applications incorporating electronic sensors represent fastest-growing market segment, driven by government regulations mandating air quality monitoring, water quality assessment, and climate change impact measurement.

Wearable air quality monitoring devices incorporating metal oxide semiconductor (MOS) gas sensors and particulate matter sensors enable personal exposure assessment for pollution-sensitive populations. Smart cities including London, Beijing, and New York deploy extensive.

Healthcare facilities deploy environmental monitoring sensors tracking indoor air quality, temperature, humidity, and pathogen levels supporting infection prevention and patient safety. Water quality monitoring applications employ photonic sensors and electrochemical sensors detecting contaminants and microorganism presence, ensuring drinking water safety across municipal systems.

Renewable energy systems incorporating solar and wind generation require sophisticated environmental sensors monitoring atmospheric conditions, temperature, and irradiance levels optimizing energy generation efficiency.

Category-wise Insights

Product Type Analysis

Image sensors dominate the product type segment with 20% market share in 2025, driven by widespread adoption in smartphones, surveillance systems, and autonomous vehicles. Advanced smartphone cameras leverage high-resolution image sensors for computational photography, facial recognition, and video capture, establishing baseline consumer demand.

Autonomous driving increasingly relies on multiple image sensors for 360-degree environmental perception, supporting decision-making and safety systems. Surveillance and security applications expand networks of high-resolution sensors, enabling real-time monitoring and analytics. The convergence of consumer, automotive, and industrial demand underscores the critical role of image sensors as a foundational technology shaping the electronic sensor market.

Technology Analysis

CMOS (Complementary Metal-Oxide-Semiconductor) technology leads sensor implementations with 36% market share in 2025 due to its energy efficiency, compact form factor, and cost-effectiveness. CMOS fabrication enables high-quality imaging, superior sensitivity, and enhanced integration density compared to legacy CCD technologies, supporting mass production across consumer electronics, automotive, and industrial applications.

Its versatility allows embedding sensors in smartphones, cameras, and wearable devices, while providing scalability for advanced industrial deployments. The technology’s balance of performance, power consumption, and manufacturability establishes CMOS sensors as the backbone of modern electronic sensing solutions, driving widespread adoption and continuous innovation across multiple market segments.

End Use Industry Analysis

Consumer Electronics dominates application segments with approximately 42.7% market share in 2025, encompassing smartphones, smartwatches, tablets, and connected appliances incorporating diverse sensor types. Smartphones universally integrate ambient light sensors for display brightness optimization, proximity sensors for call handling, and motion sensors supporting gesture recognition.

Wearable technology including smartwatches and fitness trackers incorporate biometric sensors monitoring heart rate, blood oxygen saturation, and activity patterns. Smart home solutions including thermostats, refrigerators, and washing machines incorporate environmental and motion sensors enabling intelligent operation and remote control.

Automotive & Transportation applications represent fastest-growing segment with anticipated CAGR of 12.3% through 2032, driven by electric vehicle adoption and autonomous vehicle development. Vehicle electrification requires battery management sensors, thermal monitoring sensors, and power electronics sensors supporting safe and efficient operation.

Autonomous vehicle development demands comprehensive sensor suites including cameras, LiDAR, radar, and ultrasonic sensors enabling environmental perception and decision-making.

Regional Insights

North America Electronic Sensor Trends

North America maintains market leadership with approximately 38% of global electronic sensor market share in 2025, driven by strong automotive industry, advanced consumer electronics ecosystem, and substantial aerospace and defense investments.

United States automotive manufacturers including General Motors, Ford, and Tesla lead global ADAS adoption, driving sophisticated sensor integration across vehicle platforms. U.S. government defense initiatives including DARPA-funded quantum sensor projects and advanced aerospace programs establish substantial demand for sophisticated sensing technologies in military applications.

Silicon Valley technology ecosystem supports consumer electronics innovation, with companies integrating diverse sensor modalities into smartphones, wearables, and IoT devices.

Canadian market exhibits comparable regulatory requirements to United States, supporting consistent regional adoption patterns. Honeywell's NextGen Industrial IoT Sensor Suite launched in 2024 integrates humidity, pressure, and motion sensors for remote manufacturing facility monitoring, exemplifying market innovation trajectories.

U.S. automotive industry leadership in connected and autonomous vehicle development sustains premium sensor technology adoption supporting advanced capability implementation.

Europe Electronic Sensor Trends

Europe commands approximately one-third of global electronic sensor market share in 2025, with Germany maintaining position as largest market driven by automotive manufacturing excellence and industrial automation leadership. Germany's automotive industry leadership including Volkswagen, BMW, and Daimler accelerates ADAS adoption and sensor technology integration across European vehicle platforms.

European Union regulatory initiatives including Euro 7 emissions standards and safety mandates drive adoption of sophisticated environmental and safety sensors. United Kingdom, France, and Spain implement automotive regulations supporting electric vehicle adoption and autonomous driving capabilities, establishing regional sensor demand drivers.

German smart manufacturing initiatives and Industrial Internet of Things expansion accelerates adoption of environmental monitoring sensors and process optimization sensors. France and Spain support automotive innovation through government incentives and research funding supporting sensor technology development.

European aerospace industry including Airbus operations maintains substantial sensor demand for aircraft systems and advanced avionics integration.

Asia Pacific Electronic Sensor Trends

Asia-Pacific represents fastest-growing regional market with projected CAGR exceeding 12.8% through 2032, supported by massive smartphone production, automotive industry expansion, and Industry 4.0 adoption. China commands dominant position within Asia-Pacific region, maintaining global smartphone and consumer electronics manufacturing supremacy requiring extensive sensor integration.

STMicroelectronics' NXP MEMS acquisition reflects strategic recognition of Asia-Pacific automotive growth potential and manufacturing advantages. Chinese government initiatives including Made in China 2025 and Industrial IoT programs drive substantial sensor technology investments supporting domestic manufacturing capabilities.

Japan maintains technological leadership in sensor design and miniaturization through companies including Rohm Semiconductor and Omron Corporation. India's "Make in India" program and government push toward smart manufacturing accelerates electronic sensor adoption in emerging manufacturing sector.

Singapore's Smart Nation initiative and Thailand 4.0 program drive smart city sensor deployment across Southeast Asia. ASEAN countries including Vietnam and Malaysia emerge as semiconductor manufacturing hubs attracting global sensor production investment. Chinese automotive market expansion toward electric vehicles and autonomous capabilities drives automotive sensor demand growth substantially exceeding global growth rates.

Competitive Landscape

Market Structure Analysis

The global electronic sensor market demonstrates moderate consolidation, with competition between large multinational semiconductor manufacturers and specialized sensor firms.

Market structure is characterized by a mix of diversified portfolios serving automotive, industrial, and consumer applications, alongside niche players focusing on specific sensor technologies or end-use segments. Companies increasingly pursue strategic acquisitions, partnerships, and vertical integration to strengthen technological capabilities and expand market share.

Key business strategies center on investing in research and development for advanced MEMS miniaturization, AI-enabled signal processing, and emerging sensing technologies such as quantum sensors. Differentiation is achieved through integrating sensor hardware with processing electronics, developing software platforms for real-time analytics, and providing specialized solutions tailored to automotive, industrial, and IoT applications.

Market leaders leverage platform-based approaches to combine sensors with data-driven services, enabling comprehensive solutions that enhance predictive maintenance, automation, and smart manufacturing. Continuous innovation and ecosystem collaboration remain critical to maintaining competitive positioning in this rapidly evolving market.

Key Market Developments

- November 2025: Sony introduced the IMX900 global-shutter image sensor for industrial robotics and automation, featuring high dynamic range and LED flicker mitigation for precise object detection.

- July 2025: STMicro announced a deal to acquire part of NXP’s sensor business for up to US$ 950 million, significantly boosting its MEMS and Electronic-sensor capabilities for automotive and industrial applications.

- September 2025: Honeywell introduced new pressure and environmental sensors for industrial applications, supporting predictive maintenance and facility monitoring, exemplifying integration of sensing technologies in smart manufacturing environments.

Companies Covered in Electronic Sensor Market

- ROHM Semiconductor

- ams OSRAM AG

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- TE Connectivity Ltd.

- Murata Manufacturing Co., Ltd.

- Robert Bosch GmbH

- Infineon Technologies AG

- Qualcomm Technologies Inc.

- Omron Corporation

- Texas Instruments

- Analog Devices Inc.

- Honeywell International Inc.

- Siemens AG

- SICK AG

- Sony Semiconductor Solutions

- TDK Corporation

- onsemi Corporation

- Panasonic Corporation

- Samsung Electronics Co. Ltd.

- Delphi Automotive

Frequently Asked Questions

The market is valued at US$ 251.0 B in 2025 and projected to reach US$ 476.8 B by 2032, growing at a 9.6% CAGR.

Growth is driven by IoT adoption, automotive electrification and ADAS, Industry 4.0, autonomous vehicles, wearable health devices, and smart city initiatives.

Image sensors lead with ~18.8% market share, powered by smartphones, ADAS, surveillance, and autonomous vehicle vision systems.

Asia-Pacific leads with a projected CAGR above 12.8% through 2032, supported by electronics manufacturing, EV adoption, Industry 4.0, and emerging semiconductor hubs.

Automotive electrification and autonomous vehicles, requiring battery management, thermal, and 360-degree sensor suites for Level 4-5 autonomy.

Leaders include STMicroelectronics, Bosch, Infineon, Texas Instruments, Honeywell, NXP, Qualcomm, Analog Devices, and Omron, excelling in miniaturization, AI integration, automotive specialization, and platform solutions.