- Executive Summary

- Global Automotive Infotainment and Navigation Market Snapshot, 2025 and 2032

- Market Opportunity Assessment, 2025 - 2032, US$ Bn

- Key Market Trends

- Future Market Projections

- Premium Market Insights

- Industry Developments and Key Market Events

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definition

- Market Dynamics

- Drivers

- Restraints

- Opportunity

- Challenges

- Key Trends

- COVID-19 Impact Analysis

- Forecast Factors - Relevance and Impact

- Value Added Insights

- Value Chain Analysis

- Key Market Players

- Regulatory Landscape

- PESTLE Analysis

- Porter’s Five Force Analysis

- Consumer Behavior Analysis

- Price Trend Analysis, 2019 - 2032

- Key Factors Impacting Product Prices

- Pricing Analysis, By Product Type

- Regional Prices and Product Preferences

- Global Automotive Infotainment and Navigation Market Outlook

- Market Size (US$ Bn) Analysis and Forecast

- Historical Market Size (US$ Bn) Analysis, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, 2025-2032

- Global Automotive Infotainment and Navigation Market Outlook: Product Type

- Historical Market Size (US$ Bn) Analysis, By Product Type, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Attractiveness Analysis: Product Type

- Global Automotive Infotainment and Navigation Market Outlook: Technology

- Historical Market Size (US$ Bn) Analysis, By Technology, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Attractiveness Analysis: Technology

- Global Automotive Infotainment and Navigation Market Outlook: Connectivity

- Historical Market Size (US$ Bn) Analysis, By Connectivity, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Attractiveness Analysis: Connectivity

- Global Automotive Infotainment and Navigation Market Outlook: End-use

- Historical Market Size (US$ Bn) Analysis, By End-use, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passengers Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis: End-use

- Global Automotive Infotainment and Navigation Market Outlook: Display Type

- Historical Market Size (US$ Bn) Analysis, By Display Type, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Attractiveness Analysis: Display Type

- Market Size (US$ Bn) Analysis and Forecast

- Global Automotive Infotainment and Navigation Market Outlook: Region

- Historical Market Size (US$ Bn) Analysis, By Region, 2019-2024

- Market Size (US$ Bn) Analysis and Forecast, By Region, 2025-2032

- North America

- Latin America

- Europe

- East Asia

- South Asia and Oceania

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- U.S.

- Canada

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Europe Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- Germany

- France

- U.K.

- Italy

- Spain

- Russia

- Rest of Europe

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- East Asia Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- China

- Japan

- South Korea

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- South Asia & Oceania Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- India

- Indonesia

- Thailand

- Singapore

- ANZ

- Rest of South Asia & Oceania

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Latin America Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- Brazil

- Mexico

- Rest of Latin America

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Middle East & Africa Automotive Infotainment and Navigation Market Outlook

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- By Country

- By Product Type

- By Technology

- By Display Type

- By Connectivity

- By End-use

- Market Size (US$ Bn) Analysis and Forecast, By Country, 2025-2032

- GCC Countries

- Egypt

- South Africa

- Northern Africa

- Rest of Middle East & Africa

- Market Size (US$ Bn) Analysis and Forecast, By Product Type, 2025-2032

- Standalone Systems

- Integrated Infotainment Systems

- Embedded Systems

- Portable Navigation Devices

- Market Size (US$ Bn) Analysis and Forecast, By Technology, 2025-2032

- Global Navigation Satellite System (GNSS)

- Radar Navigation

- Computer Vision

- Sensor Fusion

- Market Size (US$ Bn) Analysis and Forecast, By Display Type, 2025-2032

- Touchscreen Displays

- Head-Up Displays (HUD)

- Light Emitting Diode (LED) Displays

- Liquid Crystal Display

- Market Size (US$ Bn) Analysis and Forecast, By Connectivity, 2025-2032

- Bluetooth

- Wi-Fi

- Cellular Networks (4G/5G)

- Vehicle-to-Everything (V2X) Communication

- Market Size (US$ Bn) Analysis and Forecast, By End-use, 2025-2032

- Passenger Cars

- Commercial Vehicles

- Luxury Vehicles

- Electric Vehicles

- Market Attractiveness Analysis

- Historical Market Size (US$ Bn) Analysis, By Market, 2019-2024

- Competition Landscape

- Market Share Analysis, 2024

- Market Structure

- Competition Intensity Mapping By Market

- Competition Dashboard

- Company Profiles (Details - Overview, Financials, Strategy, Recent Developments)

- Robert Bosch GmbH

- Overview

- Segments and Product Type

- Key Financials

- Market Developments

- Market Strategy

- Continental AG

- Harman International

- Denso Corporation

- Panasonic Corporation

- Pioneer Corporation

- Alpine Electronics

- Garmin Ltd.

- Aptiv PLC

- Visteon Corporation

- LG Electronics

- Mitsubishi Electric Corporation

- TomTom International BV

- Others

- Robert Bosch GmbH

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

- Automotive Components & Materials

- Automotive Infotainment and Navigation Market

Automotive Infotainment and Navigation Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Automotive Infotainment and Navigation Market by Product Type (Standalone Systems, Integrated Infotainment Systems, Embedded Systems, Portable Navigation Devices), Technology (Global Navigation Satellite System [GNSS], Radar Navigation, Computer Vision, Sensor Fusion), Display Type, Connectivity, End-use, and Regional Analysis for 2025 - 2032

Automotive Infotainment and Navigation Market Size and Trends Analysis

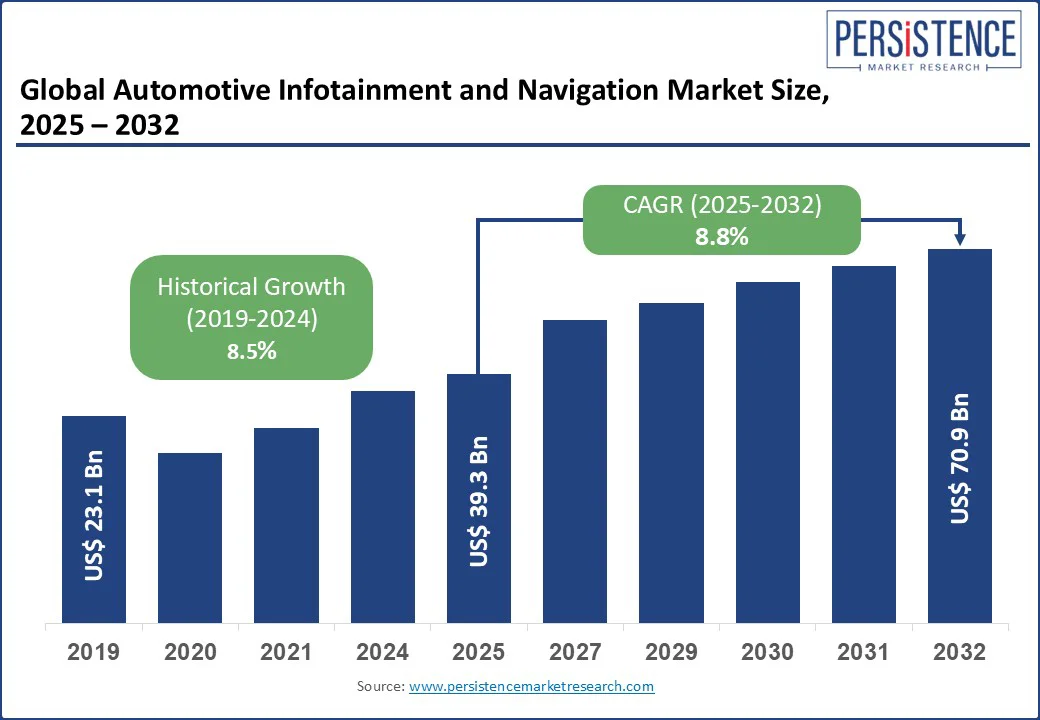

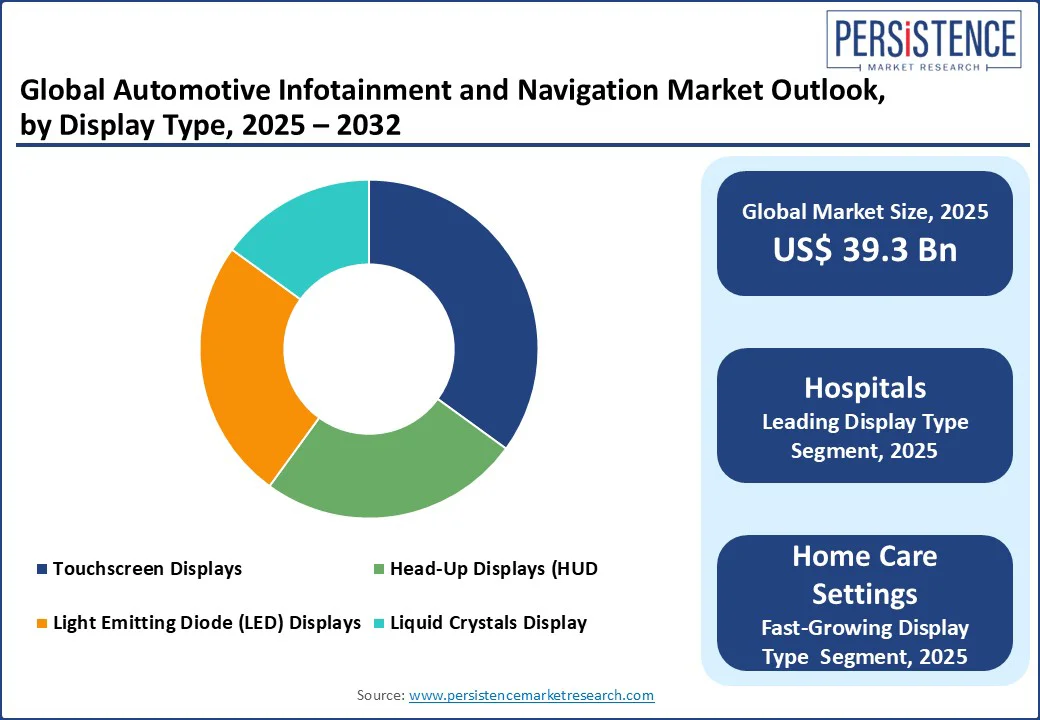

The global automotive infotainment and navigation market size is set for significant growth, with a projected market size of US$ 39.3 Bn in 2025, expected to reach US$70.9 Bn by 2032, at a robust CAGR of 8.8% during the forecast period 2025-2032

The automotive infotainment and navigation market is experiencing significant growth, driven by the rising demand for connected vehicles, advanced driver assistance systems (ADAS), and personalized in-car experiences. Modern cars are increasingly equipped with touchscreen displays, voice control, smartphone integration, and cloud-based services, transforming the driving experience into a digitally connected ecosystem.

Key Industry Highlights:

- Passenger Cars Lead: Passenger cars hold a 50% market share in 2025, driven by in-vehicle infotainment and automotive GPS.

- Integrated Systems Growth: Integrated Infotainment Systems are fueled by smart car infotainment.

- Cellular Networks Surge: Cellular Networks (4G/5G) is driven by connected vehicle platforms.

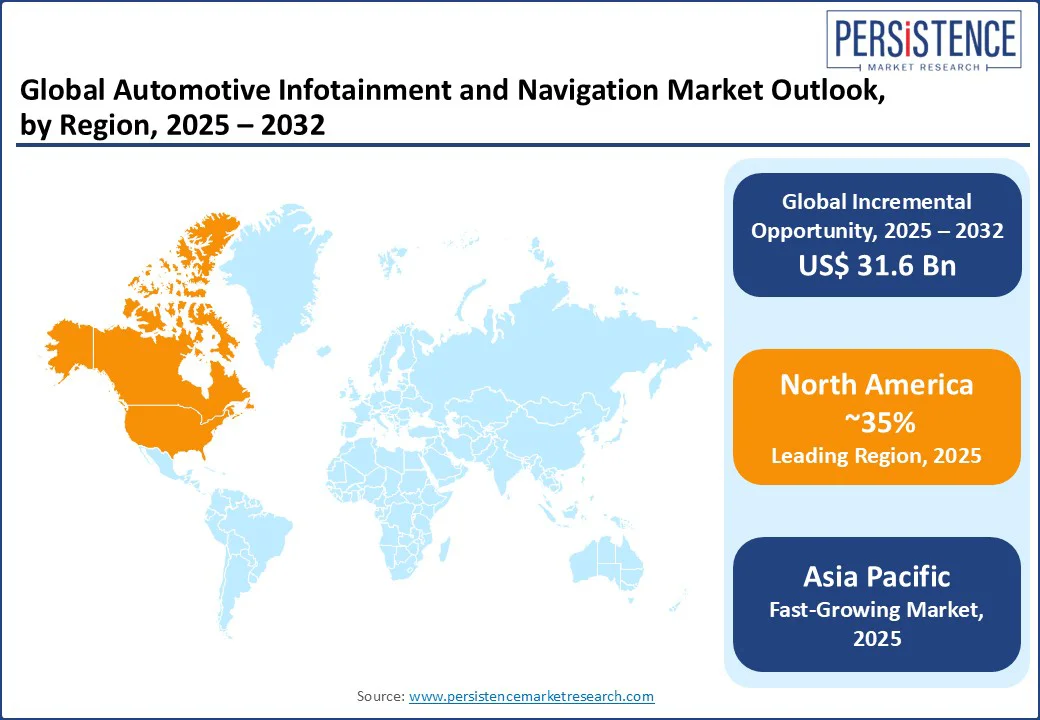

- Regional Dominance: North America commands a 35% market share, while Asia Pacific is the fastest growing with 20%.

- Innovation Impact: Voice-controlled car infotainment systems and cloud-based automotive navigation platforms boost automotive smart infotainment by 12% in 2025.

- Technology Adoption: Real-time traffic navigation systems drive 10% growth in telematics systems.

- Consumer Demand: Touchscreen infotainment for vehicles enhances digital dashboards by 15%.

|

Global Market Attribute |

Key Insights |

|

Automotive Infotainment and Navigation Market Size (2025E) |

US$39.3 Bn |

|

Market Value Forecast (2032F) |

US$70.9 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

8.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

8.5% |

Market Dynamics

Driver: Growing Demand for Connected and Autonomous Vehicles is Driving the Adoption of Advanced Infotainment and Navigation Systems

The automotive infotainment and navigation market is driven by the growing demand for connected and autonomous vehicles, which in turn boosts the adoption of in-vehicle infotainment, automotive GPS, and smart car infotainment. Globally, 30% of new vehicles in 2025 featured advanced driver-assistance systems (ADAS) requiring telematics systems, driving the need for voice-controlled car infotainment systems and cloud-based automotive navigation platforms.

Touchscreen infotainment for vehicles and digital dashboards enhance user experience, while GPS navigation devices and real-time traffic navigation systems support autonomous driving. Connected vehicle platforms with human-machine interface (HMI) in vehicles ensure seamless integration with automotive connectivity solutions, such as Vehicle-to-Everything (V2X) Communication.

The rise in OEM infotainment systems and navigation software aligns with consumer expectations for enhanced safety and connectivity, driving demand for car infotainment consoles and vehicle navigation technology in modern vehicles.

Restraint: High Development and Integration Costs Hindering the Market Development

The automotive infotainment and navigation market faces a significant restraint due to high development and integration costs, impacting the adoption of telematics systems and automotive smart infotainment. Developing advanced connected vehicle platforms and cloud-based automotive navigation platforms incurs costs exceeding US$500 Mn annually for major manufacturers, limiting scalability for smaller players.

The complexity of integrating human-machine interface (HMI) in vehicles, real-time traffic navigation systems, and vehicle navigation technology with existing vehicle architectures increases production costs, hindering the affordability of OEM infotainment systems and digital dashboards, particularly in price-sensitive markets.

Opportunity: Advancements in 5G and V2X Connectivity Enhancing Safety in the Market

Advancements in automotive connectivity solutions, particularly Cellular Networks (4G/5G) and Vehicle-to-Everything (V2X) Communication, present a significant opportunity for the Automotive Infotainment and Navigation Market. With 40% global adoption of 5G-enabled vehicles projected by 2025, there is growing demand for connected vehicle platforms and real-time traffic navigation systems.

These technologies enhance in-vehicle infotainment, voice-controlled car infotainment systems, and cloud-based automotive navigation platforms, supporting seamless data transfer and improved navigation accuracy. The rise in smart car infotainment and telematics systems aligns with global automotive technology trends, positioning the market for growth in connected and autonomous vehicle applications.

Category-wise Analysis

Product Type Insights

Integrated Infotainment Systems hold a 45% market share in 2025, driven by their seamless integration with in-vehicle infotainment and automotive GPS. With 50% adoption in passenger cars, these systems are favored for their car infotainment console and touchscreen infotainment, offering a unified user experience with navigation software. Their compatibility with Apple CarPlay, Android Auto, and cloud-based services enhances convenience and personalization, which consumers highly value

Embedded systems are fueled by demand for smart car infotainment in autonomous vehicles. With 12% growth in 2025, these systems support vehicle navigation technology and digital dashboards, driven by advancements in OEM infotainment systems. The increasing adoption of 5G connectivity, edge computing, and AI-driven analytics has further accelerated their relevance, enabling low-latency responses and over-the-air updates.

Technology Insights

GNSS commands a 50% market share in 2025, driven by its widespread use in automotive GPS and GPS navigation devices. With 55% adoption in 2025, GNSS supports real-time traffic navigation systems and cloud-based automotive navigation platforms for precise location tracking. With growing demand for integrated navigation in infotainment consoles and dependence on satellite-based navigation for rural and urban areas, GNSS remains the backbone of in-vehicle navigation systems.

Sensor fusion is fueled by its role in autonomous driving. With 11% growth in 2025, this technology integrates vehicle navigation technology with telematics systems, enhancing connected vehicle platforms. This capability is essential for autonomous driving, ADAS (Advanced Driver Assistance Systems), and next-generation connected vehicles, where safety and precision are non-negotiable.

Display Type Insights

Touchscreen displays hold a 55% market share in 2025, driven by touchscreen infotainment for vehicles and car infotainment consoles. With 60% adoption in 2025, these displays enhance human-machine interface (HMI) in vehicles and digital dashboards. They are widely adopted across passenger cars and premium vehicles, driven by the popularity of integrated infotainment systems that consolidate music, navigation, and communication into a single screen.

Head-Up Displays (HUD) fueled by demand for safety-focused vehicle navigation technology. With 10% growth in 2025, HUDs are adopted in luxury vehicles for real-time traffic navigation systems. The rapid growth of advanced driver assistance systems (ADAS), connected cars, and autonomous vehicle technologies is accelerating HUD adoption, as these systems require seamless and real-time information delivery.

Connectivity Insights

Bluetooth holds a 40% market share in 2025, driven by its widespread use in in-vehicle infotainment. With 45% adoption in 2025, Bluetooth supports voice-controlled car infotainment systems and connected vehicle platforms. Bluetooth technology is widely adopted due to its low power consumption, reliability, and ability to connect multiple devices simultaneously, making it ideal for infotainment systems.

Cellular networks (4G/5G) fueled by automotive connectivity solutions. With 15% growth in 2025, 5G enables cloud-based automotive navigation platforms and real-time traffic navigation systems. The rollout of 4G LTE and 5G networks has accelerated adoption, as these technologies provide low delays, ultra-fast speed, and high bandwidth, which enabling advanced features such as vehicle-to-some (V2X) communication, distant diagnosis, and increased security systems.

End-use Insights

Passenger Cars hold a 50% market share in 2025, driven by high vehicle ownership and demand for smart car infotainment. With 55% adoption in 2025, this segment relies on OEM infotainment systems and digital dashboards. The rise of connected vehicles, electric cars, and premium variants in mass-market segments has further boosted the adoption of sophisticated infotainment solutions.

Features such as voice assistants, real-time traffic updates, wireless charging, and OTA (Over-the-Air) updates are now becoming standard in mid-range and luxury passenger cars.

Electric vehicles are fueled by adoption. With 12% growth in 2025, this segment drives demand for telematics systems and cloud-based automotive navigation platforms. Dissimilar to conventional cars, EVs heavily rely on digital ecosystems for battery monitoring, energy optimization, route planning with charging station locators, and real-time software updates, making infotainment a critical component.

Regional Insights

North America Automotive Infotainment and Navigation Market Trends

North America holds a 35% global market share in 2025, with the U.S. leading due to its advanced automotive industry, generating US$ 13.76 Bn in sales in 2025. The U.S. market growth is recorded at a CAGR of 8.6%, driven by demand for in-vehicle infotainment and automotive GPS, with 70% of passenger cars using touchscreen infotainment for vehicles in 2025.

Key drivers include a 25% increase in connected vehicle sales, boosting connected vehicle platforms and real-time traffic navigation systems. Harman International and Garmin Ltd. drive 25% of regional revenue, with voice-controlled car infotainment systems seeing 10% growth. The focus on autonomous driving fuels telematics systems and digital dashboards.

Europe Automotive Infotainment and Navigation Market Trends

Europe accounts for a 30% global share, led by Germany, the UK, and France. Germany’s market grows at a CAGR of 8.5%, driven by its automotive manufacturing hub, with 60% of vehicles using OEM infotainment systems in 2025. The UK’s market is propelled by cloud-based automotive navigation platforms, with retail chains such as BMW adopting digital dashboards.

France sees 12% growth in vehicle navigation technology, driven by demand for human-machine interface (HMI) in vehicles. EU investments, with €200 Mn in connected vehicle technologies in 2025, boost automotive connectivity solutions. Continental AG holds a 10% market share, leveraging real-time traffic navigation systems.

Asia Pacific Automotive Infotainment and Navigation Market Trends

Asia Pacific is the fastest-growing region, with a CAGR of 9.3%, led by China, Japan, and India. China holds a 45% regional market share, driven by a 20% increase in vehicle production in 2025, boosting in-vehicle infotainment and automotive GPS.

India’s market is fueled by rising vehicle ownership, with 75% of urban vehicles using touchscreen infotainment for vehicles in 2025. Japan’s telematics systems drive 10% growth in connected vehicle platforms, supported by its advanced automotive sector. Denso Corporation and Panasonic Corporation lead, supported by US$ 5 Bn in automotive tech investments by 2030, enhancing smart car infotainment.

Competitive Landscape

The global automotive infotainment and navigation market is highly competitive, with automotive technology companies focusing on innovation, connectivity, and user experience. Robert Bosch GmbH and Continental AG lead in OEM infotainment systems, while Harman International excels in voice-controlled car infotainment systems.

Telematics systems, connected vehicle platforms, and real-time traffic navigation systems drive competition. Strategic partnerships and R&D investments in automotive smart infotainment and cloud-based automotive navigation platforms are key differentiators, addressing consumer and autonomous driving needs.

Key Industry Developments

- In January 2025- u-blox launched its first automotive-grade Wi-Fi 7 module, enabling OEMs to enhance the user experience of in-vehicle infotainment and telematics. The RUBY-W2 brings multiple benefits of Wi-Fi 7 to the automotive market, including higher throughput, support for more concurrent users, and lower latency, resulting in better network availability and user experience for various in-vehicle applications.

- In November 2024, Skyworks Solutions, Inc. (Nasdaq: SWKS) achieved IATF 16949 automotive certification at its facilities in Newbury Park, Calif. Skyworks is a major global supplier of high-performance, analog, and mixed-signal solutions for the automotive industry, with its RF front-end modules for V2X, in-vehicle infotainment, keyless entry, satellite navigation, and 5G automotive telematics.

- In January 2023, The NIA (New India Assurance) allowed insurance companies to launch telematics-based motor insurance cover, named “Pay as You Drive". This allowed vehicle owners to control and reduce their spending on insurance. This policy features coverage beyond distance limits, roadside help, and advanced protection.

Companies Covered in Automotive Infotainment and Navigation Market

- Robert Bosch GmbH

- Continental AG

- Harman International

- Denso Corporation

- Panasonic Corporation

- Pioneer Corporation

- Alpine Electronics

- Garmin Ltd.

- Aptiv PLC

- Visteon Corporation

- LG Electronics

- Mitsubishi Electric Corporation

- TomTom International BV

- Others

Frequently Asked Questions

The automotive infotainment and navigation market is projected to reach US$ 39.3 Bn in 2025, driven by in-vehicle infotainment and automotive GPS.

The demand for connected vehicles, with 30% of new vehicles featuring ADAS in 2025, drives smart car infotainment.

The automotive infotainment and navigation market grows at a CAGR of 8.8% from 2025 to 2032, reaching US$ 70.9 Bn by 2032.

Cellular Networks (4G/5G), with 40% adoption in 2025, offer opportunities for connected vehicle platforms.

Key players include Robert Bosch GmbH, Continental AG, Harman International, and Garmin Ltd.