- Technology

- Video Surveillance Market

Video Surveillance Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Video Surveillance Market by Component (Hardware, Software, Services), Technology (Analog, IP, Hybrid), Application (Commercial, Industrial, Residential, Government & Public Sector, Others), and Regional Analysis for 2026 - 2033

Video Surveillance Market Size and Trends Analysis

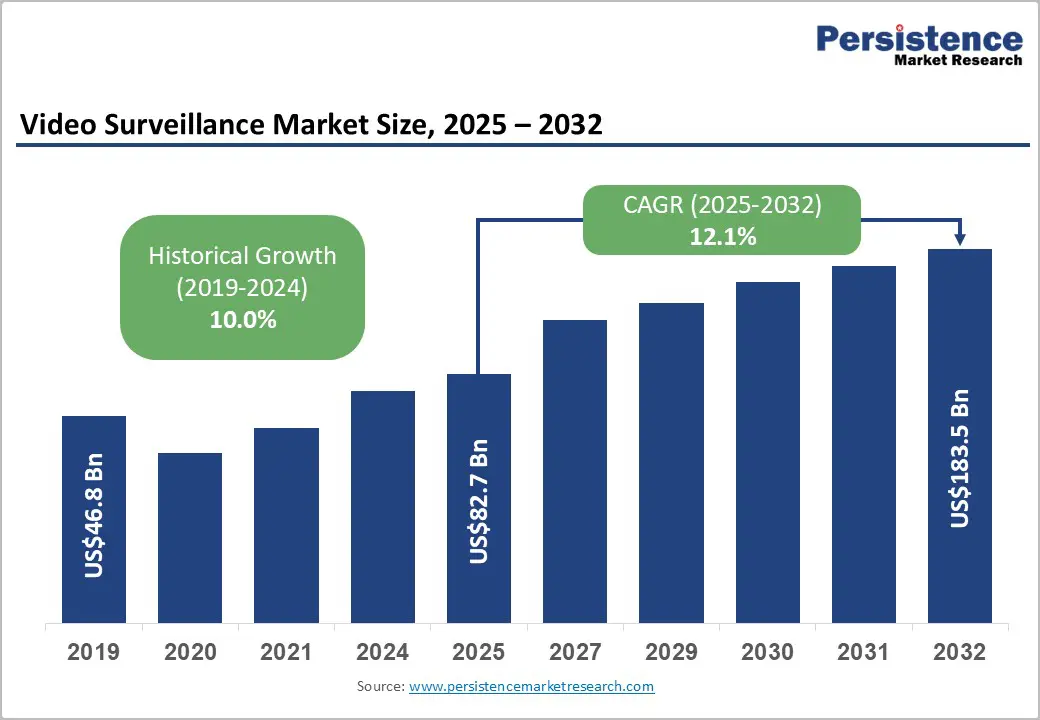

The global video surveillance market size is projected to rise from US$63.7 Bn in 2026 to US$112.8 Bn by 2033. It is anticipated that the market will grow at a CAGR of 8.5% from 2026 to 2033, driven by the convergence of artificial intelligence (AI) with edge computing, enabling real-time threat detection rather than passive recording. Rapid urbanization in emerging economies, particularly in the Asia Pacific region, has necessitated large-scale Safe City projects that integrate public safety infrastructure with intelligent monitoring.

Key Industry Highlights:

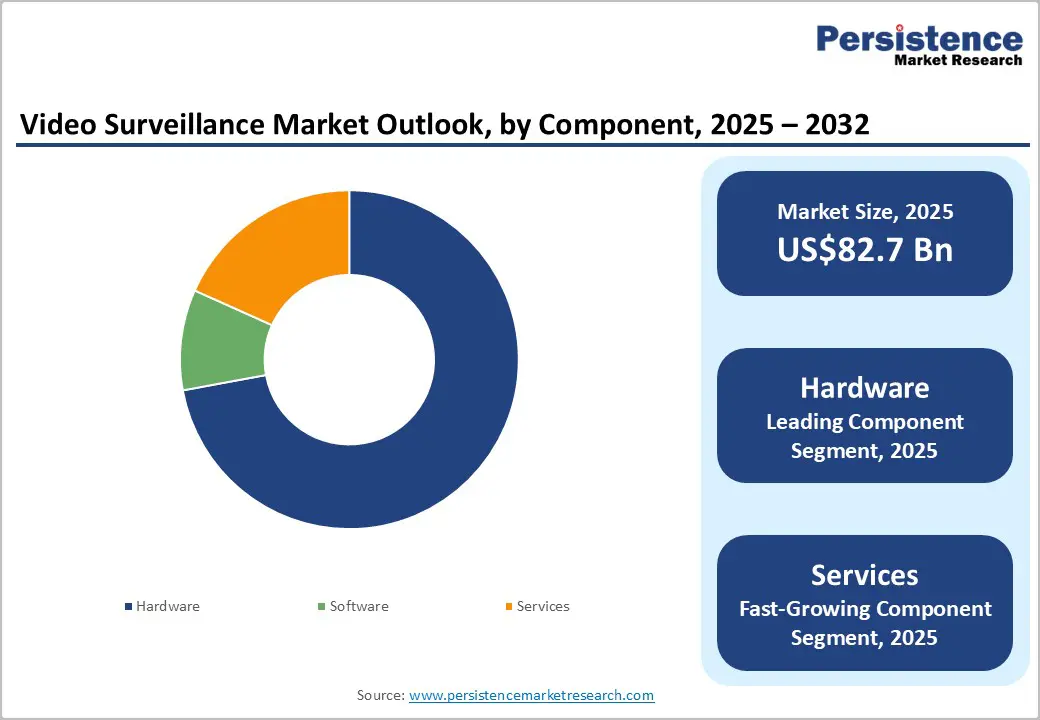

- Leading Component: Hardware dominates with over 61% market share in 2026, valued at over US$38.9 Bn, driven by demand for cameras, DVRs/NVRs, and sensors to ensure real-time monitoring, high-resolution imaging, and reliable storage. Software is the fastest-growing segment, with a 12.4% CAGR, driven by AI-based analytics, cloud integration, and remote management needs.

- Leading Technology: IP technology holds over 56% market share in 2026, valued at more than US$ 35.7 Bn, offering high scalability, image quality, and PoE simplicity. Hybrid systems are the fastest-growing, with an 8.9% CAGR, offering cost-effective upgrades by combining IP and analog advantages.

- Leading Application: Commercial commands the largest share at over 30% in 2026, valued above US$ 19.1 Bn, driven by retail, office, and public building security. Residential is growing fastest at 12.7% CAGR, supported by smart homes, IoT-enabled cameras, and remote monitoring capabilities.

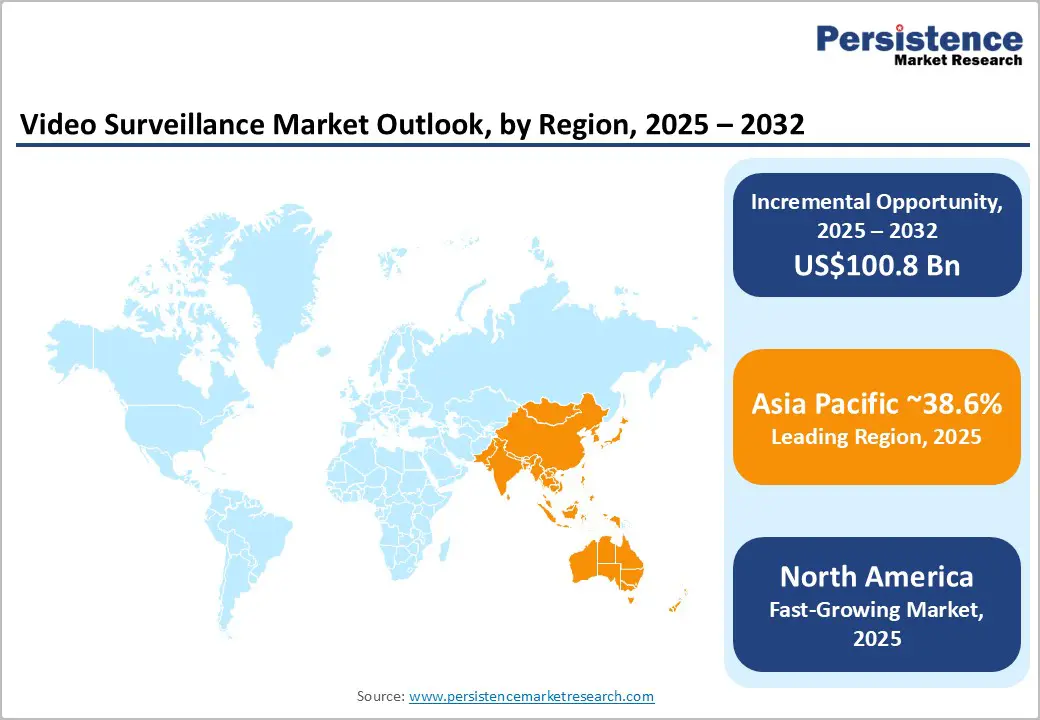

- Leading Region: Asia Pacific leads with more than 39% share in 2026, valued at US$ 24.8 Bn, driven by urbanization, government safety initiatives, and low-cost manufacturing. North America holds over 28% share, valued at US$ 17.8 Bn, supported by AI adoption, cloud solutions, and NDAA-driven replacement cycles. Europe accounts for more than a 20% share by 2033, driven by GDPR, AI Act regulations, and the demand for intelligent traffic and public transport surveillance.

- Market Dynamics: Rising security concerns, urbanization, and smart city initiatives are driving demand, while privacy regulations and geopolitical supply chain disruptions are restraining growth. The adoption of video surveillance as a service (VSaaS) and its convergence with IoT, access control, and AI-enabled smart building solutions is creating a significant opportunity.

| Key Insights | Details |

|---|---|

|

Video Surveillance Market Size (2026E) |

US$63.7 Bn |

|

Market Value Forecast (2033F) |

US$112.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.7% |

Market Dynamics

Driver - Rising Security Concerns and Crime Rates

Urbanization and population density have heightened risks of theft, vandalism, and violent crime, prompting widespread deployment of surveillance systems in public spaces and residential complexes. Law enforcement agencies increasingly rely on real-time monitoring and recorded footage to improve crime detection, investigation, and response times. Critical infrastructure, such as airports, metros, and utilities, is expanding surveillance coverage to mitigate terrorism and sabotage threats. Retailers and offices use video surveillance to prevent shoplifting, internal theft, and workplace misconduct. In 2024, at least nearly 50,000 lives were lost to armed conflict worldwide (roughly one every 12 minutes), highlighting the broad insecurity that also drives the need for monitoring systems in sensitive zones.

Smart City and Infrastructure Development Initiatives

Smart city and large-scale infrastructure development initiatives are significantly driving demand by prioritizing public safety, traffic management, and urban efficiency. Governments are integrating advanced surveillance systems to enable real-time monitoring and rapid incident response. The expansion of smart traffic systems and intelligent transportation networks increases the need for high-resolution cameras, ANPR, and AI-enabled video analytics. Infrastructure projects such as metro rail, highways, smart buildings, and industrial corridors mandate surveillance for security, asset protection, and regulatory compliance. For example, Bengaluru (India) geo-tagged more than 535,000 CCTV cameras by April 2025 under public safety and smart policing programs, more than double since January 2024.

Restraint - Privacy Regulations and Compliance Costs

Stringent data privacy regulations, such as the GDPR and the evolving EU AI Act, act as a key restraint by limiting the use, retention, and third-party access to biometric data. Compliance mandates privacy-by-design adoption, increasing costs for encryption, anonymization, e.g., facial masking, and secure data storage. The risk of heavy fines and reputational damage discourages adoption in regulated sectors like healthcare and education. Extended compliance checks and legal due diligence lengthen sales cycles and slow deployment decisions.

Geopolitical Supply Chain Disruption and NDAA Restrictions

Geopolitical supply chain disruptions and NDAA restrictions are restraining the market by barring several Chinese manufacturers from federal and critical infrastructure procurement in North America. System integrators and contractors risk disqualification if non-compliant equipment is deployed, narrowing vendor options and increasing compliance burdens. Rising geopolitical tensions are accelerating supply chain diversification and onshoring, thereby elevating production costs and weakening price competitiveness. As a result, the market is split into NDAA-compliant and non-compliant channels, reducing overall efficiency and economies of scale.

Opportunity - Expansion of Video Surveillance as a Service (VSaaS)

The rapid shift toward VSaaS creates a strong growth opportunity in the under-penetrated SME and residential segments by reducing reliance on on-premises servers and NVRs through cloud-based video management and storage. VSaaS is growing faster than traditional hardware due to its scalability, enabling instant addition of cameras and storage without upfront infrastructure upgrades. Features such as remote monitoring via mobile devices and flexible subscription models enhance adoption, while hybrid cloud solutions combining local recording with cloud backup offer reliability and accessibility, positioning providers for significant market share gains.

Convergence of Video Surveillance with IoT, Access Control, and AI-Driven Smart Building Ecosystems

The convergence of video surveillance with IoT, access control, fire safety, and building management systems presents a strong growth opportunity. Integrated, AI-enabled platforms enable real-time threat detection, behavioral analytics, and automated responses, e.g., cameras triggered by access events, shifting surveillance from passive monitoring to intelligent security. This creates value-added “smart building” solutions for system integrators and meets rising demand from facility managers for unified, single-pane-of-glass platforms to manage security, occupancy, and energy efficiently.

Category-wise Analysis

Component Insights

Hardware dominates the global market, capturing more than 61% market share in 2026 with a value exceeding US$ 38.9 Bn, as organizations continue to prioritize physical security infrastructure, such as cameras, DVRs/NVRs, and sensors, to monitor and protect assets. The rising need for real-time monitoring, high-resolution imaging, and reliable storage drives sustained investment in hardware. It forms the backbone for integration with advanced analytics and IoT-enabled surveillance systems, making it indispensable for security operations.

Software is demonstrating the highest growth rate at a 12.4% CAGR, driven by the increasing need for intelligent analytics, real-time monitoring, and automated threat detection. Organizations are prioritizing advanced features, such as AI-based recognition, behavioral analysis, and cloud integration, to enhance security and operational efficiency. The shift toward scalable, remote-access solutions also drives software adoption, enabling flexible management across multiple locations. Integration with IoT devices and cybersecurity measures is boosting the demand for sophisticated surveillance software.

Technology Insights

IP holds over 56% market share in 2026, with a value exceeding US$35.7 Bn. It offers superior scalability, high image quality, and seamless integration compared to analog counterparts. The ability to transmit power and data over a single Ethernet cable (PoE) simplifies installation and reduces cabling complexity, while inherent encryption capabilities address modern cybersecurity needs. Its scalability also allows easy expansion across multiple sites, meeting the growing demand for efficient and intelligent security systems.

Hybrid is expected to grow at a significant rate, with a CAGR of 8.9% as they combine the benefits of both IP and analog technologies, allowing businesses and homeowners to upgrade their systems gradually without replacing existing infrastructure. They meet the need for cost-effective scalability by integrating advanced analytics and remote monitoring while using legacy cameras. This flexibility addresses the growing demand for high-quality surveillance in varied environments, from residential to commercial, where complete IP deployment is not immediately feasible.

Application Insights

Commercial commands the largest market share, over 30% in 2026, with a value exceeding US$ 19.1 Bn, driven by the growing need to monitor and secure retail stores, offices, and public buildings. Businesses increasingly rely on surveillance to prevent theft, ensure employee safety, and manage operations efficiently. The rise of smart retail, integration with access control systems, and demand for real-time analytics further drive adoption. Regulatory compliance in certain sectors compels commercial establishments to deploy advanced surveillance solutions.

Residential is expected to grow at a CAGR of 12.7%, due to increasing concerns over home security and theft prevention. The rising adoption of smart homes and IoT-enabled security systems enables homeowners to monitor their properties remotely in real time. The need for easy-to-install, affordable, and user-friendly cameras that provide alerts and video access on mobile devices is driving demand. Growing awareness of personal safety and neighborhood security initiatives further fuels residential adoption.

Regional Insights

North America Video Surveillance Market Trends

North America holds over 28% share in 2026, reaching US$ 17.8 Bn, supported by early adoption of AI analytics and cloud-based solutions. The United States leads the region, driven by robust spending in retail, critical infrastructure, and law enforcement. The National Defense Authorization Act (NDAA) restricts federal agencies and grant recipients from using telecommunications and video surveillance equipment from specific foreign manufacturers, reshaping the competitive landscape and prompting a replacement cycle in government sectors. The region's mature IT infrastructure, established systems integrator networks, and enterprise IT budgets facilitate the deployment of advanced cloud-native and AI-powered solutions. Growing focus on homeland security and counter-terrorism measures has further accelerated adoption.

Asia Pacific Video Surveillance Market Trends

Asia Pacific dominates the global market, accounting for more than 39% market share in 2026, with a value of US$ 24.8 Bn, and is expected to grow at the highest rate, driven by massive urbanization and state-led public safety initiatives. China dominates the regional and global landscape, accounting for a significant share of revenue through its nationwide Skynet and Sharp Eyes projects. India is emerging as a high-growth frontier, with its Smart Cities Mission deploying surveillance across 100 cities to manage traffic and crime. The ASEAN region is also modernizing infrastructure, leaping directly to IP and wireless technologies. The region benefits from a robust manufacturing ecosystem, resulting in lower hardware costs and faster deployment timelines than in the West.

Europe Video Surveillance Market Trends

Europe is expected to hold more than 20% share by 2033, driven by a technologically sophisticated market where growth is balanced by rigorous ethical and legal frameworks. Key markets such as Germany, the U.K., and France prioritize Privacy by Design, with GDPR heavily influencing product selection. Manufacturers must demonstrate robust cybersecurity and data-anonymization features to succeed in this region. There is strong demand for intelligent traffic systems and public transport surveillance to support sustainable urban mobility goals. The U.K. remains one of the most heavily surveilled nations globally, sustaining steady demand for hardware upgrades. The EU AI Act is expected to further regulate the use of biometric identification, pushing the market toward anonymized behavioral analytics rather than facial recognition.

Competitive Landscape

The video surveillance market is moderately fragmented, with a mix of global leaders and numerous regional and niche manufacturers. Leading players compete through product differentiation, focusing on AI-powered analytics, edge computing, and high-resolution imaging to enhance accuracy and functionality. Manufacturers also adopt cost-competitive pricing and localized manufacturing to address price-sensitive markets while maintaining margins. Strategic partnerships, acquisitions, and ecosystem integration with software and cloud providers are widely used to expand portfolios and strengthen market presence.

Key Industry Developments:

- In September 2025, Axis Communications launched AXIS Secure Entry for XProtect, an integrated solution combining access control and video surveillance within the XProtect Smart Client interface. The platform streamlines security operations by enabling real-time monitoring, door entry automation, and video review, and will be showcased at GSX 2025 in New Orleans.

- In March 2025, Johnson Controls announced major upgrades to its access control and video surveillance solutions, enhancing C•CURE IQ into a unified enterprise security platform for on-prem, hybrid, and cloud environments. The upgrades integrate advanced video management, AI-powered edge analytics, intelligent dashboards, and enhanced mapping to improve real-time security response, operational efficiency, and cost optimization.

Companies Covered in Video Surveillance Market

- Hangzhou Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Tiandy Technologies Co., Ltd.

- Zhejiang Uniview Technologies Co., Ltd.

- Motorola Solutions, Inc.

- Axis Communications AB

- Hanwha Vision Co., Ltd.

- Robert Bosch GmbH

- Honeywell International Inc.

- Infinova Corporation

- CP Plus

- TKH Group N.V.

- Others

Frequently Asked Questions

The global video surveillance market is projected to be valued at US$63.7 Bn in 2026.

The need for enhanced security and real-time monitoring to prevent crime, ensure public safety, and protect assets is a key driver of the market.

The market is expected to witness a CAGR of 8.5% from 2026 to 2033.

Rising adoption of AI-powered surveillance and video surveillance as a service is creating strong growth opportunities.

Hangzhou Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., Axis Communications AB, Zhejiang Uniview Technologies Co., Ltd. are among the leading key players.