- Automotive Components & Materials

- Automotive Speed Reducer Market

Automotive Speed Reducer Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Speed Reducer Market Product Type (Planetary Gear Reducers, Helical Gear Reducers, Worm Gear Reducers, Spur Gear Reducers, Bevel Gear Reducers, Other Reducer Types), Technology (Manual, Automatic, Electronically Controlled, Adaptive), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles), Sales Channel (OEM, Aftermarket), and Regional Analysis from 2026 to 2033

Automotive Speed Reducer Market Size and Trend Analysis

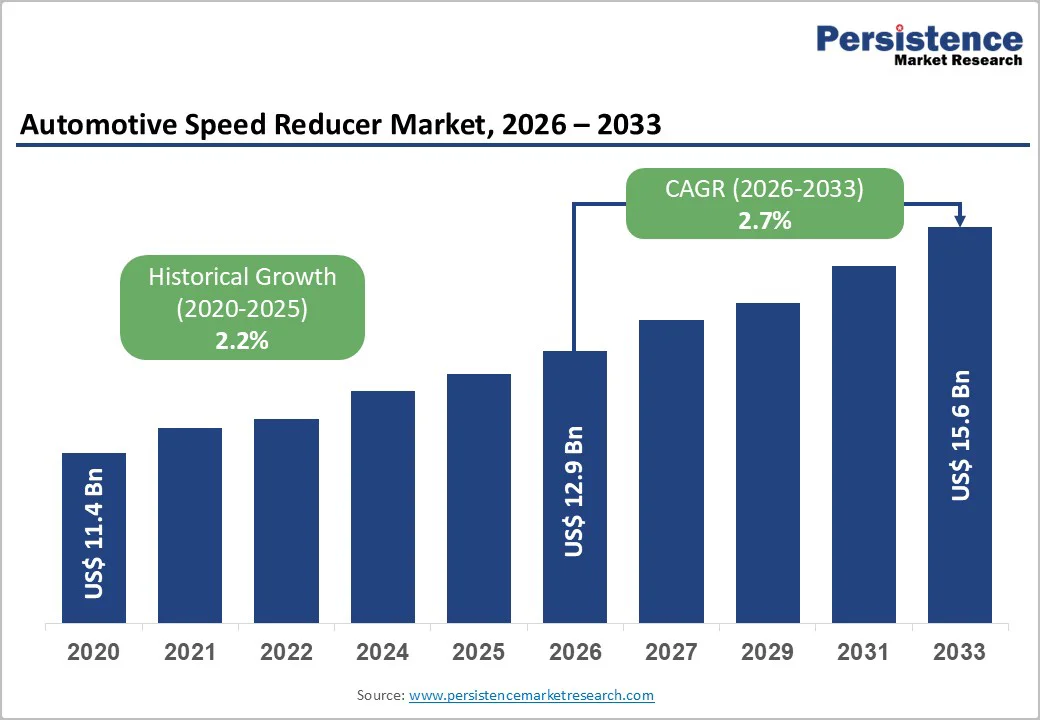

The global Automotive Speed Reducer Market size is anticipated at US$12.9 billion in 2026 and is projected to reach US$15.6 billion by 2033, growing at a CAGR of 2.7% between 2026 and 2033.

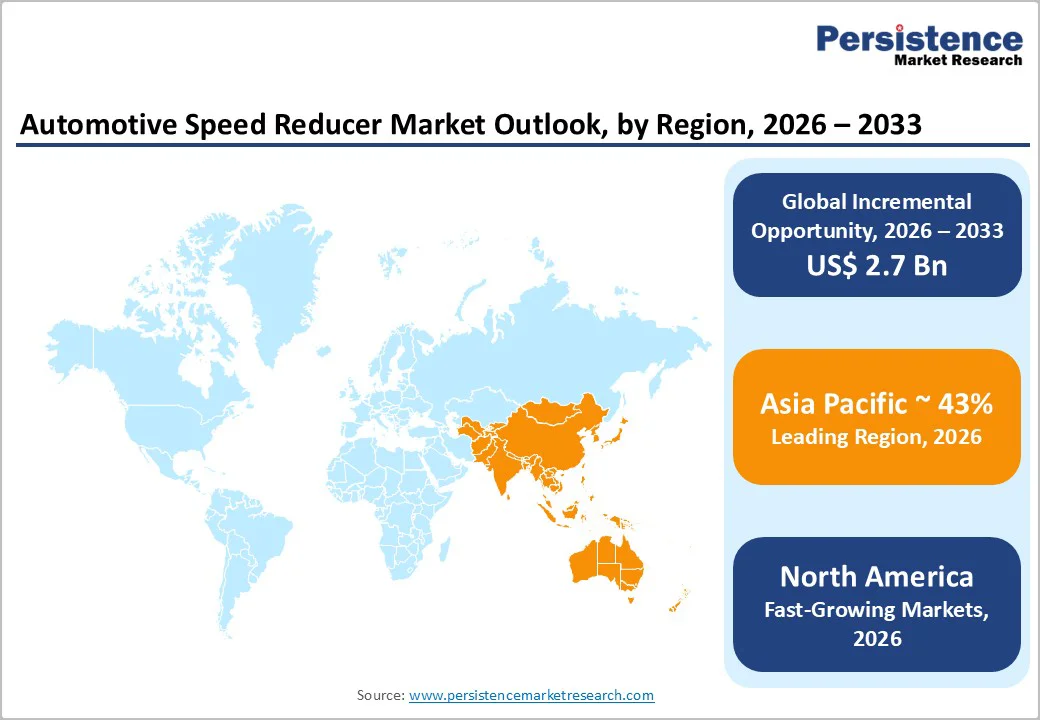

Market expansion is driven by electric vehicle adoption, which requires advanced torque management, stringent fuel-efficiency and emissions regulations mandating modern transmission technologies, and ongoing modernization of multi-speed automatic platforms to improve drivability. North America grows through regulatory support and innovation, Europe remains stable due to strength, while the Asia Pacific leads growth.

Key Highlights Summary

- Planetary gear reducers command ~28% market share, reflecting compact design and torque density advantages, while Helical gear reducers expand at 3.0% CAGR, supporting noise reduction and precision applications.

- Manual transmission technology dominates at 42% share, reflecting cost-effectiveness, while Adaptive technology expands at 6.5% CAGR, driven by AI-powered transmission optimization and electronic controls.

- Passenger vehicles lead at 46% market share, while Electric vehicles expand at 7.3% CAGR, supporting specialized EV drivetrain requirements and emerging platform development.

- Europe maintains 22% market share with emission compliance emphasis, Asia Pacific dominates 43% with EV manufacturing leadership, and North America grows at 2.2% CAGR with technology innovation focus.

- ZF launches 8-speed automatic, reducing fuel consumption 10% (January 2024), introduces eDrive 2-speed transmission, improving highway efficiency 15% (March 2024), and announces ICE transmission phase-out by 2027, demonstrating strategic technology transformation and EV-focused market pivot.

| Key Insights | Details |

|---|---|

| Automotive Speed Reducer Market Size (2026E) | US$ 12.9 billion |

| Market Value Forecast (2033F) | US$ 15.6 billion |

| Projected Growth CAGR (2026-2033) | 2.7% |

| Historical Market Growth (2020-2025) | 2.2% |

Market Dynamics Analysis

Market Drivers

Electric Vehicle Adoption and Specialized EV Drivetrain Requirements Supporting Equipment Modernization

Electric vehicle adoption and specialized drivetrain requirements are systematically driving speed reducer demand, with EV gear reducers commanding 20–22% share within the overall EV parts market and manufacturers such as Lucid Motors adopting integrated eGearDrive solutions combining motor, inverter, and transmission. Single- and two-speed EV reducers enable precise torque optimization, while compact and lightweight design requirements support vehicle range targets. High torque density support and energy efficiency improvements enhance acceleration and drivability. Integrated drivetrain solutions enable performance optimization for EVs, while emerging EV platform requirements continue to stimulate sustained investment across global electric mobility value chains and future technology adoption.

Fuel Efficiency Requirements and Emission Regulation Compliance Supporting Technology Advancement

Fuel efficiency requirements and stringent emission regulations are systematically driving speed reducer technology advancement, with multi-speed automatic transmissions increasingly adopted to comply with global standards and manufacturers achieving 10–15% fuel consumption reduction through advanced systems. Global emission reduction targets accelerate fuel consumption optimization, while the adoption of multi-speed transmissions improves operating efficiency across driving cycles. Advanced lubricants and materials reduce friction losses, and thermal management systems enhance durability under higher loads. Precision engineering support enables tighter tolerances and reliability, while cost-effective solutions ensure scalability across passenger and commercial vehicle segments, sustaining continuous modernization of transmission platforms worldwide and long-term regulatory compliance globally.

Market Restraints

Supply Chain Complexity and Manufacturing Cost Pressures Limiting Market Penetration

Complex manufacturing requirements constrain speed reducer market expansion and precision engineering demands, creating significant production costs and supply chain complexities, particularly affecting smaller manufacturers and emerging market suppliers, limiting market penetration in cost-sensitive segments. Precision manufacturing requirements. Skilled workforce requirements. Equipment investment needs. Quality control standards. Supply chain vulnerabilities. Logistics costs inflation. Component sourcing challenges.

EV Transition and Declining ICE Transmission Market Creating Structural Challenges

The speed reducer market's expansion is constrained by accelerating EV adoption and a reduction in multi-speed automatic transmission requirements. JATCO has experienced a 30% decline in CVT orders as Nissan shifts to EVs, including the Ariya single-speed reducer, creating fundamental market disruption that affects traditional transmission suppliers and requires strategic business model transformation. Declining ICE vehicle demand. Single-speed EV prevalence. Reduced transmission maintenance. Structural market disruption. Obsolescence risk for ICE suppliers. Technology transition costs. Market share realignment.

Market Opportunities

Advanced Materials and Lightweight Design Supporting Premium Market Positioning

Advanced materials and lightweight design implementation represent an emerging opportunity, with carbon-based additives in reduction gears reducing friction loss and thermal buildup. At the same time, manufacturers develop lightweight aluminum alloy and composite solutions to enhance efficiency. Carbon-based additives integration improves lubrication stability, aluminum alloy development enables structural mass reduction, and composite materials application supports targeted weight reduction without compromising durability. Defined weight-reduction targets enable performance enhancement in high-performance electric vehicle platforms while maintaining a cost-optimization balance. Sustainability positioning is strengthened through material efficiency, lower energy losses, reduced emissions, and alignment with circular manufacturing principles across global automotive drivetrain value chains.

Autonomous Vehicle Integration and V2X Communication Requirements

Autonomous vehicle development and vehicle-to-vehicle communication represent an emerging opportunity, as autonomous platforms require specialized drivetrain coordination and real-time transmission control, driving demand for electronically controlled and adaptive speed reducers. Autonomous vehicle platforms rely on advanced electronic control systems, V2V communication support, and real-time torque management to ensure smooth operation across diverse driving scenarios. Software integration requirements increase as speed reducers interface with safety-critical systems governing redundancy, fault tolerance, and response accuracy. These capabilities enable future vehicle readiness by supporting scalable architectures, enhanced safety performance, predictive control strategies, and seamless integration within next-generation autonomous mobility ecosystems globally and worldwide adoption

Segmentation Analysis

Product Type Analysis

Planetary gear reducers command 28% of market share, representing dominant reducer type reflecting high torque density, compact design, and durability supporting broad adoption across conventional and electric vehicle platforms, with particularly strong positioning in EV drivetrains where compact footprint and efficiency are critical. High torque density in a compact space. Durability and reliability focus. EV drivetrain integration. Conventional vehicle application. Cost-effective designs. Maintenance simplicity. Global market dominance.

Helical gear reducers are the fastest-growing reducer type, with a 3.0% CAGR, driven by smoother meshing and reduced noise compared to spur gears, supporting emerging demand in precision applications and noise-sensitive segments, reflecting technology advancements and market segmentation. Smooth meshing operation. Noise reduction benefits. Precision manufacturing support. Performance optimization capabilities. Cost-effectiveness improvement. Hybrid vehicle compatibility. Emerging application focus.

Technology Analysis

Manual transmission technology commands 42% of market share, representing an established standard reflecting cost-effectiveness, mechanical simplicity, and broad consumer familiarity, supporting a dominant position, particularly in emerging markets and cost-conscious vehicle segments. Cost-effectiveness advantage. Mechanical simplicity design. Easy maintenance support. Consumer familiarity positioning. Emerging market prevalence. Proven technology maturity. Broad compatibility across platforms.

Adaptive transmission technology is expanding at a 6.5% CAGR, driven by electronic controls and AI-powered transmission logic that optimize gear selection, support emerging demand for intelligent transmission systems, and maximize efficiency and performance, enhancing the driving experience. Electronic control systems. AI-powered optimization. Real-time adjustment capability. Efficiency improvement focus. Performance enhancement support. Emerging platform integration. Premium market positioning.

Vehicle Type Analysis

Passenger vehicles command ~46% of market share, representing the dominant vehicle category, reflecting the highest volume production and broad reducer adoption across diverse drivetrain architectures and performance requirements, supporting broad market penetration across global markets. Volume production scale. Diverse drivetrain requirements. Consumer demand leadership. Cost-sensitive positioning. Technology variety. Global distribution networks. Market leadership position.

Electric vehicles are the fastest-growing vehicle category, with a 7.3% CAGR, driven by specialized EV reducer requirements for torque management and efficiency optimization, supporting emerging demand for dedicated EV drivetrain solutions, reflecting accelerating EV market growth and technology specialization. EV-specific design requirements. Torque optimization support. Compact footprint advantages. Energy efficiency focus. Performance capability parity. Emerging market leadership. Technology innovation.

Sales Channel Analysis

The original equipment manufacturer channel commands around 68% of market share, reflecting direct vehicle manufacturer integration and long-term supply contracts that support sustained revenue generation across vehicle production cycles. Direct manufacturer integration. Long-term contract stability. Volume commitments predictability. Technology collaboration. Joint development programs. Supply chain efficiency. Market leadership dominance.

Aftermarket channel is expanding as a prominent, high-growth sales channel, with a 1.8% CAGR, driven by vehicle fleet modernization and equipment replacement requirements, supporting emerging demand for replacement and upgrade solutions reflecting vehicle fleet maturation and independent service provider growth. Fleet modernization requirements. Replacement demand expansion. Service provider growth. Cost-effective upgrades. Technology refreshes. Independent repair networks. Secondary market development.

Regional Market Insights

North America

North America expands at a 2.2% CAGR, driven by fuel-efficiency regulations, technology leadership, OEM supplier relationships, and regulatory frameworks that support market development and equipment modernization. Fuel efficiency mandate compliance. Technology innovation leadership. OEM partnerships dominance. Regulatory clarity. Supply chain excellence. Advanced testing facilities. Competitive dynamics.

The North American market is characterized by regulatory clarity and technology leadership, with OEM suppliers maintaining competitive advantages through scale and innovation. Established supply chains and technology centers supporting rapid advancement. Strong R&D investment and patent portfolios. Premium positioning enabling higher margins through advanced solutions.

Europe

Europe maintains a 22% market share, with considerable growth, driven by strict emission standards, manufacturing excellence, an emphasis on sustainability, and regulatory harmonization that supports advanced technology adoption. Emission standard compliance. Manufacturing excellence heritage. Sustainability focus. Regulatory harmonization support. Technology leadership positioning. Supply chain integration. Premium market focus.

The European market is characterized by strict regulatory compliance and technology excellence, with established manufacturers maintaining global leadership positions. Strong emphasis on efficiency and environmental impact reduction. Established technical standards supporting reliability. Premium positioning attracting high-value customers and partnerships.

Asia Pacific

Asia Pacific dominates at 43% market share, driven by rapid vehicle manufacturing, emerging market growth, cost-competitive production, and EV technology leadership supporting market growth exceeding global averages. Vehicle manufacturing scale. EV technology leadership. Cost-competitive production. Government support programs. Emerging market growth. Supply chain development. Regional hubs.

The Asia Pacific market is characterized by rapid growth and manufacturing leadership, with Chinese EV manufacturers driving technology innovation. Cost-competitive production attracts global supply chain development. Government EV support programs are accelerating adoption. Emerging market vehicle proliferation is supporting sustained expansion.

Competitive Landscape

The automotive speed reducer market exhibits a consolidated structure, led by players such as ZF Friedrichshafen, Aisin Seiki, and BorgWarner, which leverage technology innovation, OEM partnerships, and drivetrain solutions. Regional specialists, including Eaton Corporation, Continental AG, and Allison Transmission, strengthen their positioning through geographic focus and application expertise, while emerging EV-focused suppliers capture growth through specialized e-drivetrain solutions that enable technology-driven competitive differentiation.

Strategic Developments

- In January 2024, ZF introduced a next-generation 8-speed automatic transmission, reducing fuel consumption by 10% in ICE vehicles, featuring advanced controls and efficiency optimization supporting fuel economy improvements across conventional vehicle platforms and demonstrating technology advancement momentum.

- In March 2024, ZF disclosed eDrive 2-speed transmission for electric vehicles, improving highway efficiency by 15% compared to single-speed systems, featuring a compact design and integrated motor support for modern EV architectures, including the Jeep Wagoneer S application.

Business Strategies

Market leaders pursue technology differentiation via EV-specific drivetrains, OEM partnerships securing long-term supply, regional manufacturing expansion, and sustainability through efficiency gains. Integrated supply chains reduce costs, while R&D in advanced materials and controls supports the transition from ICE to EV platforms. Multinationals emphasize integrated solutions, regional specialists target cost-led markets, and EV-focused players capture high-growth niches through collaborations and innovation acceleration

Companies Covered in Automotive Speed Reducer Market

- ZF Friedrichshafen AG

- Aisin Seiki Co., Ltd.

- BorgWarner Inc.

- Eaton Corporation

- Continental AG

- Allison Transmission

- JATCO Ltd.

- Getrag (Magna Powertrain)

- Dana Incorporated

- Schaeffler Group

- GKN Automotive

Musashi Seimitsu Industry

Frequently Asked Questions

The global Automotive Speed Reducer Market is anticipated at US$ 12.9 Billion in 2026 and is projected to reach US$ 15.6 Billion by 2033.

Market growth is driven by rising EV adoption requiring compact torque management, stringent fuel-efficiency and emission regulations, and modernization of multi-speed automatic and hybrid transmission systems.

The market is projected to expand at a 2.7% CAGR between 2026 and 2033.

Key opportunities include emerging-market vehicle production growth, lightweight and advanced material integration, and electronically controlled reducers for hybrid and autonomous vehicle platforms.

Key players include ZF Friedrichshafen, Aisin Seiki, BorgWarner, Eaton Corporation, Continental AG, and Allison Transmission, with ZF leading through advanced automatic, hybrid, and EV drivetrain innovations.