- Automotive Components & Materials

- Automotive Side Impact Assembly Market

Automotive Side Impact Assembly Market Size, Share, and Growth Forecast 2026 – 2033

Automotive Side Impact Assembly Market: Material Type (Stainless Steel, Aluminum, Plastic, Titanium), Application (Front Side Doors, Rear Side Doors), Vehicle Type (Passenger Vehicle, Commercial Vehicle), Region Analysis 2026-2033

Automotive Side Impact Assembly Market Size and Share Analysis

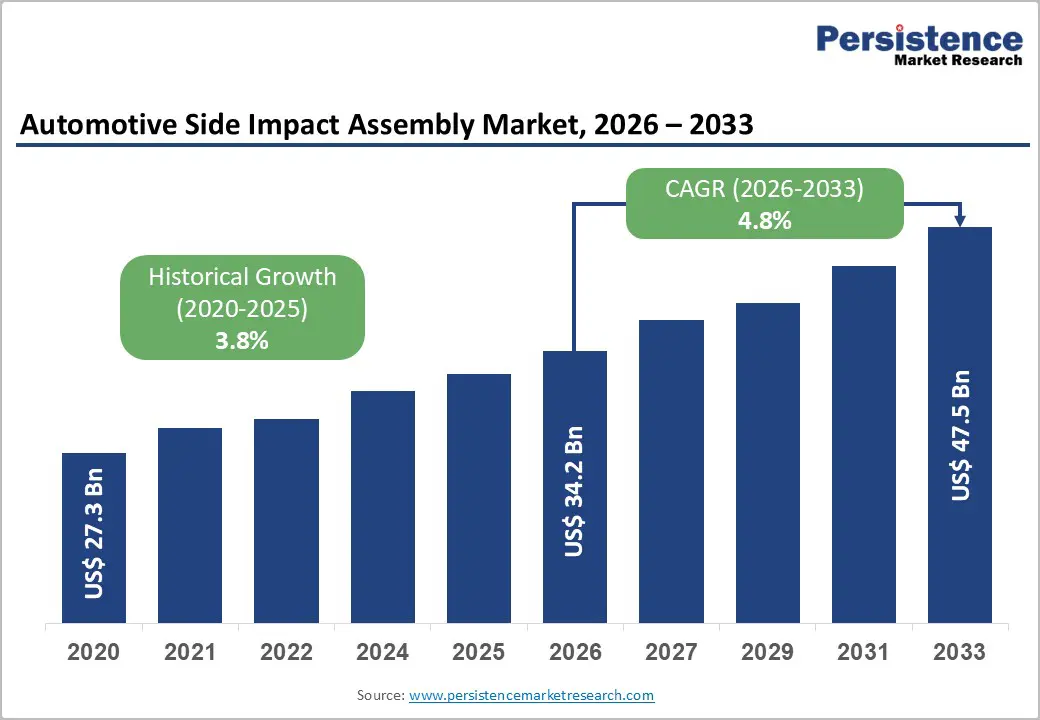

The global Automotive Side Impact Assembly Market size is likely to be projected at US$ 33.8 Billion in 2026 and is projected to reach US$ 47.5 Billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033. Market expansion is driven by systematic tightening of global safety regulations with Euro NCAP and NHTSA demanding advanced side impact protection across all vehicle categories, rapid proliferation of electric vehicles requiring specialized lightweight side impact assemblies balancing weight reduction with crashworthiness requirements, and sustained investment in advanced passive safety systems integrating sensors and adaptive technologies with traditional side impact beams creating comprehensive occupant protection ecosystems.

Key Highlights Summary

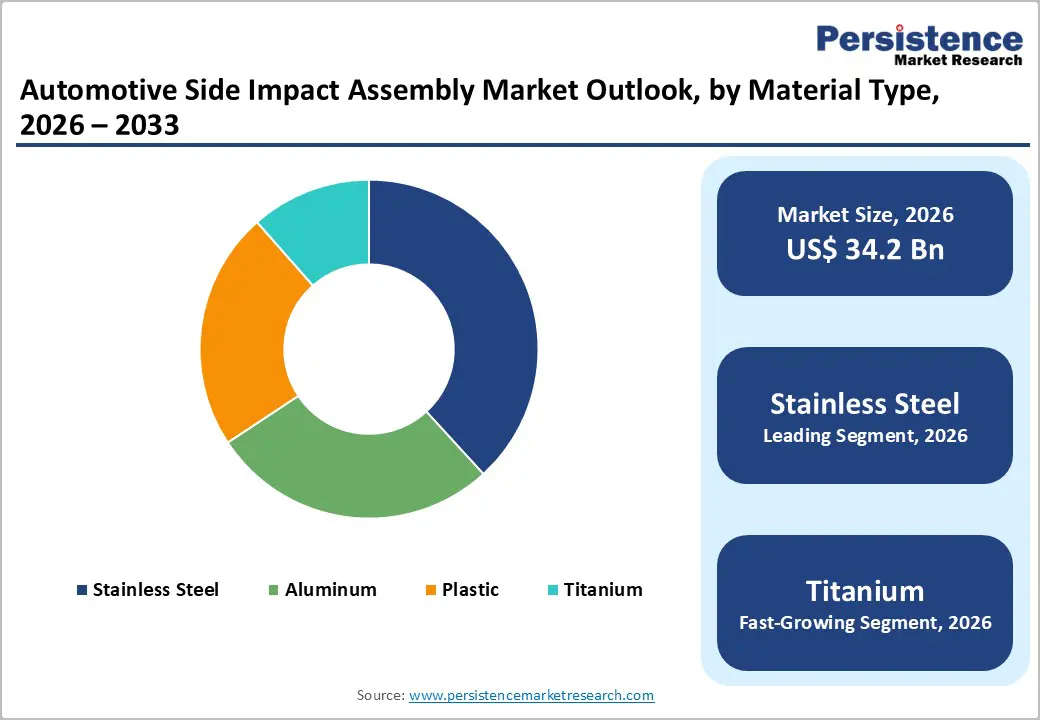

- Stainless steel commands 38% market share with stable 3.1% CAGR, while titanium expands fastest at 5.9% CAGR driven by premium EV and luxury vehicle adoption.

- Front side doors maintain 61% market share, while rear side doors expand 5.1% CAGR driven by emerging three-row SUV and premium vehicle growth.

- Passenger vehicles dominate 72% market share, while commercial vehicles expand 5.2% CAGR driven by emerging light commercial vehicle and regulatory compliance momentum.

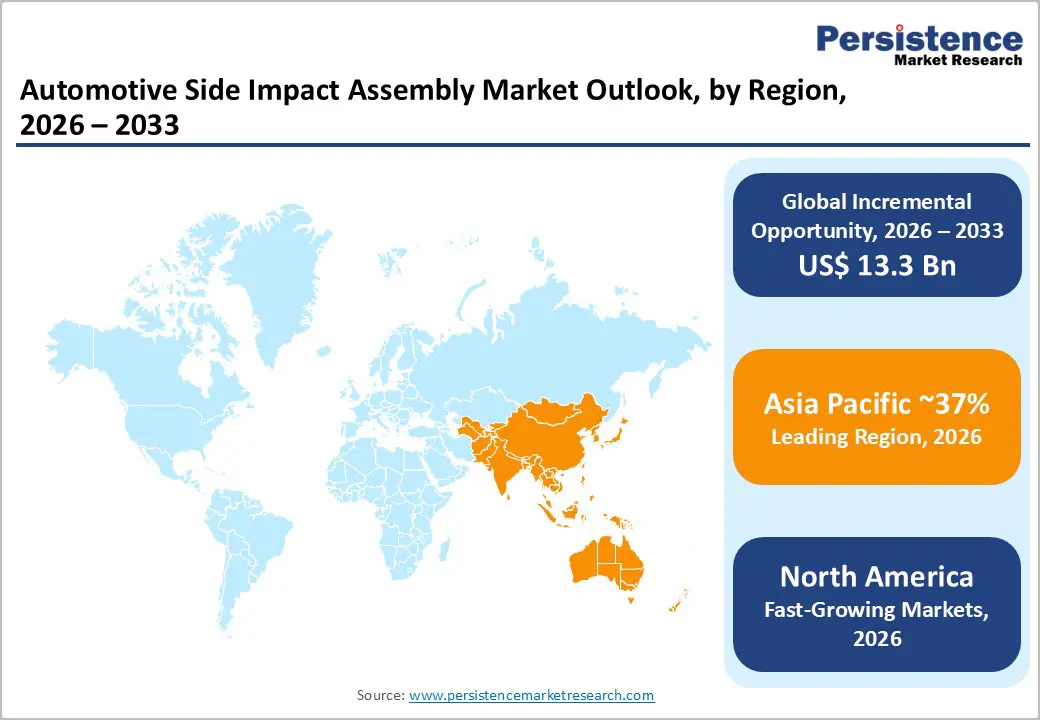

- North America holds 25% at 4.4% CAGR with EV and autonomous vehicle focus, Europe maintains 26% with 4.3% CAGR emphasizing premium solutions, Asia-Pacific dominates 37% with fastest regional growth supported by emerging manufacturing.

- Autoliv launches 50% emission-reducing recycled polyester airbag (June 2024), ZF LIFETEC showcases dual-stage innovation (September 2024), Bosch introduces AI-powered detection (November 2024), Hyundai Mobis launches door-mounted airbag (February 2025), ArcelorMittal launches lightweight steel (April 2025) demonstrating continuous technology advancement momentum.

| Key Insights | Details |

|---|---|

| Automotive Side Impact Assembly Market Size (2026E) | US$34.2 Bn |

| Market Value Forecast (2033F) | US$47.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.8% |

Market Dynamics Analysis

Market Drivers

Stringent Global Safety Regulations and Crash Performance Standards

Global safety regulations systematically drive side impact assembly demand, as Euro NCAP and FMVSS 214 mandate standardized side crash testing that requires assemblies to absorb and redistribute collision energy to protect passenger compartments. NHTSA and Euro NCAP protocols enforcing 30 mph lateral impact compliance, combined with global vehicle production of roughly 82 million units annually, highlight strong, recurring adoption momentum supporting sustained market expansion. Regulatory non-compliance penalties ranging from USD 50,000 to USD 100,000 per vehicle create powerful economic incentives, compelling OEMs to invest in advanced, reliable side impact assembly solutions, particularly for high-volume mass-market platforms requiring cost-efficient designs that consistently meet evolving global safety benchmarks across all vehicle segments.

Advanced Passive Safety System Integration and Multi-Function Assembly Design

Advanced passive safety integration systematically drives side impact assembly sophistication, as the global automotive passive safety systems market grows at a 5.6% CAGR, reflecting accelerating technology integration across vehicle platforms. Sensor-equipped side impact beams enable pre-collision detection, predictive load management, and coordinated airbag deployment, while integrated side curtain airbag mounting points and seatbelt pretensioner synchronization create multifunctional safety architectures. These assemblies enhance occupant protection during lateral impacts, improve system response timing, and support software-enabled safety optimization. The convergence of structural protection with sensing and actuation capabilities strengthens premium vehicle differentiation, justifies higher component value, and encourages OEM investment in advanced side impact assemblies aligned with evolving regulatory and consumer expectations.

Market Restraints

Material Cost Inflation and Premium Aluminum/Titanium Sourcing Challenges

Market expansion is constrained by aluminum side impact beam costs ranging USD 80–120 per unit versus USD 40–60 for steel alternatives, creating significant cost pressure for budget vehicle segments. Titanium’s limited availability and complex processing add a USD 150–200 per unit premium, restricting adoption largely to luxury and electric vehicles. These material cost disparities limit mass-market penetration, slow volume scalability, and temper overall market growth acceleration despite rising regulatory and safety-driven demand globally across key automotive manufacturing regions worldwide today.

Design Complexity and Validation Testing Requirements

Market expansion is constrained by complex crash simulation and physical testing protocols requiring 15–20 prototype iterations and USD 2–5 million in validation costs per design variant, creating high entry barriers for emerging suppliers and aftermarket players. Multi-year design-to-production timelines, combined with frequently evolving safety standards, force repeated engineering revisions, extend development cycles, inflate costs, and pressure margins, ultimately affecting supplier profitability, investment appetite, and long-term viability across competitive automotive safety component ecosystems globally and across multiple vehicle segments worldwide today.

Market Opportunities

Autonomous Vehicle Development and Sensor-Integrated Assembly

Autonomous vehicle development represents a major opportunity, as SAE Level 3–4 vehicles require predictive safety architectures where sensor-integrated side impact beams support collision anticipation, avoidance coordination, and adaptive occupant protection. These advanced assemblies enable data fusion between radar, cameras, and airbags, creating autonomous-optimized safety ecosystems beyond traditional passive protection. Waymo, Tesla, and leading OEM autonomous programs collectively invest over USD 5 billion annually in safety technology development, accelerating demand for intelligent structural components. This investment momentum is fostering an emerging market for innovative side impact solutions that enhance system redundancy, improve regulatory readiness, and deliver clear technology differentiation across next-generation autonomous and semi-autonomous vehicle platforms globally across premium mobility segments.

Lightweight Material Innovation and Sustainable Component Design

Lightweight material innovation represents a strong opportunity, as advanced composites and aluminum alloy developments reduce side impact beam weight by 20–30% while fully maintaining stringent crashworthiness standards. These advancements support an emerging sustainable materials segment valued at approximately USD 1.5–2.0 billion annually across global automotive platforms. Expanded use of recycled aluminum and high-strength steel, combined with circular economy manufacturing integration, enables OEMs to achieve emission reduction targets without compromising safety performance. This shift creates premium sustainable positioning opportunities, particularly in Europe and North America, where regulatory pressure, environmental awareness, and lifecycle carbon reduction mandates strongly influence vehicle design decisions and supplier selection strategies for future electrified and autonomous mobility programs.

Segmentation Analysis

Material Type Analysis

Stainless steel commands 38% of global market share, representing dominant material type with proven crashworthiness performance, cost-effectiveness at USD 40-60 per unit, and established manufacturing processes. Stainless steel automotive applications growing at 3.1% CAGR with established supply chains supporting consistent market dominance particularly for mid-range and commercial vehicles where cost optimization remains critical providing stable revenue anchor and reliable production capacity.

Titanium expands at 5.9% CAGR driven by superior strength-to-weight ratio enabling 20-30% weight reduction combined with exceptional corrosion resistance supporting emerging premium EV and luxury vehicle positioning. Titanium adoption growing in Tesla Model 3, BMW iX, and emerging EV platforms enables emerging high-value specialized segment, supporting premium market differentiation and emerging advanced material leadership.

Application Analysis

Front side doors command 61% of market share, driven by higher collision frequency in urban environments and frontal-offset crash scenarios requiring sophisticated side impact protection. Front door beam integration with driver/passenger safety requirements supporting dominant market positioning with established OEM specifications and consistent heavy manufacturing volume providing market stability anchor and reliable production economics.

Rear side doors expand at 5.1% CAGR driven by emerging three-row SUV and premium vehicle growth requiring rear passenger protection and evolving child safety seat accommodation standards. Rear side impact assembly customization for family vehicles and commercial multi-passenger configurations enables emerging specialized market segment supporting emerging growth momentum particularly in SUV and crossover vehicle categories.

Vehicle Type Analysis

Passenger vehicles command 72% of market share, encompassing compact, mid-size, SUV, and luxury segments with diverse side impact assembly requirements across segments. Global passenger vehicle production of 75 million units annually combined with established safety rating emphasis (Euro NCAP, NHTSA ratings) supporting consistent strong demand providing market stability anchor and revenue volume foundation.

Commercial vehicles expand at 5.2% CAGR driven by emerging light commercial vehicle and heavy commercial vehicle production growth particularly in India, China, and Southeast Asia. Commercial vehicle side impact assembly adoption driven by regulatory compliance and fleet safety standards combined with emerging commercial laundry and logistics market growth, supports emerging specialized commercial segment, enabling dedicated commercial-focused product development.

Regional Market Insights

North America

North America maintains roughly 25% market share, expanding at a 4.4% CAGR, supported by a strong OEM base including General Motors, Ford, and Tesla, a stringent NHTSA regulatory framework, and rising premium EV adoption. The U.S. market benefits from high-volume EV production as Tesla, General Motors, and Stellantis expand manufacturing capacity, reinforcing demand for advanced side impact assemblies. Emphasis on passive-to-active safety integration, sensor-enabled architectures, and autonomous vehicle readiness supports premium positioning. Advanced engineering capabilities, comprehensive crash-testing infrastructure, and mature supply chains enable rapid innovation cycles, consistent quality, production efficiency, and sustained technology leadership across evolving automotive safety and mobility ecosystems nationwide.

Europe

Europe maintains 26% market share, growing at a 4.3% CAGR, driven by stringent Euro NCAP crash testing standards, demanding OEM safety benchmarks, and strong sustainability focus. The region leads premium vehicle production and electric vehicle adoption, with Germany, the United Kingdom, France, and Spain showcasing advanced engineering expertise. This environment supports widespread adoption of lightweight aluminum and titanium side impact solutions, particularly in luxury segments balancing crashworthiness with design elegance. A dense presence of premium manufacturers drives design sophistication and advanced material integration. Robust regulatory frameworks promote continuous safety innovation, while mature circular economy initiatives accelerate sustainable material sourcing, recycling practices, and lifecycle carbon reduction across European automotive supply chains.

Asia Pacific

Asia Pacific dominates with a 37% market share and the fastest growth trajectory, driven by rapid vehicle production expansion, accelerating EV adoption, and cost-competitive manufacturing ecosystems. China, India, and Japan lead regional output, with China producing over 30 million vehicles annually and India rapidly expanding commercial vehicle manufacturing capacity. These dynamics support high-volume demand, localized side impact assembly production, and the emergence of regional suppliers, particularly in commercial vehicle segments. Expanding manufacturing capabilities enable scalable, cost-efficient solutions, while rapid urbanization increases safety feature adoption and regulatory compliance focus. Strong government support through industrial policies, localization mandates, and electric vehicle incentives further strengthens investment momentum, supply chain development, technology transfer, and long-term market leadership across the Asia Pacific automotive safety landscape.

Competitive Landscape

Strategic Developments

- In June 2024, Autoliv introduced eco-friendly side impact airbag cushions manufactured from 100% recycled polyester, delivering equivalent safety performance while reducing greenhouse gas emissions by 50% at polymer level, advancing sustainability integration and environmental responsibility.

- In November 2024, Bosch launched advanced sensor integration enabling predictive side impact detection with machine learning algorithms, supporting autonomous vehicle safety ecosystem development and collision avoidance coordination with emerging autonomous driving platforms.

- In April 2025, ArcelorMittal introduced next-generation high-strength steel enabling 15% weight reduction while maintaining crashworthiness standards, supporting cost-effective lightweight solution for emerging market vehicle segments and emerging EV platform adoption.

Business Strategies

Market leaders employ innovation-focused product development advancing sensor-integrated assemblies and lightweight materials, geographic expansion targeting Asia-Pacific emerging markets, strategic supplier partnerships strengthening supply chain resilience, sustainability positioning through recycled materials and circular economy integration, and premium feature emphasis supporting autonomous vehicle and EV market penetration. Cost leadership strategies remain critical for commercial vehicle segments.

Companies Covered in Automotive Side Impact Assembly Market

- Autoliv Inc.

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Magna International

- Aptiv PLC

- Hyundai Mobis

- Thyssenkrupp

- Brose Fahrzeugteile

- GESTAMP

- ArcelorMittal

- Novellus

- Continental AG

- Taiga Motors

- Tianjin Lishen Battery

Frequently Asked Questions

The Automotive Side Impact Assembly Market is valued at US$ 33.8 billion in 2026 and is projected to reach US$ 47.5 billion by 2033.

Market growth is propelled by stringent global side-impact safety mandates, rapid electric vehicle production growth, expanding passive safety system adoption, and rising commercial vehicle demand in emerging economies.

The market expands at 4.8% CAGR between 2026 and 2033.

Key opportunities lie in Asia-Pacific expansion, sensor-integrated autonomous vehicle safety systems, and lightweight material innovation enabling weight reduction without compromising crash performance.

Leading players include Autoliv, ZF Friedrichshafen, Robert Bosch, and Magna International, supported by Aptiv, Hyundai Mobis, Thyssenkrupp, GESTAMP, and ArcelorMittal, all actively driving innovation in safety, lightweighting, and sustainability.