- Advanced Materials

- Carbon Textile Reinforced Concrete Market

Carbon Textile Reinforced Concrete Market Size, Share, and Growth Forecast 2026 - 2033

Carbon Textile Reinforced Concrete Market by Concrete Type (Regular-Tow, Large-Tow), Application (Infrastructure Development, Residential Building, Commercial Building, Industrial Projects, Bridge Construction, Repair), Fiber Orientation, Technology, Industry, and Regional Analysis for 2026 - 2033

Carbon Textile Reinforced Concrete Market Size and Trend Analysis

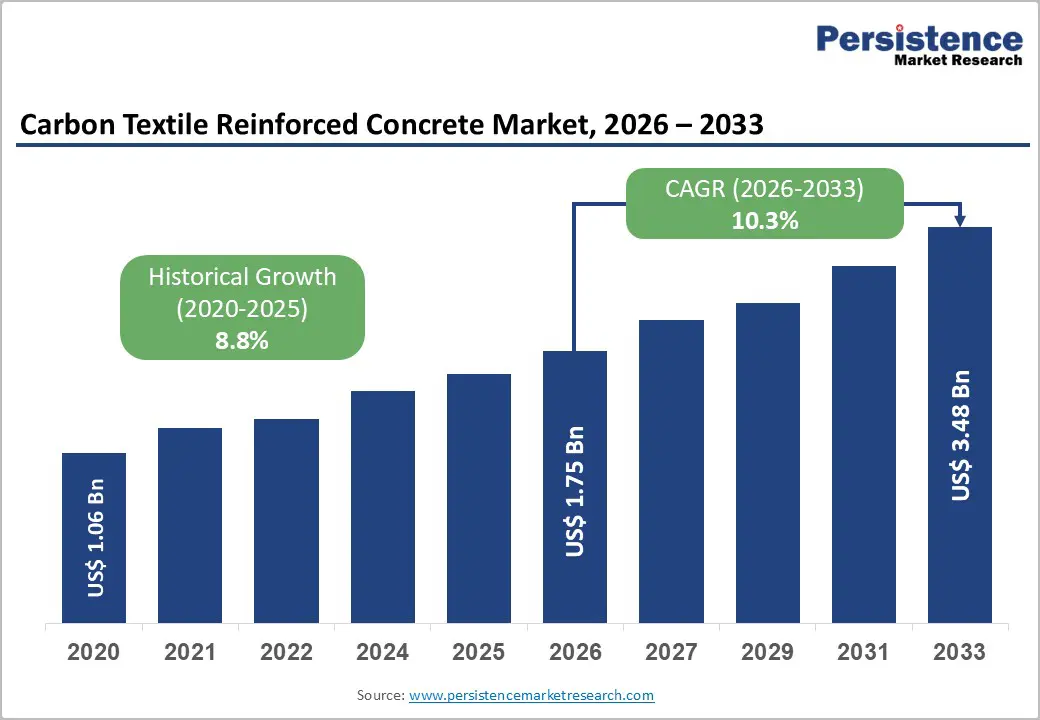

The global carbon textile reinforced concrete market size is likely to be valued at US$ 1.8 billion in 2026 and is projected to reach US$ 3.5 billion by 2033, growing at a CAGR of 10.3% between 2026 and 2033.

This remarkable expansion is primarily driven by increasing infrastructure modernization initiatives and the urgent need to address aging concrete structures globally. Carbon textile-reinforced concrete offers superior corrosion resistance compared with traditional steel reinforcement, with tensile strength exceeding 3500 MPa and an elastic modulus up to 230 GPa, enabling thinner structural designs that reduce material consumption by approximately 50% and CO2 emissions by up to 70%.

Key Industry Highlights:

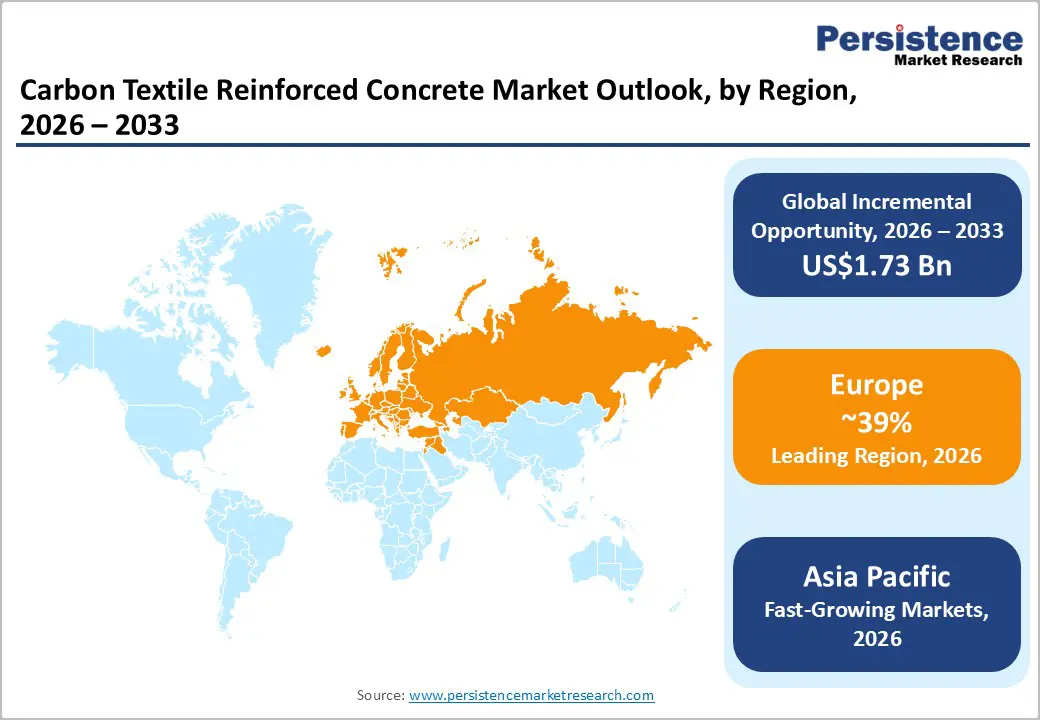

- Leading Region: Europe dominates the carbon-textile-reinforced concrete market, with a 39% market share, driven by Germany's pioneering research infrastructure, progressive regulatory frameworks, and successful demonstration projects such as the Technical University of Dresden's CUBE building, which establishes commercial viability pathways.

- Fastest Growing Region: Asia-Pacific represents the fastest-growing regional market, propelled by rapid urbanization across China, India, and ASEAN nations, massive infrastructure investment programs, government smart city initiatives, and manufacturing cost advantages supporting both consumption growth and emerging production capabilities.

- Dominant Segment: Large-tow carbon fiber concrete type commands approximately 58% market share, reflecting favorable production economics, adequate performance characteristics for mainstream structural applications, and ongoing technological improvements narrowing historical performance gaps with regular-tow alternatives across infrastructure and building construction segments.

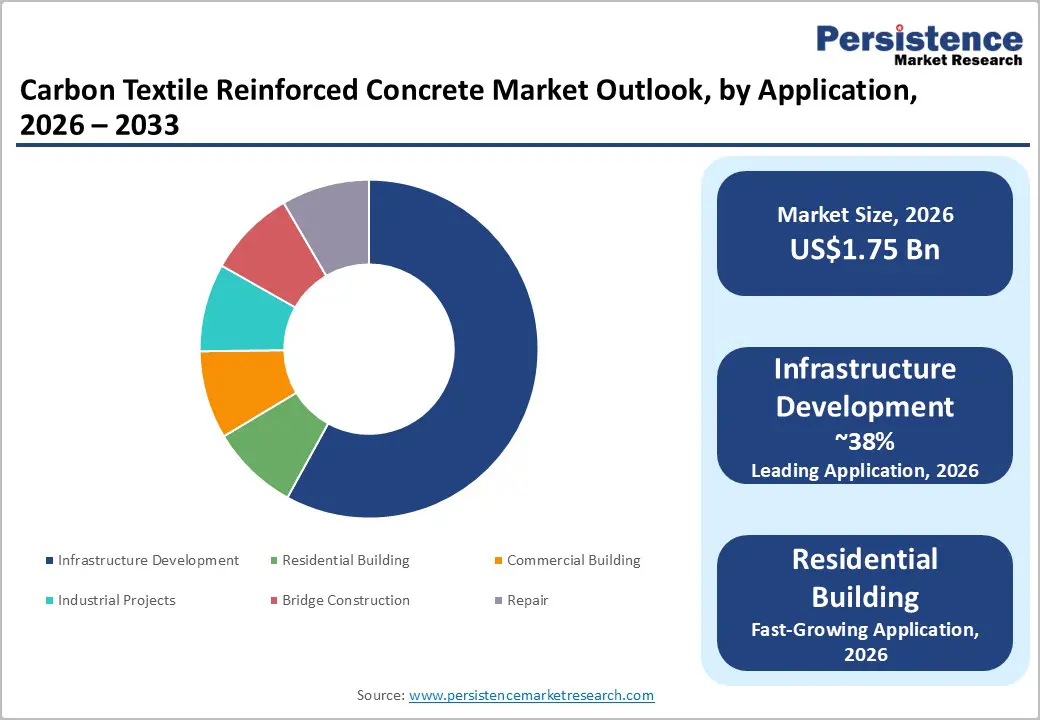

- Fastest Growing Segment: Infrastructure development application segment exhibits the strongest growth trajectory, driven by aging asset rehabilitation requirements, government embodied carbon reduction mandates, transportation authority specifications emphasizing 100-year design life objectives, and carbon textile reinforcement's superior corrosion resistance and lifecycle cost advantages.

- Key Opportunity: Green building certification requirements and embodied carbon reduction mandates create substantial expansion potential, with major contractors like Turner Construction Company committing to 50% lower-emission concrete demonstration projects by 2026 and government agencies establishing measurable emissions reduction targets for public infrastructure programs.

| Key Insights | Details |

|---|---|

| Carbon Textile Reinforced Concrete Market Size (2026E) | US$ 1.8 Bn |

| Market Value Forecast (2033F) | US$ 3.5 Bn |

| Projected Growth CAGR (2026 - 2033) | 10.3% |

| Historical Market Growth (2020 - 2025) | 8.8% |

Market Dynamics

Drivers - Growing Infrastructure Rehabilitation and Seismic Resilience Requirements

The growing urgency of global infrastructure rehabilitation and the superior corrosion resistance of carbon-textile-reinforced concrete are significantly influencing modern construction material choices. In the U.S., about 40% of the nation’s 614,387 bridges are at least 50 years old, and nearly 10% operate under load restrictions, requiring an estimated US$123 billion in rehabilitation. Traditional steel-reinforced concrete deteriorates rapidly in coastal and de-icing salt-exposed environments, resulting in high maintenance costs.

Carbon textile reinforcement eliminates such vulnerabilities because carbon fibers do not corrode when exposed to moisture, chlorides, or aggressive chemicals. Research indicates strength improvements of 51% to 100% and tensile capacities above 3,000 N/mm², enabling thinner concrete sections with substantially reduced material use. Carbon-concrete methods further reduce resource consumption by 85% and CO2 emissions by 52%, thereby reinforcing their technical and environmental advantages.

Green Building Certifications and Sustainable Construction Mandates Driving Material Innovation

The global construction industry’s shift toward sustainability, reinforced by green building certifications and regulatory mandates, is significantly increasing demand for carbon-textile-reinforced concrete. LEED v5, introduced by the U.S. Green Building Council in early 2025, emphasizes embodied carbon reduction through new assessment prerequisites and targeted credits, encouraging the use of low-impact materials.

Similarly, the World Bank Group’s EDGE certification requires at least a 20% reduction in embodied carbon, water, and energy consumption; a benchmark carbon-textile concrete readily meets this benchmark through lower material intensity. In Europe, Germany’s DIBt approvals for solidian GRID reinforcement have enabled broad adoption in both in-situ and precast construction. Demonstration projects such as Technical University Dresden’s €5 million CUBE building, which achieved substantial material and CO2 reductions, further validate the technology’s potential.

Restraints - High Initial Material Costs and Limited Production Scale Economics

The high initial cost of carbon fiber materials compared to conventional steel reinforcement remains a major obstacle to wider market adoption, particularly in cost-sensitive construction sectors and developing regions. Carbon fiber manufacturing requires energy-intensive processes, including precursor production, stabilization, carbonization at temperatures above 1,000°C, and specialized surface treatments, resulting in material prices that are five to ten times higher than those of steel on a weight basis.

Although the superior strength-to-weight ratio of carbon textiles enables thinner concrete sections and reduced material consumption, the substantial upfront investment poses challenges for project budgets and demands rigorous lifecycle cost evaluations. Furthermore, global production capacity is concentrated among a small group of specialized manufacturers, thereby limiting economies of scale. Infrastructure projects that prioritize the lowest initial bids rather than long-term performance further disadvantage carbon textile solutions despite their proven durability.

Technical Expertise Requirements and Standardization Gaps in Implementation

The implementation of carbon-textile-reinforced concrete requires specialized technical knowledge, installation skills, and design expertise that are not yet widely available across the global construction sector, thereby limiting broader market adoption. Unlike traditional steel reinforcement, which benefits from decades of standardized design and installation practices, carbon textile systems demand an understanding of fiber orientation, textile architecture, resin compatibility, and anchoring techniques to ensure reliable structural performance. The absence of unified international standards contributes to regulatory uncertainty, as approval processes differ across jurisdictions and often require project-specific engineering assessments, increasing timelines and costs.

Furthermore, limited training programs for architects, engineers, and construction personnel, especially outside early-adopter regions, create skill gaps. Installation also requires careful handling, surface preparation, and specific quality-control procedures, underscoring the need for expanded contractor training and certification initiatives.

Opportunity - Rapid Infrastructure Expansion in Asia-Pacific Emerging Economies

Rapid infrastructure development across emerging Asia-Pacific economies, particularly in India, Southeast Asia, and China’s secondary cities, creates strong growth potential for carbon textile reinforced concrete, as these regions prioritize durable, low-maintenance construction materials. India’s market is expected to expand steadily, supported by extensive modernization initiatives, including metro systems, highway corridors, and smart city projects. The region is also projected to add more than 70 billion square meters of real estate in the next two decades, reflecting its substantial share of global construction activity.

Rising sustainability commitments driven by high regional carbon emissions further strengthen the case for carbon textile solutions. Japan’s development of CO2-SUICOM technology, China’s focus on high-performance materials, and ASEAN’s rapid urbanization in corrosive tropical environments highlight strong regional suitability. Strategic partnerships, demonstration projects, and localized production can secure early-mover advantages through 2033.

Advanced Manufacturing Integration and Multidirectional Fiber Applications

The integration of carbon-textile-reinforced concrete with advanced manufacturing technologies, such as 3D concrete printing, digital fabrication workflows, and optimized fiber orientation, enables new possibilities for complex architectural forms and scalable customization. Research from the Technical University of Dresden demonstrates that carbon textiles enable thin-walled elements as slim as 80 mm for pedestrian bridge decks, as applied in Hering Architectural Concrete’s Rems Valley projects.

Such capabilities align well with parametric design and robotic fabrication, positioning carbon-textile concrete as a preferred material for digitally engineered, prefabricated components. Developments in multidirectional and hybrid textile architectures enhance performance under varied stress conditions, while processes such as VARTM and prepreg layup improve fiber consistency and reduce installation time. Regulatory approvals for multi-layer solidian GRID systems further support advanced applications, strengthening the material’s role in high-performance construction.

Category-wise Analysis

Concrete Type Insights

The Large-Tow carbon textile segment holds a dominant share of approximately 56% in the concrete-type category, driven by superior cost-efficiency and manufacturing scalability suited to large infrastructure projects. Large-tow fibers, containing more than 48,000 filaments per bundle, enable faster production and lower unit costs while providing sufficient tensile strength for most structural reinforcement needs. This makes them highly suitable for bridges, highways, and foundation systems where cost control is prioritized over maximum performance.

Automated production facilities, such as those operated by Solidian GmbH, further enhance commercial viability. Established supply chains from the automotive and industrial sectors also support broader adoption. However, regular-tow textiles remain important in applications requiring higher strength-to-weight ratios, such as architectural façades, seismic strengthening, and heritage restoration, and remain relevant in specialized, performance-driven niches.

Application Insights

The Infrastructure Development segment holds a leading market share of 58%, owing to the growing demand for durable, low-maintenance materials for bridges, tunnels, highways, and transit systems exposed to harsh environmental conditions. Carbon-textile-reinforced concrete is particularly valuable because its corrosion resistance helps reduce escalating maintenance costs associated with traditional steel reinforcement. The American Society of Civil Engineers’ estimate of US$123 billion required for U.S. bridge rehabilitation underscores the scale of the opportunity.

Carbon textiles also enable thin, lightweight overlays for strengthening existing structures, as demonstrated by the Bridge Street Bridge project in Michigan, the first U.S. vehicular concrete bridge to use carbon fiber composite cable prestressing. Regulatory approvals in Europe and expanding government investment in long-life, low-carbon infrastructure further reinforce adoption, positioning this segment as a sustained market leader through 2033.

Fiber Orientation Insights

The bidirectional fiber orientation segment holds a 42% market share due to its strong suitability for structural elements subjected to multi-axial stress conditions, where reinforcement is required in perpendicular directions. Manufactured as woven or stitched grids with fibers arranged at 0 ° and 90 °, bidirectional textiles provide versatile reinforcement for floor slabs, wall panels, shell structures, and precast elements. Their design flexibility, handling robustness, and reduced alignment-critical installation errors make them preferable to unidirectional systems in many applications.

The bidirectional fibers also enhance crack distribution and integrate well with conventional concrete placement methods. Demonstrations such as Hering Architectural Concrete’s pedestrian bridge slabs highlight the balanced performance of the material. While unidirectional textiles remain essential for principal load-path applications, and multidirectional systems serve complex geometries, bidirectional configurations offer an optimal balance of performance and manufacturing efficiency for mainstream construction.

Technology Insights

Hand lay-up technology accounts for approximately 38% of the market due to its accessibility for on-site repair applications, retrofit projects, and customized architectural work in which standardized prefabrication is impractical. It enables contractors to apply carbon textile reinforcements directly to existing structural surfaces or within formwork, providing flexibility for irregular geometries, varying field conditions, and design modifications during construction sequencing. This approach is particularly effective for aging infrastructure, where access limitations, diverse substrate conditions, and the need to preserve architectural features require adaptable, site-specific methods.

ACI CODE 562 offers standardized guidance for externally bonded fiber-reinforced polymer systems, supporting design and regulatory compliance. Although more labor-intensive than automated techniques, hand lay-up remains cost-effective for smaller projects and pilot installations, thereby advancing market adoption through practical demonstration applications.

Industry Insights

The construction end-use industry accounts for 68% of the market, reflecting the strong alignment of carbon-textile-reinforced concrete with large-scale civil engineering applications. This leadership is driven by the sector’s vast concrete consumption and growing recognition of carbon textiles’ advantages, including corrosion immunity, reduced structural thickness, and extended service life. The segment encompasses residential, commercial, industrial, and infrastructure projects in which enhanced durability and compliance with sustainability standards are increasingly essential.

Major suppliers such as Sika AG and BASF SE continue to expand material capabilities through advanced admixtures and reinforcement systems. Although smaller in share, emerging applications across the aerospace, automotive, marine, energy, and defense sectors present high-growth opportunities due to needs for weight reduction, corrosion resistance, and impact performance. These expanding use cases demonstrate the material’s versatility and support broader market adoption by 2033.

Regional Insights

North America Carbon Textile Reinforced Concrete Market Trends

North America holds a significant market share, with the United States driving adoption through substantial infrastructure rehabilitation investments and advanced regulatory frameworks that encourage the use of innovative construction materials. The region’s aging infrastructure, with four in ten of the nation’s 614,387 bridges at least 50 years old, creates strong demand for durable reinforcement solutions that extend service life without costly reconstruction.

Federal programs such as the Low-Carbon Transportation Materials (LCTM) initiative and the Reduced Carbon Concrete Consortium (RC3) have mobilized more than 35 states to pursue over US$1.2 billion in funding for low-carbon material integration, accelerating the deployment of carbon-textile concrete. State Departments of Transportation have also begun approving carbon fiber reinforced polymer systems for bridge strengthening, supported by AASHTO testing. Demonstration projects in Michigan and Georgia further highlight expanding applications across commercial and institutional sectors.

Europe Carbon Textile Reinforced Concrete Market Trends

Europe leads the market with a 39% market share, driven by Germany’s technological leadership, comprehensive regulatory approvals, and significant research investments, positioning the region as an innovation hub for carbon-textile-reinforced concrete. The German Institute for Building Technology’s approvals for solidian GRID reinforcement, granted in 2024 and supplemented in 2025, removed project-specific authorization requirements and accelerated adoption in both in-situ and precast construction.

Demonstration projects, such as the €5 million CUBE building at the Technical University of Dresden, showcase the architectural potential of carbon concrete while achieving substantial reductions in material use and CO2 emissions. Companies like Solidian GmbH and Hering Architectural Concrete continue to expand applications through high-volume production and advanced bridge projects. Broader European adoption is supported by EU climate targets and efforts to harmonize technical standards, enabling streamlined certification and cross-border implementation.

Asia Pacific Carbon Textile Reinforced Concrete Market Trends

Asia Pacific demonstrates strong growth momentum, driven by China’s extensive infrastructure modernization, India’s rapid urbanization, and Japan’s leadership in advanced construction technologies. China’s significant share of global real estate activity and its focus on improving infrastructure durability create substantial demand for high-performance, corrosion-resistant materials, such as carbon-textile-reinforced concrete. Expanding high-speed rail, metro systems, and highway networks in secondary and inland cities further support adoption.

Japan’s development of CO2-SUICOM carbon-removing concrete and its emphasis on sustainability and seismic resilience highlight regional technological advancement. India and ASEAN nations continue to accelerate demand through large-scale infrastructure programs and smart city initiatives. With competitive manufacturing costs, strong textile capabilities, and expanding carbon fiber production, the Asia Pacific is emerging as both a major consumption market and an increasingly important production hub for carbon textile reinforcement materials.

Competitive Landscape

The carbon textile reinforced concrete market is moderately concentrated, with leading companies such as Solidian GmbH, BASF SE, and Sika AG maintaining strong positions through extensive product portfolios, advanced distribution networks, and collaborative research initiatives with academic institutions. These firms differentiate themselves through performance optimization, regulatory compliance, and the development of specialized solutions for high-value infrastructure and commercial construction applications. The competitive landscape is further shaped by increased investment in automated manufacturing systems aimed at enhancing scalability and lowering production costs, illustrated by Hitexbau’s high-volume carbon fiber textile grid production capabilities. Emerging business models now integrate technical services, workforce training, and lifecycle performance guarantees, while strategic alliances with precast manufacturers and contractors streamline market penetration and procurement processes.

Key Developments:

- January 2025: Solidian GmbH received supplementary regulatory approval (Z-71.3-45) from Germany's German Institute for Building Technology (DIBt), enabling efficient production of precast concrete elements with Solidian GRID carbon reinforcements without time-consuming individual approvals, significantly streamlining commercial adoption across European markets.

- March 2025: BASF and Sika jointly launched Baxxodur EC 151, a new amine building block for curing epoxy resins developed through research cooperation, with Sika successfully applying the hardener in Sikafloor® floor coatings, while BASF scaled manufacturing from laboratory to production.

- November 2025: Lipa Betoni (Finland) activated the world's first precast concrete production facility integrating Carbonaide's CO2 storage technology, embedding carbon capture directly into precast element manufacturing processes. The facility enhancement accelerates embodied carbon reduction for building systems across European markets, reinforcing precast concrete's competitive positioning against alternative construction materials.

Top Companies in Carbon Textile Reinforced Concrete Market

- Solidian GmbH (Albstadt, Germany) operates as a leading European manufacturer of non-corrosive carbon fiber reinforcement systems, achieving significant market position through early establishment of series production capabilities in 2015 and successful navigation of regulatory approval processes, including Z-1.6-308 and Z-71.3-45 certifications. The company fosters strong partnerships with Technical University Dresden and RWTH Aachen University, working on innovative projects like the CUBE carbon concrete building. They also offer a diverse product range, including grid reinforcements, bars, and customized textiles for various construction applications.

- BASF SE (Ludwigshafen, Germany) leverages its position as a global chemical industry leader to develop advanced materials and additives supporting carbon textile reinforced concrete applications, including the March 2025 launch of Baxxodur EC 151 epoxy hardener in collaboration with Sika AG. The company's research capabilities, global distribution, and strong manufacturer relationships give it a competitive edge in creating tailored formulations, providing technical support, and offering integrated solutions for concrete admixtures, surface treatments, and protection technologies, alongside carbon textile reinforcements.

- Sika AG (Baar, Switzerland) maintains a prominent market position through comprehensive product portfolios spanning concrete admixtures, fiber reinforcement systems, and structural strengthening technologies with an established presence across global construction markets. The company's involvement in sustainability research like the URBAN project, which focuses on concrete recycling, along with products such as Sika ViscoCrete® superplasticizers, SikaRapid® accelerators, and Sikafloor® coating systems, highlights its commitment to environmentally friendly and technically effective solutions.

Companies Covered in Carbon Textile Reinforced Concrete Market

- BASF SE

- Sika AG

- ADCOS NV

- Solidian GmbH

- CarboCon GmbH

- Hering Architectural Concrete

- Raina Industries Pvt. Ltd.

- Weserland GmbH

- Rezplast Mfg

- Weihai Jingsheng Carbon Fiber Products Co., Ltd.

- Tokyo Rope Manufacturing Co., Ltd.

- Technical University Dresden

- Fischer Werke GmbH & Co. KG

- Master Builders Solutions

- Smart Engineering

Frequently Asked Questions

The global carbon textile reinforced concrete market is valued at US$ 1.75 Bn in 2026 and is projected to reach US$ 3.48 Bn by 2033, expanding at a CAGR of 10.3% during the forecast period.

The market is driven by aging infrastructure rehabilitation requirements, superior corrosion resistance compared to steel reinforcement, government embodied carbon reduction mandates, and the material's lightweight characteristics, enabling reduced structural dead loads while extending asset lifecycles.

Large-tow carbon fiber concrete type dominates with approximately 58% market share, offering favorable production economics, adequate structural performance for mainstream applications, and progressively improving technical characteristics through ongoing manufacturing innovations.

Europe maintains market leadership through Germany's advanced research infrastructure, regulatory approval frameworks, including general building certifications, and successful demonstration projects like Technical University Dresden's CUBE building, establishing commercial deployment pathways.

Significant opportunities emerge from green building certification requirements, with major contractors committing to lower-emission concrete projects by 2026, government agencies establishing measurable carbon reduction targets, and Asia-Pacific urbanization driving infrastructure investment across China, India, and ASEAN nations.

Leading market participants include Solidian GmbH, BASF SE, Sika AG, ADCOS NV, CarboCon GmbH, Hering Architectural Concrete, Weserland GmbH, and Hitexbau GmbH, competing through product innovation, regulatory approval acquisition, and strategic research collaborations.