- Automotive Components & Materials

- Automotive LiDAR Market

Automotive LiDAR Market Size, Share, and Growth Forecast for 2026 - 2033

Automotive LiDAR Market by Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Electric Vehicle), Range (Short, Medium, Long), Application (ADAS, Autonomous Cars), Type, and Regional Analysis for 2026 - 2033

Automotive LiDAR Market Size and Trends

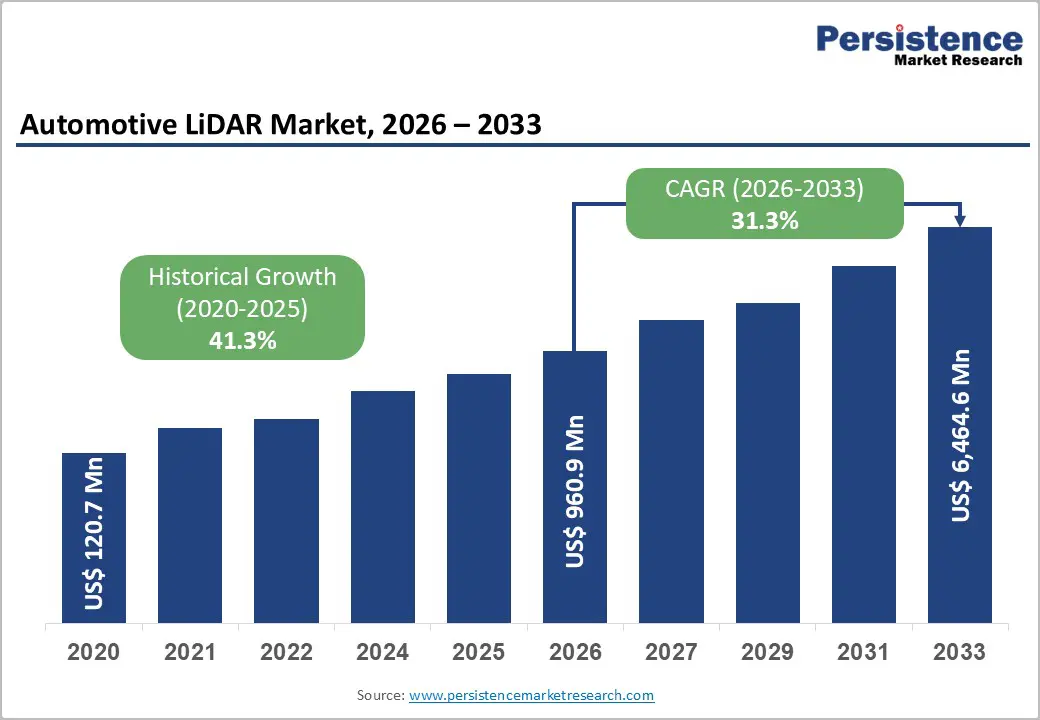

The global automotive LiDAR market size is supposed to be valued at US$ 960.9 Mn in 2026 and is projected to reach US$ 6,464.4 Mn by 2033, growing at a CAGR of 31.3% between 2026 and 2033.

The growth of the automotive LiDAR market is primarily driven by the rising adoption of autonomous and ADAS technologies, stricter safety regulations, and increasing demand for enhanced driving experiences. OEMs are pushing for higher levels of vehicle autonomy, leading to the integration of LiDAR sensors alongside cameras and radars to improve perception and safety.

Key Industry Highlights:

- Leading Region: Asia Pacific dominates with 55% market share driven by China's aggressive NEV deployment, MIIT's mandatory L2 ADAS standards incorporating LiDAR in September 2025, and domestic champions Hesai and RoboSense achieving million-unit production scale with extensive OEM partnerships.

- Fastest Growing Region: North America exhibits the highest growth through 2033, propelled by Silicon Valley innovation ecosystem, NHTSA's April 2025 Automated Vehicle Framework providing regulatory clarity, and Luminar Technologies' expanding OEM partnerships for next-generation ADAS and autonomous systems.

- Dominant Segment: Solid-state LiDAR commands 58% share due to superior reliability with 10+ year lifespans, compact form factors enabling seamless vehicle integration, and manufacturing costs declining toward USD 500 per unit at scale, representing 60-70% cost reduction versus mechanical alternatives.

- Fastest Growing Segment: Electric Vehicles grow at 35.7% CAGR driven by EV manufacturers positioning LiDAR as a premium differentiator, with global EV LiDAR sensor market projected at USD 10,500 million by 2025 and flagship models from Li Auto, NIO, Xiaomi, and Zeekr standardizing integration.

- Key Market Opportunity: Autonomous robotaxi and commercial fleet deployment prioritizing reliability over cost enables premium LiDAR adoption, with Hesai's cumulative deliveries exceeding 1.37 million units across ADAS and robotics, and projections suggesting millions of units by 2028 as dedicated autonomous fleets scale.

| Key Insights | Details |

|---|---|

| Automotive LiDAR Market Size (2026E) | US$ 960.9 Mn |

| Market Value Forecast (2033F) | US$ 6,455.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 31.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 41.3% |

Market Dynamics

Driver - Mass Production Efforts by Companies to Reduce LiDAR Costs, Making it More Accessible

The automotive LiDAR industry is experiencing significant growth, driven by increasing adoption of autonomous and semi-autonomous vehicles. Leading companies like Tesla, Waymo, and General Motors (Cruise) are heavily investing in self-driving technology, with LiDAR playing a key role in real-time 3D mapping, enabling higher levels of automation.

China is accelerating the deployment of LiDAR-equipped robotaxis, with key cities like Beijing, Shanghai, and Shenzhen granting permits for fully autonomous ride-hailing services to companies such as Baidu and AutoX. The NHTSA has approved AV testing without human drivers, pushing automakers toward LiDAR for safety.

Enhancements in LiDAR performance and cost reduction are making the technology more accessible for mass adoption. For instance,

- The traditional mechanical LiDAR units, once priced over US$ 75,000 per unit, have significantly dropped in cost due to mass production efforts by companies such as Luminar, Ouster, and Hesai, with some sensors now available for under US$ 1,000.

The development of solid-state LiDAR, such as Ouster’s REV7 and Aeva’s Atlas Ultra, has further improved affordability, durability, and compactness, making LiDAR viable for mass-market vehicles. Government funding and investments are also driving LiDAR innovation, with the European Union allocating €1.5 billion under the Horizon Europe program to support AI and sensor technologies, including LiDAR. The U.S. Department of Energy (DOE) is further backing research into LiDAR-enabled vehicles for energy efficiency and urban mobility.

Technological Advancements Enabling Cost Reduction and Mass Market Adoption

Rapid technological innovation in solid-state LiDAR is fundamentally transforming market economics and scalability. Solid-state technologies, including MEMS-based and Optical Phased Array (OPA) LiDAR, offers greater reliability, fewer or no moving parts, improved form factors, and significantly lower manufacturing costs compared to traditional mechanical scanning systems. Leading innovators like Luminar and Innoviz are achieving detection ranges exceeding 250 meters while reducing costs below USD 1,000 per unit-critical thresholds for mass adoption across mainstream consumer vehicles. Hesai Technology achieved a landmark milestone by producing its 1,000,000th LiDAR unit in 2025, becoming the world's first LiDAR company to exceed one million units in annual production, with fully automated production lines capable of manufacturing one LiDAR every 20 seconds.

Restraint - Adoption of Alternative technologies

The growth of the automotive LiDAR market is significantly restrained by the adoption of alternative solutions like camera and radar technologies. Radar has become increasingly attractive to OEMs due to its cost-effectiveness, reliable performance in diverse weather conditions, and evolving capabilities. Unlike LiDAR, which struggles in rain, fog, or direct sunlight, radar remains dependable, making it essential for adaptive cruise control and collision avoidance. Innovations like Imaging Radar and PMCW radar have narrowed the performance gap with LiDAR, offering improved resolution, reduced noise, and detailed object detection.

This shift is reflected in OEM strategies. For example, in September 2024, Mobileye ceased LiDAR development to focus on imaging radar, while Argo AI discontinued its LiDAR projects in October 2022. Despite solid-state LiDAR becoming more affordable, radar’s operational advantages and lower costs continue to attract OEMs. As a result, radar has emerged as a strong alternative and competitor, challenging the widespread adoption of LiDAR in the automotive industry.

Opportunity - Automakers to Focus on LiDAR to Improve ADAS and Real-time Object Detection in EVs

Rapid expansion of the Electric Vehicle (EV) market presents a significant growth opportunity for automotive LiDAR manufacturers. As EV adoption accelerates, there is an increasing demand for advanced safety, navigation, and autonomous driving technologies, areas where LiDAR plays a key role. According to the International Energy Agency (IEA), nearly 14 million electric cars were sold in 2023, which was a 35% year-on-year increase, thereby bringing the global EV stock to 40 million. This surge reflects the rising prioritization of smart mobility solutions, particularly in key markets such as China (60% of global EV sales), Europe (25%), and the U.S. (10%).

Autonomous Robotaxi and Commercial Fleet Deployment

The emergence of autonomous robotaxi services and commercial fleet operations represents a high-value market segment driving premium LiDAR demand. Unlike consumer vehicles, where cost sensitivity constrains adoption, commercial autonomous operations prioritize reliability and performance, justifying higher sensor costs through improved safety and operational efficiency. Luminar Technologies expanded its business with two global automakers in November 2024, including a new advanced development contract with a major Japanese automaker for next-generation ADAS systems using Luminar's LiDAR and AI software capabilities. The company's next-generation Luminar Halo product, unveiled in 2024, is designed for mass adoption by mainstream consumer vehicles while meeting industry standards developed collaboratively with multiple leading global OEMs covering all use cases from advanced safety through full autonomy.

Category-wise Analysis

Vehicle Type Insights

The solid-state LiDAR segment is projected to dominate in 2026, holding a substantial automotive LiDAR market share of 54.2% share. The segment is projected to exhibit a leading CAGR throughout the forecast period. Solid-state LiDAR is rapidly emerging as the preferred choice for automotive manufacturers due to its superior durability, cost-effectiveness, and seamless integration capabilities. Unlike mechanical LiDAR systems that rely on rotating components, solid-state LiDAR eliminates moving parts, enhancing reliability and significantly reducing maintenance requirements. This design also lowers power consumption and manufacturing costs, making it an ideal solution for mass-market vehicle deployment.

Another key advantage of solid-state LiDAR is its compact size and resilience to vibrations, which allows for flexible placement in various vehicle architectures. While mechanical LiDARs provide a 360-degree field of view (FoV), their bulky, cylindrical design limits integration options. In contrast, solid-state LiDARs can be strategically positioned around the vehicle and their data can be fused to create an FoV comparable to mechanical systems.

In January 2024, RoboSense China unveiled the M2 and M3 solid-state LiDAR sensors at CES 2024, with the M3 offering long-range detection of up to 300 meters at 10% reflectivity and the M2 offering a range of 250 meters. Similarly, in April 2024, Hesai Group China launched the ATX solid-state LiDAR, which is 60% smaller and weighs less than half its predecessor.

Application Insights

Based on application, the ADAS segment will likely hold a share of 49.1% in 2026. LiDAR plays a key role in ADAS by enhancing vehicle safety and driving efficiency through various semi-autonomous functionalities. Novel ADAS features such as adaptive cruise control, AEB, lane-keeping assistance, and pedestrian detection rely on LiDAR’s ability to provide real-time, high-precision depth perception. This capability enables vehicles to detect obstacles, measure distances accurately, and react instantly to dynamic road conditions. As regulatory mandates for vehicle safety continue to evolve, demand for LiDAR-based ADAS solutions is estimated to surge, particularly in premium and electric vehicles.

Range Insights

Long Range (Above 150 meters) LiDAR systems command approximately 48% market share, driven by highway driving and autonomous vehicle requirements for extended forward visibility. Long-range detection enables 3-4 seconds of reaction time at highway speeds (100-120 km/h), critical for safe autonomous operation and advanced collision avoidance systems. Leading systems from Luminar, Innoviz, and Hesai achieve detection ranges exceeding 250 meters with angular resolution below 0.1 degrees, enabling identification of small objects including debris, pedestrians, and motorcycles at distances sufficient for planning lane changes and emergency maneuvers. RoboSense's digital LiDAR can precisely identify distant small objects like tires, traffic cones, and cartons, meeting China's MIIT mandatory standard requirements for 70.79-meter detection range with horizontal resolution below 0.2 degrees and vertical resolution below 0.68 degrees.

Vehicle Type Insights

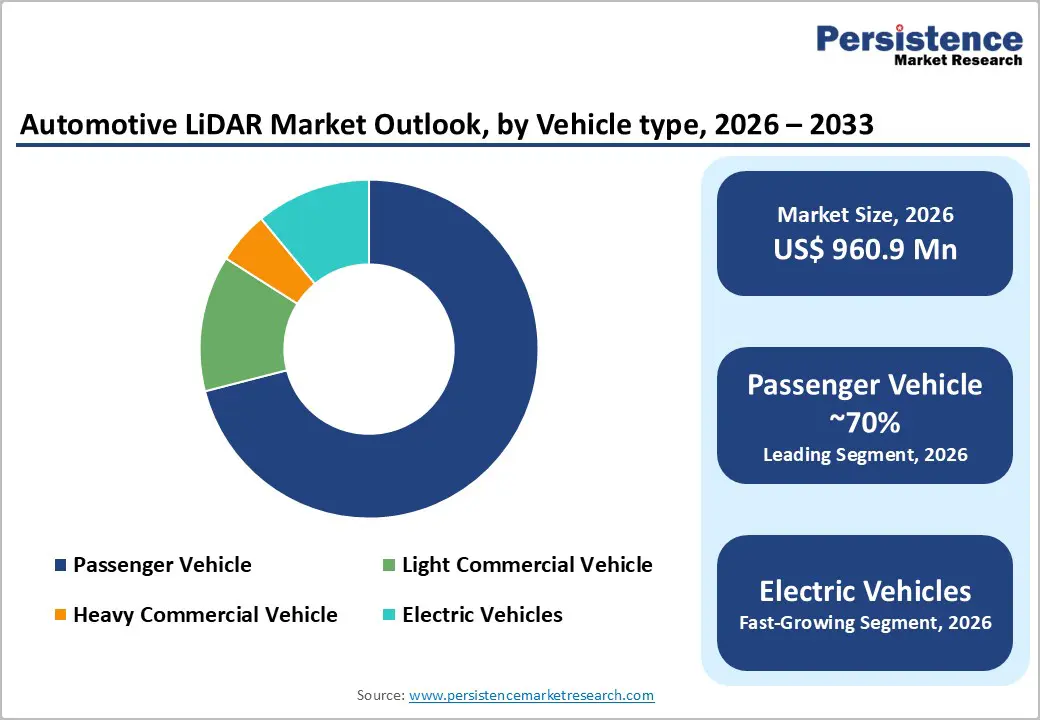

Passenger Vehicles dominate the vehicle type segment with approximately 71% market share, reflecting the segment's volume scale and consumer-driven technology adoption dynamics. Premium passenger car manufacturers including Mercedes-Benz, BMW, Volvo, and Audi have pioneered LiDAR integration in production vehicles, establishing consumer expectations for advanced safety and partial autonomy features. Chinese NEV (New Energy Vehicle) manufacturers are aggressively deploying LiDAR across mid-to-premium passenger car segments, with Li Auto, NIO, Xiaomi, and Zeekr standardizing the technology in vehicles priced above USD 30,000. According to S&P Global Mobility, global new car sales in 2025 are expected to reach 89.6 million units with production totalling 88.7 million units, creating substantial addressable market potential as LiDAR penetration increases from 6.0% in 2024 toward projected 15-20% by 2028.

Regional Insights and Trends

Asia Pacific Automotive LiDAR Market Trends

Asia Pacific is anticipated to account for a 55.3% in 2026. Demand for LiDAR technology is rapidly growing in the region, driven by increased domestic production, particularly in China, where manufacturers like RoboSense have strengthened their presence. This has led to reduced costs, making LiDAR more accessible to automakers.

Apart from China, other countries in Asia Pacific are also moving toward autonomous driving. Japan and South Korea, for instance, are preparing to introduce Level 3 self-driving vehicles. South Korea, starting in July, will allow automakers to sell vehicles with basic Level 3 self-driving capabilities, with companies like Hyundai, Kia, BMW, and Mercedes-Benz anticipated to launch such models. Such strategies are projected to create a high automotive LiDAR demand.

Europe Automotive LiDAR Market Trends

Europe is projected to register a 12.4% share in 2026. The region plays a significant role in accelerating LiDAR technology development and its integration into vehicles. Regulatory developments are shaping the market, with the European Union enforcing Regulation (EU) 2019/2144 to support automated vehicle deployment. Currently, Level 3 automated vehicles, which require a safety driver, are allowed on public roads. However, the EU is working toward enabling Level 4 autonomy by 2026. This aligns with Tesla’s timeline for introducing its Full Self-driving (FSD) technology. The EU has largely followed Germany’s regulatory approach, while the U.K. has introduced the Automated Vehicles Act 2024 to establish a robust safety framework, clarify legal liabilities, and protect consumers. The main challenge ahead is ensuring that existing regulations can support market-ready autonomous technologies on a scale.

North America Automotive LiDAR Market Trends

In North America, the U.S. automotive LiDAR market is projected to be a leading hub through 2033. Regulatory pressure is a significant factor propelling demand for automotive LiDAR in the U.S. The National Highway Traffic Safety Administration (NHTSA) is advocating strict requirements for ADAS, making LiDAR-based technologies important for car manufacturers.

In 2023, for instance, Mercedes-Benz’s Drive Pilot became the first Level 3 system to receive approval in the U.S., utilizing Luminar’s LiDAR technology for hands-free driving on highways. Additionally, states such as California and Arizona, which are at the forefront of autonomous vehicle testing, have authorized over 1,400 self-driving cars, many of which depend on LiDAR for their navigation systems.

Companies such as Waabi, Gatik, and LeddarTech are leading the way in autonomous freight transport, incorporating LiDAR technology into delivery trucks for retailers like Walmart and Loblaw. Additionally, the city of Ottawa has initiated a LiDAR-based smart road project, utilizing the technology for real-time traffic management and autonomous shuttle services.

Competitive Landscape

The competitive landscape is shaped by continuous technological developments, strategic collaborations, and the race to develop cost-effective and scalable solutions. Key players in the market focus on high-performance LiDAR sensors with improved range, resolution, and real-time perception capabilities. Integration of LiDAR into mass-production vehicles accelerates, particularly in electric and autonomous vehicle segments. Partnerships between LiDAR developers and leading automotive OEMs are becoming increasingly common, enabling wider adoption and innovation.

Key Developments:

- In 2025, Hesai Technology announced plans to deepen cooperation with BYD, providing LiDAR for more than 10 BYD models set for mass production in 2026. By this time, Hesai had already secured over 100 design wins across 22 automotive OEMs, including Chery, Great Wall Motors, and Changan.

- In 2025, Aeva and Torc extended their partnership to enhance the safety architecture of autonomous trucks. Aeva’s 4D LiDAR will be integrated into Torc’s Virtual Driver software to improve perception capabilities.

- In 2025, Aeva introduced Atlas Ultra, a next generation 4D LiDAR sensor designed for SAE Level 3 and 4 automated driving systems.

Companies Covered in Automotive LiDAR Market

- Luminar Technologies, Inc.

- RoboSense Technology Co., Ltd

- Ouster, Inc.

- Valeo

- Hesai Technology

- Continental AG

- Huawei Technologies Co., Ltd

- KOITO MANUFACTURING CO., LTD

- Seyond

- Leishen Intelligent System Co., Ltd

- Aeva Technologies

- Other Key Players

Frequently Asked Questions

The global Automotive LiDAR Market is projected to reach US$ 6,464.4 Mn by 2033, growing from US$ 960.9 Mn in 2026 at a CAGR of 31.3% during the forecast period, driven by autonomous vehicle development and mandatory ADAS integration.

The market is primarily driven by regulatory mandates including China's MIIT formally incorporating LiDAR into mandatory L2 ADAS standards in September 2025, coupled with technological advancements enabling cost reductions below USD 1,000 per unit and Hesai Technology achieving one million unit annual production in 2025.

Solid-state LiDAR dominates with approximately 58% market share, favored for superior reliability with 10+ year lifespans, compact form factors enabling seamless vehicle integration, and manufacturing costs declining toward USD 500 per unit at scale representing 60-70% cost reduction versus mechanical alternatives.

Asia Pacific leads the market with 55% share, driven by China's aggressive NEV deployment, MIIT's mandatory L2 ADAS standards, and domestic manufacturers Hesai and RoboSense achieving million-unit production scale with over 120 vehicle models across 24 OEMs for 2025 - 2027 production.

Key market players include Hesai Technology, achieving one million unit production in 2025, Luminar Technologies with OEM partnerships for next-generation ADAS, RoboSense Technology pioneering 1,080-channel digital LiDAR, Valeo, Continental AG, Ouster, and Innoviz Technologies, collectively controlling approximately 60-65% global market share.