- Medical Devices

- Automated Liquid Handling Technologies Market

Automated Liquid Handling Technologies Market Size, Share, and Growth Forecast, 2025 - 2032

Automated Liquid Handling Technologies Market By Product Type (Automated Liquid Handling Workstations, Others), Application (Drug Discovery & ADME-Tox Research, Others), End-user, and Regional Analysis for 2025 - 2032

Automated Liquid Handling Technologies Market Size and Trends Analysis

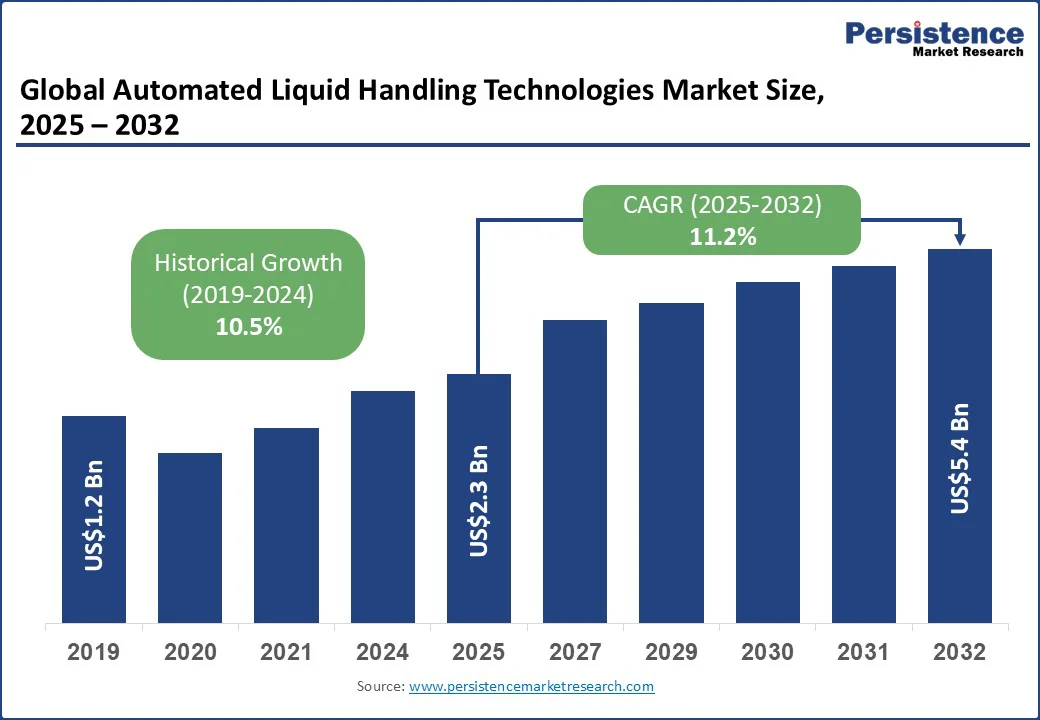

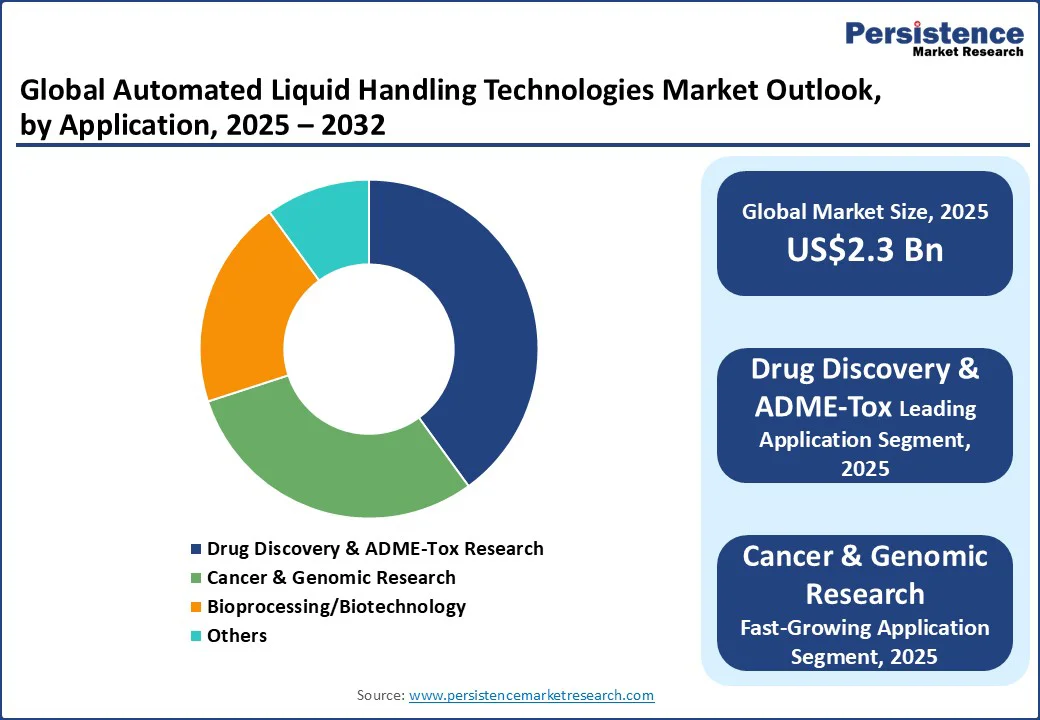

The global automated liquid handling technologies market size is likely to be valued at US$2.3 Bn in 2025 and is expected to reach US$5.4 Bn by 2032, growing at a CAGR of 11.2% during the forecast period from 2025 to 2032, driven by the introduction of novel automated liquid handling workstations for non-contact dispensing.

Key Industry Highlights:

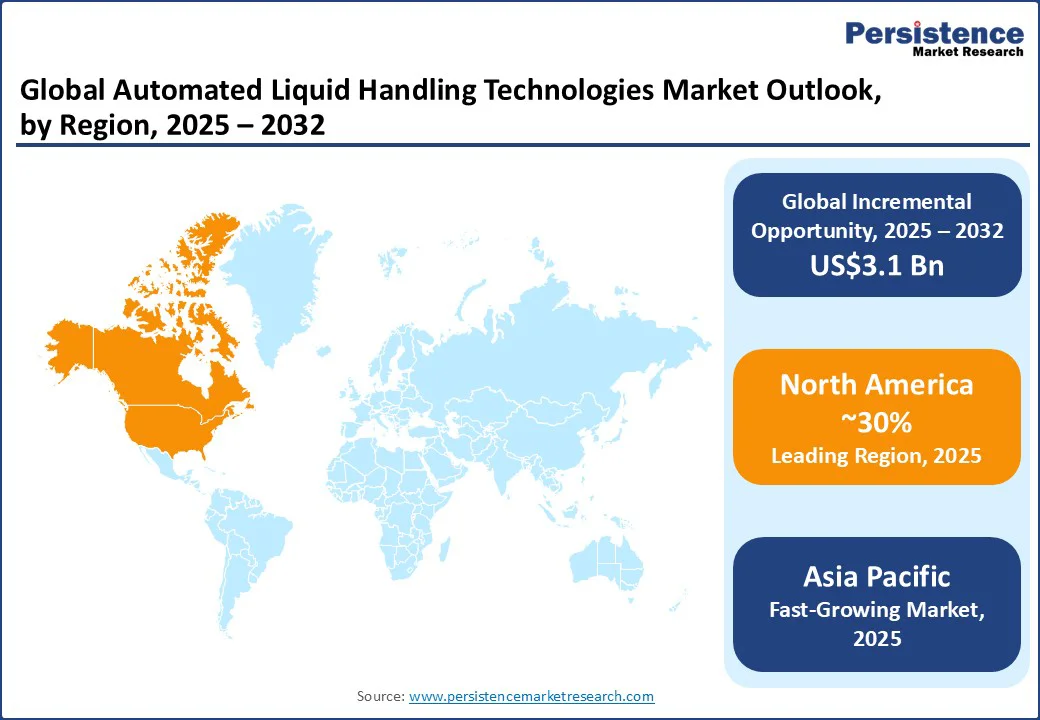

- Leading Region: North America, accounting for over 30% share in 2025, driven by the strong biotechnology and pharmaceutical sectors, which increasingly rely on advanced automation solutions to support drug research and discovery.

- Fastest-growing Region: Asia Pacific, projected CAGR of 12.2% from 2025 to 2032, fueled by the rapid rise of biopharma and biotechnology sectors, alongside the growing role of Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs) in countries such as China, India, and Japan.

- Dominant Product Type: The automated liquid handling workstations segment holds the largest share of over 57.3%, driven by increasing competition among pharmaceutical companies and their pursuit of new, effective drug treatments.

- Application Type: The drug discovery segment is projected to capture the largest share of the liquid handling system market during the forecast period, driven by rising investments in new therapeutic development.

- Import–Export Scenario: The import–export scenario for the automated liquid handling technologies market reflects strong cross-border trade, with developed regions including North America and Europe exporting advanced systems. At the same time, Asia Pacific drives imports to support its rapidly expanding biotech and pharmaceutical sectors. Rising collaborations and globalized R&D further enhance technology transfer and market integration.

|

Key Insights |

Details |

|

Automated Liquid Handling Technologies Market Size (2025E) |

US$2.3 Bn |

|

Market Value Forecast (2032F) |

US$5.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

11.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

10.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Investments in Drug Development and Research

As the number of patients increases worldwide, healthcare research is also expanding to meet growing medical needs. Automated Liquid Handling Technologies (ALH) has significant potential in biopharmaceutical and pharmaceutical companies, as well as R&D labs. Furthermore, the desire for better healthcare necessitates the conduct of healthcare research. As a result, governments around the world intend to focus their expenditure on healthcare research to meet patient needs for superior and more sophisticated technology, while maintaining quality standards.

The growing expenditure on R&D, increase in funds for drug development, growing need for high-output testing, and rising implementation of automation in various clinical trials are the primary factors propelling the growth of the automated liquid handling system industry. Moreover, growing R&D activities for new drug development and biotech research are boosting market growth.

In 2022, the U.K. government ensured that the NHS delivers new treatments to patients faster and supports more diverse and inclusive clinical research to tackle health inequalities and improve patient care. €200 Mn (US$234 Mn) of the funding will be used to invest in digital capabilities in clinical trial services and help researchers better access NHS data through trusted research environments.

High Cost of Liquid Handling Systems Solutions

The high cost of liquid handling systems remains a major restraint on market growth, particularly for small and medium-sized laboratories. These systems require significant upfront investments, with advanced models often priced in the hundreds of thousands to millions of dollars. Beyond the purchase price, ongoing expenses such as maintenance, software updates, and servicing add to the total cost of ownership, further straining laboratory budgets.

This financial burden makes adoption challenging for institutions with limited resources, especially when the return on investment is not immediately measurable. As a result, many labs continue relying on manual processes despite the efficiency and accuracy offered by automation. Prices vary widely by manufacturer and specifications, with Hamilton systems, for example, ranging from US$100,000 to US$2 2 Mn depending on specifications.

Rising Development Activities in Pharmaceutical and Biotech Industries

As per the Pharmaceutical Research and Manufacturers of America (PhRMA), U.S. companies are world leaders in the R&D of pharmaceuticals and own most of the intellectual property rights for new drugs. The biopharmaceutical sector has brought to the market over 5,000 new medicines in the world, with some 3,400 compounds under development in the U.S. At the same time, emerging economies such as India and China are actively building their pharmaceutical and biotech industries. According to the India Brand Equity Foundation (IBEF), India provides more than 50% of the world's demand for different vaccines, 40% of the demand for generics in the U.S., and 25% of the overall medicines consumed in the U.K. Moreover, India has the second-largest pharmaceutical and biotech workforce in the world.

In China, state efforts are propelling industry development. Biotechnology is named a leading sector in the country's 13th Five-Year Plan and the Made in China 2025 initiative. Such programs incorporate concrete 5- and 10-year objectives for indigenous drug manufacturers. The swift advancement of the pharmaceutical industry clusters in India and China has led to an increase in quality control, research, and drug development labs. This trend will soon open up great opportunities for lab automation companies.

Category-wise Analysis

Product Type Insights

The automated liquid handling workstations segment is anticipated to hold the largest share of over 57.3% in 2025. Automated liquid handling workstations can be further classified based on their assembly and type. The growing competition among pharmaceutical companies and their pursuit of new drugs to treat diseases effectively drives the adoption of automated workstations. The small footprint and ability to increase with other devices with nanoliter capabilities contribute to higher market penetration of standalone pipettors.

The reagents and consumables segment is expected to showcase lucrative growth from 2025 to 2032. As the adoption of automated liquid handling systems increases across pharmaceutical, biotechnology, and research sectors, there is a corresponding rise in demand for compatible reagents and consumables. These essential components, including specialized pipette tips, plates, and liquid handling cartridges, play a crucial role in ensuring the accuracy and reliability of automated processes.

Application Insights

The drug discovery segment is projected to capture the largest share of the liquid handling system market during the forecast period, driven by rising investments in drug discovery and development. This growth is further supported by the critical role of drug discovery in sample preparation, assay setup, high-throughput screening, in vitro experiments, cellular assays, and in vivo toxicity studies.

Automated liquid handling workstations play a crucial role in various applications within drug discovery and ADME-Tox, such as stepwise serial dilution across a broad concentration range, compound selection and transfer for retesting, and confirmatory and further analysis. Major applications in this domain involve plate replications, plate-to-plate dilutions, and plate reformatting. A significant advantage of employing automated liquid handling platforms in drug discovery is their capability to seamlessly integrate various types of liquid handlers and stackers, enhancing overall throughput.

Regional Insights

North America Automated Liquid Handling Technologies Market Trends

In 2025, North America is expected to lead, accounting for a market share of around 30%. This dominance is primarily driven by the strong biotechnology and pharmaceutical sectors, which increasingly rely on advanced automation solutions to support drug research and discovery. Significant investments in research and development, coupled with the growing importance of precision medicine and personalized healthcare, are further fueling adoption. In the U.S., market expansion is supported by the rising incidence of cancer and favorable reimbursement programs that encourage advanced diagnostic and treatment approaches.

Additionally, organizations such as the American Cancer Society, the American Breast Cancer Foundation (ABCF), and the Esophageal Cancer Awareness Association (ECAA) are actively implementing initiatives to aid patients, caregivers, and survivors. On the funding front, the Further Consolidated Appropriations Act, 2024 (H.R.2882) allocated US$7.22 Bn to the National Cancer Institute (NCI), marking a US$120 Mn increase over the interim budget. However, overall funding reflects a US$96 Mn net decrease from FY 2023.

Asia Pacific Automated Liquid Handling Technologies Market Trends

Asia Pacific is projected to record the fastest growth in the automated liquid handling technologies market during the forecast period. This expansion is fueled by the rapid rise of biopharma and biotechnology sectors, alongside the growing role of Contract Research Organizations (CROs) and Contract Development and Manufacturing Organizations (CDMOs) in countries such as China, India, and Japan. These nations are making substantial investments in omics research, advanced healthcare, microbiology, drug discovery, and clinical diagnostics, which is significantly boosting demand for automation technologies. India has been strengthening its biotechnology ecosystem with strong government support.

The Department of Biotechnology (DBT) has funded nine biotech parks, while BIRAC has supported sixty bio-incubators across the country. In the Interim Budget 2024–25, DBT received INR 22,515.2 Mn (US$271 Mn). Additionally, the National Biopharma Mission is sponsoring 101 projects involving MSMEs and NGOs, while the National Biotechnology Development Strategy 2020–25 provides a roadmap for fostering innovation, talent, and collaboration.

Competitive Landscape

The global automated liquid handling technologies market is focusing on advancing its research and fast-tracking the development of new automated liquid handling technologies to launch new products and gain a competitive advantage over other market players.

Major players are investing in expanded production capacity to increase their market share. Market expansion is expected to be driven by the increasing number of partnerships and collaborations among key players aiming to strengthen their market presence. The U.S. is home to key industry players, including major entities such as Thermo Fisher Scientific, Inc., Agilent Technologies, Inc., Danaher, and PerkinElmer, Inc., playing a significant role in the sector and contributing to advancements and innovation. These companies have a strong geographical foothold and are at the forefront of technological advancements, which has helped them maintain a high market position.

Key Industry Developments

- In September 2023, Eppendorf launched its epMotion range of automated liquid handling systems, marking a significant advancement in the field. In a landmark move, SLS secured exclusive distribution rights for this highly anticipated product line.

- In June 2023, Agilent Technologies Inc. launched the BioTek 406 FX Washer Dispenser, a compact device featuring plate washing and multifunctional reagent dispensing capabilities.

Companies Covered in Automated Liquid Handling Technologies Market

- Agilent Technologies

- Aurora Biomed, Inc.

- AUTOGEN, INC.

- Danaher

- BioTek Instruments, Inc.

- Analytik Jena AG

- Corning Incorporated

- Eppendorf AG

- Formulatrix, Inc.

- Gilson, Inc.

- Hamilton Company

- Hudson Robotics

Frequently Asked Questions

The automated liquid handling technologies market is estimated to be valued at US$2.3 Bn in 2025.

A key demand driver for the automated liquid handling technologies market is the growing need for high-throughput, accurate, and contamination-free sample preparation in life sciences research, clinical diagnostics, and drug discovery.

In 2025, the North America region will dominate the market with an exceeding 30% revenue share in the automated liquid handling technologies market.

Among the product types, automated liquid handling workstations hold the highest preference, capturing beyond 57.3% of the market revenue share in 2025, surpassing other products.

The key players in the automated liquid handling technologies market include Agilent Technologies, Aurora Biomed, Inc., AUTOGEN, INC., Danaher, and Analytik Jena AG.