- Transportation & Logistics

- Electronic Logging Device (ELD) Market

Electronic Logging Device (ELD) Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Electronic Logging Device (ELD) Market by Vehicle Type (Heavy Commercial Vehicles [HCVs], Light Commercial Vehicles [LCVs], Buses and Coaches), Fleet Size (Medium Fleets [50-249 vehicles], Large Fleets [250+ vehicles], Small Fleets [1-49 vehicles]), Application (Fleet Management, Compliance Monitoring, Driver Performance & Monitoring, Vehicle Diagnostic, Others), and Regional Analysis for 2025 - 2032

Electronic Logging Device (ELD) Market Size and Trends Analysis

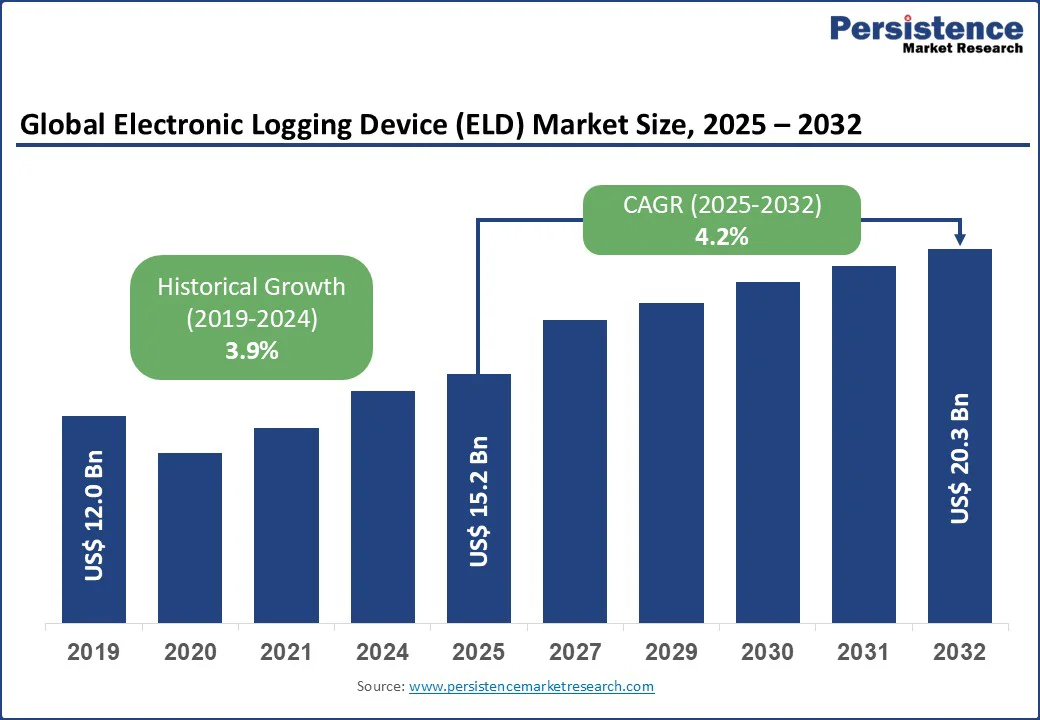

The global electronic logging device (ELD) market size is likely to be valued at US$ 15.2 Bn in 2025, with a forecast to grow to US$ 20.3 Bn by 2032, registering a CAGR of 4.2% during 2025 - 2032.

The electronic logging device market is driven by increasing concerns over driver fatigue and accident prevention, encouraging fleets to adopt ELD solutions for safer operations. The growing e-commerce sector increases the need for efficient fleet management and compliance solutions. Increased adoption of app-based solutions for small fleets and owner-operators. Rising small fleet and e-commerce-based transportation creates demand for cost-effective ELD solutions.

Key Industry Highlights:

- Leading Vehicle Type: Heavy Commercial Vehicles hold a 50% market share in 2025, driven by ELD compliance for commercial vehicles.

- Fastest-growing Vehicle Type: Light Commercial Vehicles are fueled by GPS fleet tracking.

- Fleets Dominate: Large Fleets account for 40% market share, owing to the dominance of fleet telematics.

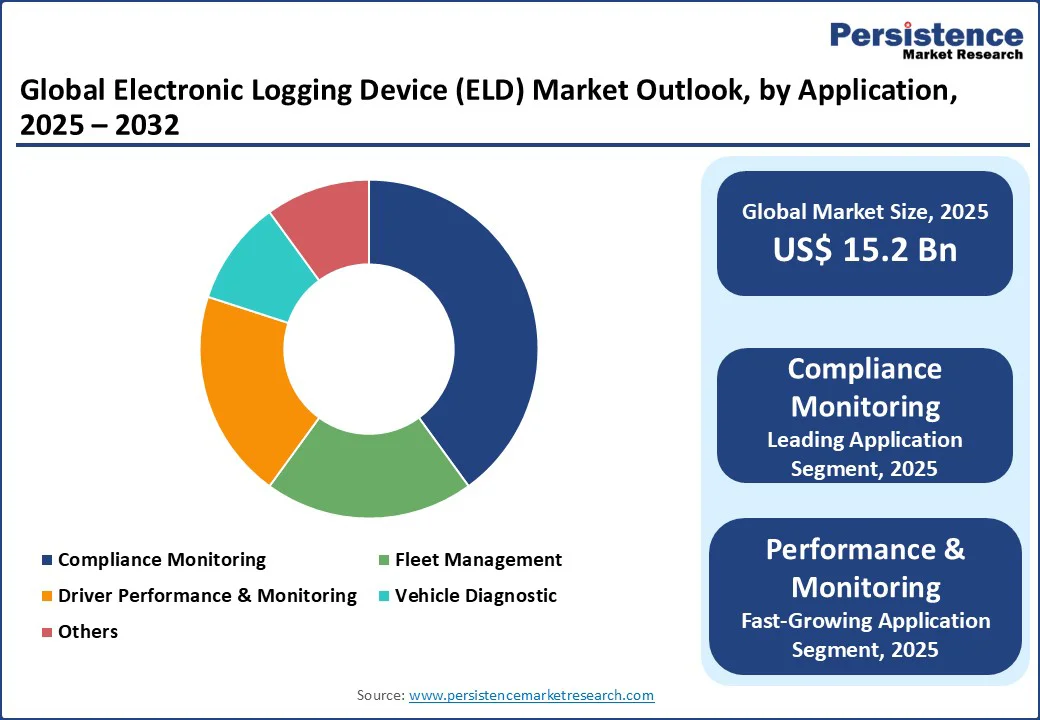

- Leading Application: Compliance Monitoring holds a 35% market share, supported by electronic logging device regulations.

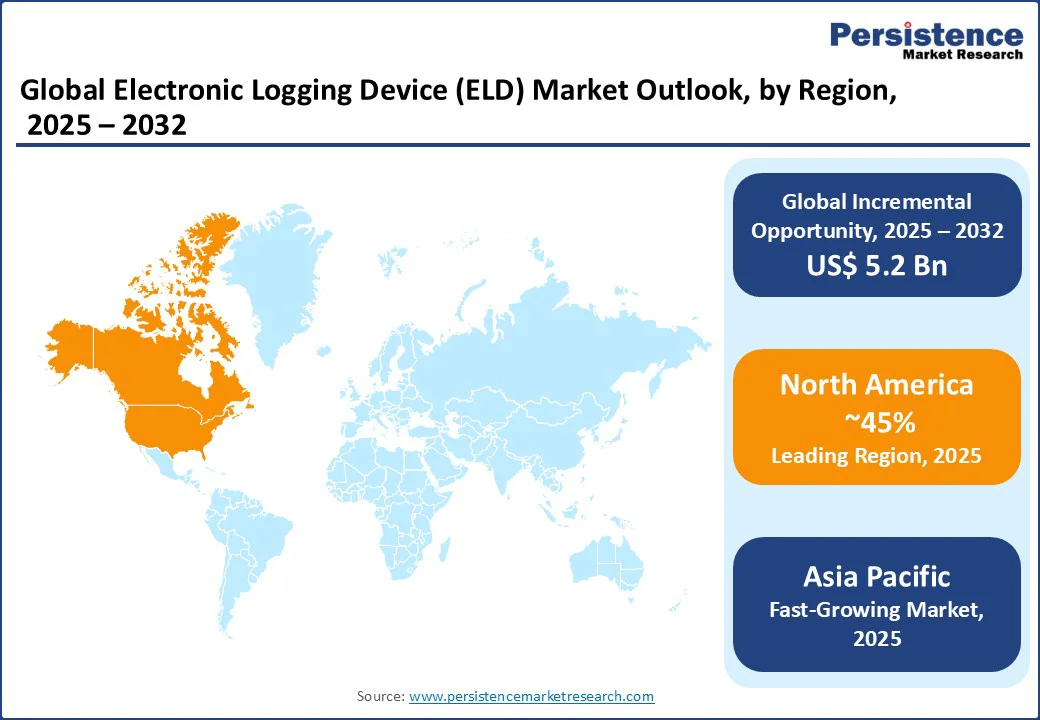

- Leading Region: North America holds a 45% market share, with the U.S. leading in trucking compliance technology.

- Fastest Growing Region: Asia Pacific holds 15% market share, driven by IoT in transportation.

|

Global Market Attribute |

Key Insights |

|

Electronic Logging Device (ELD) Market Size (2025E) |

US$ 15.2 Bn |

|

Market Value Forecast (2032F) |

US$ 20.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.9% |

Market Dynamics

Driver: Stringent Regulatory Mandates and Rising Demand for Fleet Efficiency

The electronic logging device (ELD) market is propelled by stringent ELD regulations, such as the U.S. Federal Motor Carrier Safety Administration (FMCSA) ELD mandate, and increasing demand for fleet tracking and trucking compliance technology. These regulations push fleet operators to implement ELD systems to avoid penalties and enhance accountability, particularly for Heavy Commercial Vehicles (HCVs) and buses, and coaches.

The growing need for fleet tracking and driver log automation stems from the logistics industry’s focus on optimizing operations, reducing fuel costs, and improving delivery timelines. Fleet operators, especially large fleets, leverage GPS fleet tracking to monitor vehicle locations, driver behavior, and route efficiency, boosting productivity in time-sensitive industries such as e-commerce and freight transport.

Advancements in smart logging systems and ELD integration with telematics enable real-time data insights, allowing companies to streamline fleet management, enhance driver performance & monitoring, and improve vehicle diagnostics. The rise of IoT in transportation further supports e-log devices by integrating with cloud-based platforms, offering seamless data sharing and analytics for compliance monitoring.

Restraint: High Implementation Costs and Resistance to Technology Adoption

The electronic logging device (ELD) market faces challenges due to high implementation costs and resistance to driver log automation among smaller fleets. The initial investment in ELD systems, including hardware and software from ELD hardware manufacturers, can be prohibitive for small fleets and independent operators, who often operate on tight budgets. Ongoing costs for subscriptions, maintenance, and training for smart logging systems further strain financial resources, limiting ELD adoption rate in cost-sensitive segments such as small fleets (1-49 vehicles).

Resistance to technology adoption is another challenge, particularly among drivers and small fleet operators who express concerns over data privacy and the complexity of transitioning from paper logs to e-log devices. Some drivers perceive fleet tracking as intrusive, impacting morale and slowing adoption of trucking compliance technology.

Opportunity: Advancements in IoT and Telematics Integration Will Push the Market Growth

Advancements in IoT in transportation and ELD integration with telematics present significant opportunities for the electronic logging device (ELD) market, driving demand for smart logging systems and transportation safety solutions. The integration of smart logging systems with IoT technologies enables real-time data analytics, predictive maintenance, and enhanced fleet tracking, offering fleet operators actionable insights to improve efficiency and reduce costs.

ELD integration with telematics supports advanced applications such as driver performance & monitoring, allowing companies to optimize driver behavior, reduce fuel consumption, and enhance safety through GPS fleet tracking. The expansion of logistics and e-commerce in emerging markets presents opportunities for truck log devices, as growing freight and delivery demands drive adoption in light commercial vehicles (LCVs) and medium fleets. These markets are increasingly investing in digital infrastructure, creating a favorable environment for fleet telematics market growth.

Additionally, the focus on driver safety, supported by transportation safety solutions, encourages the adoption of e-log devices to monitor driver fatigue, ensure compliance with HOS regulations, and reduce road incidents. Innovations in smart logging systems, such as mobile app-based ELDs and cloud-based platforms, offer cost-effective solutions for small fleets, further expanding market reach.

Category-wise Analysis

Vehicle Type Insights

Heavy commercial vehicles (HCVs) are likely to account for 50% share in 2025, driven by ELD compliance for commercial vehicles. HCV fleets often operate across long distances, making compliance and efficient route planning critical for safety and productivity. ELDs enable fleet managers to monitor driver performance, prevent fatigue-related accidents, and maintain real-time logs for audits and inspections.

Light commercial vehicles (LCVs) are fueled by GPS fleet tracking. LCVs, widely used in last-mile delivery, courier services, and small-scale logistics, require real-time monitoring to ensure timely deliveries and operational efficiency. The integration of ELDs with GPS technology allows fleet operators to track vehicle location, monitor driver behavior, and optimize route planning.

Fleet Size Insights

Large fleets 40% market share in 2025, driven by fleet telematics market. Large fleet operators face complex challenges, including ensuring regulatory compliance across multiple regions, reducing operational costs, and optimizing driver performance. ELDs combined with fleet telematics help address these challenges by automating Hours of Service (HOS) logs, preventing violations, and improving fuel efficiency through data-driven insights. In addition, telematics-powered ELD systems enhance route optimization, monitor vehicle health, and provide analytics to improve productivity.

Small Fleets are fueled by driver log automation. Large fleets, small fleet operators traditionally relied on manual paperwork to record Hours of Service (HOS), which is time-consuming and prone to errors. With regulatory authorities enforcing strict compliance requirements, small businesses are turning to affordable and easy-to-install ELD solutions that automate log entries and reduce administrative burdens.

Application Insights

Compliance monitoring holds a 35% market share in 2025, driven by digital logging device regulations. Government mandates, such as the FMCSA’s ELD rule in the U.S., have made it mandatory for fleet operators to adopt digital logging solutions for accurate Hours of Service (HOS) reporting.

Compliance monitoring ensures that fleets maintain adherence to legal guidelines, preventing costly violations, penalties, and operational disruptions. ELD systems simplify compliance by automating log entries, reducing paperwork, and providing real-time updates on driver status.

Driver performance & monitoring is fueled by transportation safety solutions. Fleet operators increasingly recognize the importance of monitoring driver behavior to reduce accidents, optimize fuel usage, and enhance overall efficiency.

ELD systems equipped with performance analytics track parameters such as harsh braking, rapid acceleration, speeding, and idling time. These insights enable fleet managers to identify risky driving patterns and implement corrective measures through training or incentive programs.

Regional Insights

North America Electronic Logging Device (ELD) Market Trends

North America holds a 45% global market share in 2025, with the U.S. leading due to strict E-log device regulations and advanced logistics infrastructure. The U.S. leads with widespread adoption of trucking compliance technology, driven by the FMCSA’s ELD mandate, which requires logging devices for most commercial vehicles to track HOS accurately.

The robust e-commerce ecosystem and growing demand for last-mile delivery fuel the use of GPS fleet tracking in light commercial vehicles (LCVs), as companies prioritize efficient delivery networks.

The U.S. logistics industry’s focus on transportation safety solutions drives driver log automation, with fleet operators adopting smart logging systems to enhance driver performance & monitoring and reduce accidents. Investments in IoT in transportation and ELD integration with telematics support advanced fleet management, particularly for large fleets in freight and trucking.

The presence of leading ELD hardware manufacturers and telematics providers foster innovation, with companies such as Samsara and Geotab offering integrated e-log devices to meet ELD mandate requirements in trucking. The U.S. market also benefits from a strong regulatory framework and infrastructure, encouraging fleet tracking adoption across buses and coaches and medium fleets.

Europe Electronic Logging Device (ELD) Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France, driven by digital tachograph regulations and logistics growth. Germany’s market thrives on the adoption of driver log automation and e-log devices, supported by EU regulations requiring precise tracking of driver hours to ensure road safety.

The country’s advanced logistics infrastructure and focus on trucking compliance technology drive demand for fleet tracking in large fleets, particularly in freight transport. The UK market is propelled by the need for transportation safety solutions, with smart logging systems gaining traction among medium fleets to comply with post-Brexit logistics regulations.

Emphasis on reducing carbon emissions and improving fleet efficiency encourages GPS fleet tracking and ELD integration with telematics for optimized route planning. France’s market benefits from investments in IoT in transportation, with truck log devices being adopted in buses and coaches to enhance safety and compliance.

The EU’s focus on harmonized regulations, such as Regulation 165/2014, supports compliance monitoring, driving the electronic logbook adoption rate across commercial vehicles. Companies such as TomTom Telematics lead by offering fleet telematics market solutions tailored to European logistics needs.

Asia Pacific Electronic Logging Device (ELD) Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 5.0%, led by China, Japan, and India, driven by logistics expansion and digitalization. China’s market is fueled by significant investments in logistics infrastructure, boosting demand for fleet tracking and smart logging systems in heavy commercial vehicles (HCVs).

The country’s booming e-commerce sector and increasing freight transport needs drive driver log automation, with e-log devices ensuring compliance with local safety regulations. India’s market grows due to the expanding logistics and trucking industry, with truck log devices gaining traction in small fleets to meet growing delivery demands.

The government’s push for digital infrastructure and smart cities supports IoT in transportation, encouraging GPS fleet tracking adoption. Japan’s market is driven by a focus on transportation safety solutions, with smart logging systems being adopted in buses and coaches to enhance driver safety and operational efficiency.

The region’s rapid urbanization and rising disposable incomes further boost demand for ELD systems, with companies such as Geotab leveraging ELD integration with telematics to cater to fleet management needs in emerging markets.

Competitive Landscape

The global electronic logging device (ELD) market is highly competitive, with Garmin ELD, KeepTruckin, Omnitracs, Trimble, Geotab, Samsara, Verizon Connect, AT&T Fleet Complete, Donlen, Stoneridge, TomTom Telematics, Blue Ink Technology, CarrierWeb, ORBCOMM, Pedigree Technologies, Teletrac Navman, Wheels Inc., and Transflo focusing on logging device, fleet tracking, and ELD system innovations.

Companies leverage ELD integration with telematics and trucking compliance technology to gain market share. Strategic R&D investments in smart logging systems and partnerships drive transportation safety solutions, addressing ELD mandate requirements in trucking.

Key Developments:

- In 2024, Samsara's new "smart logging system" likely refers to their continued development and integration of AI-powered features and data insights into their existing telematics and connected operations platform, which includes existing functionalities such as Hours of Service (HOS) tracking, route planning, and asset tracking.

- In 2023, Geotab expanded its GPS fleet tracking capabilities by introducing enhancements to its asset management and maintenance features within the MyGeotab platform, along with updates to its menu for better navigation, and by leveraging the Geotab Data Connector to provide deeper maintenance insights.

Companies Covered in Electronic Logging Device (ELD) Market

- Garmin ELD

- KeepTruckin

- Omnitracs

- Trimble

- Geotab

- Samsara

- Verizon Connect

- AT&T Fleet Complete

- Donlen

- Stoneridge

- TomTom Telematics

- Blue Ink Technology

- CarrierWeb

- ORBCOMM

- Pedigree Technologies

- Teletrac Navman

- Wheels Inc.

- Transflo

- Others

Frequently Asked Questions

The electronic logging device market size is projected to reach US$ 15.2 Bn in 2025, driven by logging device and fleet tracking.

ELDs enable fleet operators to monitor routes, manage fuel consumption, and enhance overall performance, resulting in improved operational efficiency and significant cost savings.

The electronic logging device market grows at a CAGR of 4.2% from 2025 to 2032, reaching US$ 20.3 Bn by 2032.

Advancements in IoT in transportation, with 15% telematics growth, drive smart logging systems.

Key players include Samsara, Geotab, Omnitracs, Verizon Connect, and TomTom Telematics.