- Media & Entertainment

- Digital Music Market

Digital Music Market Size, Share, and Growth Forecast, 2026 - 2033

Digital Music Market by Service Type (Music Streaming, Live Streaming, Digital Radio, Digital Downloads), Revenue Model (Subscription, Ad-Supported, Transactional), End-User (Individual, Commercial), and Regional Analysis for 2026 - 2033

Digital Music Market Share and Trends Analysis

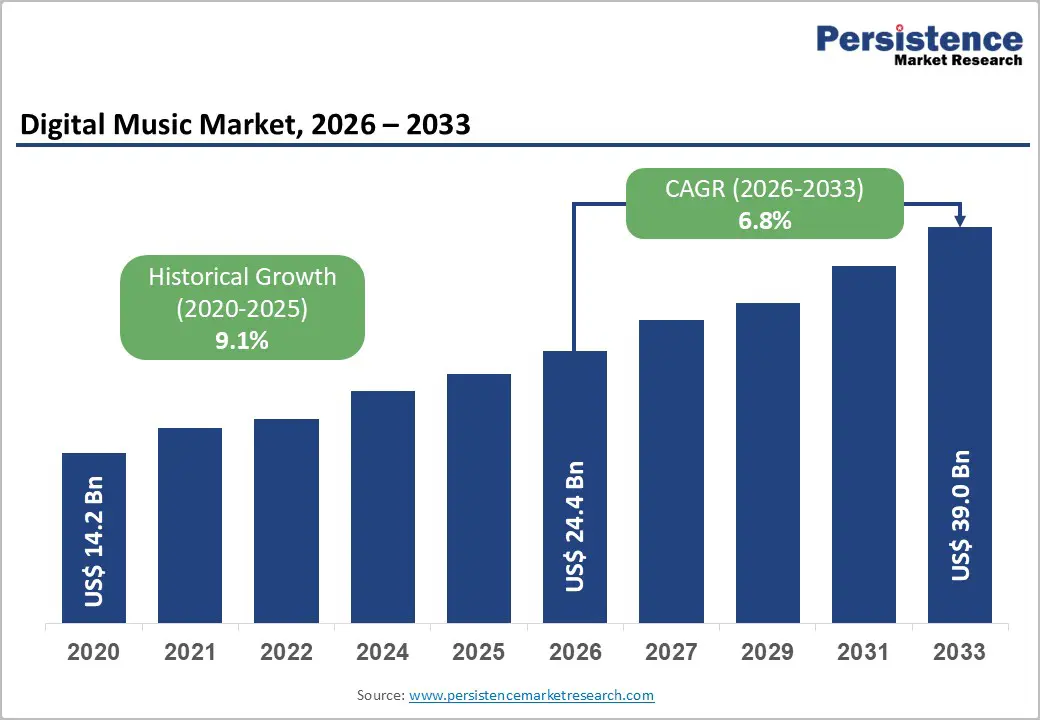

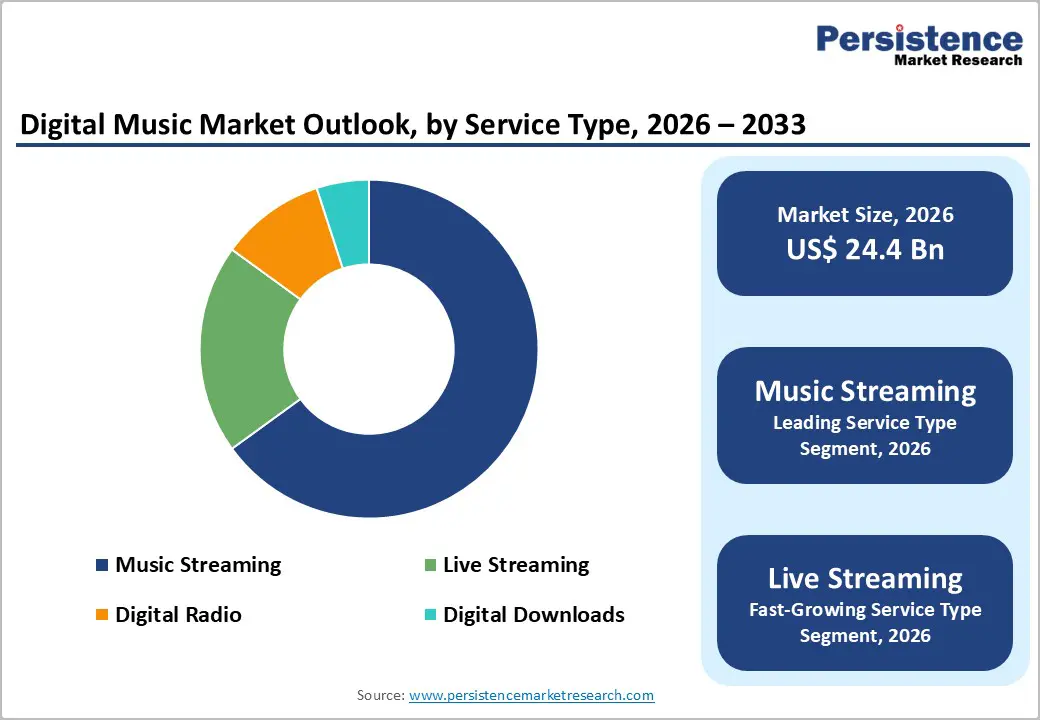

The global digital music market size is likely to be valued at US$ 24.4 billion in 2026, and is projected to reach US$ 39.0 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026 - 2033.

The market is supported by increased penetration of smartphones, broadband, and streaming platforms worldwide. Growth is increasingly driven by the shift from downloads and physical formats toward subscription and ad-supported streaming, integration of music into connected devices, and expanding monetization models, including premium tiers and bundled digital services. Over the forecast horizon, digital music will remain a critical pillar of the broader recorded music and digital media ecosystem, with platform innovation and regulatory developments shaping competitive outcomes and revenue trajectories.

Key Industry Highlights

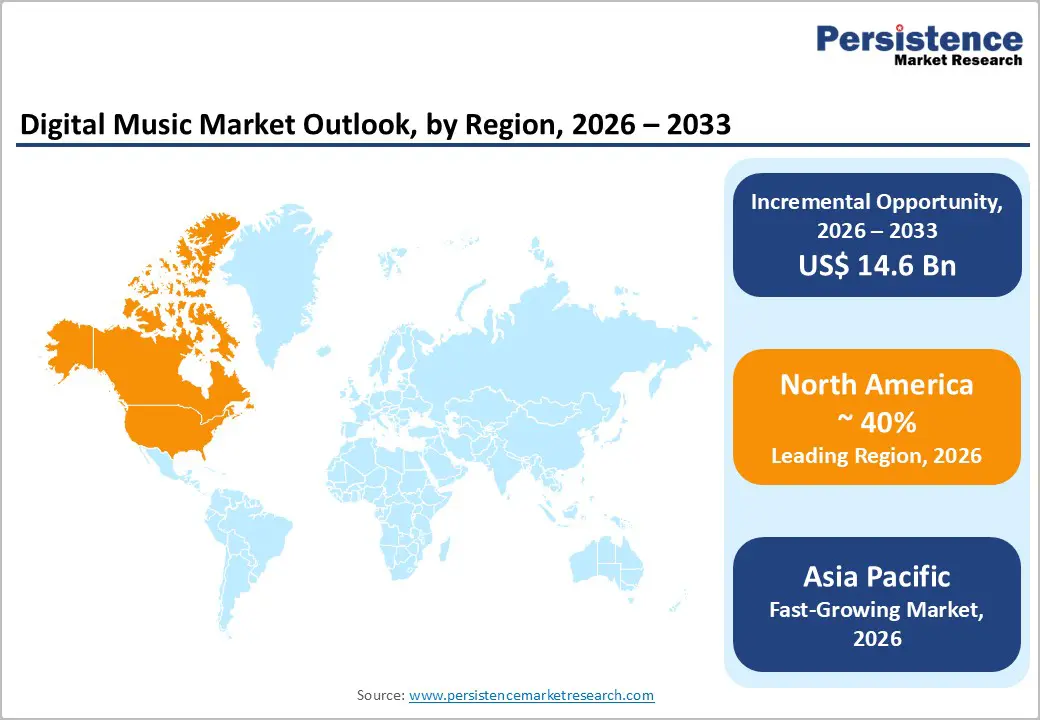

- Dominant Region: North America is expected to command about 40% market share in 2026, owing to high smartphone penetration and a well-developed digital payment infrastructure.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing through 2033 due to substantial improvements in telecommunications infrastructure.

- Leading & Fastest-growing Service Types: Music streaming is set to lead with approximately 65% revenue share in 2026, while live streaming is likely to grow the fastest during the 2026 - 2033 forecast period.

- Revenue Model Dominance: Subscription is anticipated to dominate with an estimated 70% revenue share in 2026, whereas ad-supported is poised to be the fastest-growing segment during the 2026 - 2033 forecast period.

- September 2025: India's Ministry of Information and Broadcasting (MIB) announced plans to launch a one-stop digital music licensing registry to streamline permissions and reduce compliance burdens for the live events and entertainment industry.

| Key Insights | Details |

|---|---|

| Digital Music Market Size (2026E) | US$ 24.4 Bn |

| Market Value Forecast (2033F) | US$ 39.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Integration of Artificial Intelligence and Personalization Technologies

The integration of artificial intelligence (AI) and personalization technologies is transforming how users discover and experience music on digital platforms. Advanced machine learning systems now interpret listening habits, contextual signals, and content characteristics to curate highly tailored playlists and recommendations. For example, in December 2025, Deezer introduced new personalization tools that enable users to customize the app's visual interface with color themes and creative icon layouts, along with a "Quick Access" feature that displays favorite artists, playlists, podcasts, and tracks at the top of the homepage based on listening habits. These capabilities deepen user engagement by surfacing relevant tracks and artists that align with individual tastes, moods, and activities, resulting in a more intuitive, seamless experience that feels increasingly responsive to personal preferences.

For streaming providers, sophisticated personalization has become a strategic differentiator that shapes competitive positioning and long-term growth prospects. Platforms that successfully embed AI-driven discovery tools often benefit from stronger loyalty, lower churn, and higher monetization per active user. Enhanced recommendation quality also supports artists and rights holders by improving the visibility of catalog and niche content, broadening the range of tracks that can gain traction. Over time, these technologies help build defensible competitive moats, as large platforms accumulate rich behavioral datasets and continuously refine their models. This dynamic supports market expansion by increasing customer lifetime value and encouraging sustained subscription and engagement.

Artist Compensation Concerns and Licensing Complexity

The digital music ecosystem faces persistent challenges related to equitable artist compensation and the complexity of multi-territory licensing. A sizeable section of artists, particularly independents, argues that current streaming payout structures make it difficult to generate sustainable income, even with sizable audiences. These concerns have fueled growing pressure from artist associations, advocacy groups, and policymakers, who question how streaming revenue is allocated among platforms, labels, and rights holders. As a result, streaming economics have been formally reviewed in several major markets, where inquiries have examined whether current models fairly reflect the value that artists create and whether greater transparency or regulatory intervention is warranted.

Securing multi-territory licensing remains a structurally complex and resource-intensive process for digital music platforms. Operators must negotiate with multiple performing rights organizations, mechanical rights societies, and record labels, each with distinct legal, commercial, and territorial requirements. This fragmentation increases operational overhead, extends time-to-market, and raises barriers to entry for smaller or new services that cannot easily absorb these costs. For established platforms, these challenges compress profitability margins and expose them to regulatory and contractual disputes. As a result, artist compensation concerns and licensing complexity create ongoing uncertainty for investors and strongly influence strategic decisions around expansion, pricing, and long-term platform sustainability.

Podcast and Audio Content Diversification

Digital music platforms are increasingly expanding beyond traditional music streaming into podcasts, audiobooks, and other forms of spoken-word and exclusive audio content. This diversification broadens their value proposition by appealing to a wider range of user interests and listening occasions, spanning entertainment, education, news, and wellness. Long-form audio formats encourage deeper engagement, as listeners often spend extended periods with individual episodes or series and gradually build habits around particular shows and hosts. As platforms assemble a richer mix of content types, they become more embedded in users’ daily routines, reinforcing loyalty and reducing the likelihood that listeners will switch to competing services.

A broader audio portfolio also opens new monetization pathways and strengthens competitive positioning. Exclusive podcast deals, original series, and curated audiobook selections can support differentiated premium tiers and attract advertisers seeking highly engaged, targeted audiences. These assets can be bundled with existing music offerings to create higher-value subscription packages and cross-promotional opportunities for both artists and spoken-word creators. In August 2025, for instance, PodUp raised US$ 5.8 million, offering 50+ integrated tools including 17 AI-powered features designed to help creators produce, grow, and monetize podcasts while reducing the need for multiple standalone technologies. Strong presence in podcasting and other spoken-word formats positions platforms to capture a larger share of the wider digital audio economy, supporting revenue diversification, reducing reliance on music licensing alone, and enhancing overall platform resilience.

Category-wise Analysis

Service Type Insights

Music streaming is forecast to be the leading segment with an approximate 65% of the digital music market revenue share in 2026. This segment is led by subscription-based platforms such as Spotify, Apple Music, and Amazon Music, which provide on-demand access to extensive catalogs of recorded music. Its leadership is driven by a combination of seamless user experience, broad device integration, and the convenience of unlimited access models that have reshaped how listeners consume music. Major platforms offer vast libraries supported by advanced recommendation systems that simplify discovery, deepen engagement, and encourage users to concentrate most of their listening within a single ecosystem.

Live streaming is likely to be the fastest-growing segment during the 2026 - 2033 forecast period, having expanded rapidly after the pandemic. This medium of music continues to gain traction through hybrid event formats that blend digital and in-person experiences in a single, coherent offering. In this model, artists and platforms employ immersive technologies, exclusive virtual performances, and interactive fan features to deepen engagement and unlock incremental revenue streams beyond traditional recorded music consumption and touring. For example, in August 2025, TikTok broke its previous livestream audience record by broadcasting the 2025 Tomorrowland electronic music festival to more than 74 million viewers across both weekends. The milestone reinforces TikTok's positioning as a critical hub for music engagement and demonstrates the growing momentum of its livestream commerce strategy.

Revenue Model Insights

Subscription models are slated to be dominant with an estimated 70% of the market revenue share in 2026. The leadership reflects strong consumer preference for unlimited access at predictable monthly price points. These plans, commonly structured around individual, family, and student tiers, give listeners frictionless access to large catalogs while simplifying budgeting. For platforms, subscriptions generate recurring, more stable revenue streams, support higher customer lifetime value, and typically offer more attractive margin profiles than advertising-only models. A recent industry study found that Americans aged 13 and older have been spending 66% of their daily streaming music listening time with paid platforms and only 34% with free services as of 2025, reflecting growing intolerance for advertisements, competitive pricing among providers such as Spotify and Amazon Music, and bundling with other media services despite recent price increases across digital service providers (DSPs).

Ad-supported is anticipated to be the fastest-growing segment over the 2026-2033 forecast period, driven by efforts to reach users in price-sensitive markets where premium subscription uptake remains constrained. These free tiers act as acquisition funnels, allowing listeners to experience full platform functionality in exchange for exposure to audio and display advertising, and then gradually nudging engaged users toward paid offerings over time. In July 2025, for instance, SiriusXM launched SiriusXM Play, its first low-cost ad-supported streaming music tier priced at US$ 7 monthly, offering access to over 130 channels including music, sports, news, talk, and comedy programming. Growth of this segment is further underpinned by advances in digital advertising technology, greater adoption of programmatic audio formats, and increasingly granular audience targeting, which together improve advertiser returns while enabling platforms to monetize non-paying users and build engagement and brand loyalty.

End-User Insights

Individual users are likely to dominate with a projected 80% of the market revenue share in 2026. This segment encompasses a broad demographic range, from teenagers to older adults who listen to digital music for entertainment, relaxation, workouts, and daily commutes. It is primarily monetized through individual subscription plans, with pricing tiers differentiated by factors such as audio quality, offline download options, and the presence or absence of advertising. Purchasing power varies significantly by geography, prompting platforms to adopt localized pricing strategies in emerging markets while maintaining higher standard price points in developed economies to reflect income levels and competitive dynamics.

Commercial users are expected to exhibit the highest CAGR from 2026 to 2033. The growth is underpinned by enterprises that use streaming services to enhance customer environments in retail stores, restaurants, hotels, and fitness centers. These users typically operate under specialized commercial licensing agreements that differ from consumer subscriptions and are tailored to public performance requirements. Rising awareness of music’s role in shaping customer experience and dwell time, the expansion of service-sector economies in emerging markets, and the development of dedicated business offerings with curated playlists, compliance tools, and usage reporting designed to meet specific operational and legal needs.

Regional Insights

North America Digital Music Market Trends

North America is set to command a significant portion of the digital music market share at approximately 40% in 2026. The region benefits from high smartphone penetration, a well-developed digital payment infrastructure, and mature adoption of streaming services across age groups. Consumers show a strong willingness to pay for premium experiences, and many households maintain multiple subscriptions across music, video, and gaming platforms, reinforcing cross-ecosystem engagement. Canada reflects many of these trends, with slightly lower penetration but comparable preferences for subscription streaming and bundled digital services.

Regional market growth is driven by several structural factors that extend beyond core music streaming. Platforms are integrating podcasts and other spoken-word content, enhancing their value propositions and increasing time spent per user. Premium tiers featuring high-fidelity, and spatial audio are gaining traction among enthusiasts, supporting higher effective price points. The deeper integration of streaming apps into connected vehicles, smart speakers, and other connected devices is embedding digital music more firmly into everyday routines. Against this backdrop, regulatory debates on copyright and creator remuneration continue, while competition remains concentrated among a few major platforms, creating opportunities for niche services, audiophile-oriented offerings, and specialized B2B commercial licensing solutions.

Europe Digital Music Market Trends

Europe represents one of the most important regional markets for digital music, with Germany and the United Kingdom acting as primary revenue hubs and France and Spain emerging as key growth markets. Germany benefits from strong streaming adoption and a well-established copyright and collecting-society framework, while the U.K. stands out for high per-capita streaming usage and advanced digital service penetration. France and Spain are experiencing faster growth, supported by local language content strategies and telecom bundles that integrate music subscriptions into mobile and broadband offerings, easing affordability constraints and encouraging mass-market uptake.

Regional momentum is reinforced by the efforts of the European Union (EU) to harmonize regulation and licensing, which gradually simplify multi-territory operations and reduce administrative friction for platforms. Rising smartphone adoption in Central and Eastern Europe, together with tailored local repertoire and language-specific playlists, is bringing new audiences into the streaming ecosystem and boosting engagement. At the same time, implementation of the EU Copyright Directive is reshaping platform responsibilities around licensing, artist remuneration, and content moderation, adding both compliance costs and greater legal clarity. Competition features a mix of global leaders and regional players such as Deezer, while investment focuses on localized podcasts, non-English content, and partnerships with telecom operators, alongside opportunities to raise subscription penetration and convert free-tier users to paid plans.

Asia Pacific Digital Music Market Trends

The Asia Pacific digital music market is anticipated to emerge as the fastest-growing through 2033, accounting for an estimated 25% share in 2026. China, India, and Japan serve as the primary revenue centers. China stands out for its vast user base and the dominance of local platforms such as Tencent Music and NetEase Cloud Music, which shape distinct platform structures and monetization models. India offers exceptional growth potential, supported by rapid streaming adoption, rising smartphone usage, and affordable data access, while Japan continues to perform strongly despite greater market maturity, reflecting a hybrid consumption pattern that combines streaming with ongoing physical music purchases.

Supporting regional market growth is the expansion of middle-class populations with rising discretionary income, substantial improvements in telecommunications infrastructure, and increasingly aggressive localization strategies by leading platforms. Regulatory environments vary widely, ranging from China’s stringent content controls and licensing requirements to more open or evolving digital frameworks in India and Southeast Asia, creating a highly heterogeneous operating landscape. Competitive intensity remains high between global players and regional champions, underpinned by ongoing investments in local content production, partnerships with telecom operators for bundled offerings, and low-cost subscription tiers designed to address price-sensitive user segments.

Competitive Landscape

The global digital music market has been maintaining a moderately consolidated structure, with leading providers such as Spotify Technology S.A., Apple Inc., Amazon.com, Inc., Tencent Music Entertainment Group, and Deezer S.A. commanding 60-65% of total market share. These organizations have been operating within a fiercely competitive landscape where numerous platforms vie aggressively for listener loyalty and recurring subscription income. Providers have been distinguishing their offerings through relentless enhancements to user interfaces, featuring advanced personalization algorithms, expertly curated playlists, exclusive artist content, and superior audio fidelity to foster deeper connections and minimize subscriber attrition. Organizations that master these elements will have secured sustainable advantages as consumer expectations continue to evolve toward seamless, intuitive experiences.

Regional and local services have been intensifying rivalry by targeting specific geographic areas or language communities with customized music libraries and culturally attuned functionalities that resonate with unique listening preferences. This layered competition has been compelling global incumbents to adapt swiftly while creating opportunities for nimble operators to capture niche segments. Market leaders who integrate localized strategies with technological superiority will have strengthened their positions against emerging challengers. For stakeholders navigating this dynamic, prioritizing hybrid models that blend universal appeal with regional relevance remains essential to achieving long-term revenue stability and growth acceleration.

Key Industry Developments

- In November 2025, Warner Music Group reached a licensing agreement with AI music startup Suno, settling its prior copyright infringement lawsuit and paving the way for Suno to launch new licensed AI music models next year.

- In March 2025, Concord acquired Stem Distribution, an independent artist-focused platform offering digital distribution, data insights, playlisting, and label services, which will continue to operate as a separate division within Concord Label Group under its existing leadership.

- In February 2025, Spotify launched its “Mi Primer Escenario” music contest in Argentina, giving emerging local artists the chance to win a debut performance slot at the Quilmes Rock festival and the cover of a major Spotify playlist.

Companies Covered in Digital Music Market

- Spotify Technology S.A.

- Apple Inc.

- Amazon.com, Inc.

- Tencent Music Entertainment Group

- Alphabet Inc.

- NetEase Cloud Music

- Deezer S.A.

- SoundCloud Global Limited & Co. KG

- Sirius XM Holdings Inc.

- JioSaavn

- Anghami Inc.

- Tidal

- Napster

Frequently Asked Questions

The global digital music market is projected to reach US$ 24.4 billion in 2026.

The market is primarily driven by widespread streaming adoption enabled by smartphones, high-speed internet, subscription models, and the convenience of on-demand access to vast music libraries.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Leveraging AI-driven personalization and data analytics, and integrating podcasts and immersive audio can open up new market opportunities.

Spotify Technology S.A., Apple Inc., Amazon.com, Inc., Tencent Music Entertainment Group, and Deezer S.A. are some of the key players in the market.