- Hardware & Software IT Services

- Edge Data Center Market

Edge Data Center Market Size, Share, and Growth Forecast, 2026 - 2033

Edge Data Center Market by Component (Hardware, Software, Services), Application (IT & Telecom, BFSI, Healthcare, Manufacturing, Retail), Deployment Type (On-Premises, Colocation Edge, Cloud-Integrated Edge), and Regional Analysis for 2026 - 2033

Edge Data Center Market Share and Trends Analysis

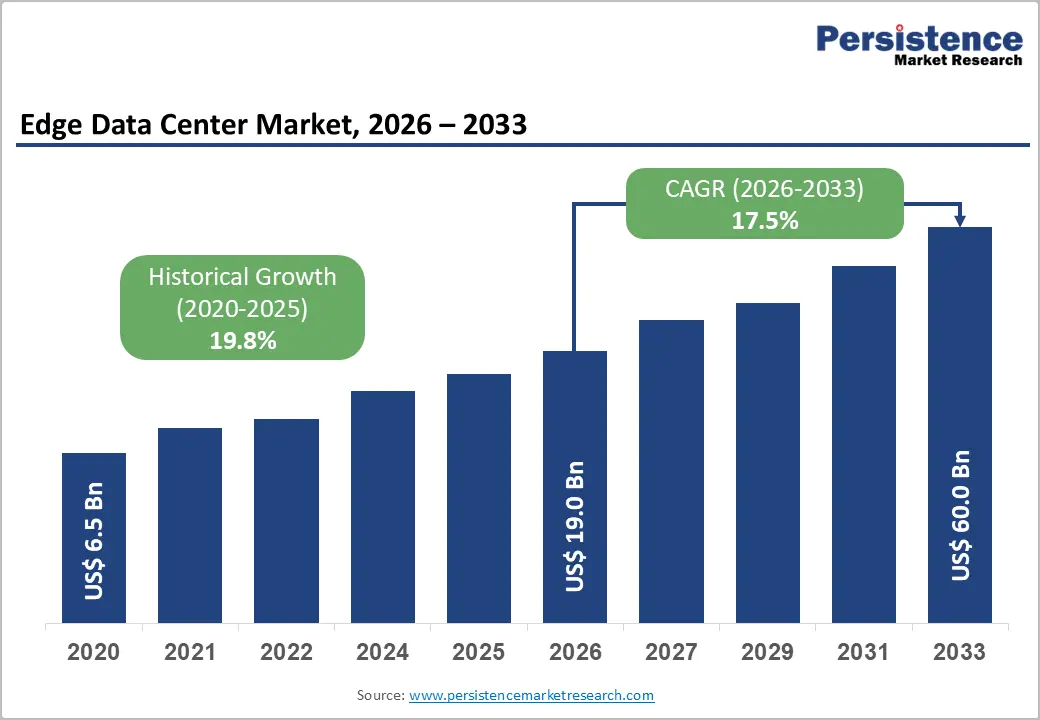

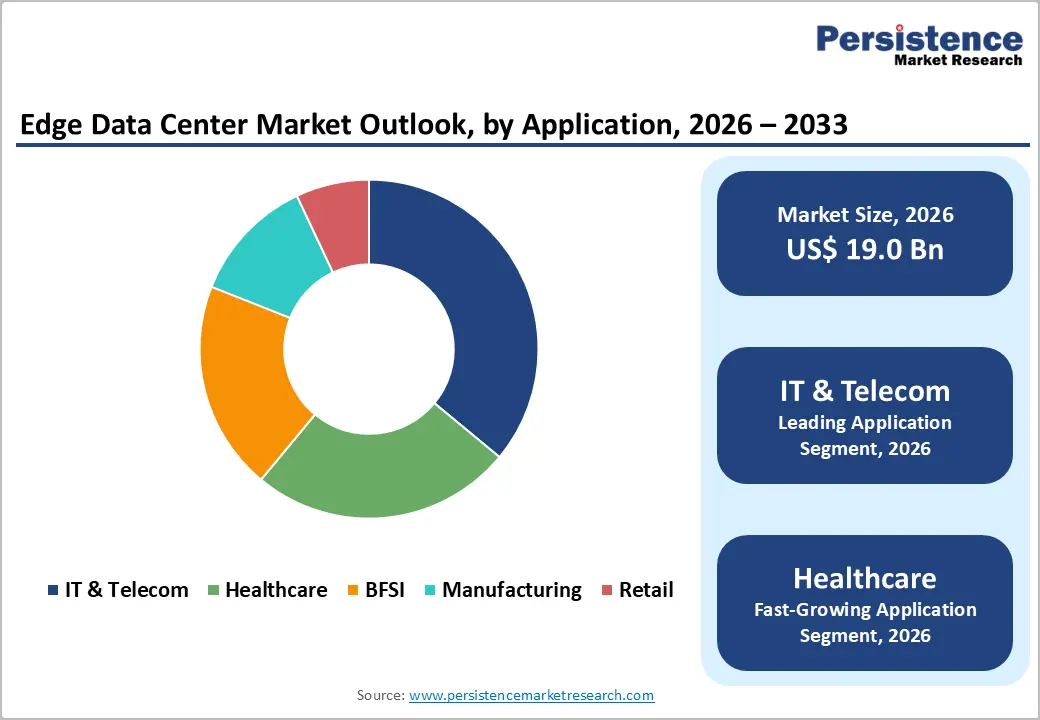

The global edge data center market size is likely to be valued at US$ 19.0 billion in 2026, and is projected to reach US$ 60.0 billion by 2033, growing at a CAGR of 17.5% during the forecast period 2026 - 2033.

This robust expansion is driven by the exponential growth of devices powered by the Internet of Things (IoT) technology requiring low-latency data processing, the proliferation of 5G network infrastructure demanding distributed computing capabilities, and increasing adoption of artificial intelligence (AI) and machine learning (ML) applications at network edges. The market demonstrated strong growth, reflecting a fundamental shift toward decentralized computing architectures driven by bandwidth constraints and real-time processing requirements across industries.

Key Industry Highlights

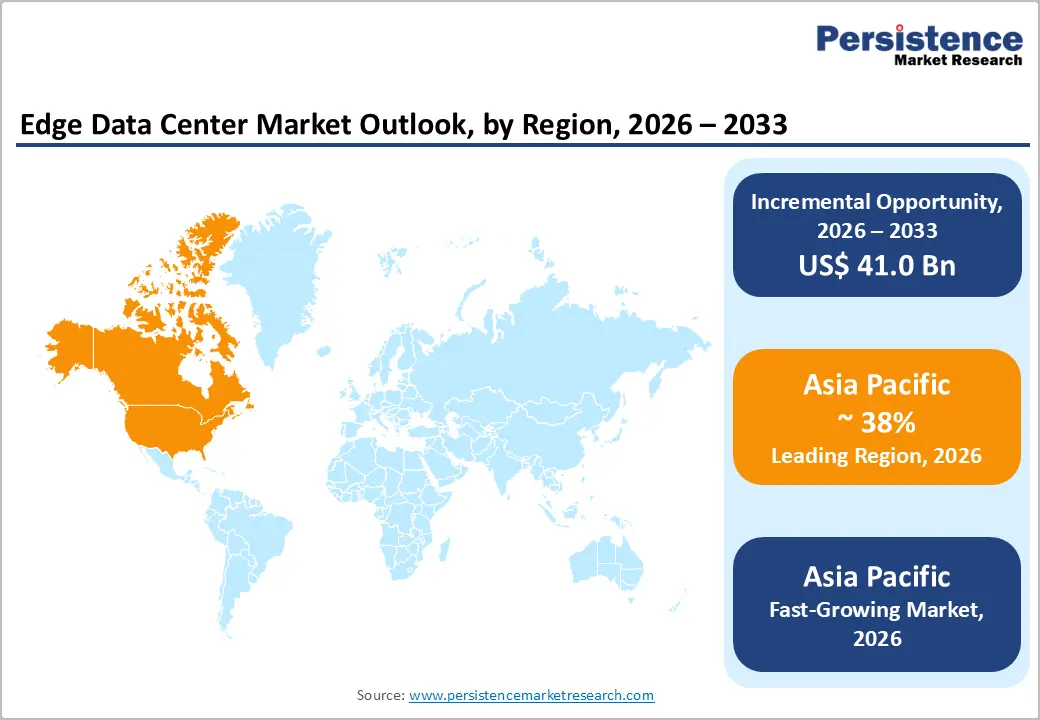

- Dominant Region: North America is expected to command about 38% market share in 2026, supported by the concentration of hyperscale cloud providers and advanced telecommunications infrastructure.

- Fastest-growing Market: The Asia Pacific market is set to post the highest CAGR through 2033, underpinned by large-scale digital infrastructure programs.

- Leading & Fastest-growing Component: Hardware is slated to dominate at an estimated 63% in 2026, where software is likely to be the fastest-growing segment over the 2026 - 2033 forecast period.

- Application Dominance: IT & telecom is expected to dominate with an estimated 36% revenue share in 2026, while healthcare is anticipated to grow the fastest during the 2026 - 2033 forecast period.

- January 2026: SoftBank acquired DigitalBridge for US$ 4 billion to deepen its position in AI infrastructure across data centers, towers, fiber, and edge facilities.

| Key Insights | Details |

|---|---|

| Edge Data Center Market Size (2026E) | US$ 19.0 Bn |

| Market Value Forecast (2033F) | US$ 60.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 17.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 19.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion of 5G Networks and IoT Devices

The rapid rollout of fifth-generation mobile networks (5G) is reshaping how organizations design and locate their computing resources. As operators activate more 5G sites, they increasingly move processing power closer to subscribers to meet strict latency, reliability, and throughput requirements. Instead of relying solely on distant, centralized data centers, telecommunications providers now deploy compute and storage in compact, distributed facilities near radio access infrastructure. This model supports critical workloads, such as augmented reality applications, real-time video analytics, and high-frequency trading tools, so they can respond in near real time. The implication of these developments is that network investments deliver their full value only when supported by a deliberate edge computing strategy that aligns capacity, siting decisions, and priority use cases.

The expansion of the IoT is reshaping data traffic patterns at the edge of the network. Connected devices in factories, vehicles, buildings, and public infrastructure continually generate operational information that can lose relevance if it must wait for centralized processing. Edge data centers enable organizations to analyze and act on this information on-site or nearby, reducing backhaul requirements and improving resilience when connectivity to core facilities is limited. This model supports advanced use cases such as autonomous vehicles, smart manufacturing, and responsive energy grids, where split-second decisions influence safety, efficiency, and customer experience. From a strategic perspective, decision-makers should view edge infrastructure as a core element of digital transformation roadmaps rather than a secondary technology layer.

Technical Complexity and Skilled Workforce Shortage

Managing distributed edge computing environments creates a fundamentally different operating model compared to traditional centralized data centers. Microsoft’s Azure edge infrastructure suffered a major incident where software defects caused multiple edge sites in Europe and Africa to crash, and remaining edge locations became overloaded, leading to significant latency and timeouts for users until traffic was rebalanced and routes were re-announced via BGP. This situation requires robust remote monitoring, standardized deployment templates, and clear runbooks so engineers can diagnose and resolve issues without being on-site. Organizations that manage edge operations using the same assumptions as a large, single-campus facility often face avoidable complexity, including inconsistent configurations and fragmented support processes.

The skills required to operate this type of environment differ significantly from those in conventional data center roles. Engineers need to understand areas such as distributed networking, site-to-site orchestration, edge security, and application architectures that remain reliable under constrained conditions. Because these capabilities are still developing in many regions, organizations gain value from structured training programs, well-defined career paths, and targeted partnerships with service providers that have practical edge operating experience. Management should also determine which responsibilities to retain in-house and which to outsource, such as remote hands support, around-the-clock monitoring, or security operations, to prevent internal teams from becoming overextended.

Large-Scale Digital Infrastructure Development in Emerging Economies

Developing economies across the Asia Pacific, Latin America, and Africa offer significant expansion potential as governments place digital infrastructure at the core of their economic transformation plans. Policy makers increasingly regard broadband networks, data centers, and cloud platforms as essential enablers of productivity, financial inclusion, and modern public services rather than discretionary technology upgrades. In markets such as India, Indonesia, Brazil, and Nigeria, the rising use of smartphones and digital services is reshaping how citizens access commerce, media, education, and government portals, creating clear incentives to position computing resources closer to end users.

Edge data centers in tier-2 and tier-3 cities in these regions can play a pivotal role by placing compute and storage closer to emerging demand hubs while easing pressure on congested national backbone networks. When operators position these facilities near growing populations and commercial centers, they can improve application performance, reduce network bottlenecks, and create more resilient digital infrastructure for local ecosystems. Well-located edge sites can also underpin government digitalization priorities, such as digital identity systems, cloud-based public services, and electronic governance platforms, while simultaneously hosting private-sector workloads in industries such as banking, retail, logistics, and media.

Category-wise Analysis

Component Insights

Hardware is slated to maintain a dominant position in 2026, with an estimated 63% of the edge data center market revenue share. This segment encompasses various physical components essential for the functioning of edge data centers, such as servers, storage devices, and networking equipment. The demand for robust and reliable hardware solutions is driven by the need to support high-performance computing at the edge. Innovations in hardware technology, such as energy-efficient servers and advanced cooling systems, are also contributing to the market's growth. Companies are investing heavily in hardware to ensure that their edge data centers can handle increasing data volumes and complex processing tasks efficiently.

Software is likely to be the fastest-growing segment over the 2026 - 2033 forecast period. The software segment plays a central role in enabling efficient and scalable edge data center operations. It comprises management and orchestration platforms, analytics engines, and security solutions that are specifically designed to improve visibility, control, and protection across distributed edge sites. As edge environments become more complex, organizations increasingly depend on advanced software capabilities to coordinate resources, enforce policies, and maintain consistent performance across diverse locations. These software platforms support real-time monitoring, automated lifecycle management, and predictive maintenance, which helps keep edge infrastructure operating at optimal efficiency while minimizing downtime.

Application Insights

IT & telecom is poised to hold the highest revenue share, estimated to reach 36% in 2026. This dominance reflects the fundamental role telecommunications providers and technology companies play in deploying edge infrastructure as foundational elements of 5G network architectures and cloud service delivery platforms. Major telecommunications carriers, including Verizon, AT&T, Deutsche Telekom, and China Mobile, are investing billions in mobile edge computing (MEC) capabilities integrated directly into their network infrastructure, positioning compute resources at cell tower sites and central offices to minimize latency for 5G applications. The segment benefits from substantial capital availability, technical expertise, and clear return-on-investment models tied directly to service quality improvements and operational cost reductions through distributed processing architectures.

Healthcare is anticipated to be the fastest-growing segment between 2026 and 2033. The exceptional growth trajectory of this segment is driven by the digital transformation of healthcare delivery, including telemedicine platforms, remote patient monitoring systems, AI-powered diagnostics, and connected medical devices generating massive volumes of time-sensitive data requiring immediate processing and analysis. Edge data centers enable healthcare providers to process patient data locally, ensuring compliance with stringent regulations, including the Health Insurance Portability and Accountability Act (HIPAA) in the United States, General Data Protection Regulation (GDPR) in Europe, and equivalent frameworks globally that mandate strict data privacy protections and residency requirements.

Deployment Type Insights

The on-premises segment is likely to capture approximately 60% of the edge data center market share in 2026, predominantly among large enterprises with substantial existing data center investments and specific data sovereignty requirements. Organizations in regulated industries, including financial services, healthcare, and government sectors, prefer on-premises edge solutions that maintain direct operational control and ensure compliance with data residency regulations. However, this segment faces growth constraints related to capital intensity and operational complexity, resulting in below-market growth rates as organizations increasingly explore alternative deployment models.

Colocation edge is expected to be the fastest-growing segment from 2026 to 2033. This deployment model allows organizations to adopt edge computing capabilities without making large upfront capital investments by using shared infrastructure operated by specialist providers. Colocation operators are extending their edge footprints into tier-2 and tier-3 cities, giving enterprises access to distributed computing capacity previously concentrated in major metropolitan hubs. The combination of flexible, usage-based commercial terms and professionally managed facilities helps organizations address constraints such as limited in-house expertise and shortages of skilled technical staff.

Regional Insights

North America Edge Data Center Market Trends

North America is set to command a significant portion of the edge data center market share at approximately 38% in 2026. The leadership is driven by the concentration of hyperscale cloud providers, advanced telecommunications infrastructure, and early enterprise adoption of edge computing strategies across industries. Providers are now accelerating build-out in secondary and tertiary cities to place infrastructure closer to regional user bases, which improves performance for distributed applications and helps enterprises support branch, campus, and local ecosystem needs without building their own facilities. For decision-makers, this pattern suggests that competitive differentiation increasingly depends on how well their organizations leverage regional edge footprints rather than on centralized data center capacity alone.

Massive investments in 5G mobile networks by carriers such as Verizon, AT&T, and T-Mobile are creating new opportunities for colocation and multi-access edge deployments, particularly at locations where radio access, fiber connectivity, and cloud on-ramps converge. Policy initiatives that support rural broadband expansion are also driving additional edge infrastructure requirements beyond traditional urban corridors, encouraging more distributed deployment patterns and new partnership models among operators, local utilities, and regional governments. Evolving data protection laws at the country level, including privacy frameworks inspired by the Central Consumer Protection Authority (CCPA), are further strengthening the business case for localized data processing and storage so that organizations can remain compliant while sustaining user trust.

Europe Edge Data Center Market Trends

Europe is forecasted to be the second-largest regional market for edge data centers and is entering a more mature, regulation-driven growth phase. Germany, the United Kingdom, France, and Spain anchor regional demand, with Germany’s industrial base using edge infrastructure to support Industry 4.0 initiatives and the United Kingdom depending on low-latency platforms for trading, risk analytics, and real-time financial applications. Across these markets, enterprises increasingly deploy edge resources to balance strict compliance obligations with performance requirements, particularly in sectors such as manufacturing, financial services, automotive, and public services.

Regulation is the defining structural force in Europe’s edge data center market and shapes both the level of demand and how infrastructure is designed and deployed. The GDPR and emerging measures such as the proposed Data Act push organizations toward localized processing of personal and industrial data, which increases the need for distributed, in-region computing nodes that can support compliant IoT and connected product deployments. Telecommunications providers such as Deutsche Telekom, Vodafone, and Orange are integrating edge computing with 5G networks to enable applications such as autonomous vehicles, smart factories, and smart cities, while infrastructure investors support pan-European platforms that can scale across borders despite permitting challenges and differing national rules.

Asia Pacific Edge Data Center Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing edge data center market through 2033, underpinned by large-scale digital infrastructure programs, rapid urbanization, and deep integration of advanced technologies into industrial and consumer ecosystems. Countries such as China, India, and Japan are at the forefront of next-generation network deployment, industrial automation, and smart city implementation, which creates a particularly favorable environment for edge data center growth. Large-scale initiatives in areas such as intelligent transport systems, urban surveillance, digital public services, and real-time environmental monitoring all require low-latency processing close to end users and devices, prompting governments and enterprises to prioritize localized computing capacity.

Regulatory conditions differ widely across Asia Pacific, which has a direct impact on how and where organizations deploy edge data centers. China enforces stringent data sovereignty rules through instruments such as the Cybersecurity Law and the Data Security Law, which require sensitive data to remain within national borders and often to be processed locally. In contrast, Singapore and several ASEAN members operate more open regimes that encourage cross-border data flows and regional cloud and edge architectures. This diversity adds compliance and design complexity, but it also pushes enterprises and service providers to establish edge footprints across multiple countries to meet local regulatory requirements while maintaining performance.

Competitive Landscape

The global edge data center market is moderately fragmented, dominated by leading players such as Equinix, Inc., Digital Realty Trust, Inc., Verizon Communications Inc., and AT&T Inc., which collectively capture 45-50% of market share. The edge data center management market is highly competitive, with numerous established and emerging providers actively seeking to expand their share. The overall landscape is defined by rapid technological progress, a steady flow of strategic alliances, and ongoing merger and acquisition activity that reshapes capabilities and reach.

Leading vendors need to focus on continuous innovation, refining their platforms to deliver more automated operations, stronger security, and better integration with hybrid and multi-cloud environments. They also need to prioritize the allocation of substantial resources to research and development activities with an aim to address the diverse requirements of sectors such as telecommunications, financial services, manufacturing, retail, and healthcare.

Key Industry Developments

- In January 2026, Duos Edge AI is deployed a modular edge data center in Abilene, Texas, at the Region 14 Education Service Center to provide carrier-neutral colocation and AI-ready compute for K-12 schools, healthcare, workforce development, and local businesses across an 11-county, 13,000-square-mile area.

- In January 2026, Fringe Infrastructure, a Nigerian edge data center startup, launched its first multi-megawatt metro-edge facility in Ikoyi, Lagos, to provide colocation, interconnection, AI inference, and sovereign computing services to enterprises and governments across West Africa.

- In September 2025, German construction firm Hochtief developed a 2MW Yexio-branded edge data center in Herne’s Funkenberg Quartier, built with a timber frame, direct water cooling, a green façade, and a connection to the local district heating network, with potential expansion to 4MW.

Companies Covered in Edge Data Center Market

- Equinix, Inc.

- Digital Realty Trust, Inc.

- Verizon Communications Inc.

- AT&T Inc.

- EdgeConnex

- Schneider Electric SE

- Vapor IO

- Vertiv Group Corp.

- Huawei Technologies Co., Ltd.

- Cyxtera Technologies, Inc.

- EdgeMicro

- CyrusOne Inc.

- Compass Datacenters

- NTT Communications Corporation

- China Telecom Corporation Limited

Frequently Asked Questions

The global edge data center market is projected to reach US$ 19.0 billion in 2026.

The market is driven by the soaring demand for ultra‑low‑latency, real‑time processing of data generated by 5G, IoT, and AI applications that must be handled closer to end users and devices.

The market is poised to witness a CAGR of 17.5% from 2026 to 2033.

Enabling low-latency, real-time processing for 5G, IoT, and AI workloads via distributed edge data centers that bring compute and storage closer to end users and devices is creating highly lucrative opportunities in the market.

Equinix, Inc., Digital Realty Trust, Inc., Verizon Communications Inc., and AT&T Inc. are some of the key players in the market.