- Medical Devices

- Automated Suturing Devices Market

Automated Suturing Devices Market Size, Trends, Share, Growth, and Regional Forecast, 2026 to 2033

Automated Suturing Devices Market by Product (Disposable and Reusable), by Application (Cardiac Surgery, Orthopedic, Gastrointestinal, Ophthalmic, Dental, Gynecological, and Others), End-user (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Others), and Regional Analysis from 2026 to 2033

Automated Suturing Devices Market Share and Trends Analysis

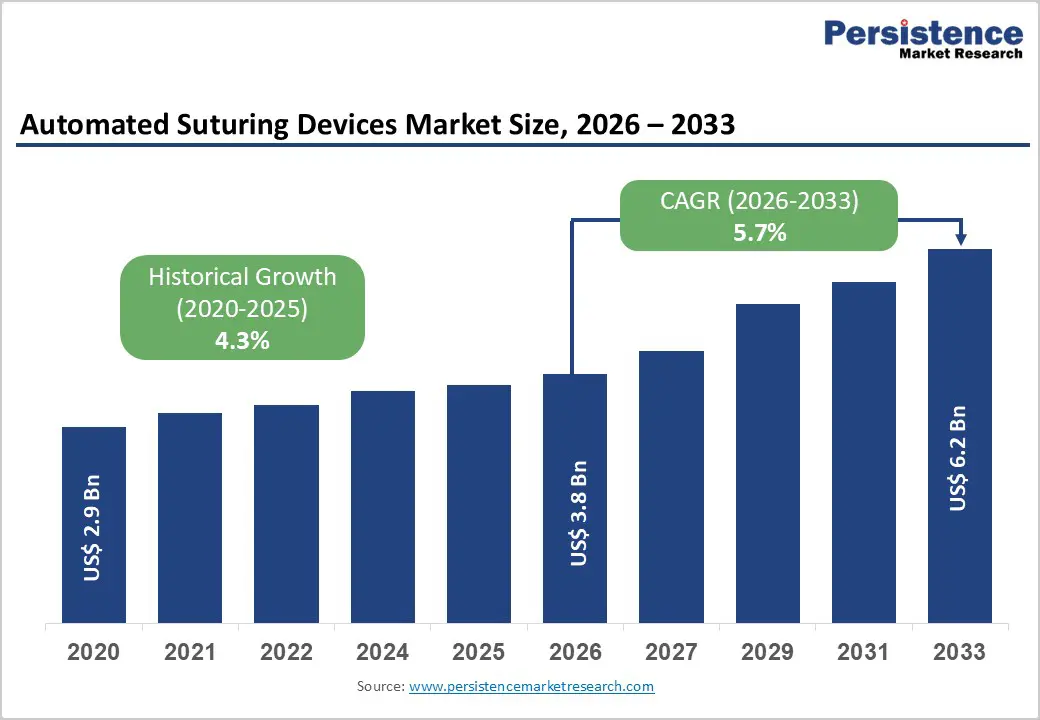

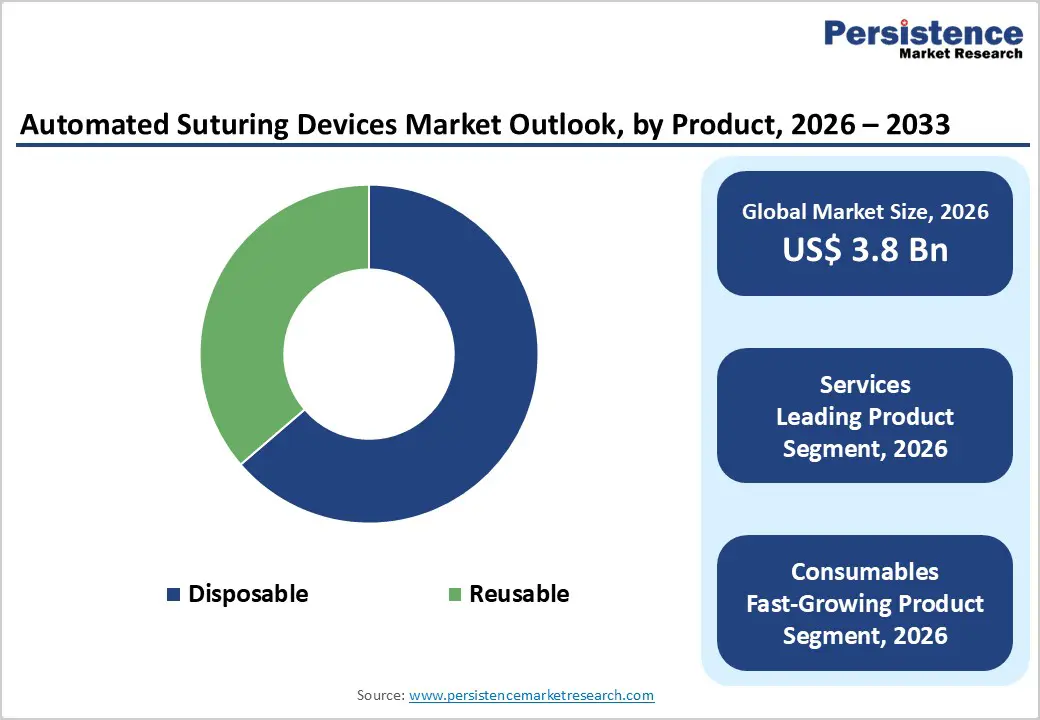

The global automated suturing devices market size is estimated to grow from US$ 3.8 billion in 2026 to US$ 6.2 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033.

Global demand for automated suturing devices is rising steadily, driven by increasing surgical volumes across cardiac, gastrointestinal, orthopedic, gynecological, and general surgery specialties. The growing prevalence of chronic diseases, trauma cases, and age-related conditions requiring surgical intervention is accelerating adoption.

The rise in penetration of minimally invasive and robotic-assisted procedures is further strengthening market expansion, as these approaches demand precise, consistent, and time-efficient wound closure solutions. Technological advancements such as motorized suturing mechanisms, controlled tension regulation, ergonomic handheld designs, and compatibility with laparoscopic and robotic platforms are improving procedural accuracy and reducing surgeon fatigue. The shift toward disposable, single-use suturing devices is gaining momentum due to heightened infection-control requirements, reduced reprocessing burden, and improved operating room efficiency. Additionally, expanding ambulatory surgical centers, favorable reimbursement structures for advanced surgical technologies, and increasing access to modern surgical infrastructure across emerging markets continue to support sustained market growth.

Key Industry Highlights:

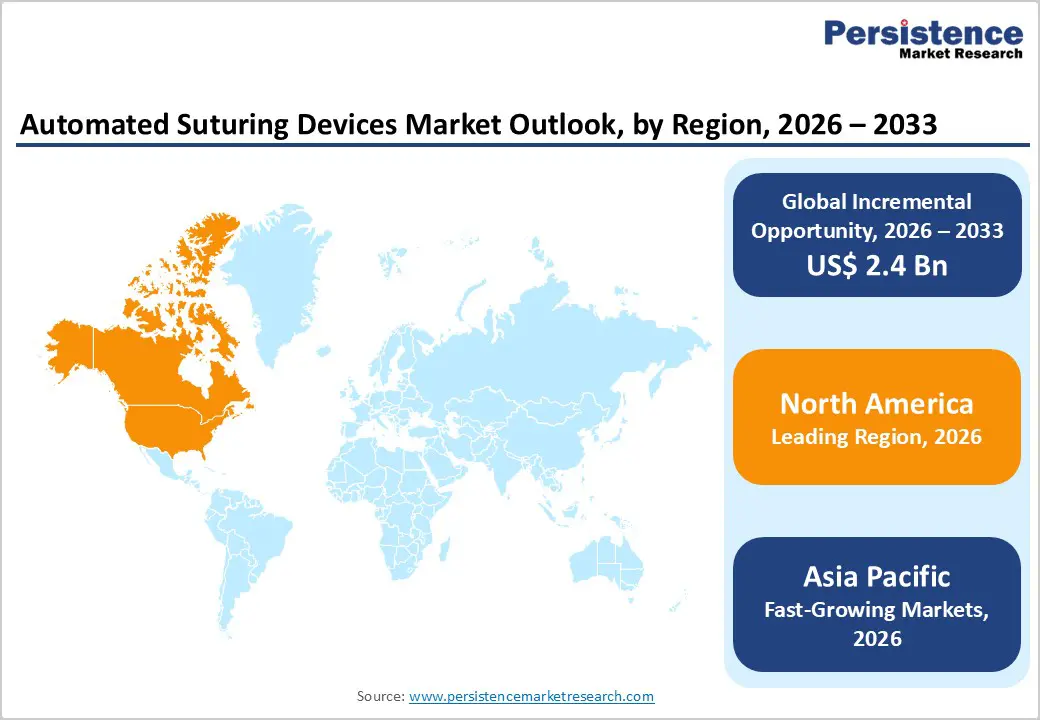

- Leading Region: North America holds the largest share at 45.8%, supported by high surgical procedure volumes, advanced hospital infrastructure, rapid adoption of minimally invasive and robotic-assisted surgeries, and strong reimbursement frameworks.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace, driven by rising surgical demand, improving healthcare infrastructure, growing surgeon workforce, and increasing availability of cost-efficient automated suturing systems.

- Leading Product Segment: Disposable dominate the market due to improved infection control, workflow efficiency, and strong clinical preference in high-volume surgical settings.

- Fastest-Growing Product Segment: Reusable are expanding the fastest owing to lower long-term cost advantages, durability, and increasing use in routine and short-duration surgical procedures.

- Leading Application Segment: Cardiac surgery leads globally due to high procedure complexity, need for rapid and secure tissue closure, and increasing volumes of cardiovascular surgeries.

- Fastest-Growing Application Segment: Gastrointestinal is scaling rapidly as minimally invasive abdominal surgeries and laparoscopic interventions become more widespread.

| Key Insights | Details |

|---|---|

| Automated Suturing Devices Market Size (2026E) | US$ 3.8 Bn |

| Market Value Forecast (2033F) | US$ 6.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver: Rising Surgical Volumes and Increasing Adoption of Minimally Invasive and Robotic-Assisted Procedures

The global automated suturing devices market is primarily driven by the rising volume of surgical procedures across cardiac, gastrointestinal, orthopedic, gynecological, and general surgery specialties. An aging global population, coupled with increasing prevalence of chronic diseases such as cardiovascular disorders, obesity-related conditions, and degenerative musculoskeletal diseases, is contributing to higher surgical intervention rates. Automated suturing devices address critical intraoperative challenges by enabling faster wound closure, consistent stitch placement, and reduced surgeon fatigue, particularly in complex and lengthy procedures.

The growing shift toward minimally invasive and robotic-assisted surgeries is further accelerating adoption. These procedures demand high precision, reproducibility, and ergonomic efficiency—areas where automated suturing devices offer clear advantages over manual suturing. Reduced operating time, lower blood loss, and improved procedural standardization are key clinical benefits driving surgeon preference. Additionally, hospitals are under increasing pressure to improve operating room efficiency and patient throughput while maintaining quality outcomes. Automated suturing systems support these goals by minimizing variability and shortening closure times. Expanding access to advanced surgical technologies, improved surgeon training, and favorable reimbursement coverage for minimally invasive procedures continue to sustain long-term market growth.

Restraints: High Device Costs, Training Requirements, and Limited Adoption in Resource-Constrained Settings

The automated suturing devices market faces notable restraints related to cost, training, and adoption barriers. Automated suturing systems particularly advanced disposable and motorized platforms—are associated with higher upfront and per-procedure costs compared to conventional manual sutures. These costs can limit adoption in budget-constrained hospitals, public healthcare systems, and low- and middle-income regions where surgical cost containment remains a priority. Additionally, successful integration of automated suturing devices requires surgeon training and procedural familiarity. Resistance to change among experienced surgeons accustomed to manual techniques can slow adoption, particularly in institutions lacking structured training programs.

Inadequate exposure during residency and limited hands-on training opportunities may further delay widespread acceptance. From a regulatory perspective, automated suturing devices must meet stringent safety, performance, and biocompatibility standards, increasing development timelines and compliance costs for manufacturers. Hospitals may also face procurement hurdles related to value-based purchasing and cost-justification requirements. Concerns regarding device reliability, compatibility with existing surgical workflows, and limited long-term outcome data in certain applications can further restrain uptake, especially in conservative or risk-averse healthcare environments.

Opportunity: Expansion of Disposable Platforms, Ambulatory Surgery Centers, and Next-Generation Suturing Technologies

The growing shift toward disposable automated suturing devices represents a significant opportunity for market expansion. Heightened focus on infection prevention, sterilization efficiency, and operating room turnover is driving demand for single-use suturing systems, particularly in high-volume surgical settings. Ambulatory surgical centers (ASCs) are emerging as a major growth avenue, as they prioritize compact, easy-to-use devices that enhance procedural efficiency and support same-day discharge models.

Technological innovation further strengthens market opportunity. Advances in motorized actuation, adjustable tension control, ergonomic design, and integration with laparoscopic and robotic platforms are improving clinical performance and expanding application scope. Manufacturers are also developing next-generation devices with enhanced precision, reduced learning curves, and compatibility across multiple surgical specialties, increasing addressable market potential. Emerging markets present additional growth opportunities due to improving healthcare infrastructure, rising surgical awareness, and expanding access to minimally invasive procedures. Strategic partnerships, cost-optimized product lines, and surgeon education initiatives can accelerate penetration in these regions. As healthcare systems increasingly prioritize efficiency, safety, and standardized outcomes, automated suturing devices are well-positioned to gain broader adoption across global surgical ecosystems.

Category Wise Analysis

By Product Insights

The disposable segment is projected to dominate the global automated suturing devices market in 2026, accounting for a revenue share of 63.7%. This dominance is primarily driven by increasing emphasis on infection prevention, cross-contamination control, and compliance with stringent hospital sterilization protocols. Disposable automated suturing devices eliminate the need for reprocessing, reduce turnaround time between procedures, and ensure consistent device performance, making them highly preferred in high-volume surgical environments. Their growing adoption is further supported by the rapid expansion of minimally invasive and robotic-assisted surgeries, where single-use precision instruments enhance procedural efficiency. Advancements in ergonomic design, preloaded suture cartridges, and standardized stitch quality are improving surgeon confidence and reducing intraoperative variability. Additionally, rising outpatient surgical volumes and the proliferation of ambulatory surgical centers are accelerating demand for disposable formats, supported by favorable reimbursement structures and cost-benefit advantages related to reduced postoperative complications and shorter operating room times.

By Application, Cardiac Surgery Dominates Owing to High Procedure Complexity and Precision Requirements

The cardiac surgery segment is projected to dominate the global automated suturing devices market in 2026, accounting for a revenue share of 24.6%, driven by the high complexity and precision demands associated with cardiovascular surgical procedures. Cardiac surgeries require rapid, consistent, and secure tissue closure to minimize bleeding risks, reduce operative time, and improve patient outcomes. Automated suturing devices offer controlled stitch placement, uniform tension, and reduced manual fatigue, making them particularly valuable in open and minimally invasive cardiac procedures. Increasing volumes of coronary artery bypass grafting (CABG), valve repair and replacement surgeries, and congenital heart defect corrections are contributing to sustained demand. The growing adoption of minimally invasive cardiac surgery and robotic-assisted platforms further supports segment leadership, as automated suturing devices integrate seamlessly with advanced surgical workflows. Additionally, an aging global population and rising prevalence of cardiovascular diseases are driving higher surgical intervention rates, reinforcing the cardiac segment’s dominant position.

By End-user Insights

The hospitals segment is projected to dominate the global automated suturing devices market in 2026, accounting for a revenue share of 56.8%. This dominance is attributed to high surgical volumes across multiple specialties, including cardiac, gastrointestinal, orthopedic, and gynecological procedures. Hospitals are primary centers for complex and high-risk surgeries that demand advanced suturing precision, robust infrastructure, and access to skilled surgical teams. The presence of well-equipped operating rooms, integration of robotic-assisted surgery systems, and availability of capital budgets enable hospitals to adopt advanced automated suturing technologies more rapidly than other end-users. Additionally, hospitals benefit from strong reimbursement coverage for inpatient surgical procedures and standardized procurement processes that support bulk purchasing of disposable suturing devices. Continuous investments in surgical efficiency, reduced operating room time, and improved patient outcomes are further driving adoption. Teaching hospitals and tertiary care centers also play a key role in surgeon training and early technology adoption.

Regional Insights

North America Automated Suturing Devices Market Trends

The North America automated suturing devices market is expected to dominate globally with a value share of 45.8% in 2026, led primarily by the United States. The region benefits from a highly advanced surgical ecosystem, widespread adoption of minimally invasive and robotic-assisted procedures, and strong penetration of automated surgical technologies across hospitals and ambulatory surgical centers. High procedural volumes in cardiac, gastrointestinal, and orthopedic surgeries, combined with a growing aging population and rising prevalence of chronic diseases, continue to drive demand.

The U.S. healthcare system demonstrates rapid uptake of next-generation disposable suturing devices, ergonomic motorized platforms, and precision-controlled stitching systems that improve workflow efficiency and reduce operative time. Strong reimbursement frameworks, favorable coverage policies for advanced surgical tools, and high surgeon awareness further support market leadership. Additionally, the presence of major medical device manufacturers, continuous clinical innovation, and extensive surgeon training programs accelerate product adoption. Growing emphasis on infection control and outpatient surgical efficiency is also reinforcing demand for single-use automated suturing devices.

Europe Automated Suturing Devices Market Trends

Europe automated suturing devices market is expected to grow steadily, supported by increasing surgical volumes and rising adoption of minimally invasive techniques across major countries such as Germany, the U.K., France, Italy, and Spain. The region benefits from well-established hospital infrastructure, strong regulatory oversight, and early adoption of advanced surgical technologies focused on patient safety and procedural efficiency. Automated suturing devices are gaining traction in cardiac, gastrointestinal, and gynecological surgeries due to their ability to deliver consistent closure outcomes and reduce operative variability.

European healthcare systems emphasize reduced surgical time, faster recovery, and lower complication rates, which align well with the clinical benefits of automated suturing solutions. The growing penetration of robotic-assisted surgery platforms and expanding day-care surgical centers are further supporting adoption. Additionally, strong clinical guidelines, high surgeon skill levels, and increasing investments in surgical innovation are encouraging hospitals to integrate disposable and reusable automated suturing devices. Regulatory focus on biocompatibility and infection prevention continues to shape product development across the region.

Asia Pacific Automated Suturing Devices Market Trends

The Asia Pacific automated suturing devices market is expected to register a relatively higher CAGR of around 7.7% between 2026 and 2033, driven by rapidly expanding surgical volumes across China, India, Japan, and Southeast Asia. The rising prevalence of cardiovascular diseases, gastrointestinal disorders, and trauma-related injuries is increasing demand for surgical interventions, thereby boosting the adoption of automated suturing technologies. Improving hospital infrastructure, expanding access to minimally invasive surgery, and increasing the availability of trained surgeons are accelerating market growth.

Governments across the region are investing heavily in healthcare modernization, tertiary care expansion, and surgical capacity building, creating a favorable environment for advanced medical devices. Local manufacturers are offering cost-effective automated suturing systems, improving affordability and penetration in price-sensitive markets. Additionally, growing medical tourism, increasing insurance coverage, and rising awareness of surgical efficiency benefits are driving adoption. The shift toward disposable devices for infection control and outpatient procedures further enhances long-term growth prospects in the region.

Competitive Landscape

The global automated suturing devices market is highly competitive, with leading players such as Johnson & Johnson, B. Braun Melsungen AG, Demetech Corporation, Conmed Corporation, and W.L. Gore & Associates leveraging strong surgical portfolios, extensive hospital and ambulatory surgery center distribution networks, and continuous innovation in minimally invasive and robotic-assisted surgical procedures. Market participants are focusing on advanced automated suturing platforms, disposable and single-use systems, ergonomic handheld designs, and enhanced stitch precision to improve operative efficiency, reduce closure time, and ensure consistent wound approximation outcomes.

Companies are increasingly advancing motorized actuation mechanisms, improved needle control and tension regulation, compatibility with laparoscopic and robotic systems, and biocompatible suture materials to support complex cardiac, gastrointestinal, orthopedic, and gynecological procedures. Additionally, manufacturers are investing in infection-control compliant disposable formats, compact device designs for outpatient settings, surgeon training programs, and cost-effective suturing kits to expand adoption across hospitals, high-volume surgical centers, and emerging markets.

Key Industry Developments:

- In December 2025, Nitinotes Ltd., an early commercial-stage medical technology company developing fully automated endoluminal suturing solutions for obesity treatment, announced the successful treatment of the first patient in its U.S. Investigational Device Exemption (IDE) EASE™ Clinical Trial. The trial is evaluating the EndoZip™ Automated Suturing System for use in endoscopic sleeve gastroplasty (ESG). The inaugural procedure was performed at Lenox Hill Hospital | Northwell Health in New York, NY, marking the activation of the study’s first U.S. clinical site.

- In November 2025, Nitinotes Ltd., a medical device company focused on advancing obesity treatment, announced that it received CE Mark approval for the EndoZip™ System, the first fully automated suturing platform designed for endoscopic sleeve gastroplasty (ESG). This regulatory milestone allows Nitinotes to initiate commercialization across the European Union and other markets that recognize CE Mark certification.

Companies Covered in Automated Suturing Devices Market

- Johnson & Johnsons

- B. Braun Melsungen AG

- Demetech Corporation

- Conmed Corporation

- W.L. Gore & Associates

- Boston Scientific

- 3M Healthcare

- Medtronic Inc.

- Healthium MedTech

- Peters Surgical

- Surgical Specialties Corporation

- Others

Frequently Asked Questions

The global automated suturing devices market is projected to be valued at US$ 3.8 Bn in 2026.

Rising volumes of minimally invasive and robotic-assisted surgeries, combined with demand for faster wound closure, procedural consistency, and reduced surgeon fatigue, are driving the adoption of automated suturing devices globally.

The global automated suturing devices market is poised to witness a CAGR of 5.7% between 2026 and 2033.

Expanding ambulatory surgical centers and increasing penetration of disposable, single-use automated suturing systems in emerging markets present significant growth opportunities.

Johnson & Johnsons, B. Braun Melsungen AG, Demetech Corporation, Conmed Corporation, and W.L. Gore & Associates are some of the key players in the automated suturing devices market.