- Medical Devices

- Digital Morphology Analyzers Market

Digital Morphology Analyzers Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Digital Morphology Analyzers Market by Product Type (Integrated Digital Morphology Analyzers, Standalone Digital Morphology Analyzers), Technology (Automated Digital Morphology Systems, Semi-Automated Digital Morphology Systems), Application (Hematology, Cytology, Clinical Diagnostics), End-use, and Regional Analysis for 2025 - 2032

Digital Morphology Analyzers Market Size and Trends Analysis

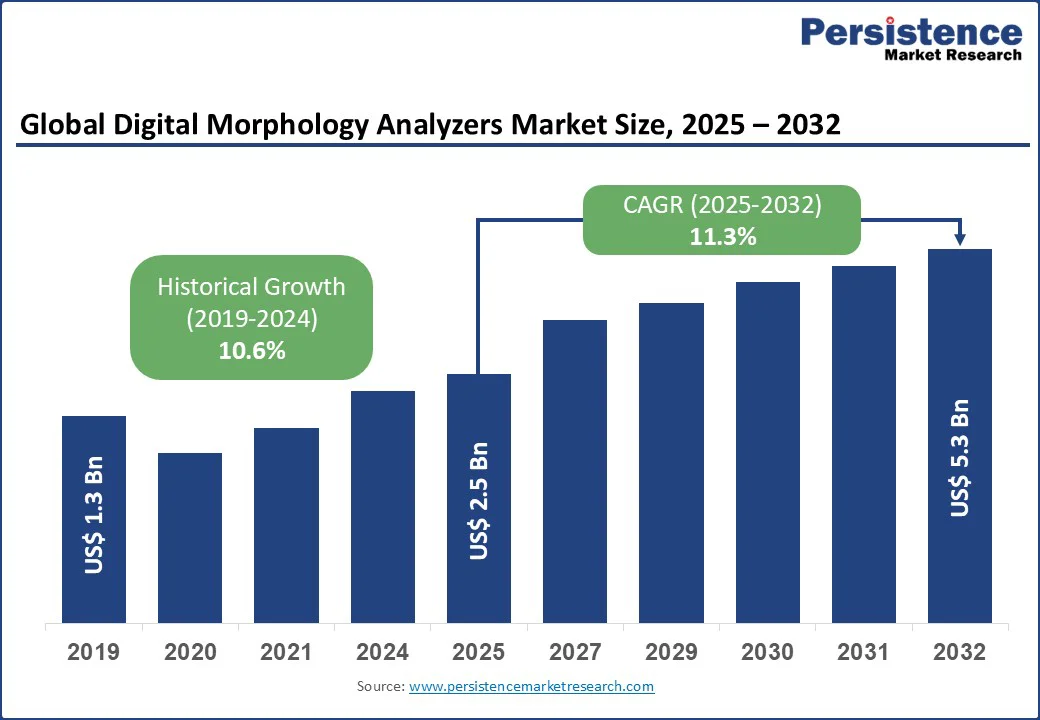

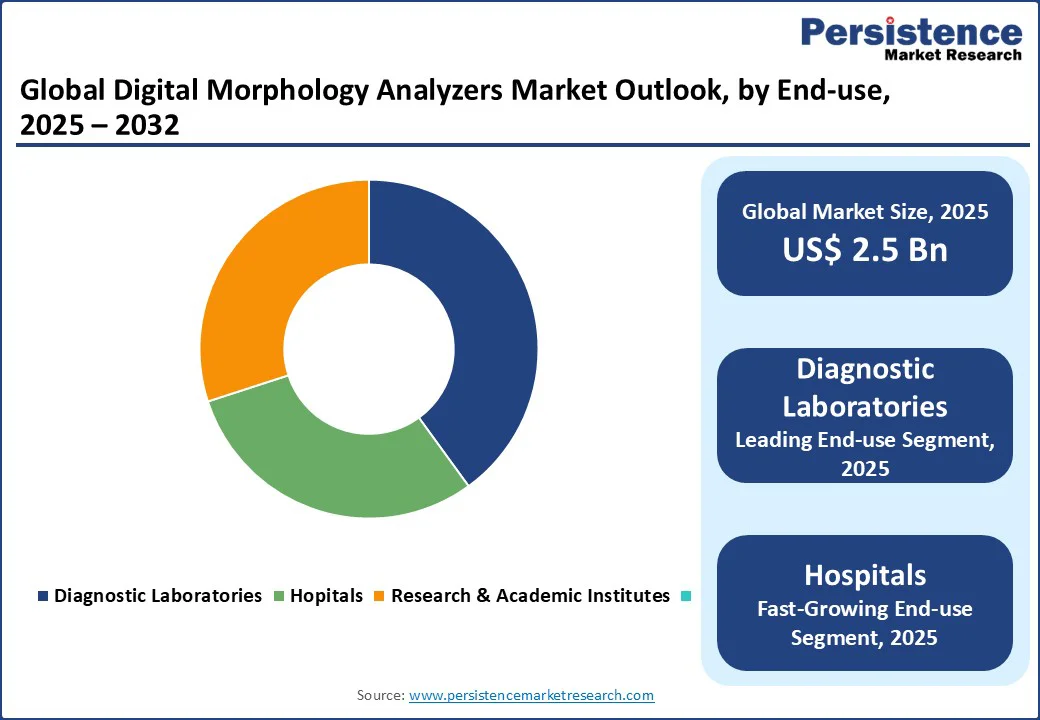

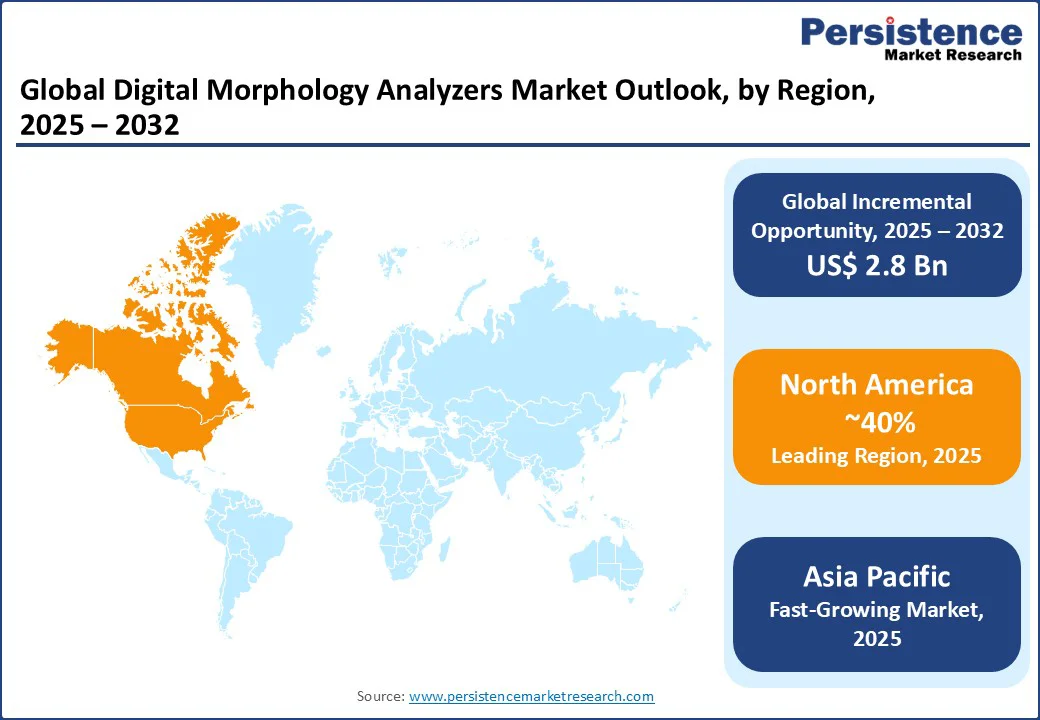

The global digital morphology analyzers market size is likely to be valued at US$2.5 Bn in 2025, with a forecast to grow to US$5.3 Bn by 2032, registering a CAGR of 11.3% during the forecast period 2025 - 2032.

The digital morphology analyzer industry is witnessing strong growth, driven by advancements in automation, artificial intelligence, and digital pathology. These systems are increasingly replacing traditional manual microscopy methods for blood cell analysis, offering higher accuracy, faster turnaround times, and improved workflow efficiency.

Key Industry Highlights

- Leading Product Type: Integrated Digital Morphology Analyzers hold a 55% market share in 2025, driven by clinical diagnostics technology.

- Leading Technology: Automated Digital Morphology Systems are fueled by digital morphology innovations.

- Dominates Applications: Hematology holds a 45% market share, supported by the demand for hematological diagnostics.

- Leading End-use: Diagnostic laboratories hold a 40% market share, driven by diagnostic laboratory equipment.

- Dominates Region: North America holds a 40% global market share, led by U.S. digital morphology trends.

- Fastest-growing Region: Asia Pacific is fueled by digital morphology growth in China and India.

|

Global Market Attribute |

Key Insights |

|

Digital Morphology Analyzers Market Size (2025E) |

US$2.5 Bn |

|

Market Value Forecast (2032F) |

US$5.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.6% |

The rising prevalence of hematological disorders such as anemia and leukemia is fueling demand for advanced diagnostic solutions across clinical laboratories, hospitals, and research institutes.

Market Dynamics

Driver: AI Integration, Rising Chronic Diseases, and Healthcare Digitalization

The digital morphology analyzers market is propelled by the integration of artificial intelligence (AI), the rising prevalence of chronic diseases, and healthcare digitalization. AI-powered digital pathology systems are revolutionizing hematological diagnostics and cytology analysis by enabling automated cell identification and classification, reducing human error, and accelerating diagnostic workflows.

This technological leap enhances clinical diagnostics technology, making automated hematology analyzers indispensable in high-throughput environments such as hospital diagnostics and diagnostic laboratories.

The rising burden of chronic conditions, such as blood disorders, cancers, and infectious diseases, fuels demand for digital morphology innovations to support accurate and timely diagnosis, particularly in hematological diagnostics for leukemia and anemia.

Healthcare digitalization, driven by the adoption of electronic health records and telemedicine, amplifies the need for medical imaging technology that integrates seamlessly with digital platforms, supporting digital morphology applications in research laboratories.

Restraint: High Costs, Skilled Workforce Shortage, and Regulatory Challenges

The digital morphology analyzers market faces challenges due to high equipment costs, a shortage of skilled professionals, and stringent regulatory frameworks. The advanced technology embedded in automated hematology analyzers, including AI and high-resolution imaging, results in expensive systems that are cost-prohibitive for smaller diagnostic laboratories and healthcare facilities in resource-constrained settings, limiting digital morphology applications.

The shortage of trained pathologists and laboratory technicians, particularly those proficient in operating digital pathology systems, hampers the efficient use of clinical diagnostics technology, as complex systems require specialized expertise for accurate hematological diagnostics and cytology analysis.

Regulatory complexities, such as compliance with stringent standards in regions such as North America and Europe, increase development and certification costs for digital morphology brands, slowing the rollout of digital morphology innovations.

Opportunity: Emerging Markets, AI Advancements, and Point-of-Care Testing

The digital morphology analyzers market offers significant opportunities through expansion in emerging markets, advancements in AI-driven digital morphology innovations, and growing demand for point-of-care testing. Emerging markets, with rapidly developing healthcare sectors, present significant potential for diagnostic laboratory equipment, as governments and private institutions invest in modernizing hospital diagnostics and research laboratories.

AI-driven advancements, such as deep learning algorithms for cytology analysis and hematological diagnostics, are enhancing diagnostic precision and speed, creating opportunities for digital pathology systems to gain traction in clinical diagnostics technology.

The growing demand for point-of-care testing, particularly in remote and underserved areas, drives the development of compact and portable automated hematology analyzers, aligning with digital morphology health benefits and digital morphology trends.

Strategic collaborations between digital morphology brands and healthcare providers, as well as partnerships with technology firms, facilitate the integration of medical imaging technology into broader healthcare ecosystems, enhancing digital morphology applications.

Category-wise Analysis

Product Type Insights

Integrated digital morphology analyzers hold a 55% market share in 2025, driven by their seamless integration with laboratory information systems, making them ideal for high-throughput hospital diagnostics and diagnostic laboratories. These systems streamline workflows by combining imaging, analysis, and data management, supporting clinical diagnostics technology and hematological diagnostics.

Standalone digital morphology analyzers are the fastest-growing, fueled by their flexibility and portability, which cater to smaller diagnostic laboratories and research laboratories seeking cost-effective digital pathology systems. These analyzers allow faster deployment and scalability, enabling labs to digitize workflows without complex integrations.

Technology Insights

Automated digital morphology systems hold a 60% market share in 2025, driven by their AI-driven capabilities, which enable rapid and accurate cell analysis for hematological diagnostics and cytology analysis, aligning with clinical diagnostics technology demands. Automation significantly reduces turnaround times for high-volume laboratories, making these systems indispensable for clinical diagnostics, oncology, and infectious disease management, where rapid decision-making is critical.

Semi-Automated digital morphology systems are the fastest-growing, fueled by advancements in medical imaging technology and increasing adoption in hospital diagnostics for automated workflows. Fully automated systems and semi-automated solutions offer flexibility for specialized testing and are well-suited for resource-constrained settings where full automation may be financially unfeasible.

Application Insights

Hematology holds a 45% market share in 2025, driven by its critical role in diagnosing blood-related disorders, such as leukemia and anemia, using automated hematology analyzers for precise hematological diagnostics. With growing awareness of early diagnosis for better patient outcomes, hematology remains a core application in both developed and emerging markets, supported by government initiatives and laboratory automation trends.

Cytology is the fastest-growing field, fueled by increasing demand for cytology analysis in cancer diagnostics, supported by digital pathology systems and medical imaging technology. Advancements in medical imaging technology and automated slide preparation systems further support growth.

End-use Insights

Diagnostic Laboratories hold a 40% market share in 2025, driven by their high-throughput testing capabilities and adoption of diagnostic laboratory equipment for hematological diagnostics and cytology analysis. With the growing demand for centralized testing and telepathology services, diagnostic laboratories continue to expand their infrastructure to support high-throughput operations.

Hospitals are the fastest-growing, fueled by the increasing integration of clinical diagnostics technology in hospital diagnostics for real-time patient care. Advanced features such as AI-assisted cell classification, automated imaging, and telepathology connectivity allow hospital pathologists to collaborate remotely with specialists, improving diagnostic accuracy for complex cases.

Regional Insights

North America Digital Morphology Analyzers Market Trends

North America holds a 40% global market share in 2025, led by the U.S., and dominates the Digital Morphology Analyzers Market due to its advanced healthcare infrastructure and strong focus on clinical diagnostics technology. The U.S. market thrives on widespread adoption of automated hematology analyzers in hospital diagnostics, driven by the need for rapid and accurate hematological diagnostics for chronic diseases such as cancer and blood disorders.

The region’s robust regulatory framework, supported by agencies such as the FDA, ensures high standards for digital pathology systems, boosting digital morphology innovations. Diagnostic laboratories leverage medical imaging technology to enhance diagnostic accuracy, while digital morphology e-commerce facilitates access to diagnostic laboratory equipment.

Europe Digital Morphology Analyzers Market Trends

Europe accounts for a 25% global market share in 2025, led by Germany, the UK, and France, driven by advanced healthcare systems and a focus on digital pathology systems. Germany’s market is growing due to its leadership in medical technology innovation, as diagnostic laboratories adopt automated hematology analyzers for hematological diagnostics and cytology analysis. The UK market benefits from a strong emphasis on cancer diagnostics, with clinical diagnostics technology supporting hospital diagnostics and research laboratories.

France’s market is driven by its focus on precision medicine, with digital morphology innovations enhancing cytology analysis in diagnostic laboratories. The rise of digital morphology e-commerce supports the distribution of diagnostic laboratory equipment, aligning with digital morphology trends and consumer preferences.

Asia Pacific Digital Morphology Analyzers Market Trends

Asia Pacific is the fastest-growing region, accounting for 20% global market share in 2025, led by China, Japan, and India, driven by rapid healthcare modernization and increasing demand for clinical diagnostics technology. China’s market is fueled by government investments in healthcare infrastructure, with hospital diagnostics adopting automated hematology analyzers for hematological diagnostics.

Japan’s market benefits from a strong medical device industry, with digital pathology systems enhancing cytology analysis in diagnostic laboratories. India’s market is growing due to rising healthcare access and urbanization, with increasing demand for digital morphology in hospital diagnostics and research laboratories. The growing prevalence of chronic diseases drives digital morphology growth, positioning the Asia Pacific as a hub for digital morphology brands and digital morphology trends.

Competitive Landscape

The global digital morphology analyzers market is competitive, with CellaVision AB, Siemens Healthineers, Sysmex Corporation, Mindray, Abbott Laboratories, Roche Diagnostics, Leica Biosystems, and Olympus Corporation focusing on digital morphology innovations and automated hematology analyzers.

CellaVision AB dominates the segment with its specialized digital morphology platforms. At the same time, Siemens Healthineers and Sysmex leverage their strong presence in laboratory automation to integrate digital morphology into broader diagnostic ecosystems. Companies leverage digital morphology trends and clinical diagnostics technology to gain market share.

Key Developments

- In 2024, CellaVision launched an advanced AI-powered platform for digital cell morphology, enabling improved classification accuracy and remote diagnostics.

- In 2022, Sysmex Corporation announced a collaboration with IBM Watson Health to integrate AI solutions into its diagnostic instruments to improve interpretation efficiency.

Companies Covered in Digital Morphology Analyzers Market

- CellaVision AB

- Siemens Healthineers

- Sysmex Corporation

- Mindray

- Abbott Laboratories

- Roche Diagnostics

- Leica Biosystems

- Olympus Corporation

- Others

Frequently Asked Questions

The digital morphology analyzers market is projected to reach US$ 2.5 Bn in 2025, driven by digital morphology analyzers market trends.

AI integration and rising chronic diseases fuel digital morphology demand in clinical diagnostics technology.

The digital morphology analyzers market grows at a CAGR of 11.3% from 2025 to 2032, reaching US$ 5.3 Bn by 2032.

Emerging markets and AI-driven digital morphology innovations drive digital morphology growth.

Key players include CellaVision AB, Siemens Healthineers, Sysmex Corporation, and Roche Diagnostics.