- Automotive Components & Materials

- Automotive Decorative Film Market

Automotive Decorative Film Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Decorative Film Market by Material Type (Metallic, Ceramic, Others), Vehicle (Passenger Vehicle, LCV (Low Commercial Vehicle), HCV (High Commercial Vehicle)), Film (Vinyl Films, Polyester Films, TPU (Thermoplastic Polyurethane) Films, Metalized Films, Textured Films), and Regional Analysis for 2025 - 2032

Automotive Decorative Film Market Size and Trends Analysis

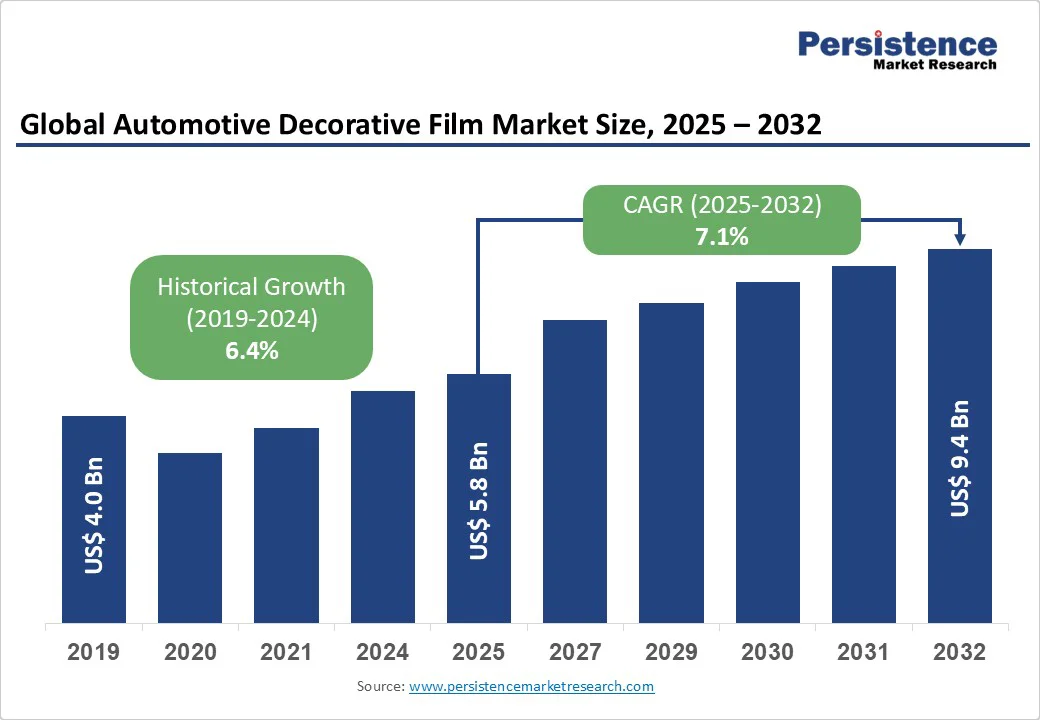

The global automotive decorative film market size is expected to be valued at US$5.8 billion in 2025. It is projected to reach US$9.4 billion by 2032, registering a CAGR of 7.1% during the forecast period from 2025 to 2032. The industry has experienced robust growth, driven by the rising demand for vehicle customization, advancements in film technologies, and the increasing need for aesthetic enhancements and protective solutions.

Key Industry Highlights:

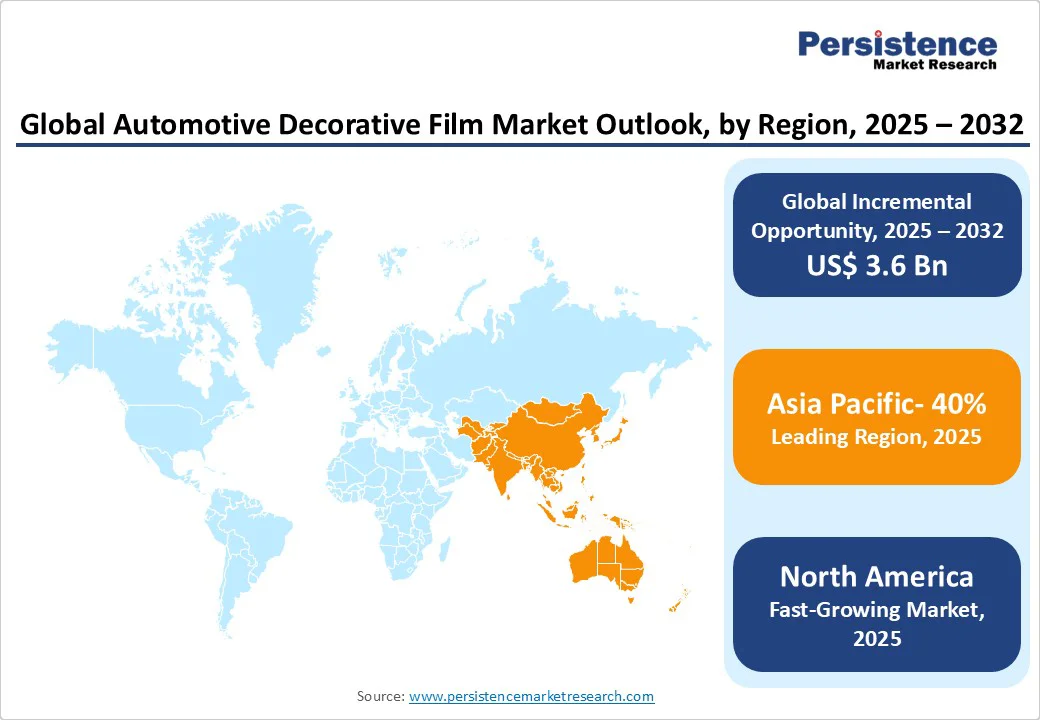

- Leading Region: Asia Pacific holds a 40% market share in 2025, driven by extensive vehicle production, rising consumer demand for stylish upgrades, and expanding aftermarket services in China, India, and Japan.

- Fastest-growing Region: North America, propelled by increasing customization trends, advanced automotive infrastructure, and growing adoption of innovative film technologies in the U.S. and Canada.

- Dominant Material Type: Metallic accounts for approximately 55% of the automotive decorative film market share in 2025, driven by its durability and visual appeal.

- Leading Vehicle Type: Passenger Vehicle accounts for approximately 65% of the automotive decorative film market share in 2025, driven by its high volume in personalization trends.

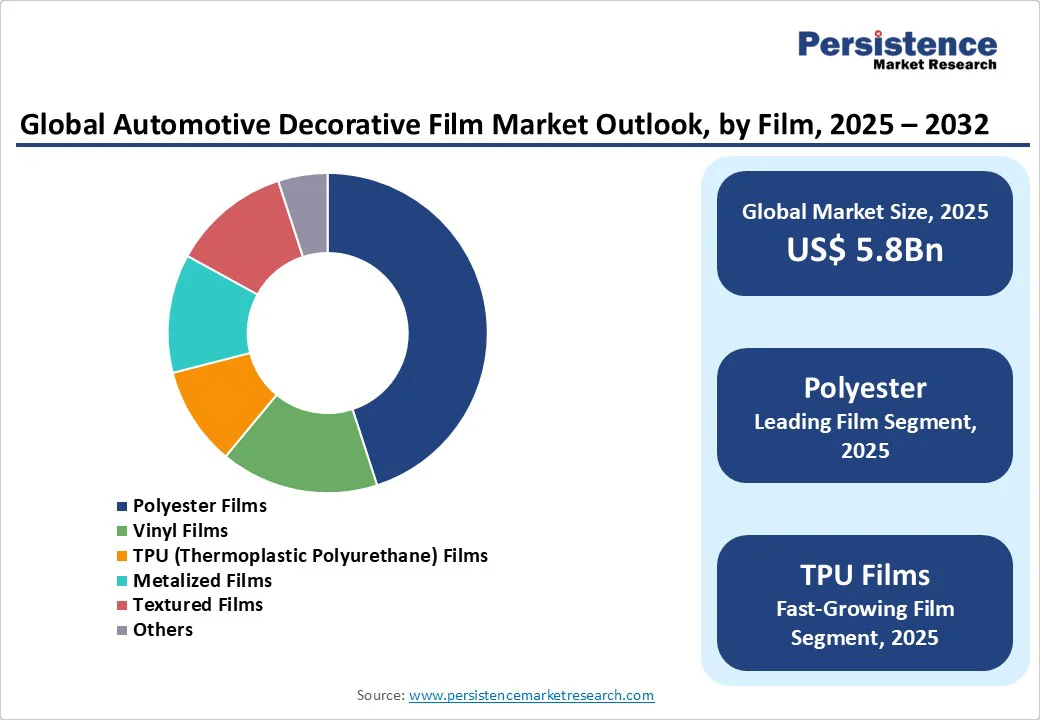

- Leading Film Type: Polyester Films accounts for approximately 45% of market share in 2025, driven by its versatility in applications.

| Key Insights | Details |

|---|---|

|

Automotive Decorative Film Market Size (2025E) |

US$5.8 Bn |

|

Market Value Forecast (2032F) |

US$9.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.4% |

Market Dynamics

Driver - Rising Vehicle Customization and Aesthetic Demands Fuel Market Growth

The global surge in vehicle customization and aesthetic demands is a primary driver of the automotive decorative film market. According to the International Organization of Motor Vehicle Manufacturers (OICA), global vehicle production reached 80 million units in 2024, with a significant portion driven by consumer preferences for personalization, where decorative films play a critical role in enhancing visual appeal and brand identity. This demand is particularly strong in the Asia Pacific, where urban mobility and rising disposable incomes drive the need for metallic finishes, UV protection, and scratch resistance for exterior and interior enhancements.

The aftermarket industry is increasingly adopting advanced films with anti-glare and color-shifting effects, driving innovation. Consumers prefer premium finishes over basic ones for vehicle wraps and trims, with a 2024 survey showing 68% of buyers prioritize aesthetic upgrades. Aftermarket applications benefit from films’ durability, preserving vehicle value and enabling quick style changes, supporting steady growth. In North America, rising disposable incomes (U.S. per capita income reached $81,000 in 2024) have boosted demand for luxury upgrades. Advancements in nano-coating and self-healing films have improved application efficiency, making them more accessible for mass-market use and fueling growth.

Restraint - Durability Concerns and Performance Limitations Impact Market Growth

The automotive decorative film market faces a significant restraint due to concerns regarding durability and long-term performance. While these films are designed to enhance vehicle aesthetics and provide protective benefits, they are often subject to harsh environmental conditions such as prolonged UV exposure, extreme temperature fluctuations, humidity, and road debris. Over time, these factors can lead to issues like fading, discoloration, bubbling, or peeling, undermining the visual appeal and protective function of the films. Such limitations raise concerns among consumers about product longevity and return on investment, particularly when compared to alternative solutions such as automotive paint coatings.

The performance of decorative films can vary based on material composition and installation quality, further impacting customer satisfaction. For premium vehicles, where aesthetics and durability are critical, any compromise in performance creates hesitation among buyers and OEMs to adopt these solutions widely. These challenges are amplified in emerging markets where extreme climatic conditions are common, intensifying wear and tear. Together, durability-related concerns limit consumer confidence, slow adoption rates, and act as a restraint on the overall market growth potential.

Opportunity - Technological Advancements in Smart and Functional Films Open New Avenues

The automotive decorative film market is increasingly benefitting from advancements in smart and functional film technologies, which present lucrative growth opportunities. Modern films are no longer limited to aesthetic enhancement but are being engineered with multifunctional capabilities such as UV resistance, anti-glare properties, self-healing surfaces, and thermal insulation. These innovations not only improve vehicle appearance but also enhance performance and passenger comfort, making them highly attractive for OEMs and end users alike.

The integration of nanotechnology and advanced coatings allows decorative films to deliver greater durability, scratch resistance, and weather adaptability, extending product lifecycles and reducing maintenance requirements. As electric vehicles and connected cars gain traction globally, manufacturers are exploring decorative films that align with lightweight design goals and energy efficiency standards, replacing heavier paint applications.

Category Analysis

Material Type Insights

The global automotive decorative film market is segmented into metallic, ceramic, and others. Metallic accounts for nearly 55% share in 2025, driven by its cost-effectiveness, reliable reflectivity for industrial applications, and broad acceptance across wraps, trims, and interior enhancements.

Ceramic represents the fastest-growing segment, fueled by rising consumer preference for heat-rejecting, non-metallic options and sustainable products. Its expanding adoption in luxury vehicles and protective films highlights the shift toward performance-oriented and premium-quality customization solutions.

Vehicle Insights

The automotive decorative film market is segmented into passenger vehicles, LCVs and HCVs. Passenger vehicle leads with nearly 65% of market share in 2025, attributed to superior volume in consumer markets, cost-efficient upgrades, and flexibility in personalization, making it highly suitable for wraps, window tints, and dashboard films.

HCV is the fastest-growing segment, supported by its fleet management benefits in commercial branding and durability needs. Increasing demand for cost-saving, long-lasting decorative solutions in logistics further drives adoption, positioning HCV films as a key growth contributor.

Film Insights

The automotive decorative film market is segmented into vinyl films, polyester films, TPU films, metalized films, and textured films. Polyester films lead with a 45% share in 2025, driven by their widespread use in window and protective applications.

TPU films are the fastest-growing segments, driven by rising consumer demand for self-healing and flexible solutions. Their strong appeal lies in impact resistance and aesthetic versatility, making them a preferred choice in premium vehicle customizations and aftermarket formulations.

Regional Insights

North America Automotive Decorative Film Market Trends

North America is positioned as the fastest-growing region in the global automotive decorative film market, supported by rising consumer awareness of vehicle customization and advancements in innovative aesthetic solutions. In the U.S., passenger vehicles account for the majority of demand, as decorative films are highly valued for their ability to provide UV protection, enhance style, and support aftermarket upgrades. Consumers are increasingly attentive to maintaining vehicle resale value and safeguarding against environmental exposure, which drives steady adoption of these films.

The market growth is further supported by higher levels of disposable income, enabling more buyers to invest in premium finishes and customization. Sustainability is another key driver, with eco-friendly decorative films gaining traction under the influence of EPA regulations promoting low-VOC materials. Accessibility has also improved, with retail partnerships involving auto accessory chains and e-commerce platforms expanding product availability to a wider consumer base. In Canada, growing interest in fleet customization and premium decorative finishes further accelerates regional expansion and strengthens market potential.

Europe Automotive Decorative Film Market Trends

Europe maintains a significant position in the global automotive decorative film market, with Germany, France, and the UK emerging as the primary contributors to regional growth. Germany leads the industry, supported by its extensive automotive manufacturing, which ensures consistent demand from the country’s robust OEM and aftermarket sectors. This advantage has enabled Germany to drive innovation in TPU and textured applications, while also aligning with the European Union’s strong emphasis on eco-friendly materials and emission reductions.

France follows closely, with rising consumer interest in luxury personalization strengthening market for metallic and vinyl films. The country’s growing demand for urban mobility solutions further supports its position as a key growth hub. The UK contributes significantly as well, with multi-application use of decorative films across LCV and HCV categories. The country’s focus on aesthetic trends and vehicle protection in variable weather drives adoption and highlights its role in the regional market landscape.

Asia Pacific Automotive Decorative Film Market Trends

Asia Pacific is a dominating market supported by extensive vehicle production and rising consumer demand for aesthetic upgrades. The region’s leadership is reinforced by strong automotive manufacturing bases and a rapidly expanding middle class that increasingly values vehicle personalization. In China, the world’s largest automotive market, demand for exterior wraps and interior films is surging as consumers seek stylish and protective finishes. India is witnessing remarkable momentum, driven by growing awareness of affordable customizations and strong sales of two-wheelers and passenger vehicles, which are prime segments for decorative film adoption.

Japan contributes significantly through its technologically advanced market, where precision-engineered vehicles drive demand for high-performance ceramic and smart films. Additionally, the region’s robust aftermarket sector, along with strong OEM integration, ensures continuous adoption of decorative films across both luxury and mass-market segments. Together, these factors solidify Asia Pacific’s dominance and reinforce its role as the primary hub for growth in the global automotive decorative film industry.

Competitive Landscape

The global automotive decorative film market is highly competitive, with global and regional players striving for an advantage through product innovation, sustainable practices, and cost efficiency. Strategic mergers, partnerships, and timely regulatory approvals serve as crucial differentiators, enabling companies to strengthen market presence and expand applications.

Key Developments:

- January 2024: Garware Hi-Tech Films launched coloured Paint Protection Films (PPF) and Head & Tail Light Glass Protection Films in India. These products are offered through new retail finance partnerships, increasing accessibility and enabling premium protection for vehicle exteriors and light assemblies.

- June 2024: Dai Nippon Printing (DNP) developed a mass-production technique for eco-friendly decorative films for automobile interiors using a polypropylene (PP) base. The film delivers high design quality and physical performance while improving recyclability compared to conventional materials.

Companies Covered in Automotive Decorative Film Market

- Eastman

- 3M

- Solar Gard-Saint Gobain

- Madico

- Johnson

- Hanita Coating

- Haverkamp

- Sekisui S-Lec America

- Garware SunControl

- Wintech

- Erickson International

- KDX Optical Material

Frequently Asked Questions

The automotive decorative film market is projected to reach US$5.8 Bn in 2025.

Rising customization trends, technological advancements in films, and consumer preferences for aesthetics are key drivers.

The automotive decorative film market is poised to witness a CAGR of 7.1% from 2025 to 2032.

Innovations in sustainable materials and multi-vehicle applications present significant growth opportunities.

Eastman, 3M, and Solar Gard-Saint Gobain are among the leading players.